SMGKF - Smiths Group: Industrials With Potential For Improvement

2023-06-13 04:15:40 ET

Summary

- Smiths Group has the potential for improvement through product innovation and increased M&A.

- The company is in a commercially attractive position with low cyclicality, operating in industries with growth potential and a wide customer base.

- A premium valuation is warranted due to industry tailwinds, disposals at attractive valuations, and an improved outlook.

- We would like to see the current trajectory materialize, as although the premium is warranted, the further scope for upside looks unlikely.

Investment thesis

Our current investment thesis is that Smiths Group plc ( OTCPK:SMGKF ) has the potential for significant improvement. Industry tailwinds can be capitalized on through product innovation and increased M&A.

Organic growth is improving but near-term margin headwinds are minimizing outperformance.

Smiths is trading at a premium to its historical average. We see some justification for this but further upside looks unlikely.

Company description

Smiths is a global technology company that operates in various markets, including security and defense, industrial, energy, and space and aerospace.

The company is divided into four divisions:

- John Crane - providing mechanical seals, hydrodynamic bearings, power transmission couplings, and specialized filtration systems.

- Smiths Detection - specializes in developing sensors and systems for detecting explosives, narcotics, chemical agents, and other threats.

- Flex-Tek - offers engineered components that heat and transport fluids and gases for multiple industries.

- Smiths Interconnect - supplies specialized electronic devices, connectors, cables, and sub-systems for applications in various sectors.

Share price

SMIN's share price has generated soft returns across the last decade, when factoring in dividends, reflecting a period of underperformance for the business. Growth has been hard to come by despite numerous efforts.

Financial analysis

Smiths financials (Tikr Terminal)

{kind=link}

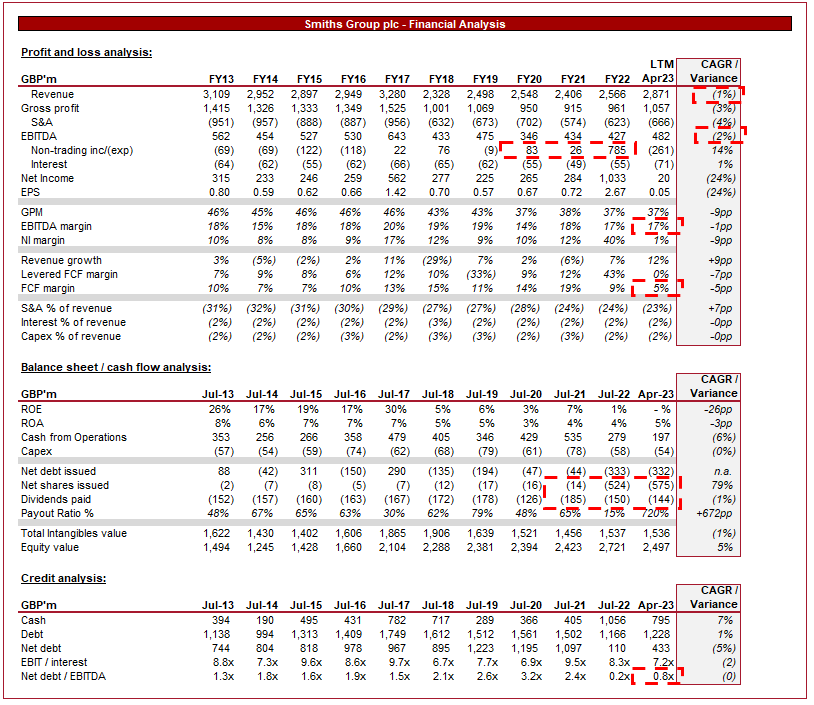

Presented above is Smiths' financial performance for the last decade.

Revenue & Commercial Factors

SMIN has experienced a decline in revenue at a rate of c.(1)% per annum. SMIN has struggled to achieve consistent growth during this period while disposing of several business segments.

The most recent of these disposals was the sale of its medical division for c.$2.4bn. Following this, Management distributed c.55% of the proceeds through share buybacks, choosing against the accumulation of funds.

SMIN has an attractive business model in our view. SMIN relies on innovation and engineering excellence to develop products and services which underpin the operational capabilities of a range of businesses.

Despite a lack of growth, SMIN continues to invest in R&D as a means of ensuring its products remain valuable to customers while also identifying new solutions. In recent years, the company has created a host of improvements, enhancing its value proposition.

Product development (Smiths Group)

{kind=link}

The company operates in economically important industries, such as energy, aviation, and HVAC. The benefit here is that demand is sticky and non-cyclical, allowing SMIN to benefit from greater certainty over revenue.

Further, many of these industries are experiencing wider tailwinds as technological development contributes to innovation. The biggest example of this is the energy transition to clean sources. The John Crane segment is winning several notable contracts, such as for hydrogen projects, a US CCUS contract with a supermajor, and the provision of dry gas seals in Canada. Additionally, we are seeing increased demand for security (and adjacent) support, as businesses expand their global footprint and require infrastructure improvement. This is to align with regulatory requirements, as well as to respond to more sophisticated threats. Interconnect is benefiting from Semiconductor demand. Finally, the Flex-Tek segment continues to see good innovation in the heating electrification market. In conjunction with clean energy, we are also seeing demand for low-emission electric heating solutions. Flex-Tek has also agreed on a partnership to launch the world's first large-scale low-emission steel production facility.

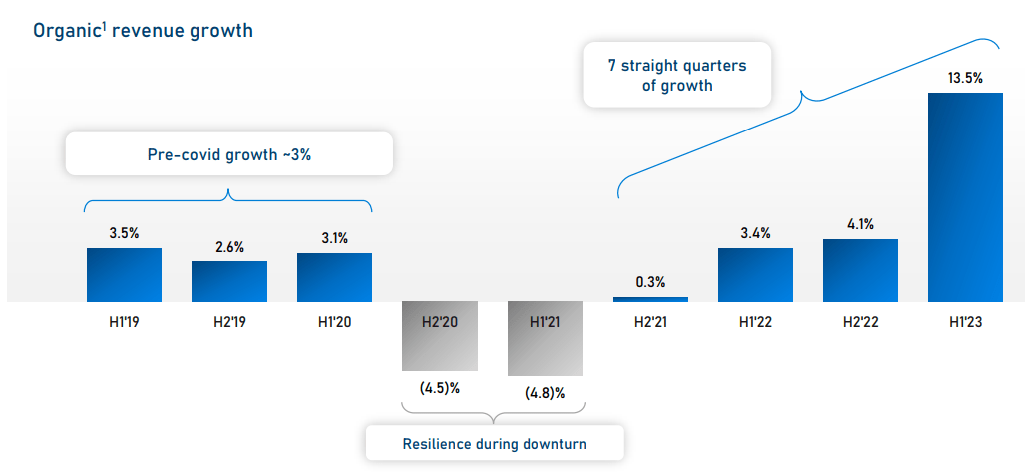

These factors are reflected in the company's organic growth, which has begun to improve. Although the sample size is small, the trajectory looks positive and in line with commercial improvement.

{kind=link}

Overall, we believe the company is in a commercially attractive position. When considering the several segments combined, SMIN has low cyclicality and is operating in industries with growth potential. Its customer base is wide and innovation remains strong.

Moat

SMIN's moat is the proprietary products and services the company has developed. Thus far, revenue implies the company's position remains robust, with underlying organic growth (revenue muddied by acquisitions and disposals). The concern is that R&D spending has not significantly increased, risking inferiority. More spending does not necessarily mean success, but the correlation is positive.

M&A

The biggest opportunity in our view is M&A. The company is positioned perfectly to conduct moderate-volume, low-value deals. The target would be to bolt on supporting businesses, as well as acquiring niches in similar industries. This will support growth and margins while maximizing the return on FCF.

We are slightly disappointed by the degree to which cash was distributed from the prior sale, as these funds could have been reinvested into the business.

Management state the M&A pipeline is strong but we would like to see efforts materially increase in this regard.

Margins

SMIN has good margins. It has a GPM of 37% and an EBITDA-M of 17%. The absolute high margins have been achieved through the quality of SMIN's products, allowing the business to demand a premium. The concern is that margins have seemingly slipped in recent years, partially impacted by the disposal of businesses. A portion of the margin slippage is due to supply chain issues and investment in R&D. Overall, we are not concerned about a material decline.

Balance sheet

SMIN is conservatively financed, with a ND/EBITDA ratio of 0.8x. Our view is that the company can push closer to 3x, owing to the sticky and non-cyclical nature of demand.

FCF has been stable across the historical period, allowing SMIN to invest consistently in both dividends and share buybacks. Our concern is that the current levels are unlikely to be sustainable, in conjunction with M&A and continued investment in R&D.

Outlook

{kind=link}

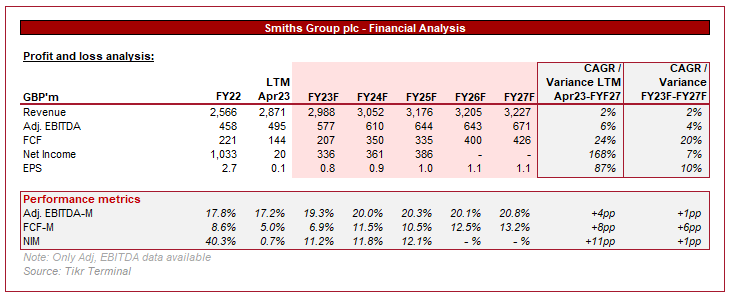

Presented above is Wall Street's consensus view on the coming 5 years.

Growth is forecast to remain mild, with analysts forecasting a 2% growth rate. Interestingly, a noticeable margin improvement is expected, with EBITDA-M reached c.20%. The outlook for this is unclear in our view, given the near-term supply chain issues and the lack of a track record for improvement.

Valuation

Valuation (Tikr Terminal)

SMIN is trading at 13x LTM EBITDA and 10.6x NTM EBITDA. This is a premium to the company's historical average.

The primary argument for a premium valuation in our view is:

- Increased industry tailwinds which SMIN has shown an ability to partake in through contract wins.

- Disposals at attractive valuations, implying a capacity to buy-and-build.

- Increased scope for M&A through utilization of FCF and debt.

- Margin stability with scale (assuming a bounceback from inflationary pressures).

Overall, we believe a premium is warranted. However, the degree to which is not sufficient. We have not seen enough evidence to suggest strong growth has returned. Further, we would like to see Management show increased M&A activity.

Final thoughts

SMIN is a good business. The company has a good competitive position, an improving trajectory (due to industry tailwinds), and strong margins. Our concerns are around Management's execution of improvement, which would allow the business to justify a premium to its current historical average. Thus far, we have not seen this.

For further details see:

Smiths Group: Industrials With Potential For Improvement