SMFTF - Smurfit Kappa: Improving Trends Reiterate Buy

2023-08-11 05:31:31 ET

Summary

- Moderately positive on volume recovery and remarkable EBITDA margin.

- Impressive Q2 with lower debt and higher DPS.

- Guidances were left unchanged, and so was our valuation. Still cheap vs. its past.

Here at Lab, we are pleased with Smurfit Kappa's stock price performance ([[SMFKY]], [[SMFTF]]). Since our initiation of coverage (released five weeks ago) called: ' Resilient Margin, A Strong Buy Now,' the company's shares are up by almost 23%. Smurfit Kappa is 2023 Evidence Lab's top pick. It is supported by: 1) the ROCE (the highest among its peers) backed by best-in-class profitability and 2) a solid balance sheet coupled with M&A optionality. In addition, the company has a strong FCF, which well-covers a growing dividend per share in the visible period and offers downside protection in our investments. Within our paper coverage, we have already commented on the quarterly results of International Paper and Packaging Corporation of America .

{kind=link}

Q2 Results

Starting with the CEO's words, he explained how the company, " in a declining volume environment, achieved market share gains across many of the countries in which it operates. "

Q2 Smurfit Kappa revenue reached €2.84 billion and fell 5% and 15% quarterly and yearly, respectively ( Q1 sales were at €2.95 billion ). Looking at the comps, we are not surprised by this negative trajectory. Indeed, in our first analysis, we anticipated a box " volume decline in the 3/5% range for 2023." The company's EBITDA declined to €534 million with a minus -7.8% on a quarterly basis (Q1 EBITDA was at €579 million). However, looking at the Q2 EBITDA margin, the ratio reached a solid 18.8% margin, confirming a resilient performance vs peers (Q1 EBITDA margin was at 19.3%). Top-line sales were impacted by lower volumes which were down by 6% in H1. Looking at the details, this implied that Q2 volume slightly recovered and signed a minus 5%. Going to our supportive investment buy, we could not be more delighted. In detail, the company confirmed:

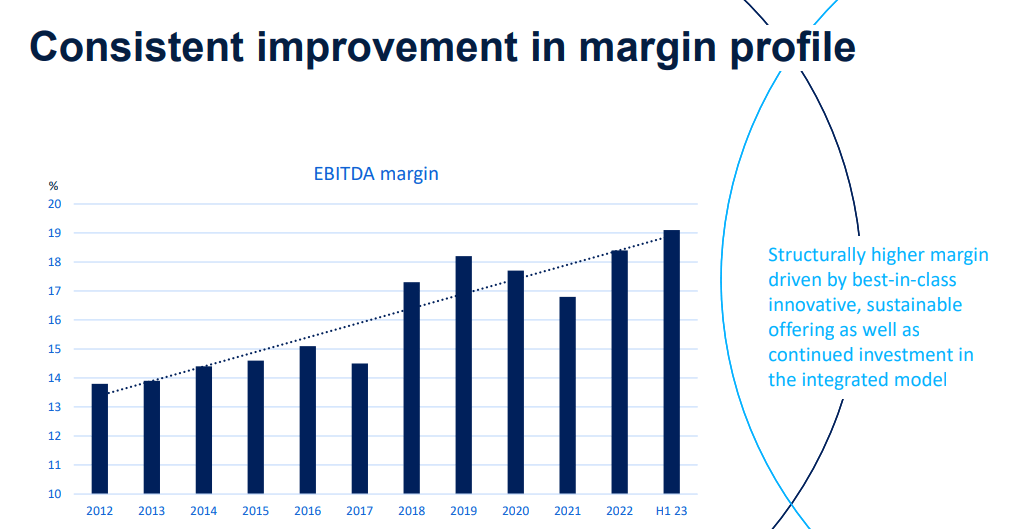

- A structurally higher EBITDA margin (Fig 1);

- A net debt of €3.17 billion with a net debt to EBITDA ratio of 1.4x vs 1.6x achieved in H1 2022 (Fig 2);

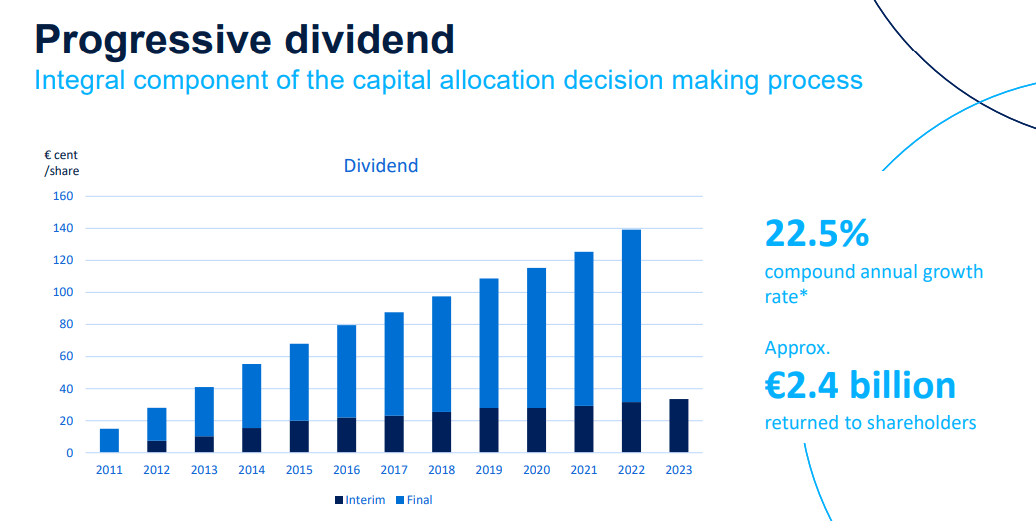

- A higher interim dividend of 33.5 cents per share, plus 6%, compared to last year (Fig 3).

Smurfit Kappa margin evolution

{kind=link}

Fig 1

Smurfit Kappa balance sheet development

{kind=link}

Fig 2

{kind=link}

Fig 3

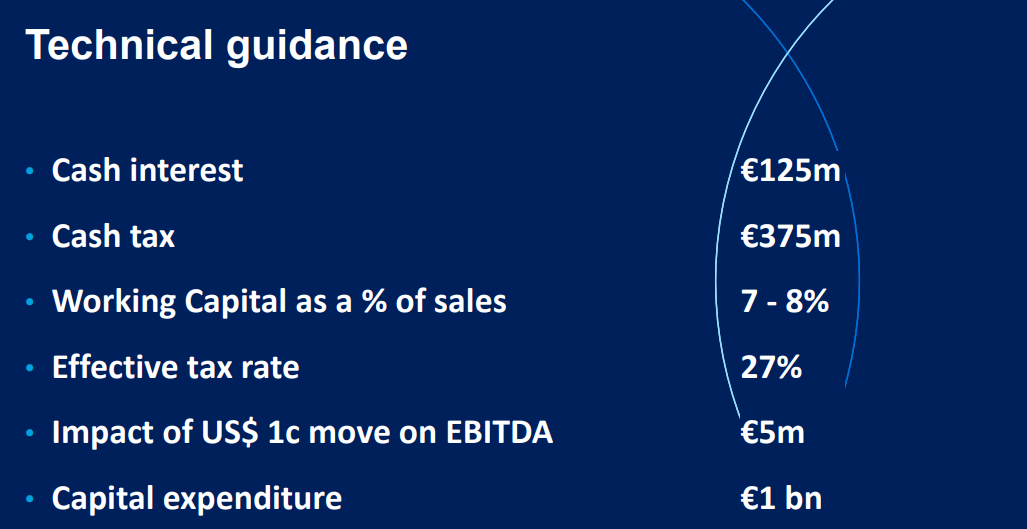

The company's technical guidances were left unchanged. We are moderately positive on volumes, and working capital requirements will reverse. H1 FCF reached €119 million and €71 million in Q2, slightly trending below our internal 2023 forecast. However, given the WC build of €254 million, this trend will likely reverse in H2. Therefore, we apply no changes in our estimates. As a reminder, we anticipate an FCF of €600 million in 2023.

{kind=link}

During the call, the CEO called out a €200 million energy tailwind but a headwind of ~€65 million on wage inflation. Even if the net effect is positive, we still believe a 2023 EBITDA higher than €2 billion is achievable. Another supportive trend is client inventories which are slightly up vs. normal levels, but we think that destocking activities are ending. This is also supported by PKG and IP's Q&A analyst call.

Conclusion and Valuation

With a 23% stock price increase, the company trades at 6x EBITDA. Here at the Lab, we see Smurfit Kappa as cheap compared to its history. In the past, the company's EV/EBITDA was at 7×. Valuing the company in line with its historical average, we derive a valuation of €45 per share. This is also supported by a 9% FCF yield and an increasing DPS. After this positive release, we also believe Wall Street will likely re-price Smurfit's volume trajectory. As mentioned in our initiation, the company's valuation is backed by a reverse discount cash flow with a WACC and an EBIT margin of 8.5% and 11%, respectively. Q2 results are encouraging, so we confirm our buy rating target.

For further details see:

Smurfit Kappa: Improving Trends, Reiterate Buy