SMFTF - Smurfit Kappa And WestRock: Exploring The Value Of Synergy

2023-12-12 07:33:13 ET

Summary

- Smurfit Kappa and WestRock plan to combine their businesses, targeting annual pre-tax synergies of over USD 400 million.

- The value of the synergies will impact the intrinsic value of the combined entity, with Smurfit Kappa likely to drive the synergies due to its better operating track record.

- The intrinsic value of Smurfit WestRock with synergies ranges from USD 49 to USD 59 per share, providing more than a 30% margin of safety compared to current market prices.

Thrust of my analysis

In Sep 2023, Smurfit Kappa Group Plc (SMFTF) (SMFKY) and WestRock Company (WRK) announced their intention to combine their businesses.

The combined entity, Smurfit WestRock, targets "…an annual pre-tax run-rate synergies over USD 400 million… delivery of synergies expected to require estimated one-off cash costs of approximately USD 235 million…" Source: Smurfit Kappa and WestRock Presentation (hereinafter referred to as the "Combination Document").

The value of the synergies is not just the USD 400 million. Rather it is how they affect the combined operating cash flows and cost of capital. These in turn will affect the intrinsic value of the combined entity.

In my previous 2 articles, I carried out a fundamental analysis and valuation of both companies independently. In this article, I will value the combined entity with the synergies built in to determine the intrinsic value of Smurfit WestRock.

The goal is to see whether a fresh investor should buy Smurfit Kappa Group (hereinafter referred to as SKG) or WRK. I based my analysis on the prices as of 7 Dec 2023 with SKG at USD 37 per share and WRK at USD 41 per share.

I was interested in 2 specific questions:

- Assuming that the combination will go through, which option will provide a better margin of safety?

- From a risk mitigation perspective, which will provide better downside protection if the combination does not go through?

This is mostly a quantitative analysis that is meant to complement what I have written earlier. If you are not familiar with either company, I suggest that you first read my 2 articles. Refer to:

• WestRock Acquisitions Did Not Create Shareholder Value

• Smurfit Kappa : Leveraging Its Track Record To Create Value From The Proposed WestRock Acquisition

Business background

Although both operate in the same packaging sector, they differ in where they operate, product categories, and customer base.

The Combination Document provides a good summary of the differences and how they complement each other. It laid out the rationale and benefits of the combination.

"Smurfit WestRock will have unparalleled geographic and product diversity with a culturally aligned customer focus and enhanced capabilities to serve customers globally."

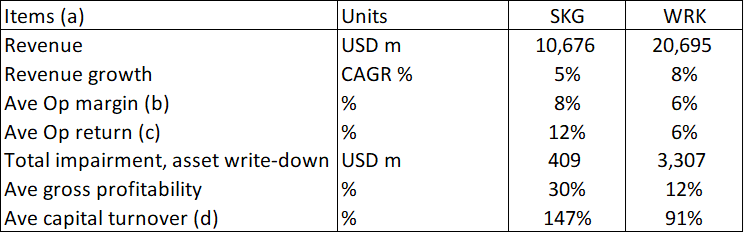

The differences between SKG and WRK also extend to their operating performance as illustrated in Table 1.

Table 1: Comparative performance (Author)

{kind=link}

Notes to Table 1.

a) The average and growth covered from 2015 to 2023.

b) Defined as after-tax operating profit/revenue.

c) Defined as after-tax operating profit / TCE where TCE = equity + debt - cash.

d) Revenue / TCE.

While WRK is about double the size of SKG in terms of revenue, it is not as efficient or productive as SKG. You can see that SKG delivered better returns with better operating parameters (margins, gross profitability, capital turnover, and impairments).

Because of these differences, the intrinsic value of Smurfit WestRock will differ depending on where the USD 400 million synergies are realized. For example, as will be shown later, the impact will be bigger if the USD 400 million are all realized within WRK.

Secondly, SKG seemed to be the "controlling" party Smurfit WestRock. I think that there is a better chance of realizing the synergies as we will have the party with a better operating track record driving them.

Value of synergies

According to Aswath Damodaran,

"Synergy is the additional value that is generated by combining two firms, creating opportunities that would not been available to these firms operating independently."

We can categorize synergies into 2 groups - operating and financial.

-

"Operating synergies affect the operations of the combined firm and include economies of scale, increasing pricing power, and higher growth potential. They generally show up as higher expected cash flows.

-

Financial synergies include diversification and a higher debt capacity. They sometimes show up as higher cash flows and sometimes take the form of lower discount rates."

The challenge in estimating the intrinsic value of Smurfit WestRock is figuring out where the USD 400 million will impact. The only information provided at this stage is that 20 % is from Selling, General, and Admin ((SGA)), 20% from procurement, and the balance 60% from integration.

I assumed that the business combination would have both operating and financial synergies and made an educated guess at them.

Damodaran further stated that:

"…Synergies seldom show up instantaneously, but they are more likely to show up over time. Since the value of synergy is the present value of the cash flows created by it, the longer it takes for it to show up, the lesser its value."

To account for this timing effect, I will assume that it will take 3 years for all the synergies to be fully realized.

Determining the value of synergies

I followed Damodaran's approach in determining the value of synergies. He suggested a 3-step process:

- First, determine the intrinsic value of each company independently.

- Secondly, estimate the "intrinsic value of the combined firm, with no synergy, by adding the values obtained for each firm in the first step.

- Third, build in the effects of synergy into the cash flows and revalue the combined firm with synergy. The difference between the value of the combined firm with synergy and the value of the combined firm without synergy provides a value for synergies."

In my earlier 2 articles, I estimated the intrinsic value of SKG and WRK based on the single-stage Free Cash Flow to the Firm (FCFF) model.

I used the same model for the above second and third steps. The intrinsic value can be represented by the following equation:

Value of firm = FCFF X (1+g) / (WACC - g)

Where:

WACC = weighted average cost of capital

g = growth rate

t = tax rate

In my analysis, I will consider the impact of synergies on 2 metrics - FCFF and WACC.

I assumed that the USD 400 million would improve the FCFF by this amount.

I assumed that there would be a 5% reduction in the respective companies' WACC. The WACC represents the risk of the cash flows. I would argue that the risk profile of Smurfit WestRock would be lower than those of SKG or WRK as independent companies. This is because the combined entity has a wider geographical coverage, product coverage, and customer base.

On top of the above 2 sources of synergy, I also considered the impact of reducing the impairments. In my valuation model, I assumed that there would be future impairments, the value of which was based on the historical records.

In the case of WRK, this was equal to USD 678 million in my valuation model. Impairment and asset write-offs are impacted by utilization and acquisition prices. With better management, the potential for future write-offs will be reduced. Since this cost was due to how I have modeled the businesses, any savings would be on top of the USD 400 million.

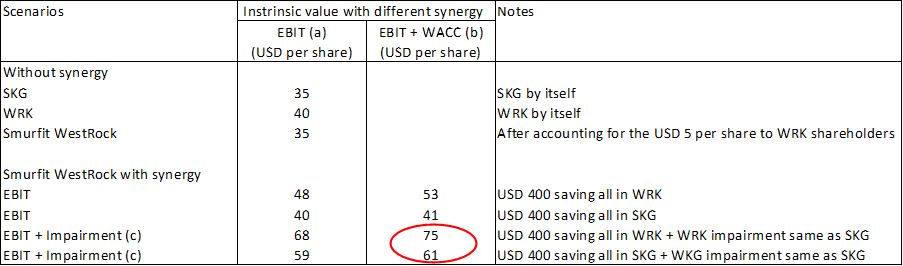

A summary of the intrinsic value under various synergy scenarios is summarized in Table 2.

- Without any synergy, the intrinsic value of the combined business is USD 35 per share.

- The intrinsic value of Smurfit WestRock with synergies ranged from USD 40 per share to USD 75 per share.

The above assumes that the synergies will occur instantaneously at the start of the combination.

But, if you assume that the synergies will only be realized in the 3rd year, the present value of the intrinsic value of Smurfit WestRock is reduced from USD 31 per share to USD 59 per share. There is about a 20% reduction in the instantaneous value. Refer to the sub-section titled "Present value of Smurfit WestRock" for how I arrived at this reduction amount.

Note that the low end of the valuation is from considering only the USD 400 million synergies. I am more confident that there will also be a reduction in the impairments as well as a lower cost of capital.

Accordingly, it is more likely for the intrinsic value to range from USD 49 per share to USD 59 per share. This is looking at the present value of the items circled in red in Table 2 reduced by 20%.

Table 2. Value under various scenarios (Author)

{kind=link}

Notes to Table 2. For the value of Smurfit WestRock with synergy, the 2nd column from the right shows the intrinsic value with just the USD 400 million synergies. The 3rd column shows the intrinsic value with both the USD 400 million and 5 % improvement in the WACC.

a) USD 400 m at the respective companies.

b) USD 400 m and 5% improvement in WACC at the respective companies.

c) I assumed that WRK impairment of USD 678 m is reduced to be the same as that for SKG.

Invest in SKG or WRK?

The market price as of 7 Dec 2023 for SKG is USD 37 per share while that for WRK is USD 41 per share.

If you buy into SKG at USD 37 per share, you will automatically be a shareholder of Smurfit WestRock assuming that the combination goes through. I have valued Smurfit WestRock at USD 49 per share to USD 59 per share. You can see that there is a margin of safety.

If you buy into WRK at USD 41 per share, on completion of the combination, you will be a shareholder of Smurfit WestRock at an effective price is USD 36 per share. This is after taking into account the share swap and the USD 5 per share payable for your shares of WRK. There is also a margin of safety here.

You may think that you are a bit better off buying WRK than SKG since you can be a shareholder of Smurfit WestRock at USD 1 less. But I would also look at the downside.

Downside protection

Based on the value of SKG and WRK as independent businesses, they are fully priced. Refer to Table 2. The value or margin of safety comes from the combination.

One way to look at the risk is to consider what happens if the combination does not go through. In such a situation:

- If you have invested in SKG, you would be holding onto a business with a good operating track record. The current market price is about ¾ of its past 5 years peak price.

- If you have invested in WRK, you would be holding onto a business with a poorer operating track record. But its current market price is about 2/3 of its past 5 years' peak price.

From the downside protection perspective, the key is not to worry about the potential gain. Rather focus on what would happen if the combination does not go through.

I am a value investor and my focus is on the business fundamentals. While we do not have a crystal ball to see the future, our track record provides some confidence that the management team can meet the challenges.

All management says the same things - focus on quality, improve efficiencies, better customer relationships, etc. As such I tend to look at the trends in the various performance metrics to see whether they are consistent with what was said.

In this context, SKG has a better track record than WRK. Refer to Table 1. I interpret this as better downside protection.

I don't think the additional USD 1 gain by investing in WKK outweighs the downside risk.

Valuation model and key assumptions

In my earlier 2 articles, I looked at 4 valuation scenarios and concluded that the expected scenario (referred to as Scenario 3 in the respective articles) was the more likely one.

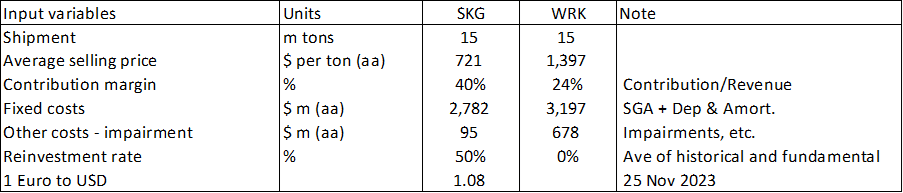

As such I based the current analysis on the parameters of the expected scenario. Table 3 summarizes the key parameters used for the valuation.

Table 3: Key parameters for the expected scenario (Author)

{kind=link}

Note to Table 3

aa) SKG in Euro, WRK in USD

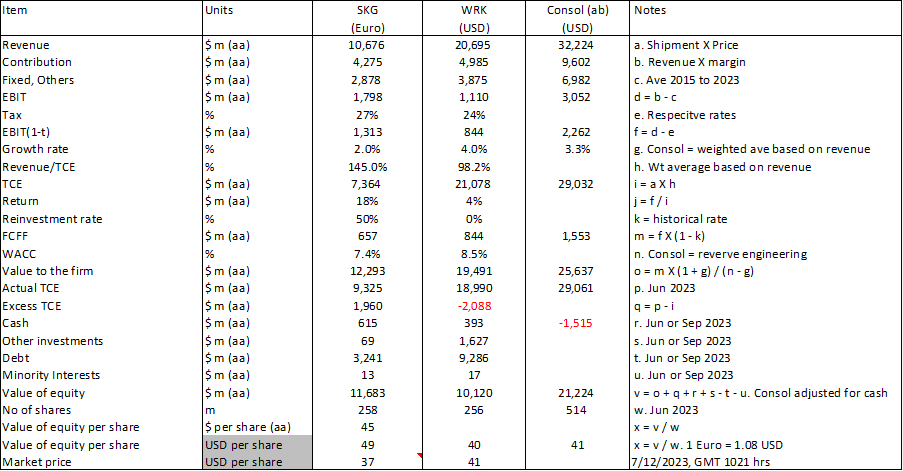

For consistency, I will use the same valuation model when determining the intrinsic value of the combined entity. Table 4 shows the key steps in the valuation model.

- The column titled "SKG" is the independent valuation of SKG. Note that the valuation is carried out in Euro as per my original article.

- The column titled "WRK" is the independent valuation of WRK carried out in USD.

- The column titled "Consol" is the combined value of SKG and WRK in USD. It combined the converted value of the SKG (into USD) with that of WRK. Effectively, it is a "sum-of-parts" approach.

Table 4: Valuation model (Author)

{kind=link}

Notes to Table 4

Item (aa). SKG in Euro, WRK in USD.

Item (ab). SKG values converted from Euro to USD.

Item (r). The negative cash in the Consol is for the payment to WRK shareholders for the shares.

Items (r) to (u). SKG is based in Jun 2023, and WRK is based in Sept 2023.

Item (v). Consol value takes into account the cash paid out to WRK shareholders

Accounting for the USD 400 million

I took a simple approach in allocating the USD 400 million synergies. I assumed that it increased the EBIT by this amount. This is equal to adding USD 400 m to item "d" in the model as per Table 4.

As for the one-off USD 235 cash cost to deliver the synergies, I added this to item "r" in the Consol column.

Accounting for improvements to WACC

According to the CAPM, the WACC is the weighted average cost of equity and cost of debt.

The cost of equity is dependent on the equity risk premium. As per Damodaran, the equity risk premium is dependent on where the companies operate. With a more diversified geographical base, the equity risk premium for Smurfit WestRock would be lower than those of either SKG or WRK.

Along the same lines, the cost of debt is dependent on the debt rating. As a bigger entity, Smurfit WestRock would likely have a better rating than just SKG or WRK by themselves.

You can understand why I see a reduction in the WACC for the combined entity. I have not attempted to quantify the possible reduction but instead assumed a 5 % improvement.

To account for the 5 % improvements in the WACC I reduced item "n" in Table 4 by 5%.

Present value of Smurfit WestRock

If the synergies are achieved at the end of 3 years instead of instantaneously, we will have to discount the cash flow to the present value.

The appropriate way to do this is to determine the FCFF for the various years.

- Year 1 will be without the synergy.

- Year 3 will be with the full synergies.

- Year 2 will be some number in between Years 1 and 3.

Rather than follow the above, I used a simple approach where I estimated the present value of the Year 3 intrinsic value. I assumed that the Year 3 intrinsic value would be the values as shown in Table 2.

The discount rate to determine the present value was derived in the following manner:

- I have the Consol value of the firm as per item "o" in Table 4.

- I have the Consol FCFF as per item "m" in Table 4.

- I derived the Consol growth rate based on the revenue-weighted growth rate of SKG and WRK as per item "g" in Table 4.

- I then reverse engineered the Consul discount rate from the equation Value = FCFF X (1+g) / (WACC - g).

Based on the above, I obtained a discount rate of 8.27%. Accordingly, the discount factor to determine the present value of the Year 3 value

= 1 / [ (1.0827) ^ 3] = 0.8. Effectively this is about a 20% reduction for the values shown in Table 2.

This approach of course undervalued Smurfit WestRock since I ignored the contribution from Years 1 and 2. I would consider the value derived as conservative.

Limitations

In my valuation, I have attempted to quantify the impact of 3 items - USD 400 million, WACC, and impairments.

The Combination Document has also listed other potential synergies on top of the USD 400 million. These include greater efficiency on capital spending, cross-selling opportunities, and improved asset footprint.

I am sure that these will translate into lower Reinvestment rates, higher growth, and lower risk profile (lower WACC). They will improve the FCFF or lower the discount rate.

These are other parameters I have not considered in my valuation. I would consider them as additional margins of safety. As such, I am confident that the estimated value of Smurfit WestRock is conservative.

The real unknown is the time taken to realize the synergies. I have assumed that if will take 3 years. If it takes long, the intrinsic values of Smurfit WestRock of USD 49 per share to USD 59 per share will be lower.

But I think that there are enough margins of safety to offset the timing concerns.

Conclusion

This is an attempt to quantify the impact of the combination of SKG and WRK on the intrinsic value of Smurfit WestRock. It is meant to complement the qualitative aspects of the combination presented in the Combination Document.

In their announcements on the combination, SKG and WRK had presented their rationale. They have even quantified some of the benefits as USD 400 million of synergies.

To the shareholders, this annual pre-tax run-rate of USD 400 million should translate into additional business value.

I have estimated that the additional business value can result in Smurfit WestRock having an intrinsic value of USD 49 per share to USD 59 per share.

There is more than a 30% margin of safety compared to the current market price of SKG of USD 37 per share and WRK of USD 41 per share. (Note that in WRK's case, you have to account for the USD 5 per share payable for the conversion of the WRK shares to Smurfit WestRock shares).

For a fresh investor thinking of taking advantage of this opportunity, I would advise investing in SKG rather than WRK. This will offer more downside protection in case the combination does not go through.

Editor's Note : This article was submitted as part of Seeking Alpha's Top 2024 Long/Short Pick investment competition , which runs through December 31. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Smurfit Kappa And WestRock: Exploring The Value Of Synergy