SOFI - SoFi Is Winning Market Share

2023-12-12 04:42:36 ET

Summary

- SoFi is experiencing strong growth in its member base and product offerings, which is driving economies of scale and scope.

- The company's lending business benefits from cheap financing through deposits and has seen significant growth in both deposits and net loans.

- SOFI's technology platforms provide low-cost innovation and licensing income, contributing to the company's overall growth and profitability.

- The shares are not cheap, and there are some risks attached to its lending business.

- Financial Services will be the main growth driver next year.

SoFi ( SOFI ) is an innovative FinTech platform with a bank business that offers the following services, divided into three reporting segments (from the 10-K ):

SOFI IR presentation

The two most important metrics describing the opportunities for SoFi, the FinTech/Bank all-in-one app are the growth of its members (the users of their app):

SOFI IR presentation

It's good to see a re-acceleration in member growth but management argues that 700K+ new members a quarter isn't the new normal, they hope nevertheless to increase it to 500K+ new members a quarter.

Another important metric is product growth (the aggregate number of lending and financial services products that members have selected on the platform since inception).

We do have to point out that these definitions are pretty aggressive and are likely to overstate both members and products, as they are cumulative.

That is, they include members who might have been active once but aren't anymore or members who used a product but aren't anymore, but in both cases, they still count under members as well as products.

SOFI IR presentation

The reasons are straightforward, more members and more products offer economies of scale and scope, leveraging existing technology infrastructure and members, as well as marketing expenses ( Q3CC , our emphasis):

The scale that we have in our member base now at over 7 million members really gives us a significant opportunity just to market to our own members .. we're continuing to see this quarter the compounding effects of everything working together across marketing and product as well as the experience in satisfaction word-of-mouth

The company started with student loans and kept adding products. Customers start with one, through which the company gains their trust so they are more inclined to use another one, increasing marketing efficiency ( Presentation at Goldman Sachs ):

We make about $800 in LTV day one if it's a new member. If it's a cross buy member that comes in through Relay at a very low CAC or comes through Invest or comes through Money, that profit goes from $800 to $1,600 to $2,000.

More financial services and more members are leading to a financial services productivity loop where financial services revenues grow much faster than its lending business:

SOFI IR presentation

There are multiple advantages to the business model here:

- Financial services require little or no capital and no credit risk or capital reserves are required,

- Economies of scale; Financial Services scale much better than its lending business so this will become its biggest growth driver.

- Economies of scope; offering multiple financial services through leveraging the same platform reduces multiple costs, like platform costs and CAC (customer acquisition costs) while at the same time increasing the LTV (lifetime value) of customers through cross-selling opportunities.

- Expanding entry points; and building more financial products also multiplies entry points for new members.

- Data generation increases with the number of customers and the products they use, the data can be used even better to fine-tune offerings towards individual needs, further increasing marketing efficiency (members get tailored advice in their personal feed in the app).

All this tends to create a bit of a flywheel effect , and that is now firmly turning towards profitability as the growth doesn't look like slowing down anytime soon even during difficult times for financial institutions.

The company is pretty good at innovation , coming up with better financial products compared to the competition as they experiment a lot until they come up with a winning formula.

For instance, their investing services allow members who signed up to join in IPOs at IPO prices (those of ODDITY, Instacart, and ARM so far).

After a period of heavy investment and scaling new products, Q3 was the first quarter that Financial Services posted a profit ($3.3M). Growth was blistering with net revenue up 142% y/y and 21% q/q to $118M.

It's remarkable how fast Financial Services have scaled, the net revenue in Q1/21 was just $6.4M, which ballooned to $118.2M in Q3/23.

Despite the rapid rise in members, financial products per member remained stable at 1.5x and illustrates that there are still tremendous opportunities here.

Lending business

Its lending business confers another competitive advantage (Goldman Sachs):

We -- because we are a bank, we charge an APY that helps us fund our loans at about a 200 basis point margin. We could bring the APY down when Fed funds goes down, leave our loans where they are at, expand that spread to 300 basis points or leave it where it's at and gain massive market share, because no one else can actually fund the APY where we can.

APY = (Annual Percentage Yield). It has cheap financing through deposits (apart from its own cash flow). This is an important advantage versus FinTechs and the lack of an expensive branch network is an advantage over most banks.

The company produced $2.9B of deposit growth in Q3 and $2.8B of net loan growth (Q3CC):

the bank contributes to strong growth in SoFi Money products... SoFi Money products have increased nearly 53% year-over-year to 3.1 million accounts... More than 50% of newly funded SoFi Money accounts are setting up direct deposit by day 30.

SoFi Money offers a competitive product with no account fees on checking and savings accounts and earns competitive rates . But there are of course risks attached to the mostly unsecured loans that the company originates.

However, they usually keep the loans on the books for 6-7 months and sell or securitize them after, even though they collect all the payments on all its loans (the ones that haven't paid back or defaulted), whether it sold them or not.

Lending adjusted net revenue grew 15% y/y to $342M with 77% of adjusted net revenue being net interest income (+90% y/y to $265M), which is nearly 2x the directly attributable lending expenses (at $139M).

The segment contribution margin was up nearly 300bp q/q to 60%. GAAP segment net income $84.8M at a 19.3% margin, representing 13% annualized turn on tangible equity. We should also not forget that the Lending business has other advantages (Q3CC):

the bank contributes to strong growth in SoFi Money products, high-quality deposits and great levels of engagement. This has led to higher average account balances even as average spend has increased. SoFi Money products have increased nearly 53% year-over-year to 3.1 million accounts.

Home lending, while still small, was up strongly (46% q/q and 64% y/y) as a result of the integration of Wyndham capital.

Technology platform

The company has two technology platforms (Galileo, a payments platform, and Technisys, a cloud multi-product core banking platform), which are being merged with most of the investments behind us. The Technology Platform brings several advantages:

- Low-cost innovation

- Licensing income

On the former (Goldman Sachs):

So having the Tech Platform allows us to control our own destiny, innovating faster than we could by just using other people's technology. It also gives us an opportunity to be a low cost operator and being a low-cost operator typically becomes a competitive advantage.

On the latter, these platforms are so good that they can be licensed to other (mostly financial) companies, which is where the revenue in their Technology platform comes from (upfront implementation fees, licensing fees, subscription fees).

A year and a half ago management started to shift towards bigger more durable customers and added verticals (also in non-financial sectors), and this is starting to pay off as they have a huge pipeline (Q3CC):

And right now, we're in RFP status with a number of large financial institutions. We've actually won a regional bank deal, that's one component of a larger piece of their business that will come on over the next 18 months to 24 months. But the pipeline is very strong in both financial institutions, incumbent banks and non-financial institutions as well as B2B.

Given that sales cycles are long and onboarding as well, this isn't producing instant growth but over time this will produce a steady nice growth segment with improving margins (towards 30%+) as the investments taper off.

SOFI IR presentation

Management argues that their pipeline is very strong and growth will accelerate in Q4. Segment revenue was up 6% y/y to $89.9M.

They're also benefiting from the majority of newly signed clients bringing existing customer bases and portfolios, which produces much more revenue compared to startups.

New products

The company introduced a corporate credit solution with expense management, an expansion of the Buy Now Pay Later product to enable lenders to offer it as a form of working capital loans for small businesses, and a Galileo-powered debit card program that received MasterCard certification.

Data and AI

The company already introduced Konecta, the AI-driven digital assistant that provides faster customer contact resolution and reduced contacts per customer (also for partners).

Capital ratios

The company is still well above the minimum capital ratio (10.5%) at 14.5% and there seem to be no imminent reasons to worry here:

- Book value keeps on growing ($68M in Q3, $171M for YTD).

- Robust demand for their loans; $100M in Q3 at 105.1% unhedged, $475M in Q4, and a $2B forward flow lined up at favorable execution. Their loans have a short maturity with high amortization quarterly ($2B in Q3 or $8B annualized).

- The company is still scaling up some products that produce large losses ($100M+ from two businesses) which management might choose to slow (and in any case, the increasing scale will lower these losses over time).

Interest rates

The higher-for-longer mantra from the Fed could provide SoFi with another competitive advantage (Q3CC):

hire for longer will absolutely put pressure on other financial companies that unlike SoFi are not benefiting from growing deposits and that faced notable interest rate risk because they either don't hedge. They lack the ability to pass on higher rates the way that we are able to

Management argues that they won't expand loans aggressively (even if there is plenty of demand) as they want to be conservative and prefer quality over quantity. In any case, they argue that Financial Services and the Technology platform are the growth drivers (and require little capital) with loans in a supporting role.

Credit quality

Their PL borrowers have an average income of $167K and a FICO score of 744 with the company's on-balance sheet 90-day PL loan delinquency at 48bp and their annualized personal loan charge-off rate (the percentage of loans that have been written off as losses) was 3.44%.

However, the company's use of AFS accounting is a way around upfront CECL credit loss provisions and they will likely have to increase provisions especially when the economy deteriorates.

While SoFi deals with mainly unsecured loans, it has ways to deal with credit risk:

- The loans have a fairly short duration

- SoFi often sells the loans (usually after 6-7 months).

- Securitization (risk isn't entirely gone here there is residual risk retention debt and in some cases securitization debt).

- Whole loan sales, cuts all risk and obligation

- Interest rate hedging (interest rate swaps)

- They also have and collect lots of info about borrowers

- They seek borrowers with relatively high incomes and credit scores.

Whether this is enough during tougher times remains to be seen though.

Profitability

While the company is still investing significantly and some products (like Credit Cards and Invest) still produce significant losses, management guides for GAAP profitability for Q4 and FY24.

Financial Services and Technology Platforms are simply eminently scalable businesses that require little capital, and the investments they are making are generating well over 30% incremental EBITDA and 20% net income margins, at least this year, management has a point when they argue (Q3CC):

I can't find another company that's driven the level of consistent growth that we have in revenue as well as our member base and product base while driving such significant improvement in profitability and building a high quality deposit and funding base and diversifying it, in addition to growing tangible book value by the level that I mentioned... I remain confident that no company is better positioned than SoFi to be the winner that takes most in the digital transformation of financial services

GAAP profitability includes stock-based compensation, which arguably is pretty high $273M for the past 12 months on revenues exceeding $2B, which is some 14% of revenue, which is steep.

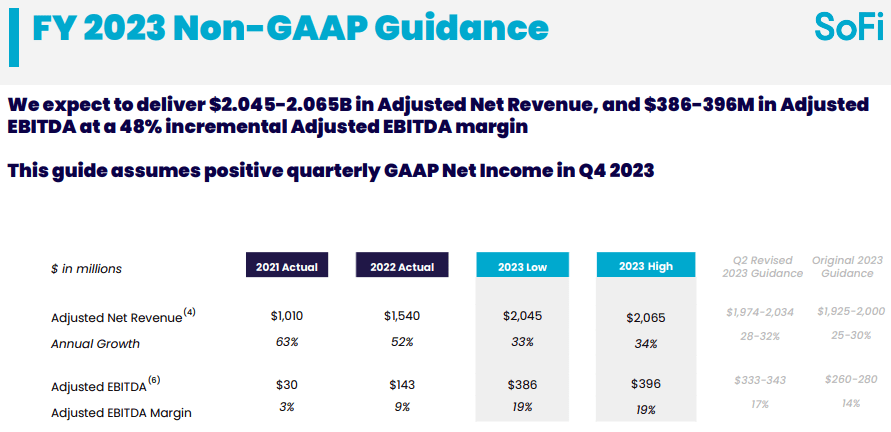

Guidance

{kind=link}

Valuation

There is considerable ongoing dilution from share-based compensation running at 14% of revenue, and there is this, from the 10-Q :

SOFI 10-Q

So fully diluted there are 1.18B shares outstanding which, at $7.8 produces a market cap of $9.18B. The company also has $2.8M of unrestricted cash so the EV is $6.38B or 3.1x EV/S and 16.3x EV/EBITDA.

The company had $3.27B in tangible book value at the end of Q3 so the shares traded at just under 2x tangible book.

The Bear case

Unlike other banks, the company doesn't make any CECL provisions at origination because it classifies its loans as AFS (Available for Sale). This boosts their upfront earnings which is especially marked in the ramp-up phase of origination when the company was using its excess capital:

- Avoiding a 7-8% CECL loss in the quarter of origination

- Recognizing a fair-market value gain on the loan

- Generating net interest income immediately

SA contributor IP Banking has argued :

A back-of-an-envelope calculation suggests the CECL deduction would be in the order of $800m to $900m. This is based on end-of-period loans of ~$13 billion by June 2023 and a CECL provision of ~7%. Currently, the capital allocated to the SoFi banking subsidiary is ~$1.45 billion, so such an adjustment would (notionally) deplete its capital to a great extent.

And excess capital is already depleting rapidly anyway so lending growth is likely to slow down. SoFi is likely to get away with this as long as they intend to sell the loans, but they have only sold $15M in loans in Q3 versus $3.8B in originations, so regulators could start to take a dim view on this at some point.

The upshot here is threefold:

- Lending is going to decline as excess capital is drying up

- Lending profits are inflated by the lack of up-front CECL provision and the instant booking of GOSM profit, especially pronounced as loans are ramping up fast, but these are accounting idiosyncrasies and over the lifetime of the loans profit and losses will even out, especially as the pace of growth in lending is going to decline.

- The company runs the risk of regulatory interventions as it's not selling loans while qualifying all loans as AFS.

On not selling loans, management argued this (Q3CC):

I'd also highlight our $2.9 billion of deposit growth in the quarter compared to the $2.8 billion of net loan growth on the balance sheet period-over-period. With 219 basis points of cost savings between our deposits and our warehouse facilities, this has resulted in a meaningful benefit to our net interest margin and has underscored the advantage of holding loans on the balance sheet and collecting net interest income.

Management expects this to continue as they increase deposit funding (at present they fund 60%+ of originations) and can pass on interest rate rises.

Another element is that as long as deposits are growing faster than loans on the books they are not really running out of excess capital, but equally, one could argue that touting the advantages of holding loans on the books is tempting the regulators with its liberal use of AFS. They can't have it both ways.

Some comfort might be derived from the fact that they did sell loans in Q4 (at 105.1% execution level) and did so again in Q4 (Q3CC):

we are selling $475 million in Q4 at a favorable execution. And we have a $2 billion forward flow lined up at favorable execution. We are also in the market, including in discussions with funds and accounts managed by BlackRock with respect to a $375 million securitization at favorable execution levels, and that is expected to close mid-November.

And amortizations (paydowns) ran at $2B in Q3. Management sees their non lending businesses as the growth driver for next year (Q4CC):

In the quarter, you saw that we drove 67% of our growth in absolute dollars from non-lending from the Tech Platform and from Financial Services. I think you should expect that type of trend to continue in that -- it's balanced or skewed more towards non-lending... So really strong prospects and Tech Platform, great trends in Financial services. So think about SLR and PL being additive to growth, not the driver of growth as we go into '24.

So in case capital becomes more of a constraint on its lending business they have other parts as growth drivers.

Conclusion

The selling point for SoFi is its unique business model where the whole is much more than the sum of the parts and the company leverages its infrastructure and membership to sell more products, reducing CAC and increasing LTV while increasing the touch points and customer data in a virtuous cycle that is inexorably driving towards growth and profitability.

Becoming a bank added another plank as it provides a cheap source of funds and customers alike while it has multiple ways to minimize credit risk exposure.

It's no wonder the rapid growth mainly is produced through gaining market share and we struggle to see what could short-circuit this, while at the same time, this points to secular growth that will continue even under unfavorable macro circumstances.

With the rapid deposit growth the company seems able to generate an ongoing cheap source of funds with which to expand origination but it can ultimately run out of excess capital.

The company's use of AFS accounting provides up-front accounting advantages that even out over the lifetime of loans so they provide an inflated picture during the present ramp of deposits and loans.

There are some regulatory risks attached to that if they don't sell loans but recently they've started selling loans again, possibly placating regulators.

Even if they become more capital constrained the company has considerable momentum in Financial Services and Technology Platform revenue growth is set to accelerate and management has designated these as their main growth areas for next year anyway.

The downside is that shares are still expensive, stock-based compensation is high and there are some risks attached to its lending business.

For further details see:

SoFi Is Winning Market Share