SWBI - Smith & Wesson: Rating Downgrade To Buy Due To Longer-Than-Expected Pressure

2023-12-08 11:36:05 ET

Summary

- Smith & Wesson's Q2 earnings show an increase in net sales but a decrease in gross profit margin due to higher costs.

- The company bought back shares but the number of outstanding shares did not decrease significantly.

- Relocation costs and temporary margin issues have taken longer than expected, but management expects gross margins to improve in Q4.

Thesis

Smith and Wesson is one of my highest conviction picks as normalized FCF post-relocation could be used to reward shareholders as management has indicated several times. In my last article , I outlined what this might look like.

However, due to the longer than expected slump, I have to downgrade Smith & Wesson from a Strong Buy to a Buy. I still like the prospects once the move is complete, but unfortunately the costs are dragging on and the debt reduction is taking longer than expected. So a small downgrade should be justified.

SWBI'S Q2 Earnings

{kind=link}

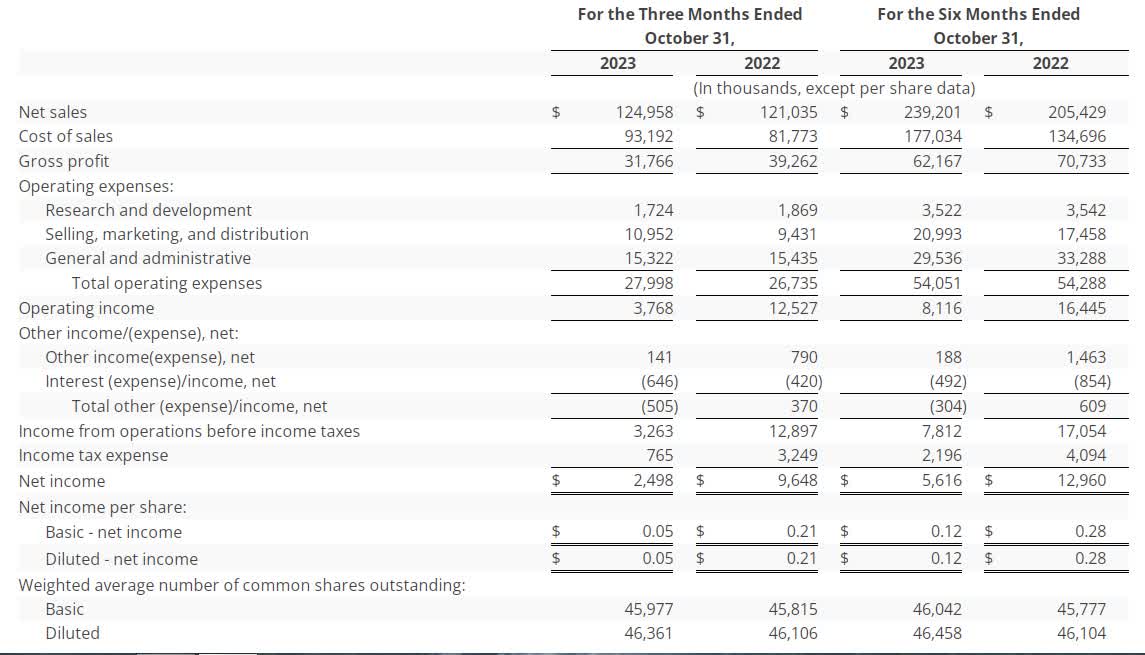

Net sales increased 3.2% year over year to $124.9 million, an increase of $3.9 million. Unfortunately, due to a combination of factors, cost of sales increased even more, resulting in a gross profit margin of 25.4%, 4.4% lower than last year. However, part of this was due to a one-time legal settlement of $3.2 million. And the other part of the cost increase is due to inflation, lower production levels and inventory adjustments.

But even if we look at the H1 numbers, we see that the increase in cost of sales is greater than the increase in revenue, and selling, marketing and distribution costs are also up. On the other hand, income expenses decreased from -854 to -492 in H1, which is a positive sign.

One piece of news that investors liked was that they announced a $50 million share repurchase program, of which they used $8.2 million in the quarter, buying back 646,000 shares at an average price of $12.70. However, if you look at the weighted number of shares outstanding, it is higher than last year, so even after they bought back that much, the number of shares outstanding did not go down. Of course, these are weighted numbers, but I would have thought we would have seen a bigger change. Especially as SBC expenses for H1 are almost as high as in H1 last year, namely 2,759 vs. 2,605.

{kind=link}

The relocation costs are down this quarter, but if we compare H1 24 to H1 23, the costs are slightly higher and there is still about $25 million to $30 million of costs left according to Smith & Wesson's guidance. Unfortunately, the relocation costs have taken longer than expected and the temporary margin issues have also taken longer than expected. However, management said that gross margins will most likely return to the low 30s in Q4.

{kind=link}

FCF is still negative at -$29 million in H1, but is a strong improvement compared to last year's H1. Payments for the acquisition of property, plant and equipment were $66m in H1 23 compared to $39m last year, and this is most of the net cash used in investing activities, which has the most impact on FCF this year. I expect the fourth quarter to be FCF positive and the next fiscal year to be strongly FCF positive, if the "temporary" costs do not last longer than expected now.

Smith & Wesson Earnings Call Q2

Smith & Wesson's management is pleased with the quarter as they are increasing sales and shipments while distributor inventory is down and Smith & Wesson is outperforming NICS by 7%+ indicating they are gaining market share from the competition.

In addition, new products are a key revenue driver, accounting for 29% of total revenues in Q2 and 31% in H1. Furthermore, Smith & Wesson received two "Innovator of the Year" awards from Guns & Ammo Magazine and NASGW.

The opening of the new headquarters in Tennessee was a success, with production up and running and 300 employees on site. However, as we already know, there will be further relocation costs, and therefore the date for becoming debt-free has shifted slightly from the end of the fiscal year to somewhere between April and December 2024. It could happen in April, but Q2 is the target where they want to be debt free.

They ended the quarter with $44.2 million in cash and cash equivalents, paid $5.5 million in dividends, and expect H2 to be much better than H1 in terms of sales and cash generation with the upcoming holiday season. Further share repurchases are possible, but debt reduction is a priority. However, when the time is right, shares will be bought back.

Conclusion

Given that H2 is typically the stronger half of the year and the holiday season is important, I can see a strong Q3 with perhaps even double-digit revenue growth. And the closer we get to a debt-free company generating positive free cash flow, the better for shareholders, as management could use the $80 million to $100 million in FCF next fiscal year to increase dividends and buy back shares.

Furthermore, an EV/EBIT of about 13x is cheap and multiple expansion once the company is no longer completely under the radar is within the realm of possibility. In a boom phase, the multiple can also go into the 20s, as we saw in the period between 2018 and 2021. High barriers to entry, market share gains in recent quarters and a strong brand name are also factors that make Smith & Wesson special. In addition, there is the possibility that Smith & Wesson will become a stock cannibal, as another share repurchase program of the same magnitude could significantly reduce the share count over the next few years.

In the long run, I remain convinced that they will be winners and have only lowered the outlook because the period of pressure is unfortunately longer than originally thought. However, the upcoming elections, the easing of short-term pressures and a shareholder-friendly management should lead to a positive development of the stock in the long term.

For further details see:

Smith & Wesson: Rating Downgrade To Buy Due To Longer-Than-Expected Pressure