SDXOF - Sodexo: Worth Buying But Solely To Benefit From The Spinco

2023-09-15 10:30:00 ET

Summary

- Sodexo's Benefits and Rewards division is expected to grow revenue at a double-digit percentage, with operating margins of more than 30%.

- Sodexo reported a strong cash flow performance in the first half of FY 2023, with an increase in operating profit and net income.

- The company plans to spin off the Benefits and Rewards segment, which is expected to create value and increase its market share in that segment.

Introduction

Sodexo ( OTCPK:SDXAY ) ( OTCPK:SDXOF ) is an interesting French company as it operates in two very different business segments. The Sodexo Group employs in excess of 400,000 people in the food industry where it operates on-site dining facilities. Surprisingly, the operating margin in that division is okay’ish with an anticipated 5.5% operating margin, increasing to 6% in the next few years. That being said, I'm more interested in the smaller Benefits and Rewards division which will soon be spun off from Sodexo. That division is expected to grow its revenue at a double-digit percentage while maintaining operating margins of in excess of 30%. Sodexo is trading at around 16 times its anticipated full-year earnings which is kinda pricey. But as mentioned, I'm mainly interested in the Spinco.

{kind=link}

Sodexo is a French company and its main listing is on Euronext Paris where it's trading with SW as its ticker symbol . The average daily volume in Paris is 165,000 shares. There are currently approximately 146M shares outstanding resulting in a market capitalization of 14.9B EUR based on the current share price of just under 102 EUR. You can find all relevant financial documentation here .

It’s about the cash flow, always about the cash flow

Sodexo is a cash flow machine. As a relatively asset-light company, it's always interesting to see how the company performs.

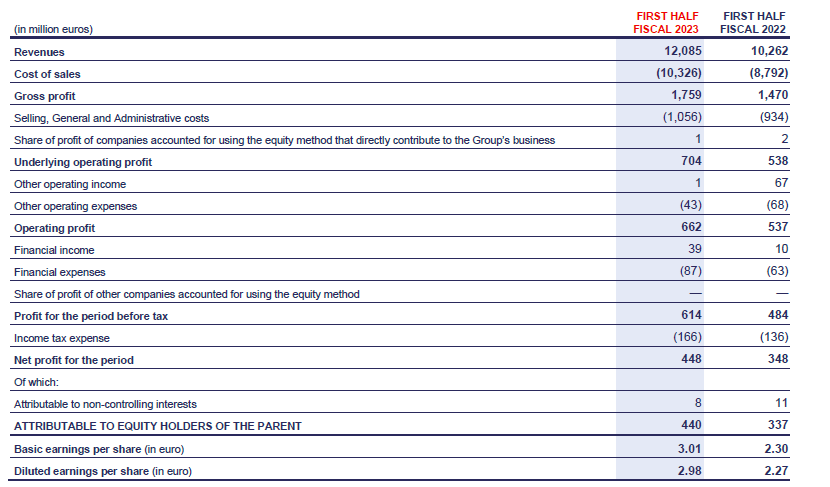

In the first half of FY 2023 (which ended in February), Sodexo reported a total revenue of 12.1B EUR , which is an increase of approximately 18% compared to the first half of FY 2022. The total gross profit increased by almost 20% to 1.76B EUR but unfortunately the increasing inflation had a negative impact on the SG&A expenses which increased by almost 15%.

{kind=link}

That’s not a massive problem as the percentual cost increase is lower than the gross profit increase, and that becomes clear when you have a closer look at the underlying operating profit which increased from 538M EUR to 704M EUR. That’s an increase of almost 31%. And as the net finance expenses decreased, the pre-tax income jumped from 484M EUR to 614M EUR. That’s a 27% increase. After taking the tax payments into consideration, the net income was 448M EUR of which 440M EUR was attributable to the shareholders of Sodexo. This represents an EPS of 3.01 EUR.

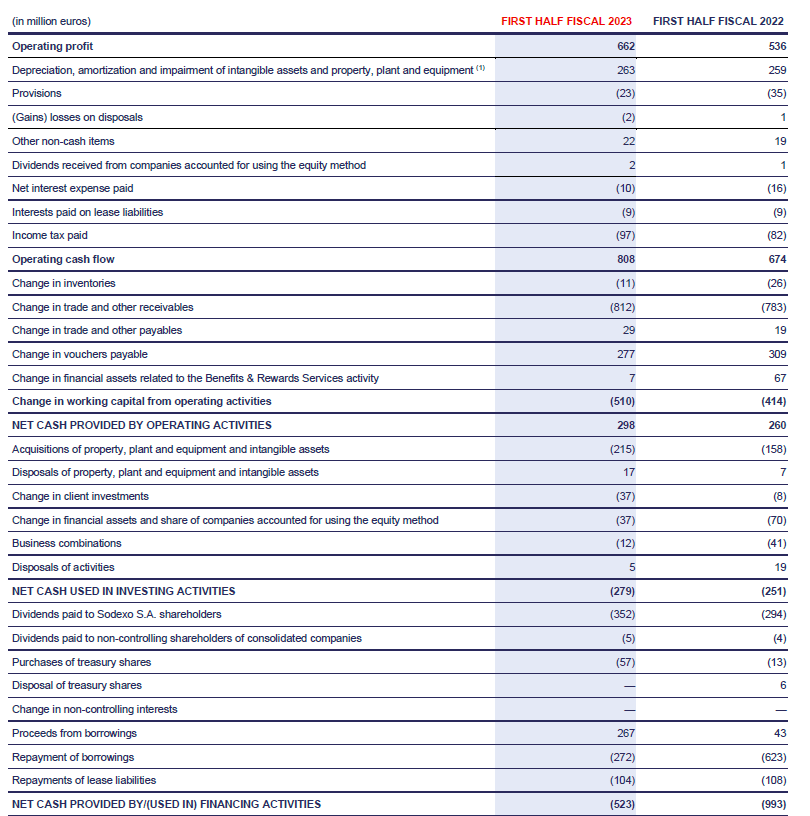

As explained in the introduction and earlier in this article, I mainly focused on Sodexo’s ability to generate a positive free cash flow. In the first half of FY 2023, the company reported an operating cash flow of 808M EUR before changes in the working capital position. That includes a 97M EUR tax payment although 166M EUR was due based on the H1 income statement. This means we should deduct an additional 69M EUR in cash taxes while we should also deduct the 5M EUR paid in dividends to non-controlling interests and the 104M EUR lease payments.

{kind=link}

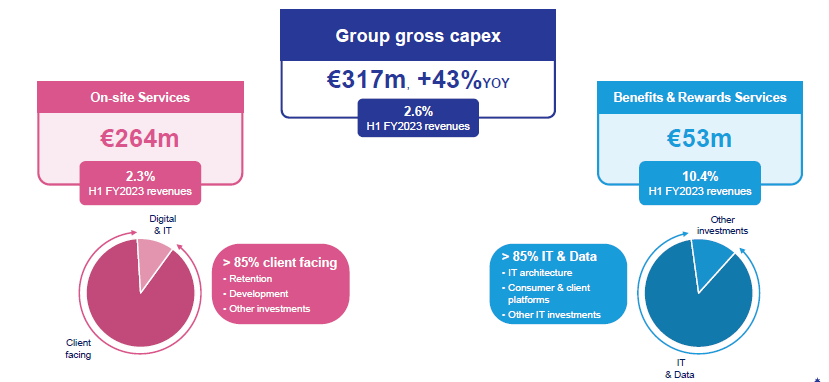

This means that on an adjusted basis, the company’s operating cash flow was 630M EUR. The total capex was 215M EUR (spent on tangible and intangible elements) resulting in an underlying cash flow of 415M EUR. That’s 2.84 EUR per share and although this is lower than the attributable net income, the difference between both results can easily be explained. During the first half of the year, the total depreciation and amortization expenses came in at 263M EUR while the total capex plus lease payments was higher at 319M EUR (I’m not sure how the 317M EUR in the image below was calculated) as the company continues to invest in itself.

{kind=link}

Sodexo confirmed the H1 performance was better than the company initially expected, and this resulted in a full-year outlook increase. Sodexo’s guidance consists of two pillars: The "group" Sodexo and the Benefits & Rewards Services. The company is planning to spin off the Benefits & Rewards segment to drive additional shareholder value and it's positive to see the company providing a detailed breakdown of both divisions.

When it comes to the Group guidance, there will be an 11% organic growth thanks to strong growth results and price increases. Meanwhile, the company expects to keep its operating profit margin stable at approximately 5.5%.

{kind=link}

The Benefits and Rewards Services will see a 20% organic revenue growth while the operating margin of that division will come in at in excess of 32% (which implies a minor guidance increase from the "close to 32%." Those margins are pretty impressive, but Sodexo also provided a 2024-2025 guidance. The organic revenue growth for the group will be approximately 6%-8% while the operating profit margin should increase to approximately 6%. The Benefits & Rewards services will grow at an even faster pace: It expects a low double digit organic revenue increase while the margins should remain protected: the company is guiding for a 30% operating profit margin.

I think that spinoff will effectively create value. As a small investor, I mainly care about Sodexo’s benefits & rewards division, exactly because of its higher margins.

The spinoff will likely be completed in 2024 and will strengthen the company’s No. 1 position in public benefits and its market leadership in 17 of its 31 core markets.

While the Benefits & Rewards Services only generates about 508M EUR in revenue in the first half of the year, I'm very charmed by the anticipated double-digit revenue growth. Assuming a 12% revenue growth with a starting point of 1B EUR over the next few years, the total revenue will increase toward 1.3B EUR and applying a 31% operating margin, the operating profit should be approximately 400M EUR.

Investment thesis

I have a small long position in Sodexo, but I may add to this position in anticipation of spinning off the Benefits and Rewards division in 2024. When that happens, I may just sell the remaining Sodexo shares (as I have little affinity with the on-site services) and depending on the valuation of the Spinco, reinvest the proceeds into the Spinco.

Thanks to the high margins, strong growth projections and a very substantial total addressable market of 1T EUR (and growing at 10% per year), I'm more interested in owning the Benefits & Rewards division. I also think the official guidance for "low double-digit revenue growth" may be too conservative considering that division will post a 20%-plus revenue growth

For further details see:

Sodexo: Worth Buying, But Solely To Benefit From The Spinco