SOFI - SoFi: Seeking The Optimal Entry

2023-08-07 15:00:00 ET

Summary

- SoFi's Q2 2023 signifies strong growth with record Tech Platform and Financial Services results.

- Robust results indicated record Personal and increased Home loan originations.

- SoFi's growth trajectory is supported by adept deposit management, strategic cross-selling, and a focus on innovation and modernization.

- Its progressive outlook is supported by its focus on profitability in Q4, driven by lending income, efficiency, and product innovation.

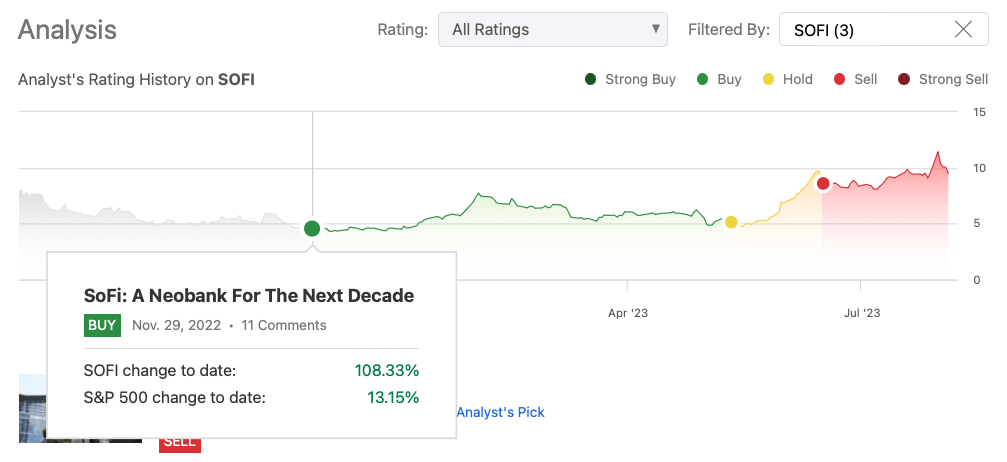

- I decided to exit my position, nearly doubling my money, booking all the profits, but looking to reenter in the price range of $7-$8.

Investment Thesis

In a stellar quarter, SoFi Technologies, Inc. ( SOFI ) demonstrated a solid YoY revenue surge, driven by record Personal and Home Loans. SoFi is setting the stage for sustained growth and innovation at the intersection of these domains.

I initiated coverage and invested in SOFI last November when the market sentiment was overwhelmingly negative. Half a year later, I decided to exit my position, nearly doubling my money, booking all the profits . Being a long-term investor, this short-term move goes against my investment philosophy, but I had to rotate the profits to more attractive opportunities with much more favorable risk/reward profiles.

Nevertheless, despite SoFi's strong Q2 2023 performance suggesting a bullish outlook, I am looking to reenter at lower levels when the time is right. Finally, d espite looming obstacles, the article explores how SoFi's outlook remains bullish for the long term, bolstered by technology and finance convergence.

{kind=link}

Author's SOFI Coverage

SoFi's Q2: Record Growth & Diversified Success

SoFi, in Q2 2023, exhibited remarkable growth, achieving record financial results in its Technology Platform and Financial Services segments. Record adjusted net revenue at $489 million (beating expectations by $15 million ), a 37% YoY increase, and adjusted EBITDA of nearly $77 million with 43% incremental margin and 16% consolidated margin underscore operational efficiency.

At the bottom line, it has delivered an EPS of negative $0.06 (beating expectations by $0.01), and non-interest income saw Q2 originations rise 37% YoY to $4.4 billion, buoyed by personal loan volume. Loan portfolio sales execution levels were strong, ranging from 101.2% to 104.5%.

Additionally, a $528 million rise in cash and cash equivalents showcased robust liquidity, complemented by deposits nearing $13 billion and a solid total capital ratio of 16% . Notably, profitability and EBITDA margin enhancement were evident, while balanced investment prioritization between growth and profitability persisted. Operating leverage in the Technology and Financial Services segments fostered margin expansion. Although a 70:30 reinvestment ratio is the long-term goal, market uncertainties prompted a strategic resource reallocation.

Further, Q2 results highlighted effective cost optimization and efficiency enhancement, apparent in decreased functional expense lines. Sales and marketing expenses decreased by 300 basis points YoY, displaying improved cost management. Similarly, technology and product development costs were reduced by 200 basis points, reflecting efficient resource allocation.

Notably, diversification was critical to solid financial performance, as both the Technology Platform and Financial Services segments significantly contributed. SoFi added 584,000 members in Q2, totaling 6.2 million, a 44% YoY increase. The Financial Services segment's net revenue more than tripled YoY to $98 million, driven by member growth, cross-buying, and effective monetization. The Tech Platform reported record net revenue of $88 million, up 4% YoY, driven by Galileo account expansion. Lastly, Financial Services saw an impressive 223% YoY net revenue increase to $98 million, propelled by diverse financial products.

Earning Presentation (SoFi)

Lending Operations Soar: +25% YoY Growth & Record-Breaking Originations

SoFi recently reported a robust performance in its Lending operations, with lending products obtaining a +25% YoY growth. The Lending segment achieved an impressive adjusted net revenue of $322 million, with noteworthy growth in the Personal Loans division, which originated a record $3.7 billion. The company's commitment to stringent credit standards and reliable underwriting processes translated into a reduced net charge-off rate.

Additionally, the Home loan sector saw a nearly threefold increase in originations, benefiting from enhanced capacity and capabilities. Within the Lending segment, Q2 demonstrated a 29% rise in adjusted net revenue, primarily driven by a remarkable 103% surge in net interest income. This growth was fueled by a 17% uptick in average interest-earning assets and a substantial 289 basis point increase in average yields.

As a result, the net interest margin expanded to 5.74%, marking a 50 basis point improvement YoY and a 26 basis point increase from Q1 2023. This positive trend showcased SoFi's adeptness in maintaining higher loan yields compared to prevailing market rates, reflecting effective pricing strategies.

Earning Presentation (SoFi)

However, the Lending segment faced challenges influenced by market dynamics, such as interest rates, charge-offs, and prepayments, which impacted net interest income. Notably, non-interest income in this sector dipped due to fair market value write-downs attributed to rising interest rates and increased dollar amount of PL write-offs.

Despite a rise in dollar charge-offs, the annualized charge-off rate for Personal Loans decreased to 2.94%, underscoring successful risk management strategies. The company's ability to hold loans for extended periods is poised to amplify net interest income and bolster Lending segment revenue.

SoFi Bank, a pivotal arm of the company, reported over $63 million of GAAP net income with a solid 17% margin. The strategic bank license facilitated profitability by optimizing net interest income and leveraging cost-effective deposits for loan funding.

SoFi's Student Loan Business Outlook Is Positive

Regarding Personal loan and Student Loan businesses, factors influencing these businesses include adjustments in discount rates and spread-related changes. Notably, actual default rates in Q2 were lower than expected, signaling the potential for reduced losses. The Student Loan segment also experienced fair market value markup reductions due to shifts in discount rates and prepayment assumptions. Realized Q2 annual default rates in this segment were significantly below estimates, indicating a favorable outlook for losses.

Despite the upcoming end of the moratorium, SoFi remains optimistic about the student loan refinancing market, as the company has maintained strict credit standards and emphasized loan quality. In Q2, SoFi announced that its loan applicants' weighted average income and FICO score were $163,000 and 768 , respectively. With many Americans carrying student loan debt, the potential for refinancing remains promising.

Finally, the company foresees a recovery in student loan refinancing demand post-September, contributing to a stronger financial performance in Q4.

Growth Trajectory: Adept Deposit Management & Strategic Cross-Selling

SoFi exhibits favorable growth prospects across various dimensions. The company's strength lies in its adept management of deposits, driven by competitive APY rates on SoFi Money, which has fueled substantial deposit growth through direct deposit customers.

This robust deposit base, coupled with the unique advantage of being a loan originator and a bank, positions SoFi to efficiently harness deposits for profitability even amid fluctuating rates and heightened competition. SoFi's commitment to maintaining a high-quality deposit acquisition strategy bolsters its position in the APY market.

Anticipated revenue growth is expected to follow a gradual trajectory, with the potential for acceleration in Q4 due to contributions from new partnerships. The company's focus on innovative technology solutions and modernization capabilities affords it a competitive edge, fostering sustained growth.

The member base's impressive 44% increase underscores SoFi's robust growth. Remarkably, the products per member ratio hold steady at 1.5 despite rapid member expansion, a testament to the skillful balance between acquisition and adoption. This equilibrium is expected to persist, possibly rising as member growth stabilizes. The objective is cultivating deeper member relationships, potentially translating into multiple product adoptions per member over time.

Earnings Presentation (SoFi)

Finally, the strategic significance of cross-selling is evident in SoFi's approach. By leveraging data from products such as SoFi Money, the company identifies avenues for cross-buying, enriching members' financial well-being. The emphasis lies on nurturing trust, broadening product portfolios, and delivering guidance for significant financial decisions throughout a member's lifecycle.

Can SoFi's Profitability Vision Redefine Finance's Future

SoFi's forward trajectory has a focus on growth and profitability. The company envisions achieving GAAP profitability by Q4, propelled by robust lending net interest income, enhanced efficiency, and positive contribution profit in the Financial Services segment. This optimism is bolstered by their commitment to innovation, evident through recent product launches like SoFi Travel and their expansion into new verticals and geographies via their Technology Platform.

In the upcoming months, SoFi aims to deliver adjusted net revenue ranging from $1.025 billion to $1.085 billion and adjusted EBITDA between $180 million and $190 million. The annual projections for 2023 forecast revenues of $1.974 billion to $2.034 billion, along with adjusted EBITDA of $333 million to $343 million. These figures imply a substantial 40% to 44% incremental adjusted EBITDA margin for the full year, underscoring their pursuit of profitability.

Also, the company's comprehensive marketing approach and effective customer acquisition strategies play a pivotal role in its ongoing momentum. Addressing balance sheet dynamics, SoFi anticipates maintaining robust asset growth, particularly in Personal Loans, despite the impact of amortization resulting from paydown's.

A shift towards student loan refinancing might influence net interest margin ((NIM)), with potential pressure stemming from increased costs of funds and pricing strategies. However, SoFi plans to mitigate this through prudent pricing aligned with the forward curve and a balanced approach between loan origination and deposit growth.

Interestingly, the strategic evolution of the Galileo platform towards substantial partnerships indicates a deliberate shift towards larger, more impactful collaborations. This strategic direction aligns with their long-term vision of leveraging cutting-edge technology and cloud-based infrastructure to attract significant institutional clients.

Finally, prominent institutions' growing interest in innovative, real-time, and regulatory-compliant financial technology solutions signals a burgeoning demand that SoFi is well-positioned to cater to.

Awaiting Optimal Entry Points For Strategic Accumulation

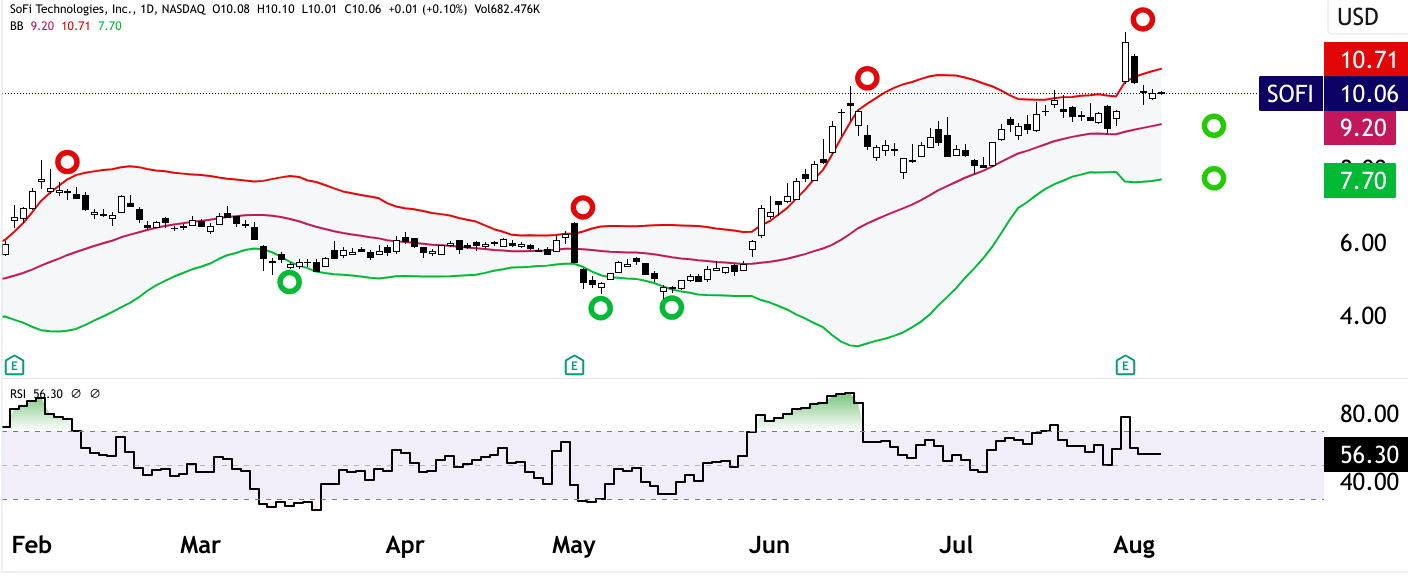

As observed from the price chart of SoFi's stock, it is trading near 2023's high of around $10.50. But based on technical analysis, it has not reached the optimum buying zone even after dropping from the high of $11.70.

SoFi's stock can be accumulated from $9.20 moderately to below $7.70 aggressively once the price drops below the lower limit of the Bollinger Band (based on a 31-day moving average).

Finally, filtering the price state through the Relative Strength Index ((RSI)), based on the ten-day moving average, can mean waiting to initiate accumulation until the RSI level goes below 50 and, ideally, below 30.

{kind=link}

tradingview.com

Takeaway

In conclusion, SoFi's robust Q2 2023 performance signals a bullish outlook. Strong growth in technology platforms and Financial Services, record revenues, and adept risk management showcase resilience. Competitive APY rates and deposit growth ensure profitability amid rate changes. Member expansion, cross-selling, and innovation drive sustained growth.

The technical analysis supports stock accumulation around optimal levels. SoFi's strategic convergence of technology and finance positions it for continued success, aiming for GAAP profitability by Q4 and ambitious revenue targets. As the field of finance evolves, SoFi's unique position and focus on growth, innovation, and profitability may continue to yield solid value growth.

For further details see:

SoFi: Seeking The Optimal Entry