SCGLF - Societe Generale: One Of The More Attractive EU Banks Still Out There

2023-07-26 07:38:57 ET

Summary

- Societe Generale (SocGen) is viewed as a high-quality bank with a strong balance sheet and a diversified portfolio, making it an attractive investment prospect.

- Despite a temporary expected decline in earnings for 2023, the bank is predicted to see a bounce-back of over 20-40% in 2024-2025, with a current yield of almost 7%.

- The bank is currently undervalued, with a potential upside in the triple digits, making it a recommended "BUY" for investors.

Dear readers/followers,

I'm a fairly prolific bank investor and finance analyst here in SA. Many of my articles go to this space - especially insurance, both multi-line and other types of companies. Société Générale ( OTCPK:SCGLF ) (SCGLY) is one of the largest banks in Europe - In the world in fact. While I own a small stake in the bank, I haven't yet expanded it to the likes of some of my other bank investments. It's still below the 0.5% mark, which I've been comfortable holding it at.

However, in line with my article from January , I have been increasing my exposure, especially as the bank saw a significant drop in valuation in conjunction with the early 2023 bank "hiccough". That's really how I view what happened back then - a hiccough that caused the demise of the players that were by far in the most dire health given what they had been doing over the past 5 years or so.

In this article, I'll update on Societe General for you, and show you why this bank remains an interesting prospect to me.

Societe Generale - Why the next few years look excellent for this high-quality bank

Despite what some investors may say, I view SocGen as one of the more qualitative banks coming out of the nation of France. That's why when it comes to French banks, I have a total of two investments - SocGen and Credit Agricole ( OTCPK:CRARY ).

Both of these investments offer what I view as the duality of positives when it comes to investing - having both a conservative upside as well as a good yield, which together can bring about more than 15% RoR. That's really what I am looking for when I invest in anything - an annualized yield of 13-15% or above . Preferably above.

In some markets and some sectors, that's easy to find - but not all. Over the past 6 months, for instance, the premia for cash-secured puts have been declining and compressing markedly. It's now associated with significant risk-taking to get a good 14-15% from a CSP even on the broad EU market, which was much "easier" just half a year back.

As a result, many of the cash-secured puts I used even on things like SocGen no longer work in my favor. I'd have to invest in the common - or do something like buy-writing covered calls.

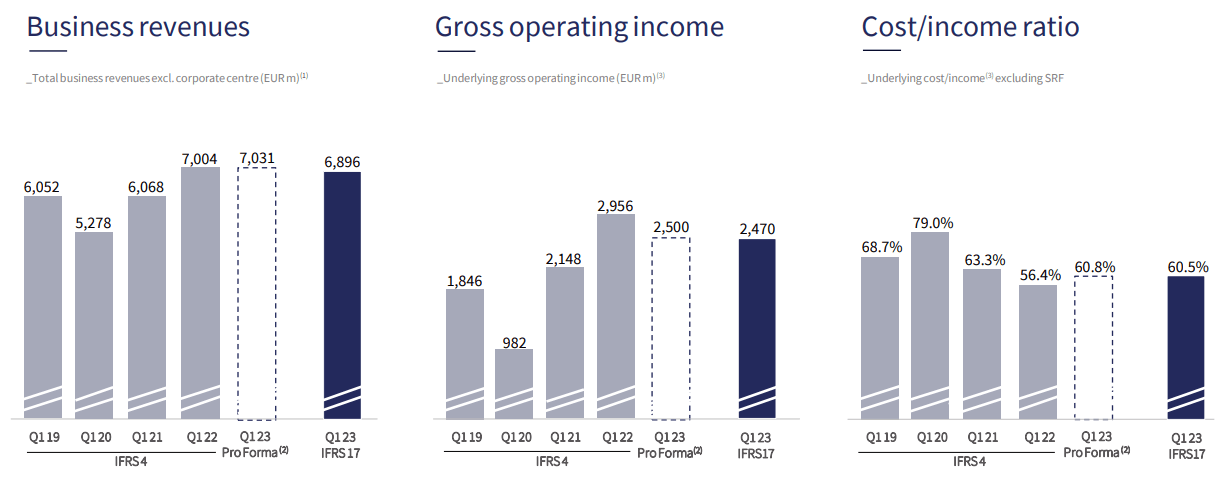

With SocGen though, I believe the bank is in a very good position to get potential profit from investing in the common - both yield and upside. And I also say that the company's recent results confirm my overall positive thesis on the business. The last quarterly results were out in mid-May. Those results saw continued revenues above the €6.6B level, with about flat development overall, but good growth for key business areas like Boursorama, ALD, and international retail banking.

On that revenue, the bank managed to generate €2.5B in gross operating income, at a continued C/I of above 60%, but close to that 60%. SocGen's C/I is significantly higher than some of its European peers. I recently wrote an article on DNB ( OTCPK:DNBHF ), where I called out (positively speaking) the Norwegian bank's C/I, which is now less than 40%. A variance of 20%+ is nothing to sneeze away - but then again, SocGen is both larger and more complex than a national bank like DNB.

SocGen has a very strong balance sheet. With an overall cost of risk at 13 bps, the company has done much to limit defaults, credit risk and provisions. The company's CET-1 rating is good enough, but again, below where the banks I typically invest in in Scandinavia are, by more than 5%. The current CET-1 is at 13.5%, but at the same time comes with a liquidity coverage ratio of well above 150%.

1Q23 was a solid quarter. Nothing results-smashing as such, but a very solid one.

{kind=link}

What I find positive here is the bank's continued low cost of risk, as well as its focus on further lowering risk. Its NPLs have gone from 3.5% in '19 to lower than 2.8% despite the inflation and interest rate increase, reflecting a focus on credit quality and upside. Less than €210M of current loans are in stage 3.

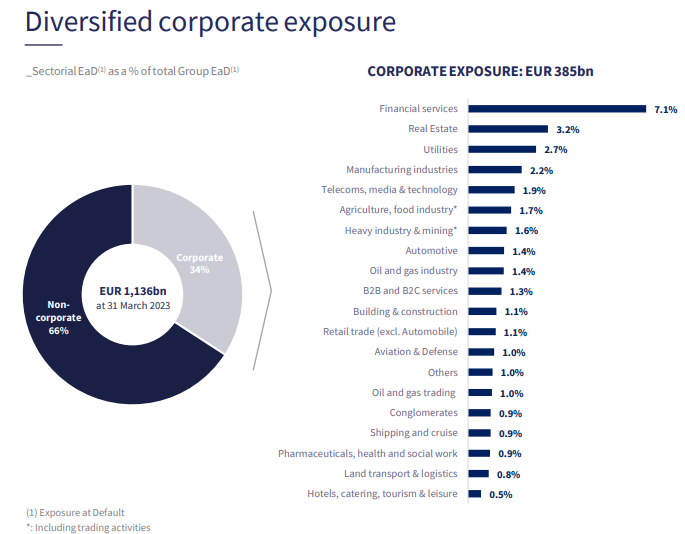

The bank's exposures are extremely diversified. No one corporate sector is above 7.2%, and only one is above 3.3%.

{kind=link}

When looking at these sorts of banks, you want to keep an eye on corporate exposure, even though in this case the bank is more a non-corporate than a corporate bank.

SocGen has extremely low exposure to US regionals - less than €100M, low exposure to any sort of real estate on the corporate side, at around 1.9%, an origination which puts LTV at 50%, less than 25% exposure to overall office, and low exposure overall in US and Asia (less than 20% altogether). SocGen is, as things stand, a primarily European bank, and a primarily Western European bank at that. And while geography can be accused of many things, a lack of financial stability going back 200+ years is not one of them.

Russia?

Some left. The company has worked actively to remove Russia from its active risk, though it's a slow process. It goes down about €200M per quarter, and compared to 4Q21, the risk/exposure is down 50% already. Some provisions and some work are still left, but it's nothing that impacts severely the bank's top or bottom lines.

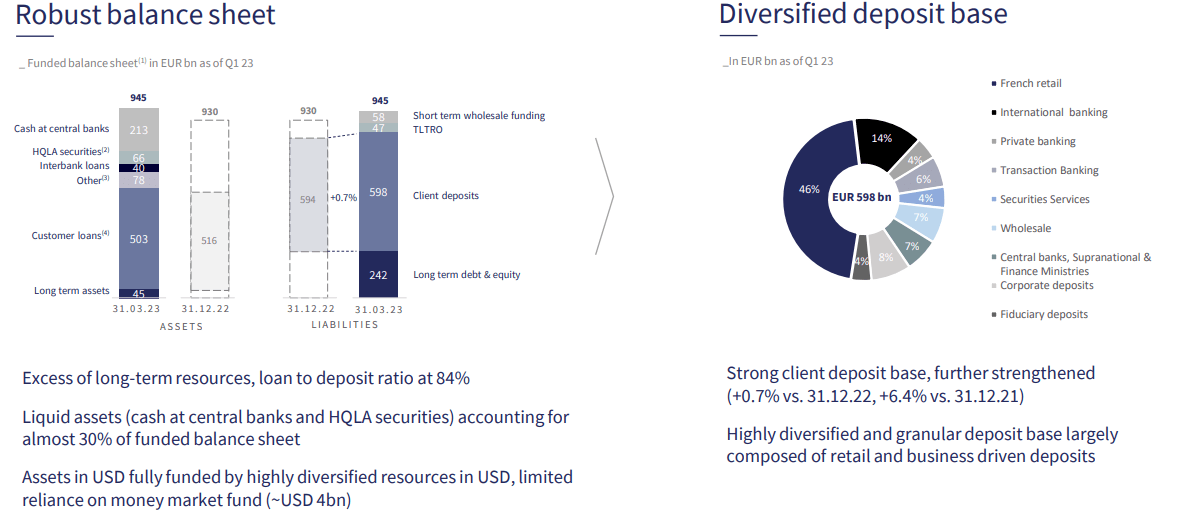

With a leverage ratio at less than 4.5% and a fully-loaded CET-1 at 13.4%, this puts the bank very comfortably above minimum requirements - and deposit and loan trends are in the bank's favor.

{kind=link}

No real bubbles of worry in terms of the various business units exist. Deposits are solid, loans are growing or stable, life insurances are stable as well, and the global private banking sector is increasing as well.

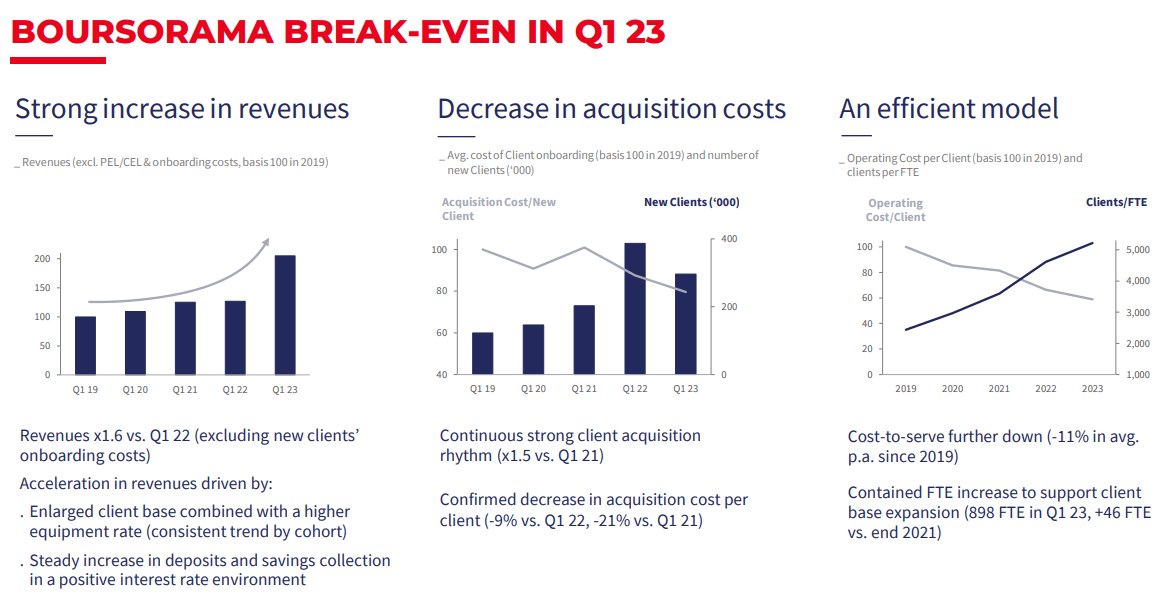

Clients continue the same trends they're doing in other geographies - namely moving to safer, larger banks, represented by continued onboarding of hundreds of thousands of new banking clients. The company's growth projects, such as Boursorama, are finally breaking even due to strong revenue increases and good customer acquisition costs. We might therefore see profit from this going forward.

{kind=link}

Where I would say SocGen is lagging behind its competition somewhat is that due to hedging costs and some specificities of the French retail market, NII continues not to show the same impressive trends as we're seeing in Scandinavia, with record results and earnings possibly going forward. For SocGen, the bank expects these rebounds to occur in 2024 - not before.

All in all, I say SocGen had a solid set of 1Q23 results for the longer-term perspective, and it would not be wrong in the least to expect the bank to outperform here. The bank has stable growth in both financials and insurance, and its advisory fees and business are also seeing good growth here. In fact, for the advisory business, SocGen had close to historic high results and excellent momentum in overall asset finance across all asset classes.

Remember, SocGen is a bank that's been through a lot over the past 20 years. So it's not as conservative as some other banks, because of its ongoing renewal in its business model - but it's come to a point where I see distinct advantages for the company and no longer view it as any sort of risk - I see the upside now, and that's it.

Moving on to valuation.

SocGen Valuation - There is an upside still here in the company

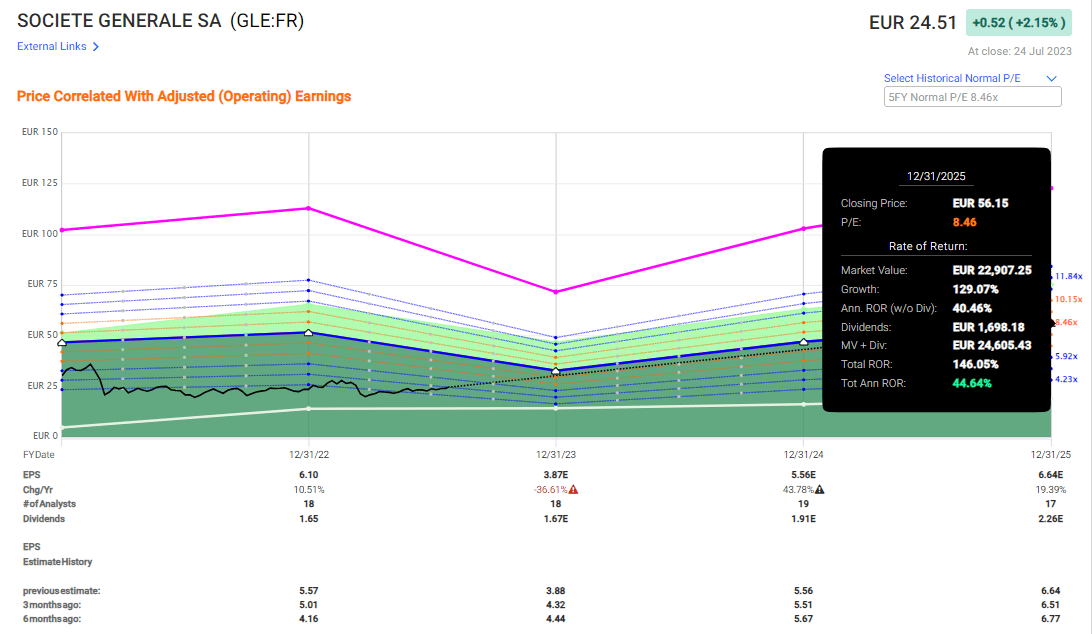

Societe Generale remains extremely undervalued for the increase in earnings that I see realistic for the bank beyond 2023E. The company is expected to see a double-digit decline in earnings for the year - but this is only temporary. Once the hedges go into place and we see the reversal in trends from net interest income, this will lead to a bounce-back of over 20-40% as I see realistically. This is currently expected by another 15-20% EPS growth in 2025E, which altogether represents a double-digit EPS increase of over 20% per year in 2024-2025. The bank currently yields almost 7% in yield. It's A-rated, it's massive, it's what I would consider safe, and the bank currently trades at a normalized P/E ratio of below 5x.

Even just forecasting the bank to its 5-year average, there's an upside in the triple digits to be had here.

{kind=link}

And this one is realistic, as I see it. You could even forecast it at the current level of 5-6x - heck, you could even forecast it at 4.2x P/E, and you'd still make 11.8% RoR based on today's estimates.

That's a remarkable level of overall downside protection for this investment - and it's why I'm growing more and more positive here. I added shares to my position after the regional bank dip, I've continued adding small amounts of shares now as well, and I'll continue to add shares into the weakness.

The 2023E results should bring about a bit more pressure. I consider it very likely that those results will be negative - and so you may get an opportunity to buy more shares of this bank in the near term.

However, as of this time, I would add SocGen to your watchlist - this is a bank that has the sort of potential upside trajectory that other financials for the most part long since have lost, due to interest rate increases. Credit Agricole does not have the same conservative upside or yield. Neither do any of the German ones and certainly, not Scandinavian banks, which are trading closer to their full valuation.

SocGen is a stand-out here - and there are current reasons for it, with weakness in the 2023E, but those reasons will quickly evaporate once the upside for the next few years starts materializing.

This has turned SocGen from what I see as a good CSP target, to a target that I actually want to "BUY".

S&P Global agree with my positive view on the company. 21 analysts following it have price targets ranging from €25.5 to €43/share with an average of €33.6, with 14 analysts at either "BUY" or "Outperform". This merely confirms my positive outlook with its limited downside.

My previous PT for SocGen was €30/share. I'm not bumping it at this time because I do see some near-term price risk, but I'm stating here that I will be bumping it once I see the clear signals for when we can expect the beginning of the reversal. For now, I expect to be bumping it in either 3Q23 or 4Q23.

This company is a "BUY" here with the following thesis.

Thesis

- This is a class-leading French financial institution with absolutely stellar fundamentals - the sort of business I love investing in. I believe that at the right valuation, alpha isn't just possible for SocGen, it's an absolute given based on the current rate environment and the company's earnings trajectory.

- Recent results do more than imply that this is possible - these results more or less confirm the bullish view for me.

- At dirt-cheap valuations, I, therefore, give the company a "BUY" with a PT of €30/share.

Remember, I'm all about:

Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The bank is close to not being "cheap" any longer, but I would still consider it cheap here, given where it may go in the near future.

For further details see:

Societe Generale: One Of The More Attractive EU Banks Still Out There