ALB - Snow Lake Resources: A Risky Bet On Lithium Scarcity

2023-08-21 05:27:16 ET

Summary

- Snow Lake Resources: Lithium demand is increasing due to the widespread adoption of electric vehicles and energy storage systems.

- About 2 billion EVs need to be on the road by 2050 for the world to hit net-zero, the IEA says, but sales stood at just 6.6 million in 2021 and 10.8 million last year.

- Snow Lake Resources, a Canadian company, has a large lithium resource and is undervalued, but there are financial and technical risks to consider.

Discovered In 1817 by Swedish chemist Johan August Arfwedson, Lithium is a metal that occupies a central role in the current transformative shift as one of the crucial elements instrumental in the widespread adoption of electric vehicles and energy storage systems, with more of the 85% of the 2023 global lithium supply predicted to fuel lithium-ion batteries.

As the energy transition accelerates, lithium demand escalates.

This year's projected electric vehicle sales are remarkable, with an estimated 14.7 million units anticipated to be sold . This reflects a substantial year-over-year expansion of 36% compared to the 10.8 million units sold in 2022. The United States is poised to drive demand strongly, projecting an impressive year-on-year growth of about 45%. Nonetheless, China takes the spotlight, surpassing global figures and constituting approximately 65% of the anticipated electric vehicle sales for 2023.

There is also a growing consumer preference towards larger vehicles , and as a consequence the average battery size will increase, leading to a higher lithium requirement per vehicle sold.

{kind=link}

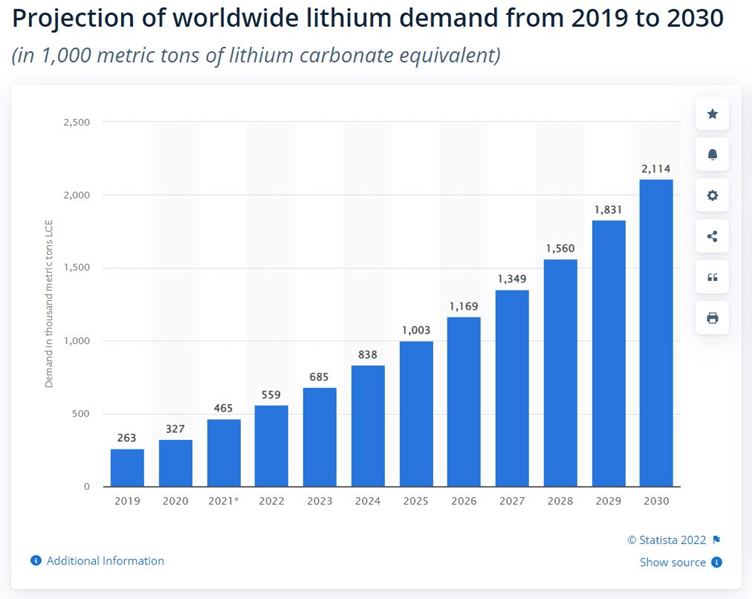

The International Energy Agency recently stated that " Mineral demand for use in EVs and battery storage is a major force, growing at least thirty times to 2040. Lithium sees the fastest growth, with demand growing by over 40 times " and that " The world could face lithium shortages by 2025 ".

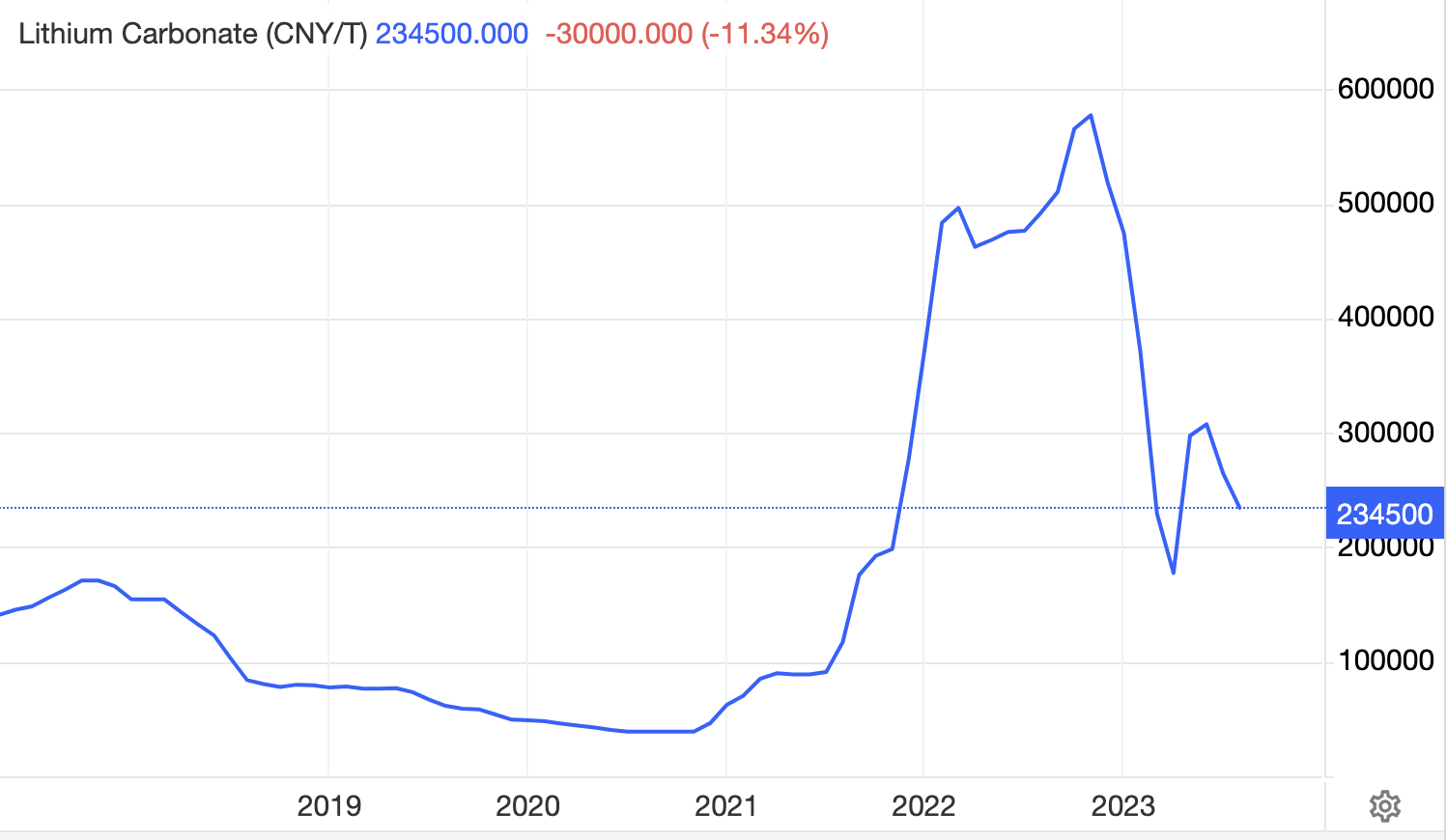

Chinese lithium spot prices have recently declined due to inventory drawdowns, new pricing structures, and seasonal effects.

Lithium spot price in China (TradingEconomics.com)

{kind=link}

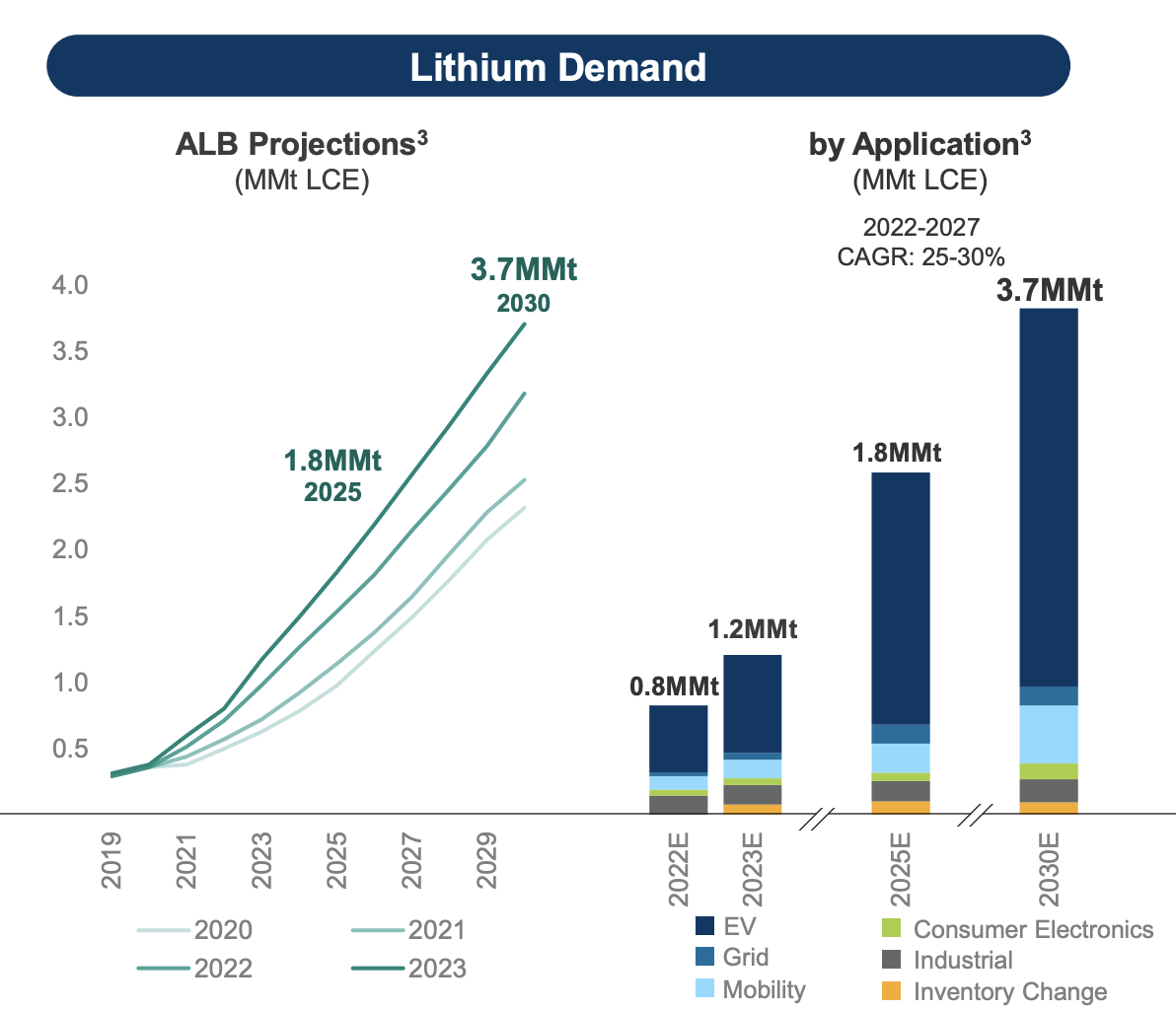

However, a recovery is evident, with potential sector growth in the coming months. Albemarle ( ALB ) raised its forecasts for lithium demand by about 15 percent, suggesting the world would consume 1.8 million tonnes of the commodity (lithium carbonate equivalent) in 2025 and 3.7 million tonnes in 2030. This dynamic presents an opportune time for investors to re-engage with lithium stocks.

Investor presentation - June 2023 (Albemarle Corporation)

{kind=link}

Snow Lake Resources: Is it Hugely Undervalued?

Snow Lake Resources ( LITM ) is a Canadian company based in Winnipeg, committed to operating a sustainable lithium mine in northern Manitoba; it owns a property named "Snow Lake Lithium Project" comprising 60 thousand acres of lithium pegmatite dyke clusters in a "mining-friendly jurisdiction".

Initial testing suggests that a fully functioning lithium mine could produce 160k tonnes per annum of 6% lithium ore concentrate over an 8 to 10-year period, enough to supply approximately 500k electric vehicles per year.

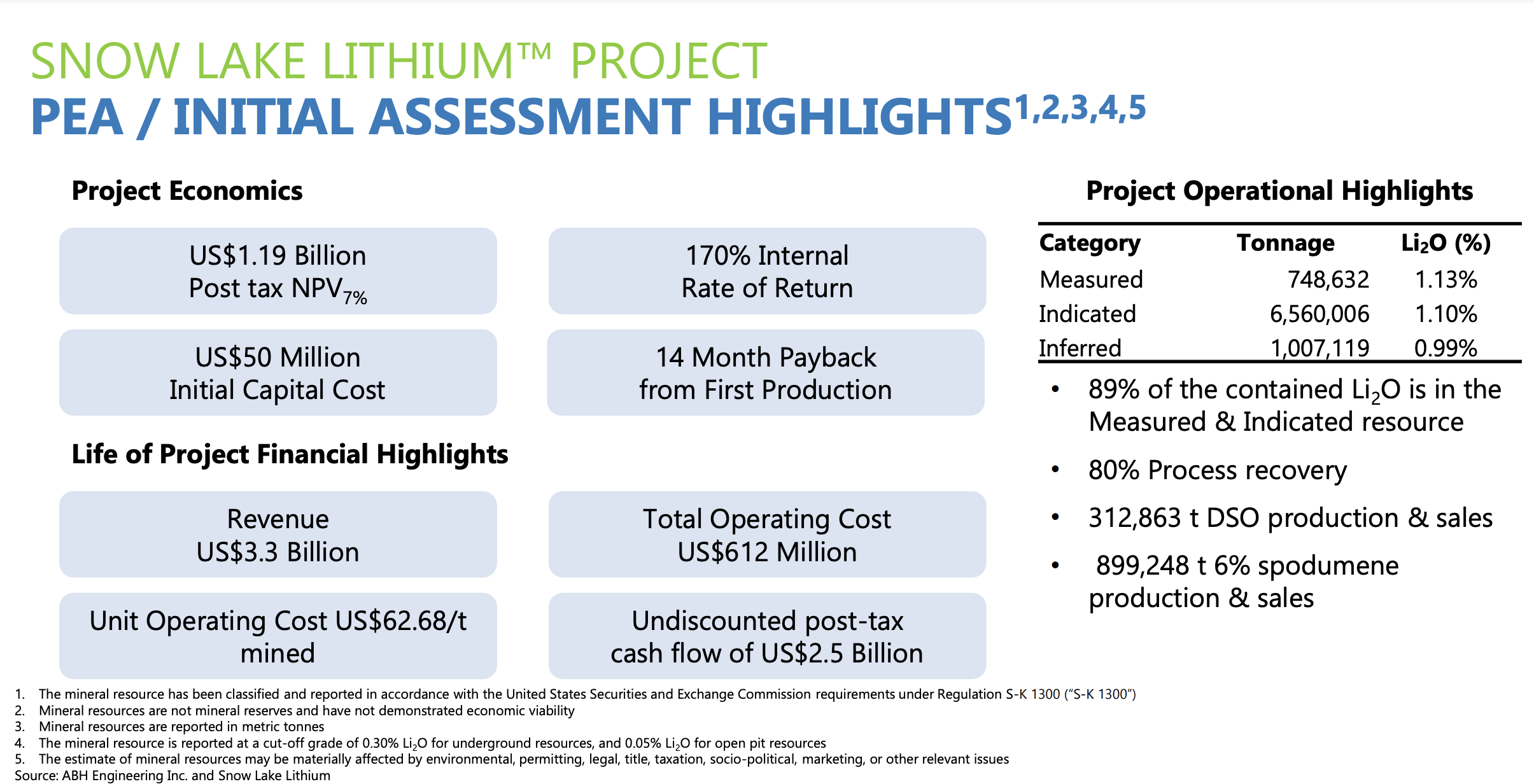

According to the latest (summer 2023) company's investor presentation "the 59,587-acre site has only been 1% explored and already uncovered 8.2 million metric tonnes of measured, indicated and inferred resource at 1% Lithium Oxide."

More specifically they reported:

-

Measured resource estimate of 748,632tonnes @1.13% Li2O;

-

Indicated resource estimate of 6.56 million tonnes @ 1.1% Li2O;

-

Inferred resource estimate of 1.01 million tonnes @ 0.99% Li2O using a 0.3% Li2O cut-off grade

They also released a PEA (Preliminary Economic Assessment) which estimates revenues of $3.3 billion and an undiscounted projected cash flow of $2.5 billion over a 10-year life of the project.

Investor Presentation (Snow Lake Resources)

{kind=link}

The company also states that it will benefit from the Inflation Reduction Act of 2022; the act names 50 "applicable critical minerals" for the energy transition and mining companies excavating these minerals, which include lithium, will be able to seek production credit equal to 10% of production costs.

Using a simple discounted cash flow calculator, setting a 15% discount rate, based on the company's assumptions, I came up with a terminal value of the project between 1 and 1.5 billion dollars in today's money, which makes the company - currently valued at just $35 million - seem a huge bargain.

But before rushing to buy the shares, there are many factors to consider.

Running Costs and Shareholder Dilution

From its inaugural public offering in 2021, the company garnered a total of $24 million in gross proceeds. Throughout the fiscal year of 2022, the company faced a net loss of $9.5 million. This loss was mainly attributed to a non-cash stock-based compensation worth $8 million, which was allocated to directors and officers. This expense, constituting a significant portion of the IPO proceeds, raises concerns about management's judgment (or greed), especially given the present lack of revenue generation. Furthermore, professional fees and administrative costs reached a cumulative total of $830 thousand. As of June 30, 2022, the company's financial records indicated a cash reserve of $23.8 million, and in the latest presentation , they reported that cash as of December 31, 2022 stood at $9.6 million, while in a quarterly SEC filing from March 31, 2023, they reported that cash on hand at December 31, 2022 was $13 million, so I am a bit confused. I could not find more recent data, but assuming the stock-based compensation was a one-time event and administrative and exploration costs are constant, as of this writing there should be a cash reserve of at least $9 million.

The projected total initial capital expenditure is estimated to be US$50 million in the first year of operation, probably 2024, and US$96 million over the balance of the 9-year mine life, with the majority being spent in the first year, and US$10 million in closure costs, for a total of US$146 million.

Since the current cash on hand is not enough to start the mining operations, the company submitted a prospectus on August 4, 2023, outlining its intention to offer shares valued at $100 million. Given the current market price of $2 and 18 million outstanding shares, this will require the emission of 50 million additional shares, resulting in a massive existing shareholders dilution and a big share price drop; this fund infusion is aimed at supporting the aforementioned project. Given that an initial $50 million is earmarked for initiating mining activities, uncertainties arise about whether the remaining funds will suffice to maintain mining operations throughout the mine's lifespan. There is a possibility that, following the initial year, the extracted lithium will be sold, generating additional revenue to sustain the business, ideally yielding profits.

Other Risks

Snow Lake Resources is still in the early operational stages and this comes with a series of financial and technical risks to take into account.

-

Inaccurate Resource Estimates: The measured resource estimate of 748,632 tonnes at a Li2O content of 1.13% translates to approximately 8,450 tonnes of viable lithium; assuming a conservative average price of lithium of $25 thousand per ton, this equals $211 million; yet most of the assessed lithium resources fall into the "Indicated" category, which implies a lower level of confidence compared to measured resources. They are estimated from data that is obtained from a greater distance between drill holes or samples than what is used for measured resources. This implies a somewhat higher level of uncertainty, but the data is still reliable enough to allow for reasonable projections of the deposit's characteristics. The indicated resource estimate of 6.56 million tonnes at a Li2O content of 1.1% corresponds to approximately 72,160 tonnes of viable lithium. Let's assume that only 50 thousand tonnes of indicated resources are viable for extraction; assuming a conservative average price for lithium of $25K per metric ton, that would correspond to a gross value of $1,25 billion.

-

Volatile commodity prices can significantly impact revenue projections and profitability, especially for a company yet to establish its foothold.

-

Financing Challenges: Difficulty in securing adequate funding to support exploration, development, and production can hinder progress and lead to operational delays.

-

Technical Challenges: Geological uncertainties, unexpected technical difficulties, and equipment malfunctions can impede efficient mining operations.

-

Unrealistically optimistic timing evaluation: Given that it takes from 2 to 4 years for a lithium mine to achieve full operational status, the company will likely incur significant losses in its initial years. This scenario may necessitate the company to secure additional funding by either increasing its debt load or issuing more shares, potentially resulting in the dilution of existing shareholders.

-

Overly optimistic PEA: The company's projection of generating $3.3 billion in revenue throughout the project's lifespan is marred by a lack of transparency regarding the feasible amount of extractable lithium and the average lithium price considered in the calculation. Although lithium prices a likely to escalate in the forthcoming years, there exists a possibility that their assessment is excessively positive, potentially resulting in substantially reduced actual revenues.

Additional Risks Related to Microcap Investing

Investing in companies with a market cap below $100 million carries specific risks that investors must consider. Shares in microcap companies often trade with low volumes, making them illiquid and difficult to buy or sell at desired prices. Exiting a large position swiftly is challenging due to limited trading activity, potentially leading to big price declines. These stocks are also vulnerable to market manipulation due to reduced scrutiny. Furthermore, microcap companies provide limited financial information, increasing uncertainty. Their higher risk of business failure and lower regulatory oversight compound these challenges.

Conclusion

As always when investing, the potential for substantial profits is paralleled by elevated levels of risk. Snow Lake Resources potentially holds vast lithium resources, a coveted metal in escalating demand due to its pivotal role in transitioning from conventional gasoline-powered vehicles to electric ones, one of the prevailing megatrends of the 21st century . At current market prices, the company's valuation appears attractive, contingent upon the successful execution of its business plan and the feasibility of resource extraction. However, being a low market cap company in the early developmental stages introduces a series of uncertainties and associated risks. As time unfolds and the landscape clarifies, the company may need to recalibrate its goals, grapple with considerable financial setbacks, revise its revenue projections downward or even contemplate abandoning the project altogether.

For further details see:

Snow Lake Resources: A Risky Bet On Lithium Scarcity