SQM - Sociedad Química Y Minera De Chile: Get Ready To Buy

2023-10-17 07:19:44 ET

Summary

- Valuations already factor in low LCE prices and political risk.

- Downgrades may occur after 3Q23 results due to high consensus estimates.

- Demand and supply may balance at $20/kg LCE.

- Nationalization is not a risk.

Summary

Sociedad Química y Minera de Chile S.A. (SQM) shares have derated on falling LCE (Lithium Carbonate Equivalent) prices and concession renewal or nationalization risk. In addition I see potential for downgrades post 3Q23 results on high consensus estimates. However, the shares are nearing a positive risk-reward scenario. On one side EV penetration is accelerating at a higher rate than estimated. On another side, LCE prices have come down to levels that should produce rational capacity expansion and price stability. This LCE price stability may actually drive valuations higher for the sector. Finally, the renewal of the concession is not priced in and could trigger a rally if/when this occurs. Buy SQM post 3Q23 results.

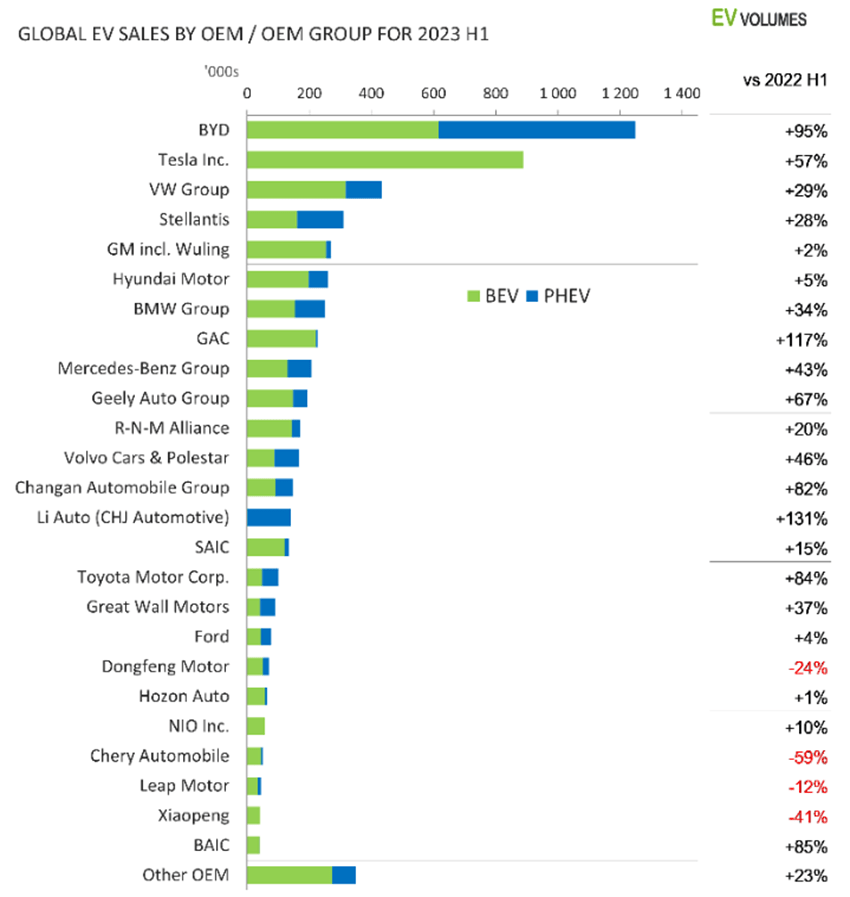

EV Penetration

EV auto sales and penetration are growing faster than anticipated. Falling car prices, higher fuel costs, government rebates, and charging infrastructure expansion have combined to boost consumer demand for EVs. More importantly, the global automakers and their supply chain need to transition to EVs as fast as possible, running two different platforms is expensive, and they need to scale up EVs. There is no turning back, in order to be relevant, the US/European automakers must convert to EVs, otherwise, Tesla (TSLA) and BYD (BYDDF) may take the lion's share of the market.

EV Sales in 1H23 (Image by EV-Volumes.com)

{kind=link}

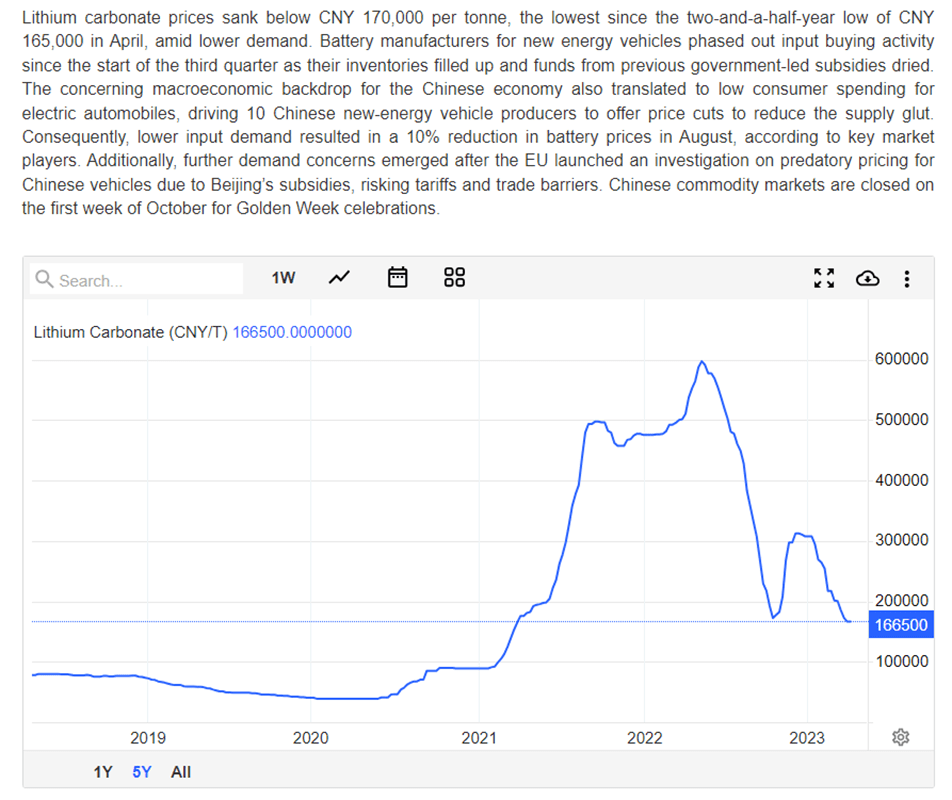

LCE Prices and Cost Curve

After skyrocketing to over US$80kg, LCE prices are back to a healthier US$20kg as supply and demand balanced. For SQM this is a sweet spot that allows for over 40% gross margins, free cash flow to continue to fund expansion, and keeps higher cost assets from entering the market at a reckless pace.

LCE China Spot Prices (Image by Tradingeconomics.com)

{kind=link}

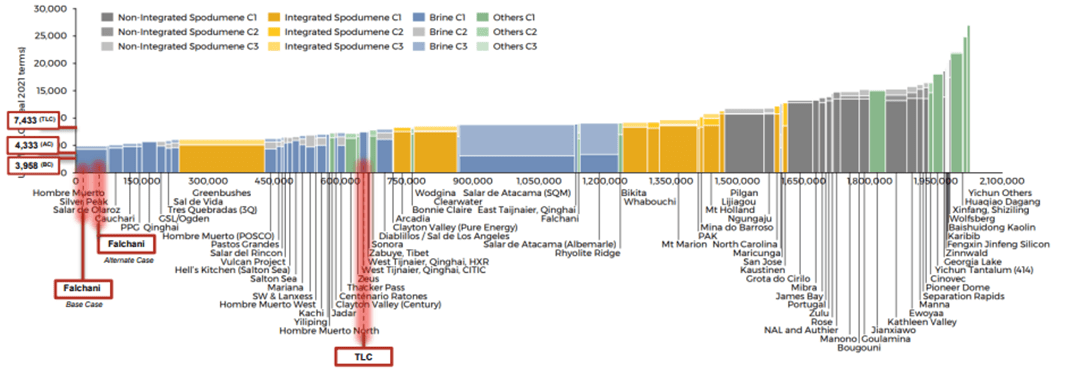

The cost curve at US$20kg makes many key China capacity not economical (without subsidies) and with high environmental costs, according to recent data by [[LAC]] and [[UBS]]. If spot prices continue to decline, new capacity may get stalled or need to look for long-term supply contracts to fund mines and chemical conversion.

In addition, LCE is not yet a commodity like oil or copper, actual transactions and the ability to hedge, and buy forward contracts, are in diapers. The market is still largely based on bilateral negotiations between mining companies, chemical converters, battery makers, and automakers. Demand in China may have paused but in the USA and Europe, it's increasing. In my view, the China spot price is a guide but not likely what SQM or other non-China companies are realizing with customers.

LCE Cost Curve (Image by Lithium Americas)

{kind=link}

Direct Lithium Extraction

A process that promises to further enhance the cost competitiveness of brines vs rock or clay lithium fields. As illustrated in an extensive paper by Goldman Sachs ( GS ), the Latin American brines could expand share via low-cost environmentally benign technology. DLE may reduce processing time and increase yields. Thus, if and when SQM can renew its concession that would very likely be accompanied by a DLE expansion project and enhance capacity and cost competitiveness.

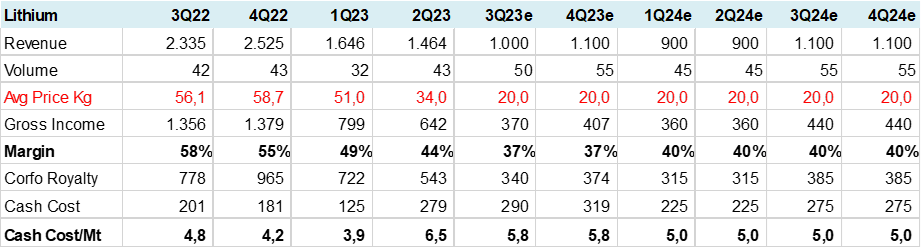

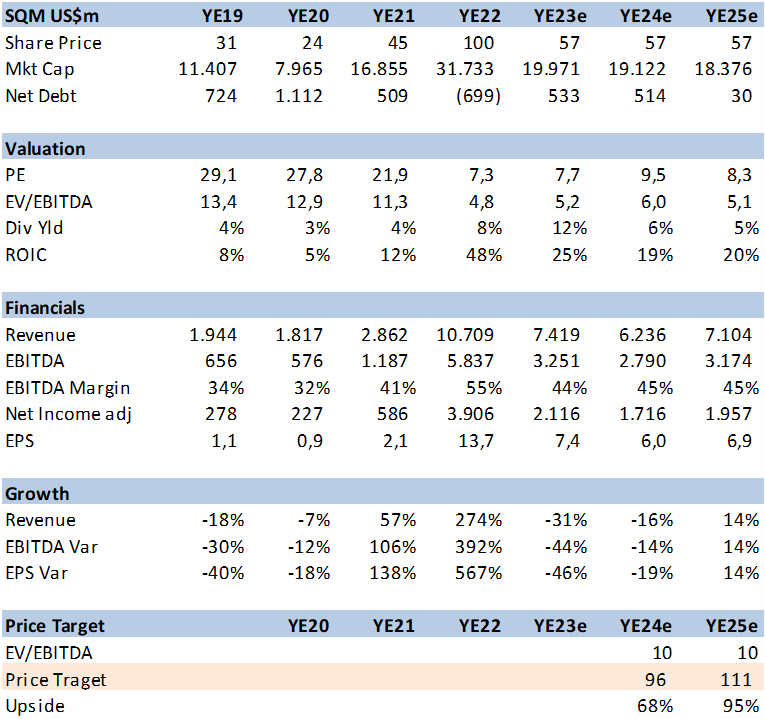

SQM Estimates

Post 2Q23 guidance I have adjusted volumes and now I assume a lower LCE price of US$20kg going forward (vs 30k in 2H23). This may reduce gross margins from 50% to 40% as seen in the table below. Note that cash cost estimates decline in YE24 as new capacity comes online. SQM has been growing very rapidly adding costs faster than revenue that can't always be capexed.

For the other segments of the company, I assume Iodine continues to see near US$70kg prices and over 60% margins. Specialty fertilizers and Potash improve on higher agricultural and natural gas prices while industrial chemicals are flat.

SQM LCE Quarterly Estimates (Created by author with data from SQM) SQM LCE Estimates (Created by author with data from SQM)

{kind=link}

Valuation and Nationalization

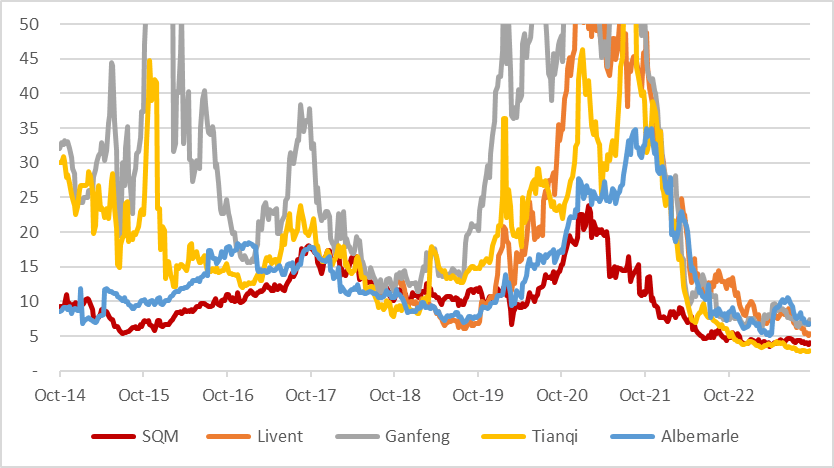

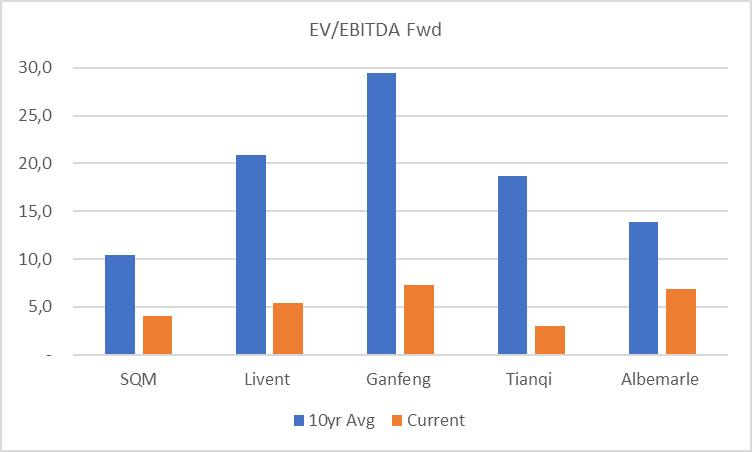

I continue to value SQM at 10x EV/EBITDA, this has been it's historic multiple and coincides with a DFC valuation and long term growth rates. However, the market has de rated SQM down to 5x and the consensus price target uses an implied 5.8x multiple. This de-rating is also evident in many peers such as Albemarle (ALB), Livent (LTHM), Ganfeng (GNENY) and Tianqi. Part of the rationale for this lower multiple is that LCE prices spiked and would fall, which they have. Yet the market continues to discount the sector due to price volatility, much as is seen in the oil and iron ore sector. However, I believe this sector should not be considered a pure commodity given that LCE, or Lithium Carbonate Equivalent as the name implies, is not pure lithium, this is a specialty chemical compound with varying formulations.

The second reason for SQMs derating is due to recent political risk, the famous nationalization threat. This is very unlikely to come to fruition for many reasons, the primary one is that the current government has almost zero political power and no budget to acquire SQM's assets at a reasonable price. At present there is no bill in front of Congress to enact its "take over" proposal of lithium assets via joint ventures where the government controls the assets (51%) but does not contribute capital. The only action reported by SQM and in the media is that Codelco (national copper mining company) has been tasked with negotiating the concession renewal (which expires in 2030). In my view, Chile is not going to nationalize anything.

When/if the concession renewal is announced the valuation may jump several points, which would also be positive for ALB. There is considerable upside risk to SQM's valuation.

SQM Financial Summary & Valuation (Created by author with data from SQM) SQM & Peer EV/EBITDA Evolution (Created by author with data from Capital IQ) SQM & Peers EV/EBITDA (Created by author with data from Capital IQ)

{kind=link}

{kind=link}

{kind=link}

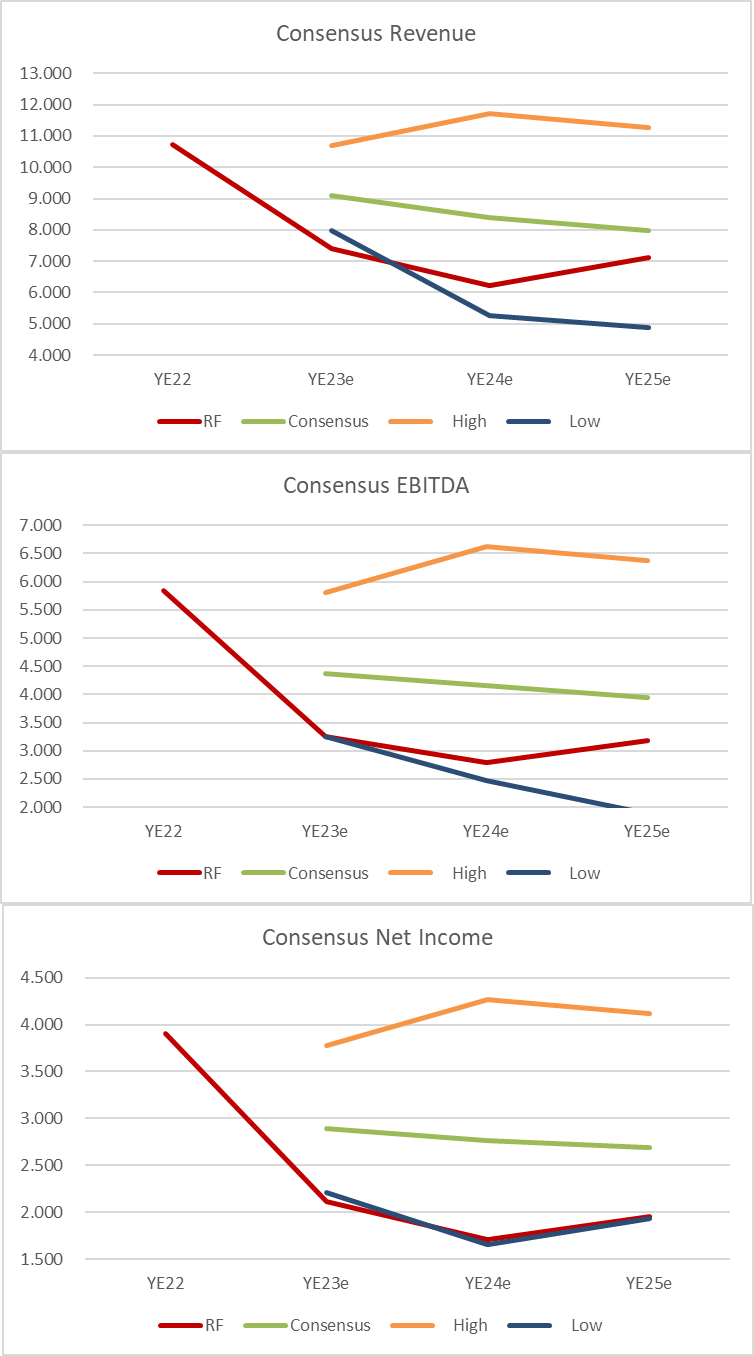

Consensus is a problem

My current estimates, that use LCE prices of US$20kg from 3Q23 forward, are at the low end of consensus. This is a problem, if SQM does realize LCE prices at this level, there could be a rash of downgrades that would not be positive for the shares. Thus, it may be worthwhile waiting for 3Q23 result before buying the stock.

SQM Consensus Estimates (Created by author with data from Capital IQ) SQM Consenus Estimates (Created by author with data from Capital IQ)

{kind=link}

{kind=link}

Conclusion

Buy SQM post 3Q23 results. Consensus may need to correct for lower LCE prices. However, at US$20kg for LCE prices going forward, SQMs valuation is cheap at 5x EV/EBITDA, which has room to re-rate on less volatile LCE prices and more importantly, resolution of the concession renewal.

For further details see:

Sociedad Química Y Minera De Chile: Get Ready To Buy