SWBI - Smith & Wesson: A Solid Long-Term Investment With Some Short-Term Headwinds

2023-10-06 17:47:28 ET

Summary

- From a long-term perspective and even under a conservative set of assumptions SWBI should prove a profitable investment.

- But the latest downturn in firearm background checks with still elevated inventory levels increases the possibility of disappointments for the next two quarters.

- With those short-term headwinds and the stock trading near 52 weeks high there should be some better entry points in a couple of months.

I have been following Smith & Wesson Brands, Inc. ( SWBI ) for a couple of years and as of today my perspective on the company is very different depending on what is your investment horizon. From a long-term perspective, this should be a solid investment even under conservative assumptions but from a more short-term perspective I think that most of the near-term catalysts are negative, pointing to the likelihood of better entry points in the near future. So, through this article, I would try to flesh out those differing short and long-term perspectives with the objective of providing a solid thesis that can be of help to potential and current investors in this name.

The Short Term

My first SA article was on SWBI . In that article, I tried to focus mainly on the cyclicality of the industry marked by the ups and downs in the background check statistics that the FBI reports on a monthly basis, probably the most important variable to track in the industry.

In hindsight, I was clearly early in my recommendation as this last cycle has been much larger than previous ones, especially the downturn as you can see in this next table.

FBI monthly NICS

And this last one still has not given many signs of being over.

By the end of 2022 and early 2023, we saw a few positive readings on reported NICS after more than a year of steep monthly down readings. After that, April and May's readings made me hopeful that perhaps the next up cycle was starting with sequential readings of +5% and +9%. But after that, we have seen 4 months of steep reductions of around 15% over readings that were already depressed versus the peak of a couple of years ago.

One caveat regarding this set of statistics is that the company uses an adjusted version reported by the NSSF , undoubtedly that's a more refined reading of final demand, but I do not have access to that data set, and the figures as reported by the FBI do a pretty fine job tracking the financial evolution of the company.

One other important thing to have in mind regarding the implication of the evolution of the reported NICS figures is to understand that those are readings that can be interpreted as a proxy of final demand experienced by the distribution channel. And that demand affects SWBI with a lag as inventory in the distribution channel adapts to the ups and downs of demand. So usually, the quarterly evolution of the company's results reflects final demand (NICS) of one to two quarters in the past. And the following chart does a good job of reflecting that lagged effect.

FBI monthly NICS and SWBI SEC Filings

{kind=link}

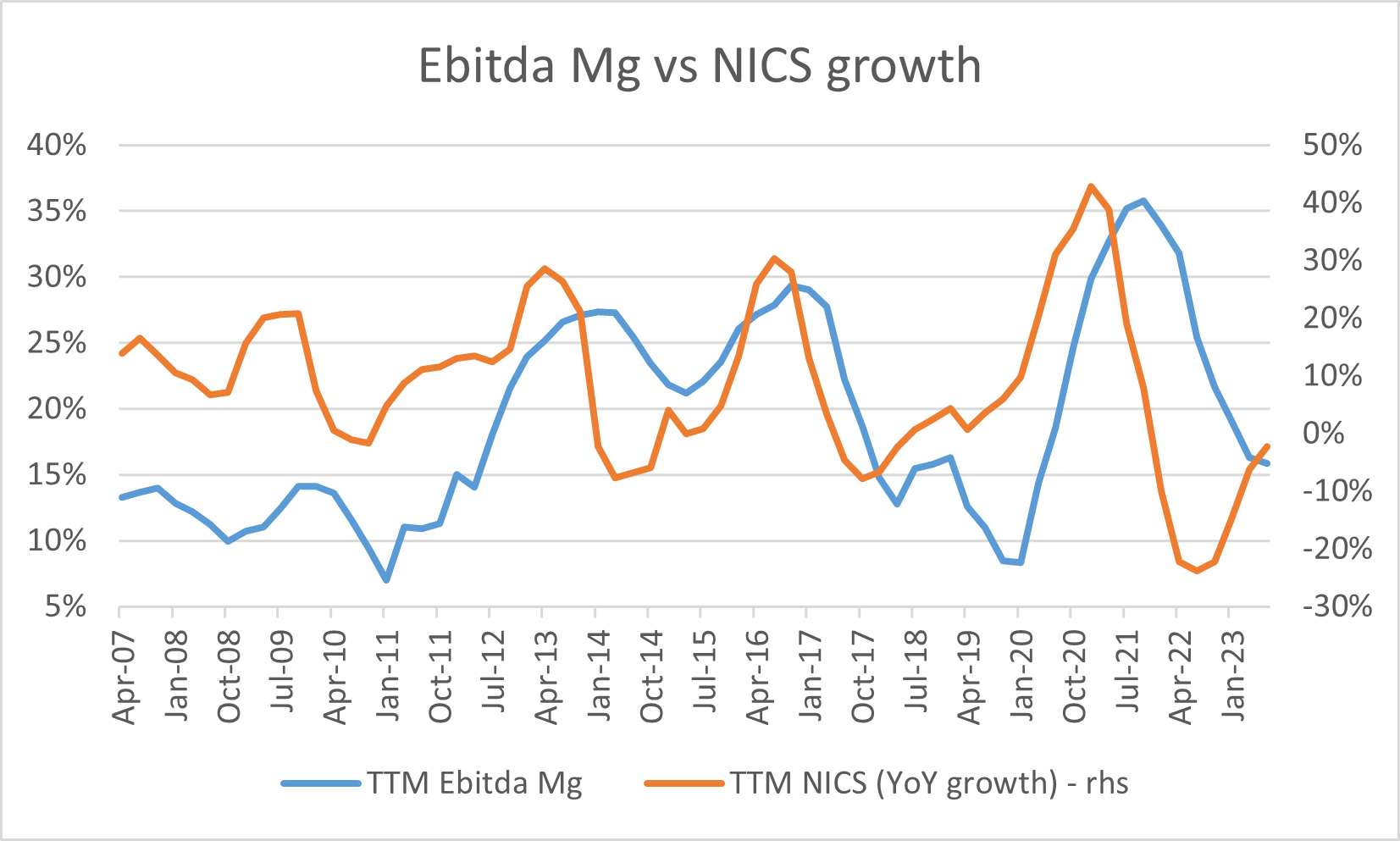

As you can see, when the downturn starts, the distribution channel usually is unprepared and they get clogged with inventory, that clogged inventory reduces orders to the manufacturer that also starts to accumulate inventory requiring a more promotional environment that negatively affects margins. And the opposite happens when an upturn occurs as the distribution channel is prepared for a more subdued level of demand, they exhaust their inventory and a flurry of orders hits the manufacturers reducing or even eliminating the need for promotional activity positively affecting margins.

One other important insight to get from that chart is to understand that usually, the company is unable to hold on to operating margins as it faces a downturn in demand (lagged by one or two quarters) so the next one or maybe even two quarters should reflect the sharp reduction on final demand that we have seen from June to September.

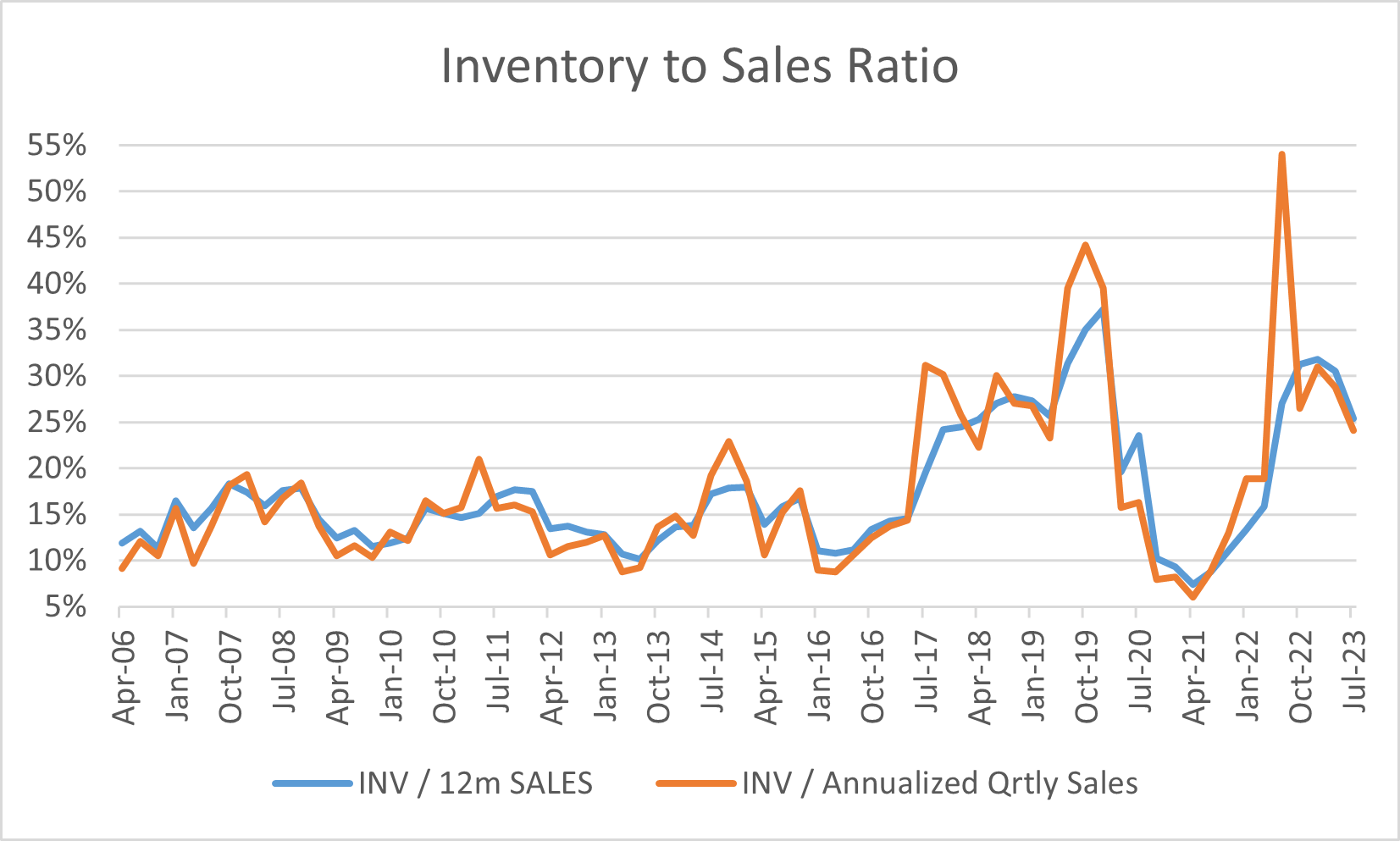

That should be worrying considering that inventories are still elevated from an historical perspective even when looked through the lenses of trailing sales that are higher than the ones that should be expected for the next one or two quarters.

{kind=link}

The company has stated in the past few earning calls that they are purposefully running higher inventories as a precaution during their relocation to Tennessee but unless that implies that a significant manufacturing downtime is coming or is happening at this time, that inventory is still going to be there and will need to be moved through a distribution channel that is facing lower levels of demand.

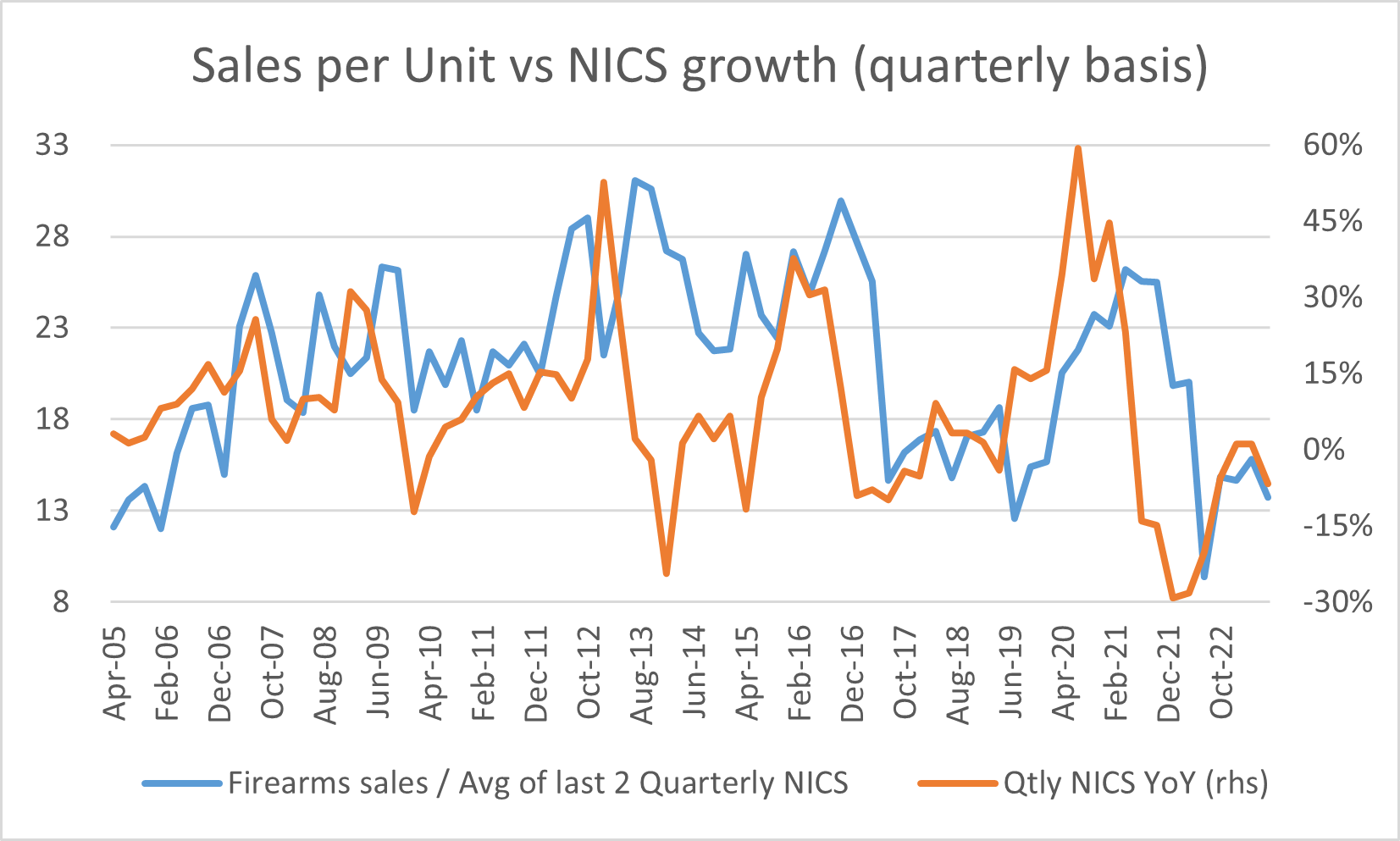

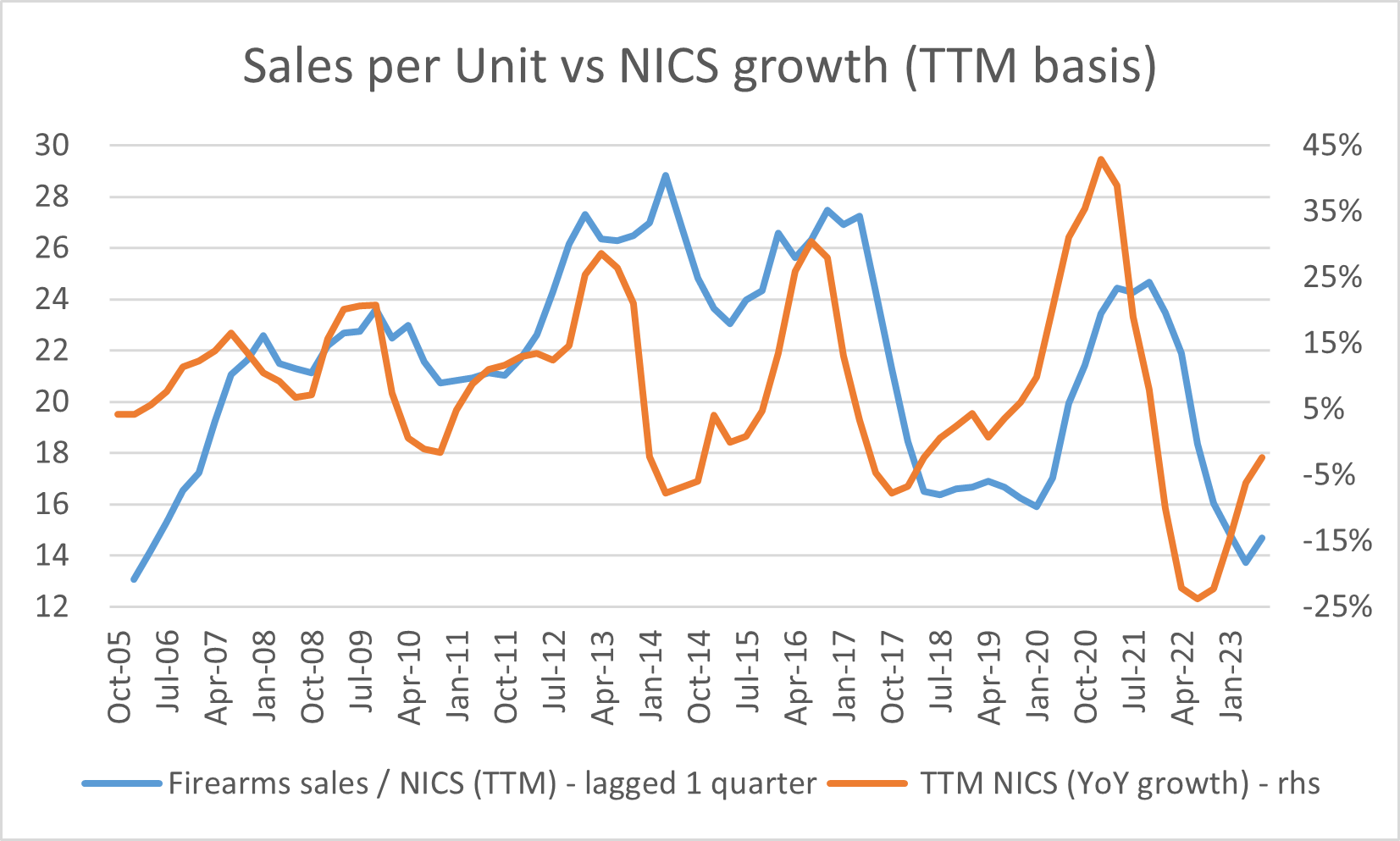

So, the short-term risk relates to the next two quarters considering that the stock is trading near its 52-week high, and now I will try to explain my thinking starting with the relationship of firearms sales to NICS ratio and the NICS growth rate.

FBI monthly NICS and SWBI SEC Filings FBI monthly NICS and SWBI SEC Filings

{kind=link}

{kind=link}

On those charts, you can see that as NICS contract or expand, the promotional environment is reflected by the ratio of firearm sales to NICS. The TTM basis chart is clear and very smooth and obviously, the quarterly one is noisier, but the relationship is clear: As NICS expand the proxy of sales per unit increase and the opposite occurs when NICS contract.

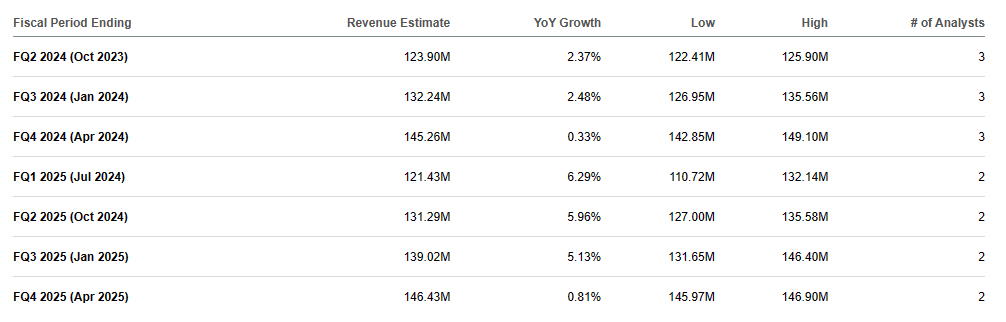

Looking forward, as NICS contract is hard to see sales per unit increase so I will assume the average of the last 4 quarters for that ratio to project firearm sales. As I am using the average NICS of the last two quarters for the sales per unit ratio, the following table shows the relevant months to project firearms sales for the next two quarters with my assumptions marked in light orange.

FBI monthly NICS and author assumptions

Under those assumptions, I get to firearms sales of $98.8 and $108.6 million respectively, and to those, we need to add the sales of Other Products & Services to get to total net revenues. For that category of revenue, I will assume the same amount recorded for the same quarter of the previous fiscal year. Those revenues have been contracting at an average YoY rate of 18%, so it's not a particularly conservative assumption.

With all of that, I get to total revenues of $109.8 and $120.4 million for the next two quarters, figures that are roughly 10% below the estimates for the next two quarters that you can find on SE as of October 5, 2023.

{kind=link}

To end the short-term section of the article it's important to point out that the company should be ending the investment period related to their relocation to Tennessee in the 2nd quarter of the current fiscal year, giving management more flexibility to return capital to investors. And even though that is great, I think it might already be priced in as the company recently announced the approval of a share repurchase authorization of $50 million and, as I already stated, the company is trading near its 52-week high in an adverse financial market environment and without any reignition of the firearms cycle.

Now let's move to the other side of the coin.

The Long Term

From the perspective of a long-term investor, a DCF under a set of conservative assumptions that provide a sufficient margin of safety, should be appropriate to assess the likelihood of obtaining an attractive return from an investment in SWBI.

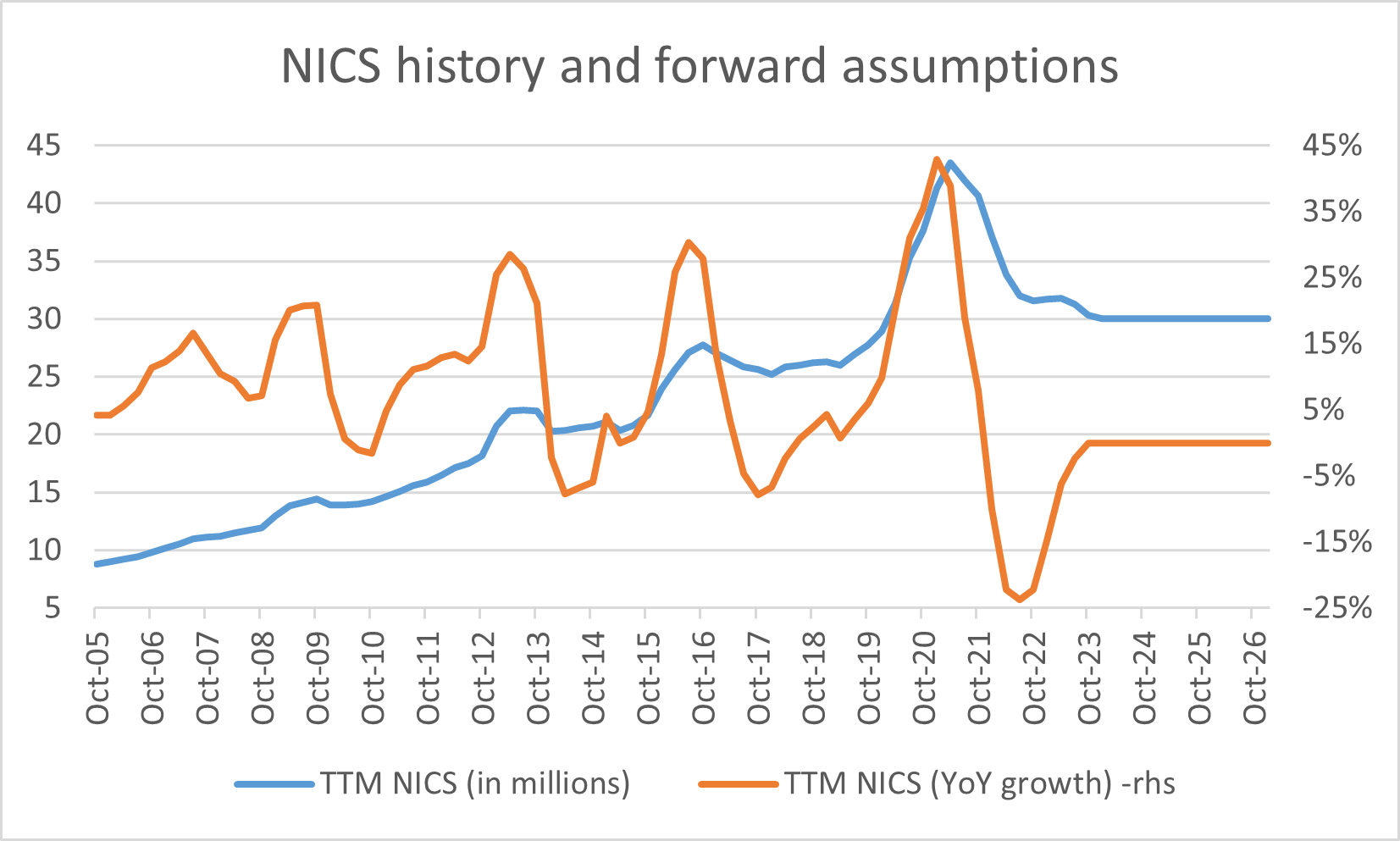

For that, I will start with the same set of short-term NICS assumptions detailed in the previous section and after that, I would assume a stabilization and zero growth going forward. The following chart shows how that assumption looks from an historical perspective.

FBI monthly NICS and author assumptions

{kind=link}

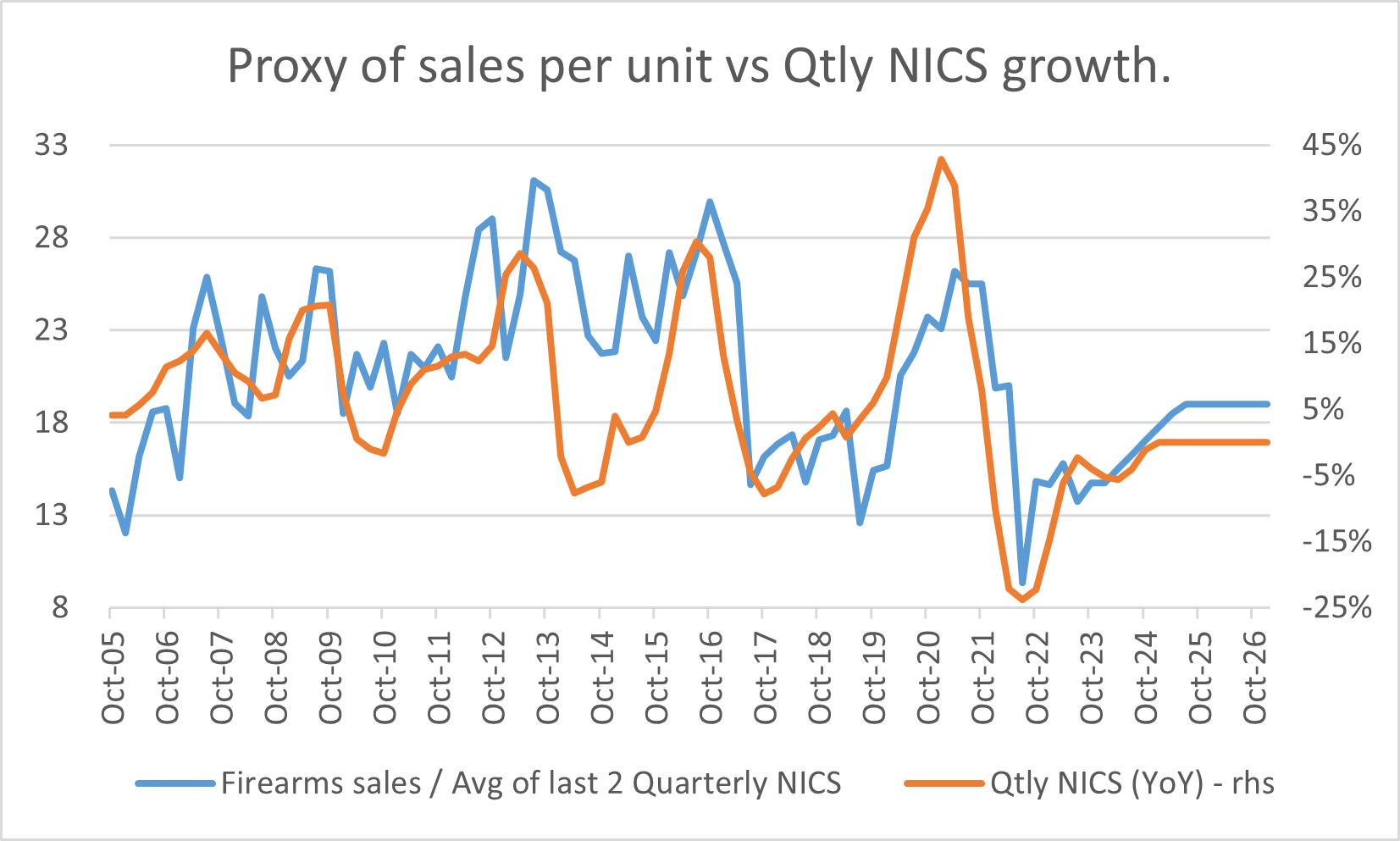

With the expected stabilization of final demand, the promotional activity should slowly move to a more average level and that would be reflected in my projections of the proxy of sales per unit as reflected in the next chart.

FBI monthly NICS, SWBI SEC filings and author assumptions

{kind=link}

The final level for that ratio (proxy of sales per unit) will stand at 19 (SWBI sales per NICS) according to my assumptions while the historical average stands closer to 21.

Under those assumptions, TTM sales bottom at around $486 million three quarters from now and then slowly pick up reaching a level of $570 million by the quarter ending on April 30, 2026. After that, revenues stay at that level for the window of projection.

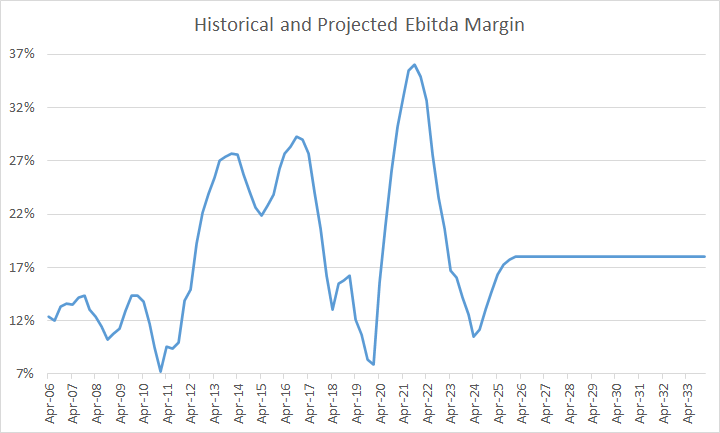

After that, we move to the assumption for EBITDA margin. I am working with quarterly data for the company starting in calendar 2006 and the quarterly EBITDA margin has moved widely from a low of -0.9% to a maximum of 39.1% as the company moves around the cycle. The average during that period has been 19% and the average of the last 10 years stands at 22%.

It's important to point out that the company in the past delved into a few different businesses before focusing exclusively on the manufacturing and sale of firearms, I covered that theme in my initial article, so I won't do it again here. But all of those on average were less profitable than their main business, so those averages probably would have been higher if the company stayed always focused only on their bread and butter as they are doing now.

TTM EBITDA margins stand at 16% and my assumptions would have that margin bottoming at around 10.5% and then slowly increasing and stabilizing by the first calendar quarter of 2026 at a level of 18% and staying at that level for the window of projection.

SWBI SEC filings and Author projections

{kind=link}

For capex, I am assuming a final elevated amount for the coming quarter with an investment of $28 million and then stabilizing at the same level of depreciation at 6% of sales. I think that after this latest period of elevated CAPEX for the relocation to Tennessee, we might experience a period of depreciation being higher than capex, but that won't go into the projection with the idea of maintaining a conservative approach.

Tax rate would be 24%, slightly above the average since Trump's tax cuts.

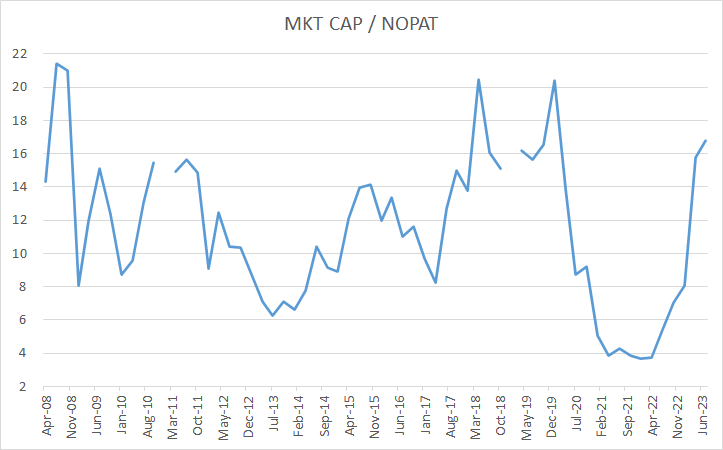

So, finally, we need an appropriate discount rate and an exit multiple. As I am working with an FCF to the firm model, the closest thing to an appropriate multiple would be the historical ratio of Market Cap to NOPAT. That is assuming that CAPEX is roughly equal to depreciation, something that is very close to what I see in SWBI's financial statements when looking at a long enough window of time (10 years or more). And that ratio looks like this from an historical perspective.

SWBI SEC filings and historical stock prices from Excel historical price function

{kind=link}

The average stands at 11.47 times, which seems a little high for me to really feel that I am working with a sufficient margin of safety. So, to err on the conservative side I will be using 9 times as the assumption for the DCF.

The final required assumption is the discount rate and for that, I have historically used 10% as a personal benchmark, but with the latest jump in long-term rates I would say that something a little higher would be appropriate, so I will be using 11%. That is an entirely debatable assumption but a somewhat conservative one in my opinion as the beta of this stock stands at 0.5 according to MarketWatch .

With all those assumptions I get to an upside of 39% from today's market price of $13.3.

It's obvious that things won't go as I am assuming quarter by quarter because the cycles in the industry will probably continue, but all my expectations (EBITDA margin, proxy of sales per unit, zero long-term NICS growth) are in my opinion on the lower side of what we would probably see on average looking forward.

Conclusion

Today I do not hold any shares in the company as the stated short-term risks weigh on me, especially with the stock trading close to its 52-week high, but at the same time, it's very hard for me to see the stock being a poor investment for a long-term investor. So, in the end, each investor can make up his own mind, buy the stock right now as a solid long-term investment, or wait for a better entry point if you as I think that the next few earning releases should bring better entry points.

Thanks for reading, hope this article was informative, and good luck with your investments.

For further details see:

Smith & Wesson: A Solid Long-Term Investment With Some Short-Term Headwinds