SMFTF - Smurfit Kappa: Resilient Margin A Strong Buy Now

2023-06-27 02:58:52 ET

Summary

- Smurfit Kappa reported a record Q1 driven by resilient box prices and easing input costs.

- The company's net debt/EBITDA ratio is at 1.2x, a 0.5x improvement from 2021. This might provide an upside in M&A optionality.

- Positive outlook for 2023 with a solid track record in shareholder remuneration.

Our followers know that we like paper companies, and looking at our recent coverage divided by geographical area, you can check out our latest analysis:

- USA: International Paper , WestRock and Packaging Corporation Of America ;

- EU: Mondi plc .

Given our sector expertise, today we decided to move on with another European player, i.e., Smurfit Kappa ( OTCPK:SMFKY , OTCPK:SMFTF ). The company is a worldwide leader in paper-based packaging solutions thanks to over 350 industrial facilities in 35 countries. However, 22 production sites are in Europe, while 13 are in the American region. The 2022 year-end results show that the company's 80% EBITDA was related to the EU, while the rest was achieved in America. Smurfit Kappa's products portfolio is 100% renewable to improve its customers' environmental footprint.

Why are we supportive of Smurfit Kappa?

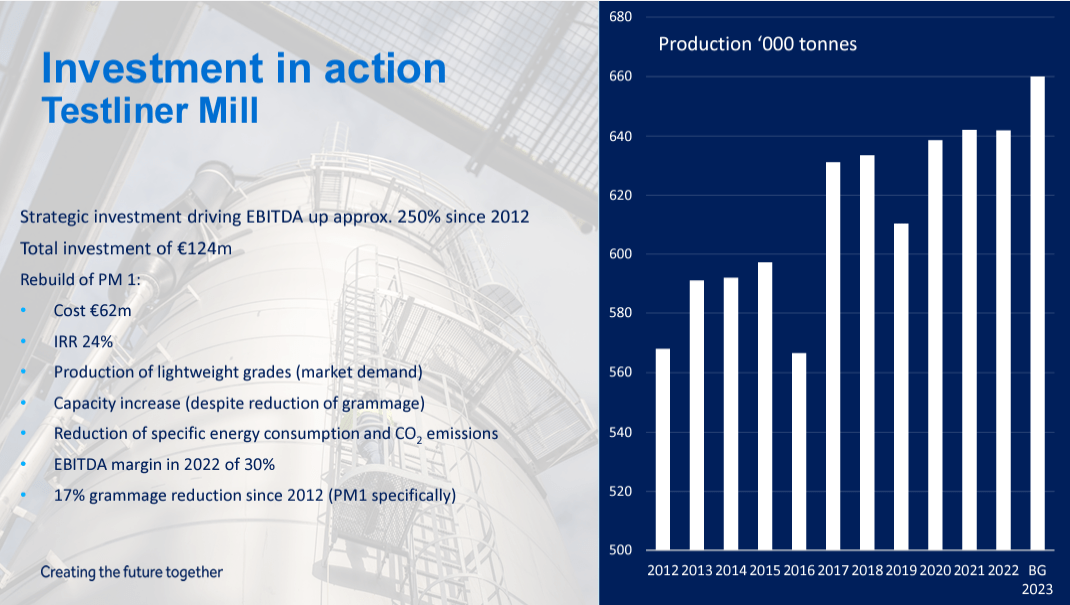

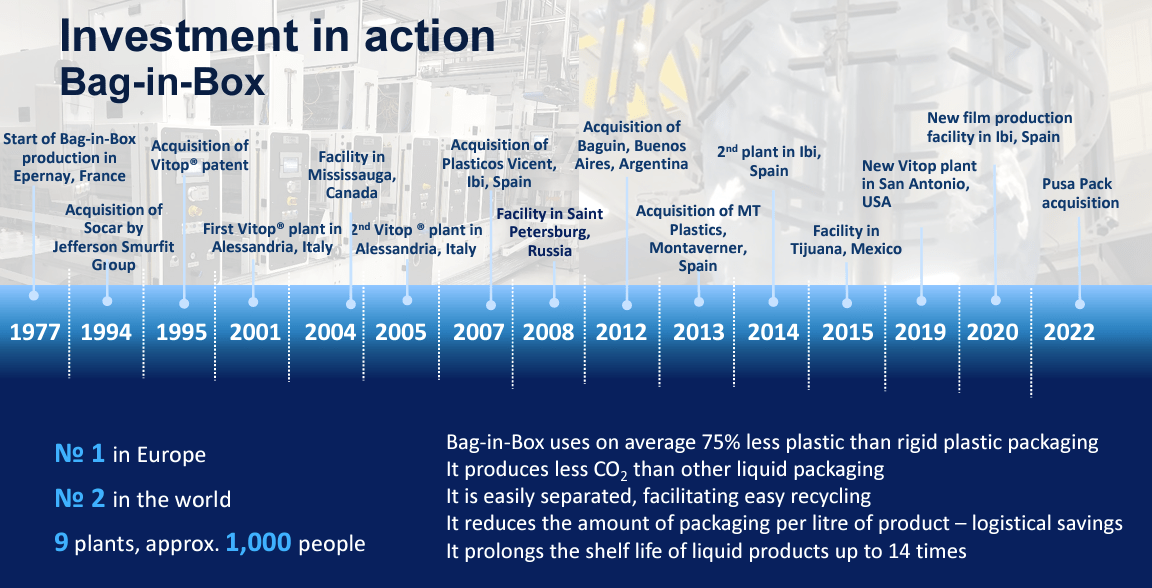

- Compared to its competitors, in a challenging environment, the company was able to increase its EBITDA margin (by 13%) despite weak volumes (-8% in 2022 Q4 and -7% in Q1 2023). Our latest US publications were called " Disappointing Guidance " for WestRock and " Challenges Ahead " for International Paper. We believe that Smurfit Kappa has built a better, more resilient business and is better prepared to navigate the current backdrop. In the past, the company had an accretive CAPEX program that could capitalize on growth opportunities and be at the forefront of the plastic-to-paper switch. This is supported by Fig 3, called " Investment in action Bag-in-Box ";

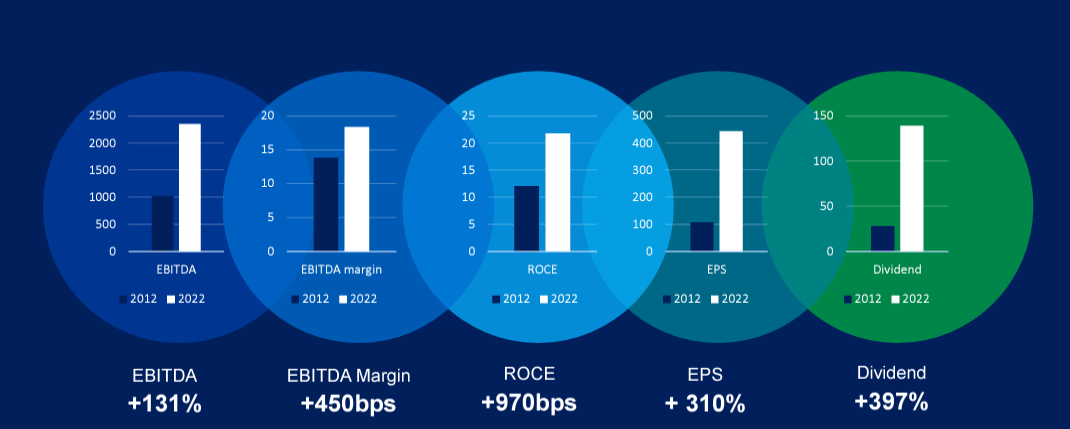

- In detail, the company's ROCE is set at 17% and is the highest among its competitors (IP: 11.29%, WestRock: 6.87%, and Mondi: 21.64%). In fact, the 2022 fiscal year ROCE was at 21.8% and was up from 16.0% in 2021;

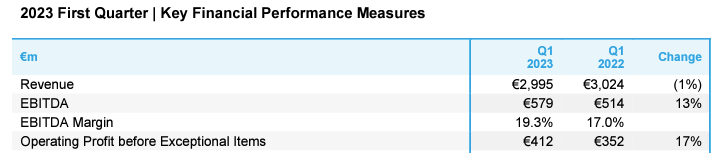

- While the contribution from price/mix development could have been more optimal in Q1, the company (once again) demonstrated an improving trend in cost/efficiency. Despite lower volumes, Smurfit Kappa's resilient box prices and easing raw material costs such as energy have already driven the company's margin expansion to 230 basis points to 19.0% (Fig 4). This positive results more than offset the lower volume and offer downside protection to investors;

- Our estimates forecast a box volume decline in the 3/5% range for 2023. This is due to clients destocking activities and a consumer slowdown. Containerboard prices might continue to drift lower, and we also expect corrugated prices to weaken due to a normalized demand. That said, looking at the latest RISI data , the company is gaining market share, outperforming its competitors. Even if we are estimating lower volumes, Smurfit Kappa's resiliency is a testament to the company's value-added offering to its clientele;

- In addition, the company has an excellent balance sheet. The Net debt to EBITDA reached 1.2x (Fig 2), a 0.5x improvement compared to 2021. Looking at the yearly interest expenses, the company is forecasting a cash interest cost of only €130 million;

- Related to point 5), even if we are not speculating on a potential acquisition, Smurfit Kappa might have an M&A upside. And we believe that the company will look for external growth opportunities given the multiple favorable environments;

- In line with the company's estimates, we are leaving unchanged the 2023 CAPEX set of €1 billion;

- FCF well covers the company's dividend payment. This again offers downside protection to our investment. Smurfit is currently yielding more than 4%. Our FCF estimates are €600, €700, and €800 million for 2023, 2024, and 2025 respectively, with dividend payment estimates at €370, €400, and €425 million for the related years.

{kind=link}

Fig 1

Smurfit Kappa Q1 financials in a Snap

{kind=link}

Fig 2

{kind=link}

Fig 3

{kind=link}

Fig 4

Conclusion and Valuation

Here at the Lab, we believe Smurfit Kappa has started 2023 very well and has a solid track record (Fig below). While challenges remain on volumes and consumer slowdown, the company has never been in " better shape operationally, financially, and strategically." Very briefly, in Q1, the company delivered an EBITDA of €579 million. It was above the Wall Street consensus estimate by 6% despite lower revenue on a yearly comparison (analysts were forecasting an EBITDA of €544 million and lower volumes). ROCE achievements offer a strong backdrop in this environment and a solid capital position on Smurfit Kappa's balance sheet. Given Q1 results and the latest positive trend on market share gain, we are raising our EBITDA growth estimates by 5% in 2023 and 2024, and our earnings per share guidance increased by 6% and 7%, respectively.

{kind=link}

Going to the valuation, we do have two approaches. 1) on reverse estimates, the company is currently trading at 5x EV/EBITDA, which is 0.8x below COVID-19 lows and 1.8x below its historical average. At our target price set at €45 per share, Smurfit Kappa is trading at a 7x EV/EBITDA multiple. Target multiple in WestRock and IP is set at 7x and 8x on the EV/EBITDA. Given its resiliency and shareholder remuneration record, we believe it is very attractive. This valuation is also supported by a reverse DCF, using a WACC and a core operating profit margin of 8.5% and 11%. Our terminal growth rate is set at 2%. In addition, the EBIT margin is conservatively 100 basis points lower than the company's past three years. Using this methodology, we arrived at a target price of €47 per share, in line with our multiple target price. Therefore, given the potential upside, we decided to initiate Smurfit Kappa coverage with an outperform rating.

Downside risks to our buy rating include a slowdown in economic growth, lower industrial production (especially in Europe), higher energy costs, and new industrial capacity in containerboard and corrugated packaging.

For further details see:

Smurfit Kappa: Resilient Margin, A Strong Buy Now