SOFI - SoFi Technologies: Emerging From Unprofitability

2023-11-29 06:06:27 ET

Summary

- SoFi achieved record revenue and adjusted EBITDA, with 67% of growth coming from non-lending businesses.

- The company added 717,000 new members and experienced its highest quarter ever of new products.

- SoFi raised its full-year 2023 guidance, expecting continued strong growth and profitability.

- Though recently unprofitable, SOFI is stabilizing quarter by quarter. Based on my calculations, the current valuation indicates a potential upside of >35% in the next 12 to 15 months.

Introduction

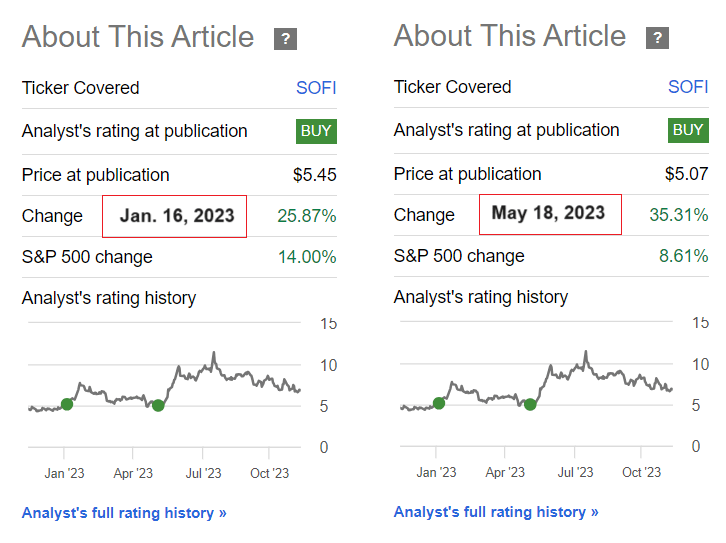

I initiated coverage of SoFi Technologies (SOFI) in January 2023 with a 'Buy' rating and confirmed this again in May 2023 . Since then, my calls have performed well, even though SOFI is currently trading >40% off its high [considering this year's timeframe].

Seeking Alpha, the author's coverage of SOFI stock

{kind=link}

Today I have decided to test the strength of my thesis again, as the upside potential I derived last time has already been reached.

Recent Financials

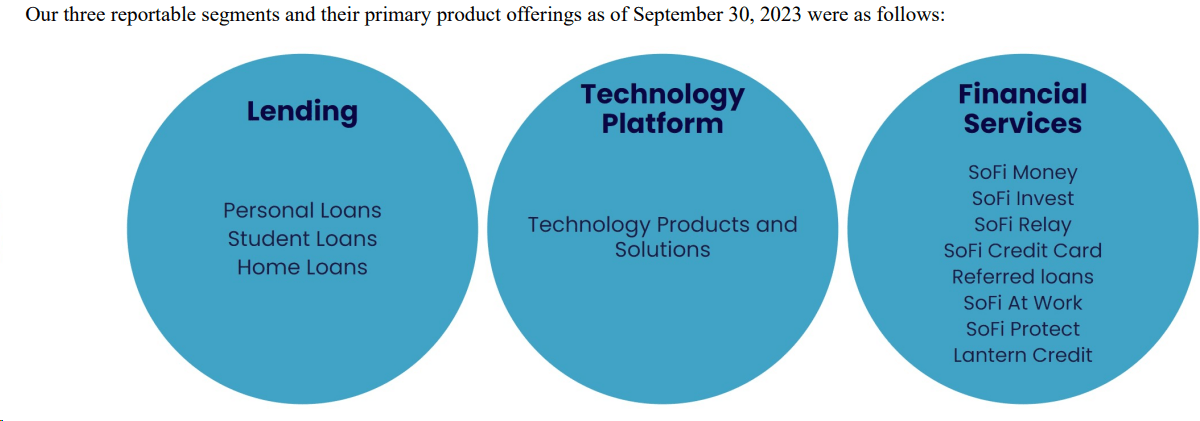

SoFi Technologies, Inc. is a financial services company headquartered in San Francisco, California. Operating through three segments-Lending, Technology Platform, and Financial Services-SoFi offers a variety of financial products and services, including personal loans, student loans, home loans, and banking products. The company also operates Galileo, a technology platform serving financial and non-financial institutions, and Technisys, a cloud-native digital and core banking platform. SoFi provides members with checking and savings accounts, debit cards, and investment opportunities through SoFi Invest.

{kind=link}

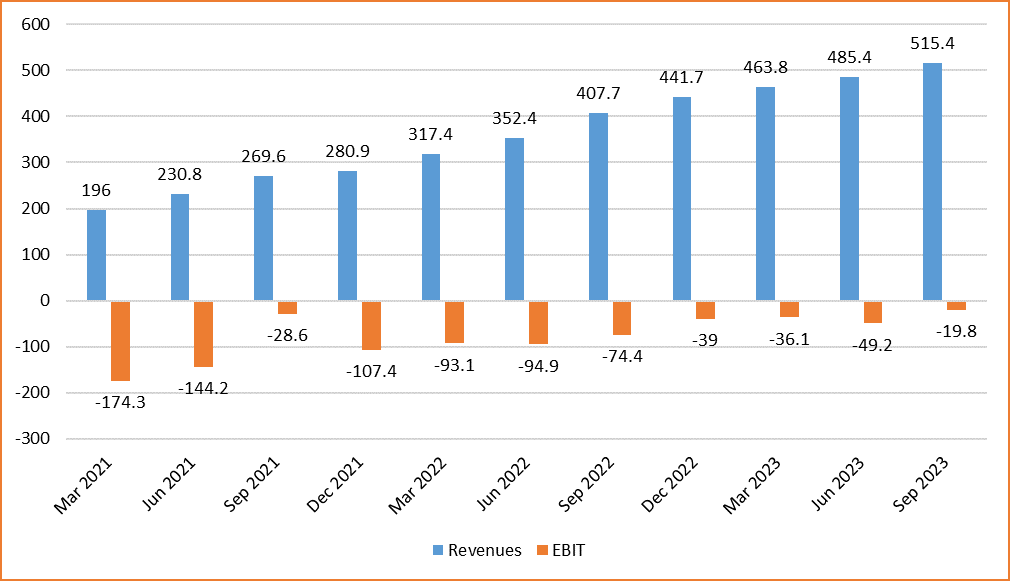

Despite global challenges, SoFi achieved its 10th consecutive quarter of record revenue and a fifth consecutive quarter of record adjusted EBITDA in Q3 FY2023 . Notably, 67% of the growth in adjusted net revenue came from non-lending businesses, specifically the Technology Platform and Financial Services segments. The Financial Services segment achieved positive contribution profit for the 1st time, contributing to overall profitability even amid aggressive investments.

SOFI's IR materials, author's notes

{kind=link}

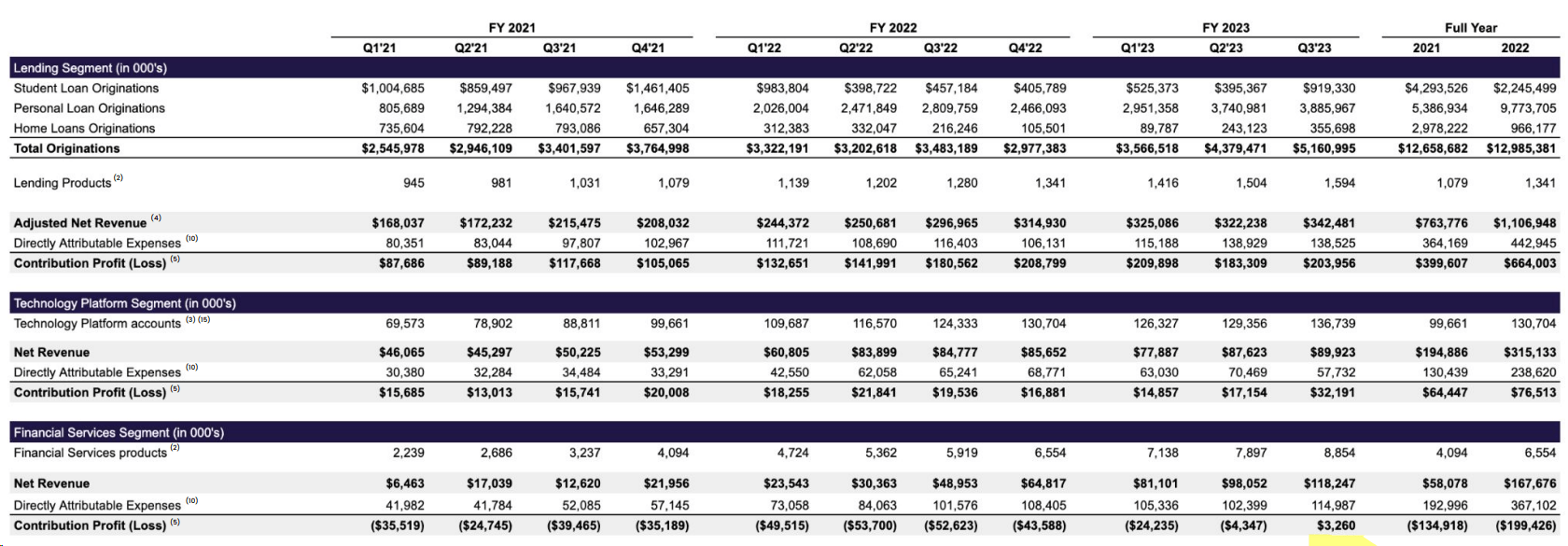

Within the Lending segment, adjusted net revenue grew 15% YoY to $342 million, with strong performance in personal loans, student loans, and home loans. The net interest income in the Lending segment grew by 90% YoY to $265 million, demonstrating a robust margin improvement. SoFi's lending capacity remained robust, with over $27 billion in total capacity to fund loans.

The Technology Platform segment reported net revenue of $89.9 million, with a focus on diversified growth strategies, including new vertical segments, products, and geographies. The segment made significant strides, and its growth rate was expected to accelerate into Q4.

In the Financial Services segment, net revenue grew 142% YoY to $118 million. Despite continued heavy investment in credit card and investment businesses, the segment achieved a positive contribution profit of $3.3 million. SoFi's differentiation in product selection, including enabling investment members to participate in IPOs, contributed to increased brand awareness and member growth.

The firm's total adjusted net revenue of $531 million, a 22% YoY increase, and adjusted EBITDA of $98 million, representing a 48% incremental margin and a record 18% consolidated margin. The Financial Services segment reported a positive contribution profit of $3.3 million, a significant improvement from the previous quarter. SoFi Bank reported $84.8 million of GAAP net income, reinforcing the company's path to overall GAAP profitability by Q4.

SoFi's unique value proposition continued to attract high-quality deposits, increasing by a record $2.9 billion sequentially to nearly $15.7 billion in total deposits. More than 90% of consumer deposits are from direct deposit customers, providing some sort of stability. Tangible book value grew for the third consecutive quarter by a record $68 million at the consolidated level.

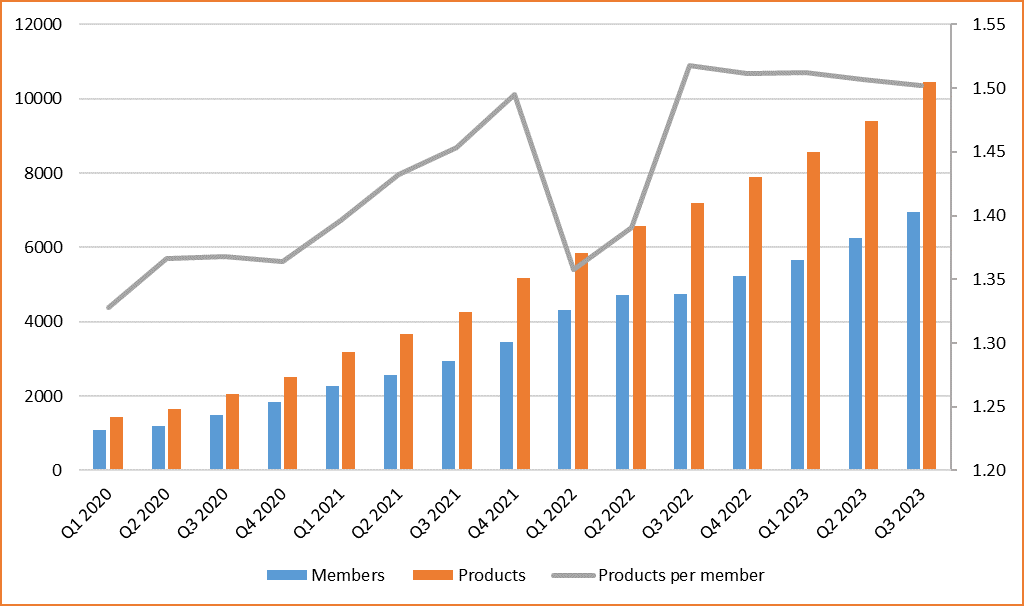

In terms of members and products, SoFi added 717,000 new members in Q3, reaching nearly 7 million, a 47% YoY increase. According to the management commentary , the company experienced its highest quarter ever of new products, bringing the total to $10.4 million at quarter-end, growing by 45% YoY. Despite rapid member growth, products per member remained at 1.5x, potentially showcasing the appeal of SoFi's product suite.

Author's calculations, SOFI's data

{kind=link}

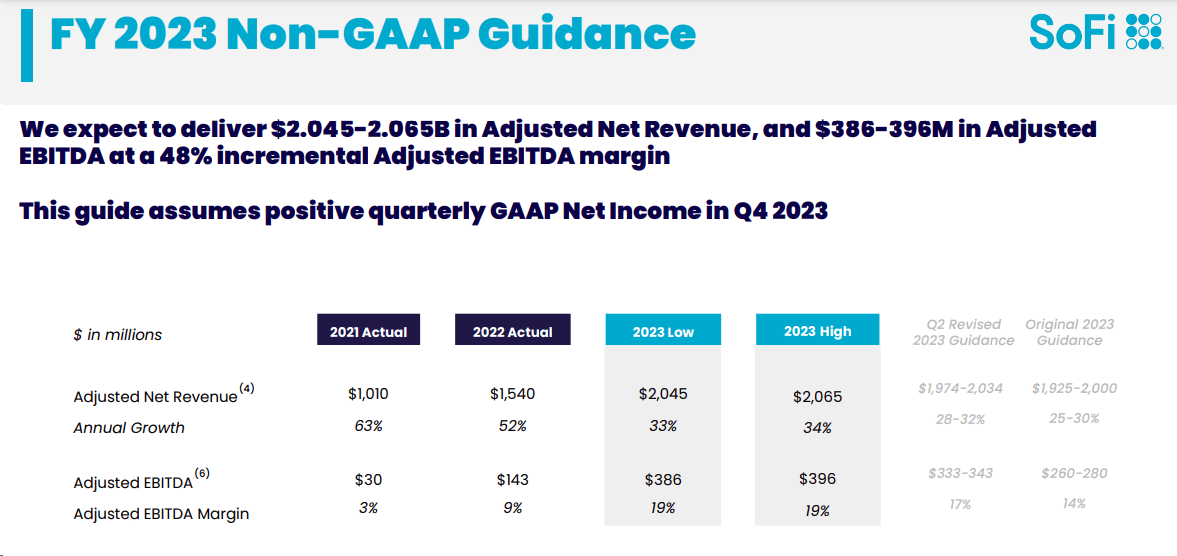

Looking ahead, SoFi remains well-capitalized with strong liquidity, a diverse set of revenue streams, and a focus on high-quality credit underwriting. The company raised its full-year 2023 guidance, expecting adjusted net revenue of $2.045-2.065 billion and full-year EBITDA of $386-396 million, reflecting continued strong growth and profitability.

{kind=link}

From what I can see from the company's recent results, SOFI really does seem to be one of the highest-quality growth companies in the entire fintech industry right now. According to third-party reports , the global market for financial services is expected to grow at a CAGR of 7.5% over the next 10 years - that's a healthy backdrop for the firm. And looking at how actively SOFI is expanding, I expect the company's share to only increase in the future.

But what about SOFI's valuation?

SOFI's Valuation & Expectations

SOFI is still an unprofitable company, but its operating performance shows clear signs of breaking even in the near future - the recent increase in guidance confirms this assumption.

Excel, author's work, Seeking Alpha data

{kind=link}

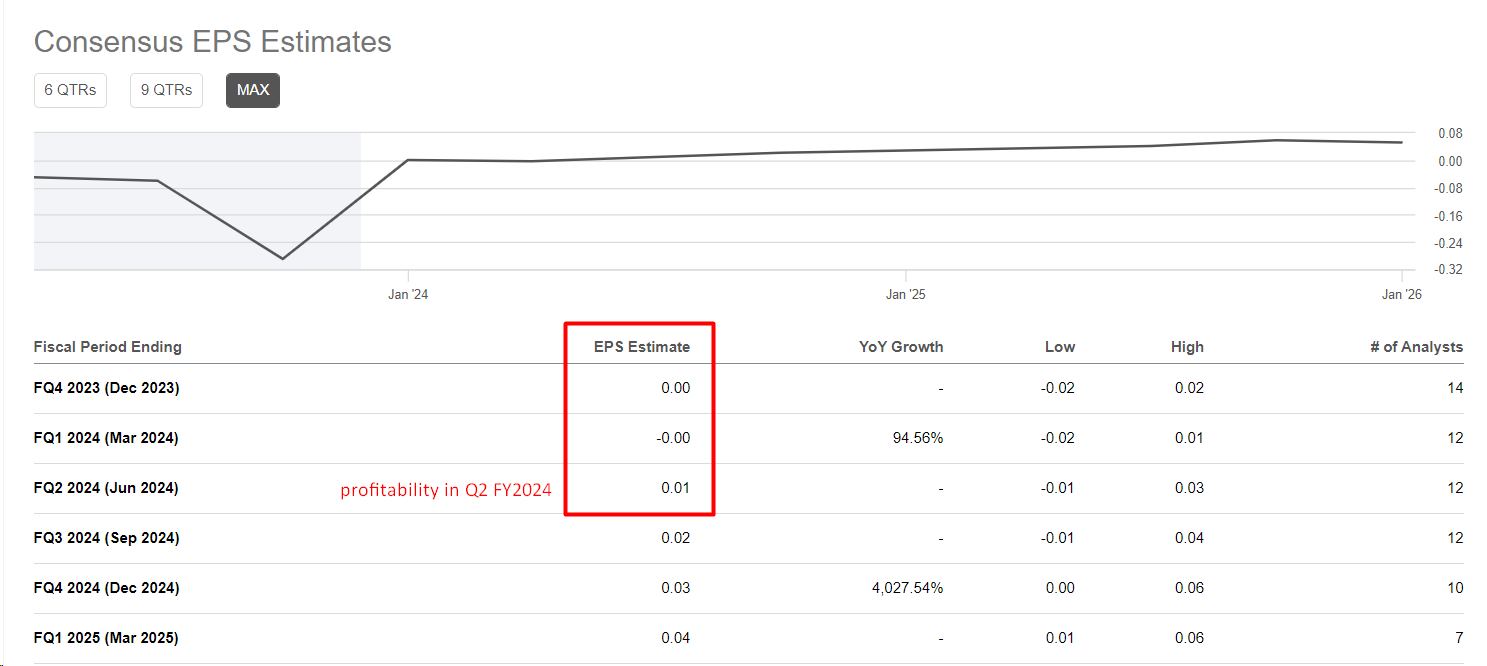

Wall Street expects FY2023 to be the last non-profitable year for SOFI, and we should see a first loss-free quarter in Q4 FY2023:

{kind=link}

So we cannot yet value SOFI based on its P/E ratio, but we do have a forward P/S ratio in our analytical arsenal, according to which SOFI cannot be called 'dirt cheap' compared to its peers:

However, a comparison with other companies would be unfair if it didn't also take into account the expected growth rates. Since we're talking about revenue-related valuation multiples, let's look at next year's sales growth.

As you can see, SOFI is second only to Upstart Holdings ( UPST ) in terms of expected revenue growth, which is ~24.25% more expensive than SOFI in terms of forward P/S ratio. According to consensus data, SOFI should achieve sales growth of ~16% over the next 5 years, while UPST should only achieve a CAGR of 17.5% over the next 4 years. At the same time, UPST will continue to be a more expensive company during this period according to FWD implied P/S ratios.

| Expected growth in sales |

| First-year |

| Final year |

| # years |

| CAGR |

| UPST [] |

| 506.49 |

| 976.00 |

| 4 |

| 17.8% |

| SOFI [] |

| 2.05 |

| 4.31 |

| 5 |

| 16.0% |

Source: Author's calculations, Seeking Alpha data

If we look at EPS expectations, the overall picture is clearly in favor of SOFI. Both companies should report their first positive EPS numbers in FY2024 according to Wall Street forecasts. UPST doesn't have enough forecast data, so I only take 3 years (and 4 years for SOFI, as in the example above). Based on these inputs, SOFI's earnings per share growth rate should exceed UPST's by almost a factor of two, which is very fast.

| Expected growth in EPS |

| First-year |

| Final year |

| # years |

| CAGR |

| UPST |

| 0.35 |

| 1.31 |

| 3 |

| 55.3% |

| SOFI |

| 0.05 |

| 0.72 |

| 4 |

| 94.8% |

Source: Author's calculations, Seeking Alpha data

I believe SOFI should trade at a P/E of 3.5x by the end of FY2024, maintaining its high quality and rapid operational growth. This expectation of mine in part includes the stock's sensitivity to a very likely Fed rate cut (lower rates lead to higher multiples). If the company can then reach the midpoint of the consensus FY2024 revenue forecast of $2.54 billion, we should see a market cap of $8.89 billion, 35.16% higher than today.

The Bottom Line

Of course, investing in SoFi Technologies, Inc. comes with its share of risks. First off, the stock is susceptible to market ups and downs, regulatory changes, and the impact of interest rate fluctuations. Second, competition in the financial services sector, economic downturns affecting consumer behavior, and credit risk in the loan portfolio are also factors to consider. Additionally, potential disruptions in technology, challenges in executing business strategies, reliance on partnerships, and risks associated with goodwill and intangible assets add complexity to the investment landscape. So it's crucial for investors to do thorough research, assess their risk tolerance, and stay updated on industry dynamics.

Despite the many existing risks, SOFI still seems to me to be a very good investment over the next 3-5 years. While the company is emerging from unprofitability (it seems to have little time left to do so), its business is becoming more stable from quarter to quarter and the current valuation level suggests an upside potential of >35% over the next 12 to 15 months, according to my calculations.

Therefore, I reiterate my 'Buy' rating again this time around.

Thanks for reading!

For further details see:

SoFi Technologies: Emerging From Unprofitability