SOFI - SoFi Technologies: Rapid Growth Might Be Worth The Risk

2023-12-26 14:41:46 ET

Summary

- SoFi Technologies is a diverse financial technology firm that offers a wide range of services, including loans, credit cards, and investment products.

- The company has experienced significant growth in revenue and user base, with net revenue nearly tripling from 2020 to 2022 and the number of members growing to 6.96 million recently.

- While the company faces challenges in generating profits, its long-term prospects are promising, especially considering the potential for increased demand from younger generations and the ongoing wealth transfer.

When it comes to the new world financial technology firms that are out there today, many are single products or simple platforms with only a few different offerings on them. One company that has avoided that kind of designation is SoFi Technologies (SOFI), a firm that considers itself to be a one-stop shop for financial services. In recent years, the business has achieved fantastic growth on both its top and bottom lines. Some of this growth is likely temporary since it is based on elevated interest rates that will likely start dropping sometime next year. But the vast majority of its growth looks to be here for the long haul. The company does have some issues generating profits. But when you consider just how rapidly the enterprise is expanding and the potential that offers investors down the road, the company makes for a decent long-term prospect for those who don't mind paying for growth.

A diverse firm

Operationally speaking, SoFi Technologies is a rather complex organization. The firm offers a multitude of financial services for its clients. Examples include brokerage accounts, credit cards, various financial technologies, different types of loans, and more. At the end of the day, however, management has done well to consolidate all of these different pieces of functionality under three different operating segments. The first of these is the Lending segment, which originates and services personal loans, student loans, and home loans. The second is the Technology Platform segment, which consists of Galileo that the company acquired in 2020 and Technisys, which it acquired in 2022. Galileo provides certain services to financial and non-financial institutions, while Technisys is a cloud native digital and core banking platform, their focus is mostly on the Latin America market. And lastly, there is the Financial Services segment, which provides investing services, credit cards, loan referrals, and so much more, to its customers.

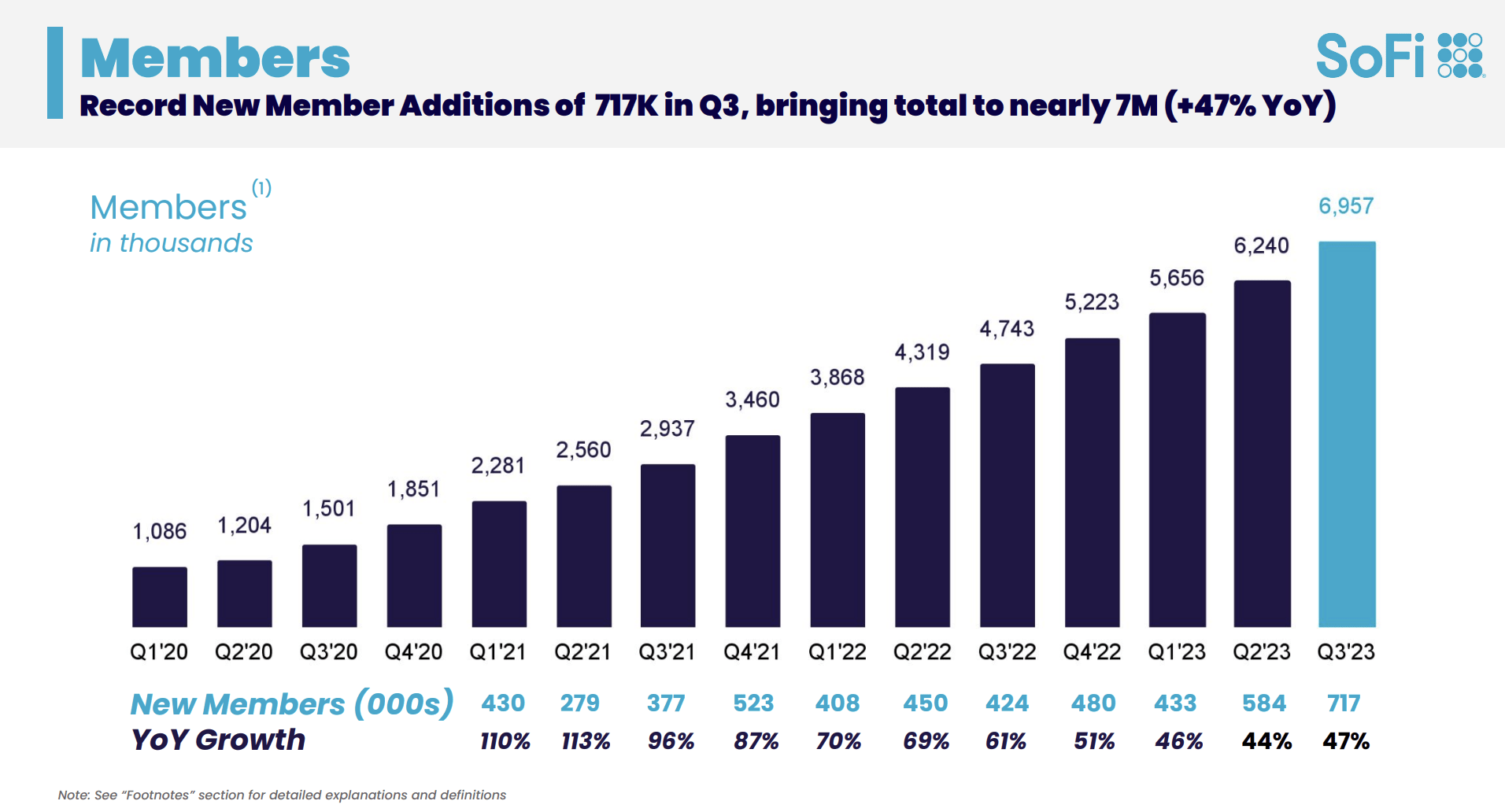

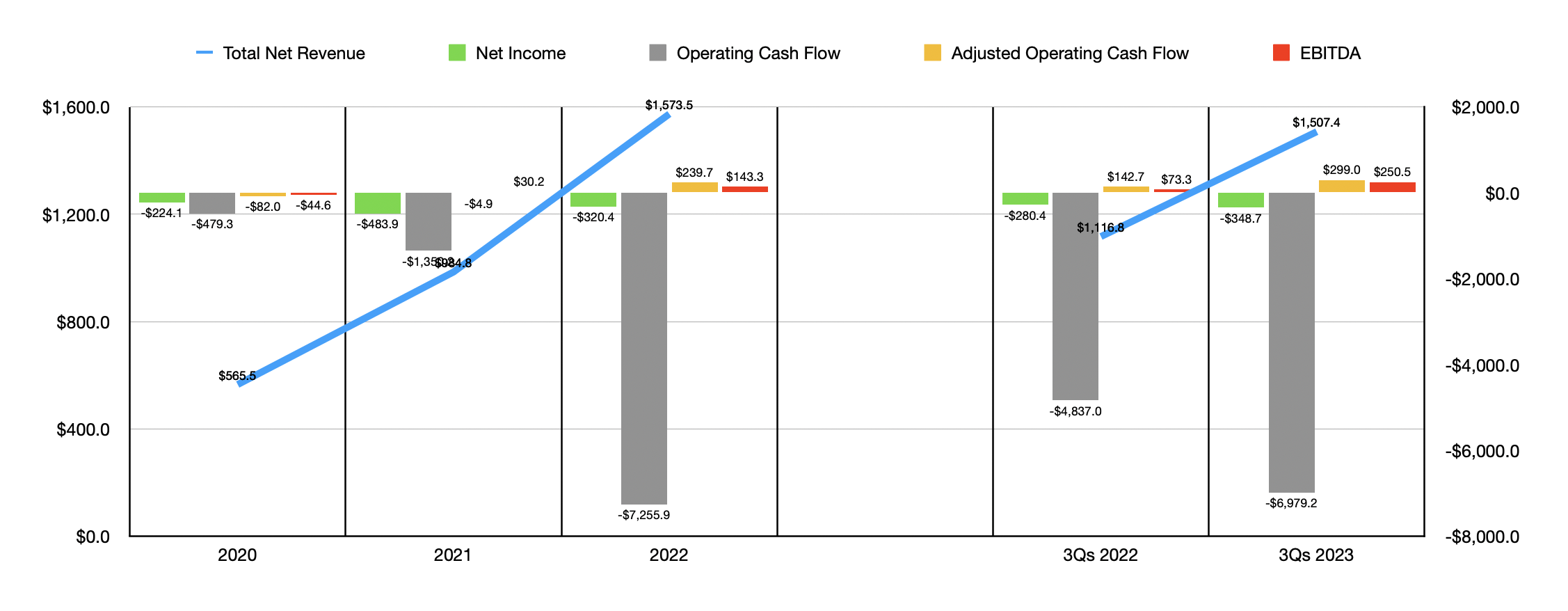

Truth be told, this only touches the surface of what the business does. But instead of digging into that kind of info that is readily available, I think it would be more helpful to look into just how well the company has performed over the past few years. It would probably be best to start with revenue. From 2020 through 2022, net revenue for the company nearly tripled from $565.5 million to $1.57 billion. There are different ways that we can look at this as well. Perhaps the simplest is to look at just how many additional individuals have come to utilize the company's services. At the end of the first quarter of the 2020 fiscal year, the company had about 1.09 million members who had used its services. This number has only continued to grow since then, hitting 5.22 million by the end of the fourth quarter of last year before shooting up further to 6.96 million as of the end of the third quarter. In fact, the 717,000 new members that the company reported during the third quarter represented the largest increase in new members in the span of a single quarter.

{kind=link}

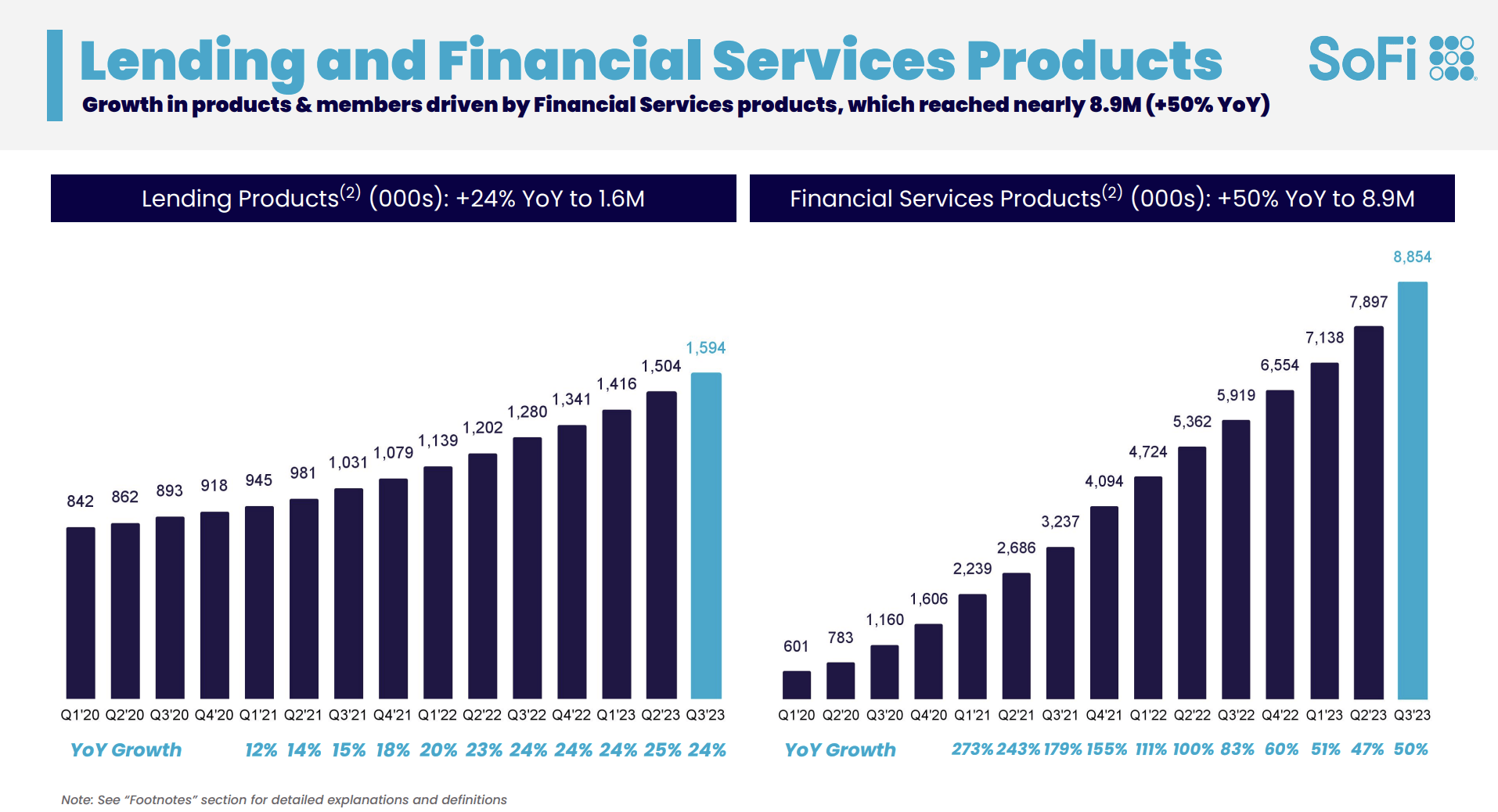

There are other measurements that are not financial in nature that management goes by. But honestly, I don't view all of these as being relevant. For instance, there are a number of products that the company sells. This is basically defined as any particular feature that any one user ends up paying for. While the company does record this on a quarter over quarter basis, It really just is an aggregate of all of the products ever sold by the enterprise. I view a product that was sold five or six years ago as not being relevant today. Though a case could be made that seeing an increase in products from one quarter to the next does have some value in it. And in that regard, as the image below illustrates, the company has been doing quite well.

{kind=link}

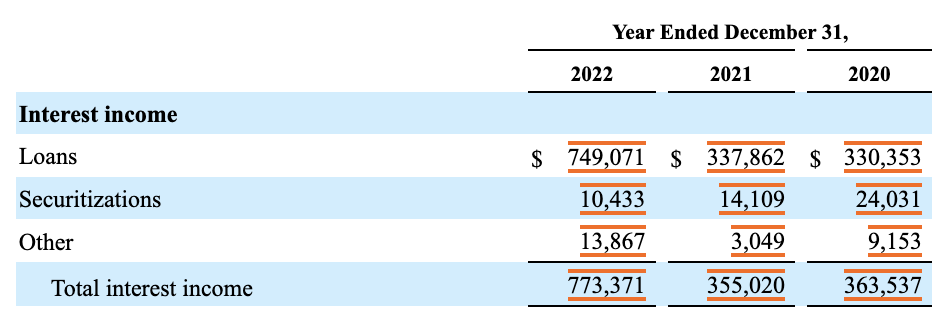

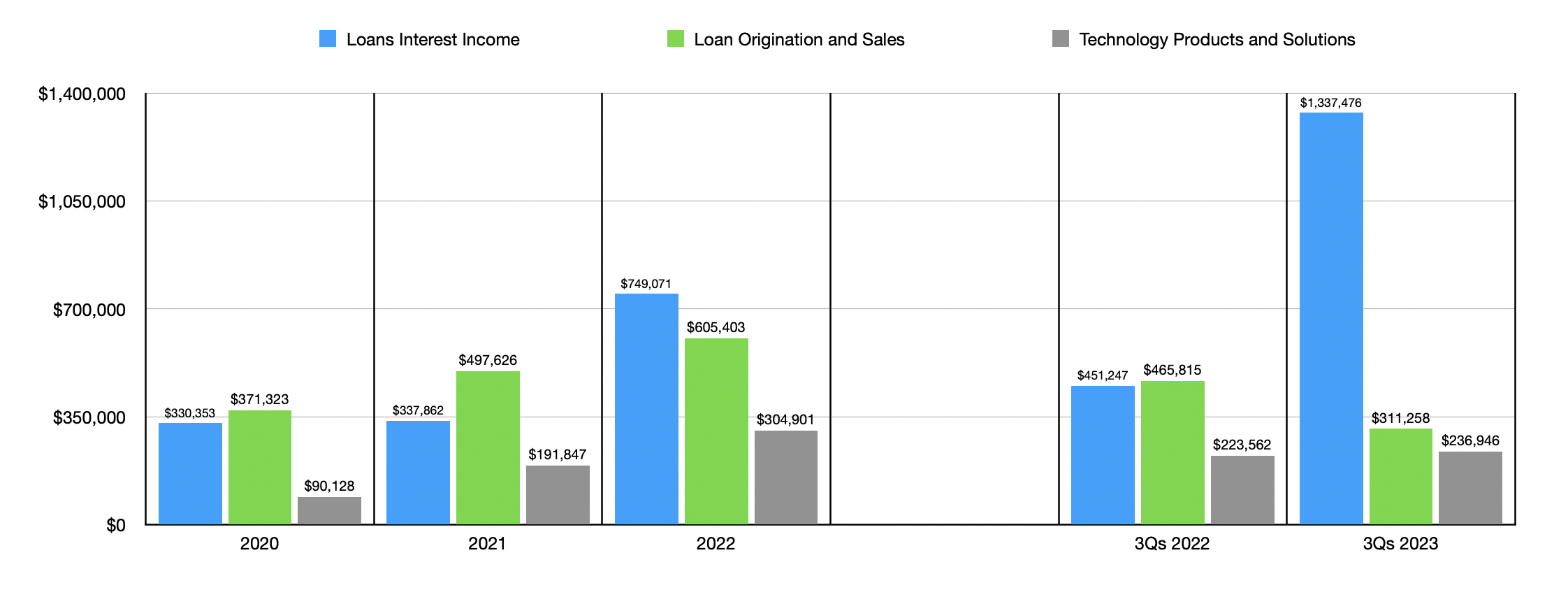

When it comes to the financial picture, growth has really been seen across a few key areas. The first of these falls under interest income associated with loans that the company has generated in recent years. From 2020 to 2022, this has jumped from $330.4 million to $749.1 million. As the company has further established itself as a relevant player in the financial industry, it has done well to grow the value of loans on its books that it has originated. In 2022, for instance, the company had an average balance for its loans of $9.20 billion. That's nearly double the $4.78 billion reported in 2020.

{kind=link}

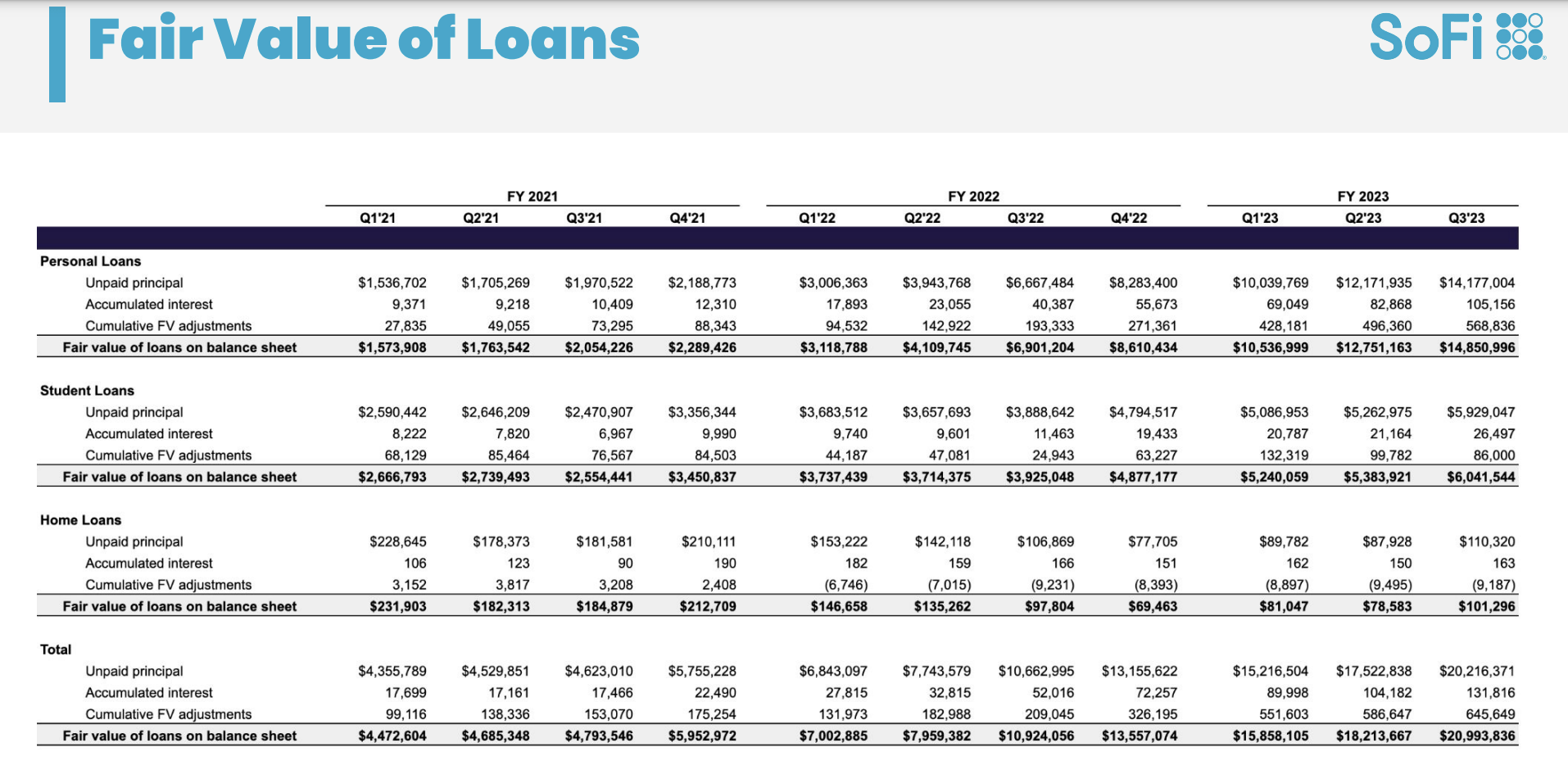

Most of the increase in the value of loans in that three-year window came from 2021 to 2022, with the company reporting a surge in personal loans from $2.29 billion to $8.61 billion. Student loans also managed to grow from $3.45 billion to $4.88 billion. At the same time, average interest rates charged to these loans increased because of a rise in interest rates. In 2020, they totaled 6.91% per annum. In 2022, they totaled 8.14%. To put this disparity in perspective, applying a 1% change in the effective interest rate on loans would result in an extra $135.6 million in income for the company each year.

{kind=link}

Next, we have something that is tied directly in with the loan activity that the company has. You see, it also collects fees when it originates loans. Plus it generates revenue from selling off certain loans. Back in 2020, the firm generated $371.3 million from these activities. By 2022, that number had grown to $605.4 million. And finally, we have the entire Technology Products and Solutions segment, where it earns fees for providing its platform as a service for both financial and non-financial firms. Account growth, combined with increased activity associated with the company's existing technology solutions clients, and revenue generated from its absorption of Technisys last year, were all responsible for revenue under this segment growing from $90.1 million to $304.9 million in the past three years.

{kind=link}

The bottom line has been a bit more complicated for the company. If you look back at the first chart in this article, you can see that the firm continues to generate significant net losses. A lot of this has to do with scaling and stock-based compensation. A better metric, then, might be cash flow. Operating cash flow is significantly negative because of how the company does its books. But if we adjust for changes in working capital, we actually see a pretty consistent improvement from negative $82 million to $239.7 million. Meanwhile, EBITDA for the company has expanded from negative $44.6 million to $143.3 million.

{kind=link}

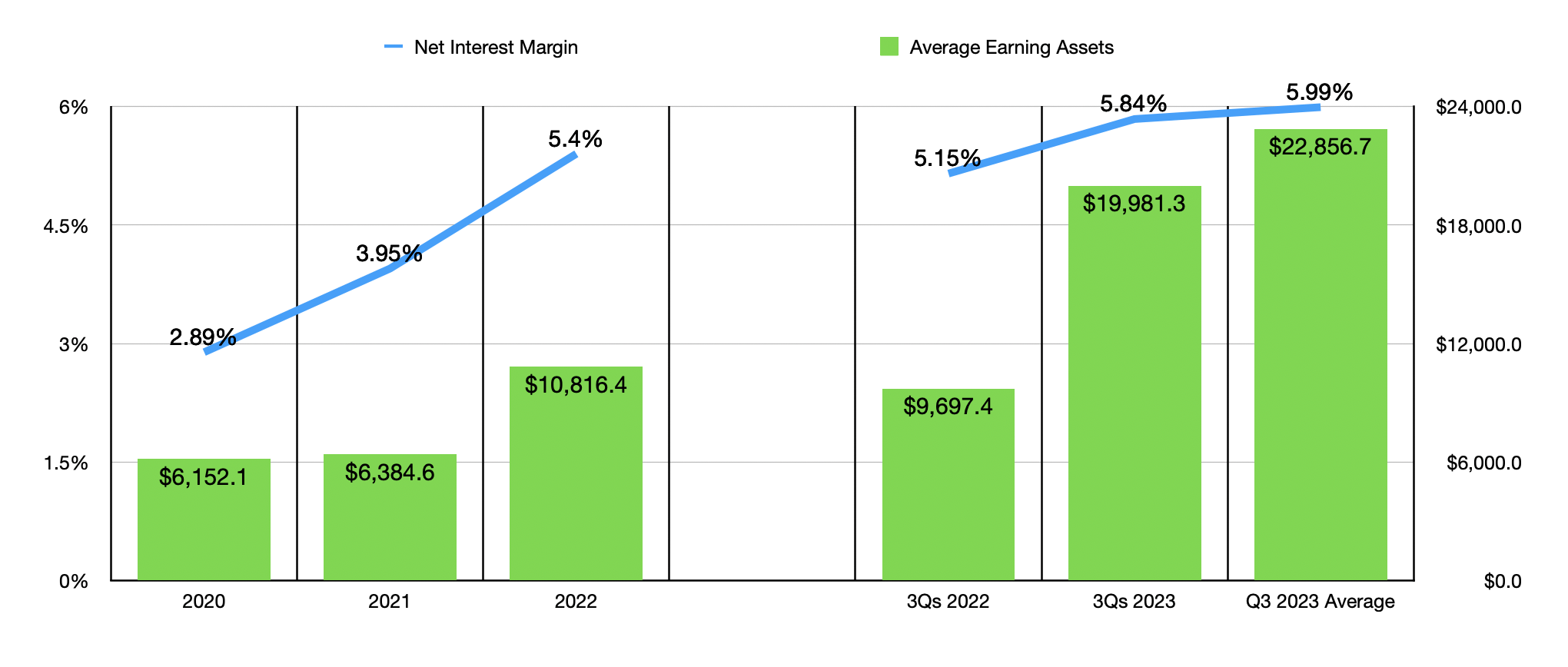

The same drivers of growth, for the most part, that have led the way in recent years continue to play a role for the company so far in 2023 . For the first nine months of this year, net interest income totaled $872.1 million. That dwarfed the $375.5 million reported for the same time last year. A jump in average earning assets from $9.70 billion in the first nine months of 2022 to $19.98 billion in the first nine months of this year, combined with an increase in the company's net interest margin from 5.15% to 5.84%, caused interest income associated with loans to grow from $451.2 million last year to $1.34 billion this year. The Technology Products and Solutions portion of the company still happened to grow, though only modestly from $223.6 million to $236.9 million. The only weakness amongst the big three revenue sources has been loan origination and sales revenue. This managed to fall from $465.8 million to $311.3 million. The biggest contributor there was a $223.7 million swing associated with the write-off expense of whole loans rising thanks to the company experiencing higher loan volumes and dealing with longer loan holding periods than in the past.

Despite these troubles, SoFi Technologies continued to see its bottom line results improve on a year-over-year basis. The one exception to this was net income, which worsened materially from the first nine months of last year to the same nine months of this year. However, adjusted operating cash flow grew from $142.7 million to $299 million, while EBITDA expanded from $73.3 million to $250.5 million. As things stand, management has some pretty high hopes for this year. They are currently forecasting EBITDA of between $386 million and $396 million.

{kind=link}

*$ in Millions

When it comes to the long-term picture, things are definitely looking up for SoFi Technologies. I say this for two reasons. First, the total value of interest-earning assets at the institution continues to expand and that's because of both a growth in the number of members utilizing the firm's services and, second, there's the fact that we are in the early stages now of a historic wealth transfer where about $84 trillion will be transferred from the oldest generation to the younger generations. Given the tech-savvy nature of the younger generations and the money troubles that these groups have already faced, it stands to reason that they will turn even more in the direction of technology, particularly if that technology can offer a one-stop shop for their needs. This doesn't mean that everything will go great. Next year, we are looking at three possible rate cuts from the Federal Reserve. Although a reduction in rates makes it more likely that borrowers will pay their debts, it also means that the company has to charge less for the loans that it originates. For instance, in the first nine months of this year, the average rate on its loans was 10.21%. That's up from the 7.51% reported one year earlier. When applied to the $17.52 billion in average loan balances that the company had in the first nine months of this year, that difference alone is $473.1 million in revenue.

Takeaway

In the long run, I suspect that SoFi Technologies will do just fine for itself. The company does have some issues, particularly when it comes to profits. But from an operational perspective, it is a quality firm that continues to grow at a nice rate. I don't see any reason why that growth should stop at any point soon. We might see some weakness in some areas such as when it comes to interest rates pulling back, but for those focused on the long haul, I wouldn't use that as a reason to not buy SOFI.

For further details see:

SoFi Technologies: Rapid Growth Might Be Worth The Risk