TDC - Snowflake: Disrupting Siloed Data With Data Analytics And Machine Learning

2023-06-18 03:06:37 ET

Summary

- I believe Snowflake is disrupting the data market with its cloud platform for machine learning and data analytics, capturing market share from legacy incumbents.

- I think Data Analytics and Machine Learning are still in the early stages of adoption, with steep adoption curve ahead.

- Despite short-term consumption uncertainties, Snowflake's long-term growth outlook remains strong, making it an attractive investment for long-term investors.

Snowflake ( SNOW ) originally built their cloud-based warehouse on AWS in 2014, then started to build their platform and applications to operate workloads beyond data warehousing. Over the past few years, Snowflake has experienced whopping growth, with sales growing from $100 million in FY19 to more than $2 billion in FY23. They are taking market share from legacy incumbents like Teradata ( TDC ), Oracle ( ORCL ), IBM ( IBM ), and EMC.

I believe Snowflake is disrupting the siloed and structured data, combined with database management, data analysis, machine learning, cyber security, and data sharing. In addition, Snowflake Marketplace enables enterprise customers to combine internal data with external third-party data products for improved data analytics and decision making. From my perspective, Snowflake will become the most relevant cloud platform for machine learning and data analytics.

How Big is the market?

According to Gartner, database management spend will outpace the broader software market, growing from 13% of software spend in 2021 to 17% in 2026. One clear reason for this growth is the migration of workloads to the cloud. In conjunction with workload migration, the cloud's share of the database market is expanding and expected to reach 71% in 2025.

Data infrastructure and the data cloud are two key elements. Enterprises require cloud data infrastructure for storing and aggregating data from various sources, including CRM, cybersecurity, HRM, etc. With structured and unstructured data, enterprises need to share data, perform data analytics, and utilize machine learning for their AI capabilities. The ideal approach is to run all these workloads in the data cloud.

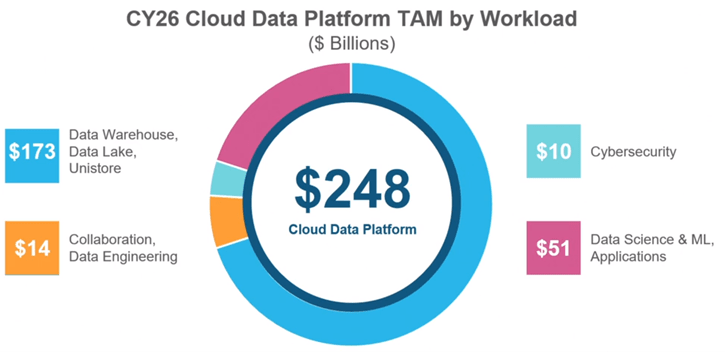

The data cloud encompasses all workload executions, data sharing, and the data marketplace. According to Snowflake, the total addressable market for the entire cloud data platform is estimated to be $248 billion in 2026. Undoubtedly, this is a huge market for Snowflake.

{kind=link}

How much Growth can Snowflake Capture?

Data Analytics and Machine Learning are still in the early stages of adoption : I believe that data analytics and machine learning are enduring trends regardless of the macro environment, and they are still at the early stage of industry adoption. To deploy machine learning and data analytics, you need to migrate all the data to the cloud, design the workloads and applications for the cloud, and run these applications on the data cloud.

I believe Oracle and Teradata are losing the game. Why? Oracle and Teradata provide data warehouses, but the data sets are siloed and structured. In some cases, customers use spreadsheets to download and share data across platforms/divisions. In other words, the data cloud and workloads are not fully integrated, and the data is siloed. On the contrary, Snowflake's platform powers data, whether structured or unstructured, disrupts the siloed data, and supports all these workloads within their data cloud. These features are critical for data analytics and machine learning.

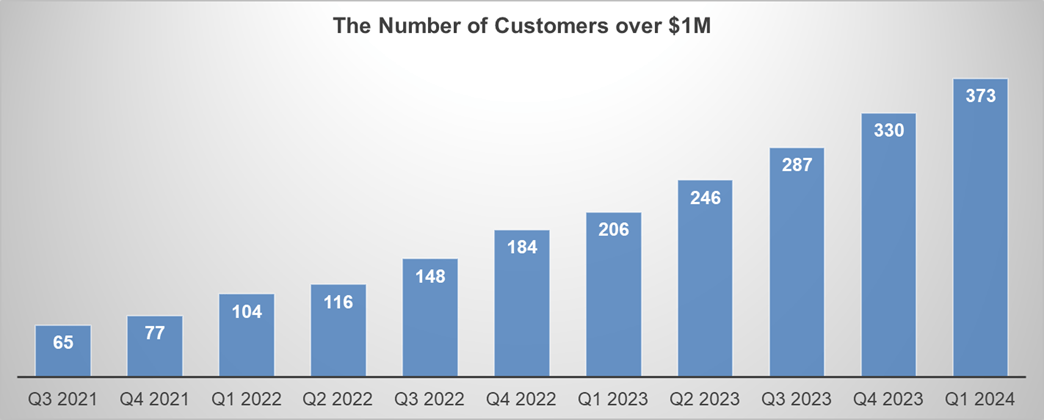

Large Customer Growth Potential : Snowflake is focusing on customers who have the potential to generate more than $1 million in sales over a trailing 12-month period. It is important to note that Snowflake does not operate on a SaaS pricing model, but instead follows a consumption-led model. Their revenue depends on the amount of consumption that occurs in a certain period. Among their current $1 million customers, only 45% are from the Global 2000, 55% are enterprise accounts, and 1% are corporate accounts. In other words, Snowflake has significant growth potential among these large accounts. The chart below illustrates the increasing number of customers with sales over $1 million.

Snowflake Quarterly Result, Author's calculation

{kind=link}

Rising Net Revenue Retention : During the Q1 FY23 earnings call, Snowflake indicated that their net revenue retention rate is expected to remain well above 130% for an extended period. Since Snowflake operates on a consumption-led revenue model, customers are likely to increase their usage over time if the data cloud workloads, data sharing, and analytics continue to provide value for them. Achieving a net revenue retention rate of over 130% is exceptional among software companies, in my opinion.

Why is Snowflake Disrupting the Data Cloud Industry?

I am using Teradata as a comparison. The key difference between Snowflake and Teradata is twofold: architecture and flexibility.

Teradata's warehouse uses hardware and software components that need to be installed on-premises for optimal operations. Although they offer a cloud service, it is not as popular as their proprietary software and hardware usage. Teradata utilizes a shared-nothing architecture, where each node works independently with optimal speed using on-premises software and hardware.

In terms of capacity and flexibility, Teradata relies on fixed capacity specified in their hardware and software. Once the data exceeds this capacity, customers need to purchase more hardware and software to expand. In other words, the data warehouse lacks the flexibility to address the growing demand for datasets.

In contrast, Snowflake utilizes a combination of shared-nothing and traditional shared-disk architecture. This new architecture enables Snowflake to provide database storage, query processing layers, and cloud services. Consequently, Snowflake operates as a cloud solution, with all components residing in the cloud. There is no software and hardware installation required, and there are no capacity constraints. All queries with SQL leverage the cloud infrastructure providers, including AWS, Azure, and GCP.

From the customer's perspective, there are no upfront capital expenses associated with data storage and data analytics. In other words, customers do not need to purchase hardware and software initially. Instead, they migrate their workloads to the cloud and utilize Snowflake as the data cloud, paying for its services on a consumption-based model. As more workloads are migrated to the cloud, there is no doubt that Snowflake will disrupt the data management industry.

Outlook and Key Risks

Weakness Consumption in Data Cloud : as mentioned earlier, Snowflake's business model is primarily based on consumption. This means that customers have the flexibility to spend less on Snowflake during challenging macroeconomic conditions. During the Q1 FY24 earnings call, there were inquiries about the macro environment and enterprise data consumption. Snowflake's management acknowledged the difficulty in predicting their short-term growth due to their consumption-based model, as customers have the potential to alter their consumption patterns. Additionally, enterprises may defer their cloud migration projects to cut expenses. If that is the case, workload migration could experience a hiccup in the near term, which could negatively impact Snowflake's sales.

Competition from Hyperscalers: Snowflake is partnering with all the major Hyperscalers, including AWS, Azure, and GCP, and provides a significant amount of usage on these platforms. Approximately 80% of Snowflake's sales are on the AWS platform. At the same time, Amazon offers services like Amazon RedShift, Athena, Amazon EMR, and others focused on workload analytics. However, Snowflake offers a comprehensive platform that covers a full spectrum of data warehouse, data lake, data science, data analytics, and data application development. Amazon, on the other hand, is only designing some data analytics functions to meet simple applications, and they are more suitable for small businesses.

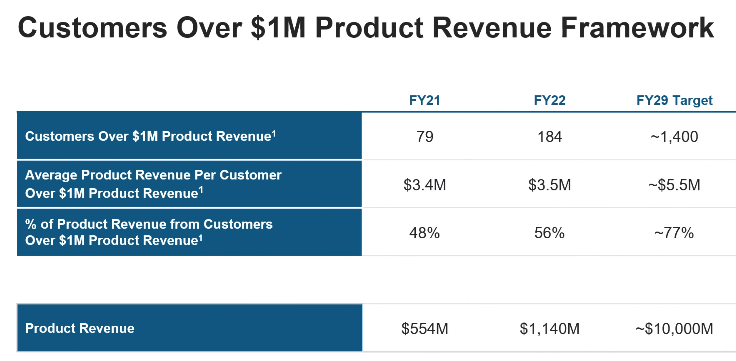

However, despite this uncertainty, I remain optimistic about Snowflake's long-term growth. Their platform plays a mission-critical role for their customers, and the adoption of data analytics and machine learning is still progressing among many of their clients. Snowflake maintains their growth target for FY29, aiming to achieve $10 billion in sales, which implies a compound annual growth rate of 36% over the next seven years.

{kind=link}

For FY24, Snowflake has provided guidance for a 34% growth in product sales. They anticipate a product gross margin of approximately 76% and an adjusted free cash flow margin of 26%. In addition, Snowflake has adjusted their hiring plan for the year and now expects to add 1,000 employees in FY24, including any potential additions resulting from mergers and acquisitions.

Valuation

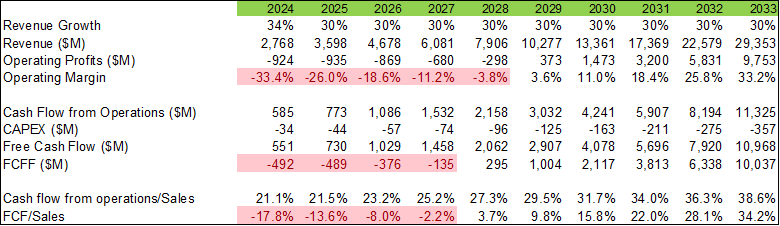

I am using a two-stage DCF model to estimate Snowflake’s fair value. In the model, I assume 30% of normalised sales growth rate, and the growth rate is in line with their long-term guidance: $10 billion sales in FY29.

I assume they can turn profitable in FY29 and expand their operating margin to 33.2% in FY33. For a software company, 30-40% of operating margin is quite normal, in my opinion.

DCF Model-Author's Calculation

{kind=link}

In the model, their free cash flow conversion is estimated to reach 34% in FY33. Again, it is quite usual for a software company. In addition, I use 10% of WACC in the model.

The present value of Free Cash Flow to the Firm over the next 10 years is estimated to be $8.9 billion, and the present value of terminal value is $67 billion. As such, the total enterprise value is estimated to be $76 billion. Adjusting gross debt and cash balance, the fair value of the stock price is $245, according to my estimate.

DCF Model-Author's Calculation

Other than the DCF model, I am using the ratio of current market capitalization and sales forecast in 5 years to compare some growth software companies, including ServiceNow, Adobe, and Microsoft. As the table below indicates, Snowflake's sales multiple is not significantly different compared to its peers. However, it is important to note that Snowflake is aiming to achieve a compound annual growth rate of 36% over the next few years, which is the highest growth rate among these peers.

{kind=link}

Conclusion

Throughout my 15-year investment career, I have constantly sought out technology disruptors before they gain widespread recognition in the market. I always ask myself several key questions:

- What is the potential market size that the new technology could generate or substitute within the next decade? How steep is the adoption curve?

- How much growth can the company attain, and do they possess the necessary resources and strong leadership to capture that growth?

- What competitive advantages or "moats" will the company establish to prevent other firms from entering the same space?

When I analyze Snowflake, it meets all the criteria I have for a future unstoppable disruptor. It exhibits tremendous potential for growth, possesses the required technology and competent leadership to deliver on that potential, and has the ability to create and maintain competitive advantages in the market.

Based on my assessment, I highly encourage long-term investors to consider owning this remarkable company at its current price.

For further details see:

Snowflake: Disrupting Siloed Data With Data Analytics And Machine Learning