SOFI - SoFi Technologies Stock: Analyst Downgrade In The Spotlight

2024-01-04 07:00:00 ET

Summary

- I am of the opinion that SOFI's future EBITDA will be in line with expectations, considering the company's net interest margin outlook, good cost control, and its revenue diversification target.

- SoFi Technologies' shares are at a fair valuation based on my analysis of its P/B and EV/EBITDA valuation metrics.

- I still assign a Hold rating to SOFI, as I disagree with the KBW analyst's view that the stock is overvalued and that the company's EBITDA will be below consensus.

Elevator Pitch

I rate SoFi Technologies, Inc. (SOFI) shares as a Hold.

A Wall Street analyst recently lowered his rating for SOFI to Underperform (equivalent of a Sell), and SoFi Technologies' stock price fell by -13.9% on January 3, 2024 in response to the latest rating downgrade. This has prompted me to publish an update on SOFI.

Earlier, I highlighted that SOFI shares were fairly valued in my prior July 7, 2023, article . SoFi Technologies' share price rose by a modest +3.2% (source: Seeking Alpha price data) in the six months following my July 2023 write-up, which serves as a validation of my Neutral view of the stock.

In the current update, I assess if the sell-side analyst's recent rating downgrade for SoFi Technologies is justified. According to Seeking Alpha News' January 3, 2024 article , Keefe, Bruyette & Woods analyst Michael Perito has rated SOFI as an Underperform or a Sell on the basis that the stock "is trading at premium valuations with 15-20% downside potential to consensus EBITDA." This will be the focus of my latest update.

My analysis leads me to the conclusion that SOFI is deserving of a Hold rating, rather than the Sell rating that the Keefe, Bruyette & Woods analyst has assigned to the stock. In my opinion, SOFI can meet the market's financial expectations, but this has been factored into its valuations, which implies a Hold rating for SoFi Technologies.

Market's Expectations

Keefe, Bruyette & Woods analyst Michael Perito sees "more downside risks than upshots" and his financial forecasts for SOFI are "materially below consensus" as highlighted in that January 3, 2024, Seeking Alpha News article that I referred to above.

I disagree with the Keefe, Bruyette & Woods analyst's opinion regarding SoFi Technologies' financial prospects; I think that SOFI can meet the market's consensus EBITDA expectations.

The current sell-side consensus FY 2023 EBITDA projection for SOFI is $393.3 million (source: S&P Capital IQ ). This is pretty close to the mid-point of SoFi Technologies' FY 2023 EBITDA guidance at $391 million as indicated in its Q3 2023 results press release . The analysts also forecast that SoFi Technologies' EBITDA will grow by +45.6% to $572.5 million in FY 2024 as per S&P Capital IQ consensus data. I take the view that SOFI's actual FY 2023 and FY 2024 EBITDA are likely to be in line with the sell-side's forecasts.

SoFi Technologies' EBITDA Outlook

SOFI's EBITDA jumped by +121.3% YoY to $98.0 million in Q3 2023, which exceeded the sell-side analysts' consensus estimate of $63.6 million by +54.1% (source: S&P Capital IQ ). There are good reasons to believe that SoFi Technologies can maintain its strong EBITDA growth momentum for the foreseeable future.

Firstly, SoFi Technologies' net interest income outlook is favorable.

Net interest income for SOFI grew by +18% QoQ and +119% YoY to $345.0 million for the third quarter of 2023, as the company's net interest margin expanded by +13 basis points YoY and +25 basis points QoQ to 5.99% in the most recent quarter. As per S&P Capital IQ data, SoFi Technologies' Q3 2023 net interest income and net interest margin were +8.2% and 0.55 percentage points above expectations, respectively.

At the Stephens Annual Investment Conference in mid-November last year, SoFi Technologies guided that "we expect to maintain strong NIM (Net Interest Margin) going forward." At this November 2023 investor event, SOFI explained that factors like a "shift in the overall funding stack to being more deposit driven versus reliant on warehouse capacity" and the focus on "high prime or super prime customers" will drive its NIM expansion going forward.

Secondly, SOFI's top line is expected to become more diversified, which will lend stability to the company's future revenue.

The company noted at its Shareholder Q&A Session last month that it expects to derive half of its revenue from the Lending Segment, and generate the remaining half of its top line from the Technology Platform segment and Financial Services segment for FY 2024. In the medium to long term, SOFI sees the three business segments each contributing a third of the company's top line.

As a reference, the Lending, Technology Platform, Financial Services segments accounted for 62%, 16%, and 22% of SoFi Technologies' Q3 2023 top line, respectively. A diversification of SOFI's revenue base translates into lower volatility in the company's future top line, and improves its chances of achieving its future financial targets.

Thirdly, the company is doing a good job in managing expenses, especially sales and marketing costs.

Previously, SoFi Technologies shared at the November 2023 Stephens Annual Investment Conference that it has "made tremendous progress" in reducing its "customer acquisition costs", which supports its goal of delivering "longer-term target margins of 30% adjusted EBITDA margins and 20% GAAP net income margins." This is validated by SOFI's most recent quarterly financial performance.

SOFI disclosed at the company's Q3 2023 earnings call that its "sales and marketing" expenses "as a percentage of adjusted net revenue" decreased by "349 basis points" YoY in the latest quarter. The company attributed this improvement in cost efficiency to the increase in "unaided brand awareness and the scale (positive operating leverage)"

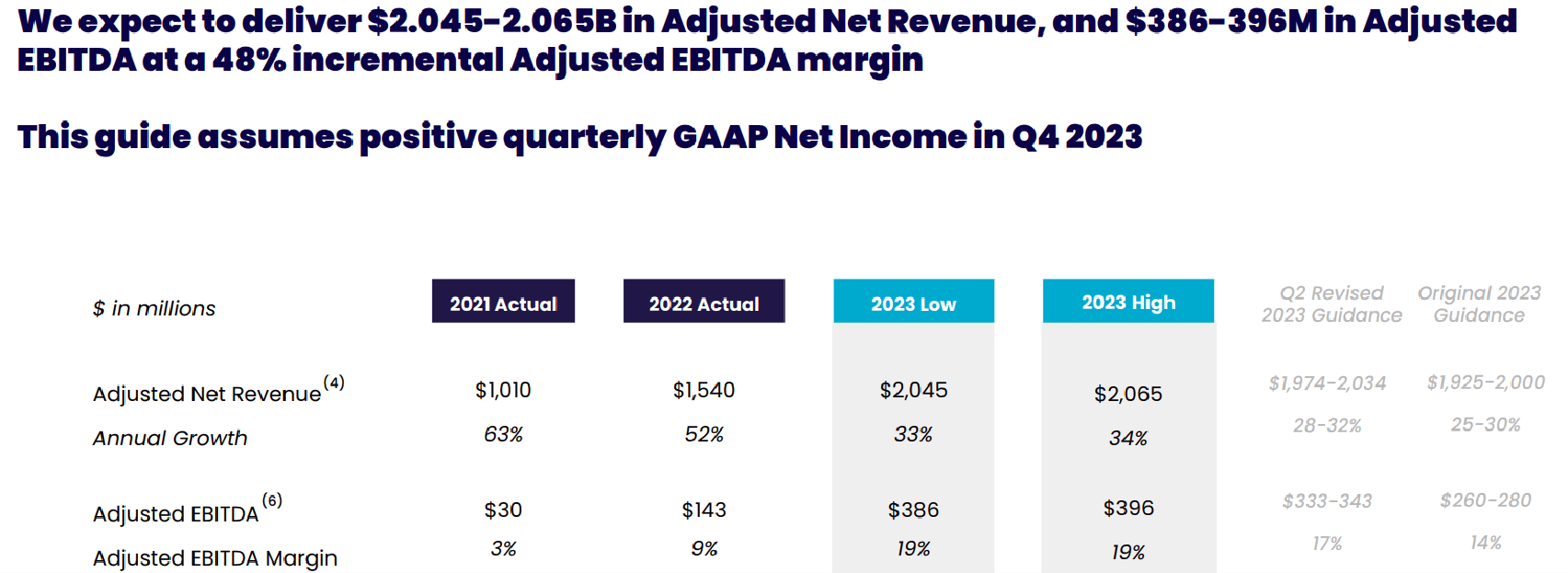

SoFi Technologies' Historical Financial Results And Forward-Looking Guidance

{kind=link}

As per the chart presented above, SOFI's EBITDA margin has been improving and the company has raised its FY 2023 EBITDA guidance in recent quarters. Notably, SoFi Technologies' FY 2023 EBITDA margin guidance of 19% is still way below its long-term target of 30%, which implies that there is lots of room for profitability improvement.

SOFI Stock Valuation

I also have a different view from the Keefe, Bruyette & Woods analyst, when it comes to SoFi Technologies' valuations. In the January 3, 2024 Seeking Alpha News article, the analyst Michael Perito is quoted as referring to SOFI's "recent (stock price) outperformance that took it to a premium valuation."

SOFI currently trades at a trailing P/B multiple of 1.58 times, which is more than twice the stock's historical all-time mean P/B ratio of 0.77 times (source: S&P Capital IQ ). But I am of the opinion that SoFi Technologies' shares are still fairly valued rather than being overvalued.

In my July 2023 update, I evaluated SoFi Technologies' valuations using the Gordon Growth Model, a comparison of SOFI's earnings multiple and earnings growth outlook. I will provide an update of my valuation analysis here.

As per the Gordon Growth Model, one arrives at a fair P/B metric for a stock by dividing (ROE minus Perpetuity Growth Rate) by (Cost Of Equity Minus Perpetuity Growth Rate). My ROE, Perpetuity Growth Rate, Cost Of Equity assumptions are 11% (consensus FY 2027 ROE estimate as per S&P Capital IQ data), 3% (higher to reflect a more favorable long-term growth outlook), and 8% (same as that of the July 7, 2023 article), respectively. This translates into a fair P/B multiple of 1.6 times for the stock, which is roughly where SoFi Technologies' shares are now trading at.

Separately, SOFI is now valued by the market at 31.4 times (source: S&P Capital IQ ) consensus FY 2023 EV/EBITDA, which is not that far from its FY 2023-2026 consensus EBITDA CAGR forecast of +34.3%. Similar to how a Price-To-Earnings Growth ratio of 1 is deemed to be fair, the narrow gap between SoFi Technologies' EBITDA multiple and its expected EBITDA growth rate suggests that the stock is trading at close to fair valuation.

Final Thoughts

SOFI continues to be rated as a Hold, after considering the recent analyst downgrade. SoFi Technologies' shares are still fairly valued as the positive EBITDA growth outlook has been priced into its valuations.

For further details see:

SoFi Technologies Stock: Analyst Downgrade In The Spotlight