NRDS - SoFi Technologies: The New Age Of Banking?

2023-08-31 09:30:00 ET

Summary

- SoFi Technologies is a financial technology company that offers a range of online financial services, including loans and banking solutions.

- The company differentiates itself through its customer-centric approach, round-the-clock support, and diverse product portfolio.

- SOFI's growth strategy includes vertical integration, adaptability to changing interest rates, and technological innovation to establish itself as a resilient neobank.

- We believe the company can currently be rated as a buy.

Introduction

SoFi Technologies, Inc. ( SOFI ), originally founded as Social Finance back in 2011, initially focused on assisting individuals with their student loan refinancing needs.

Over the years, their scope expanded to encompass a broader array of financial services, including mortgages and personal loans. In 2021, SOFI went public through a distinctive merger, rebranding itself as SoFi Technologies in May of that year. This strategic move propelled its overall valuation to approximately $7.9B today.

What differentiates SOFI from its counterparts is its pioneering online business model, establishing a digital ecosystem that seamlessly merges technology with finance to offer a streamlined experience for its customers.

What sets SOFI apart from other financial institutions?

SOFI 's core approach revolves around customer-centricity, delivering round-the-clock support, and diversifying its product portfolio. This methodology fosters enduring customer relationships, ultimately leading to an increase in per-customer revenue over time.

When delving into the inner workings of SOFI’s business, three pivotal sectors come to light: Lending, Technology Platform, and Financial Services. The Lending division encompasses crucial services such as student, home, and personal loans. Complementing this, the Technology Platform houses a pivotal tool called Galileo, acquired in 2020, which furnishes businesses with money transfer solutions, catering to both financially oriented and non-financial enterprises.

Finally, the Financial Services sector encompasses an extensive range, from cash management to investment guidance. Notably, SOFI 's operations are exclusively online. With the acquisition of Golden Pacific Bancorp, the company secured a banking license, positioning itself as a neobank (neobanks being fintech companies that provide banking solutions) and an online financial institution.

Bypassing traditional physical networks potentially allows neobanks to offer improved services and reduced fees . SOFI aptly aligns with this trend, targeting digitally-savvy generations, a tendency further accelerated by the surge in online financial interactions brought about by the pandemic.

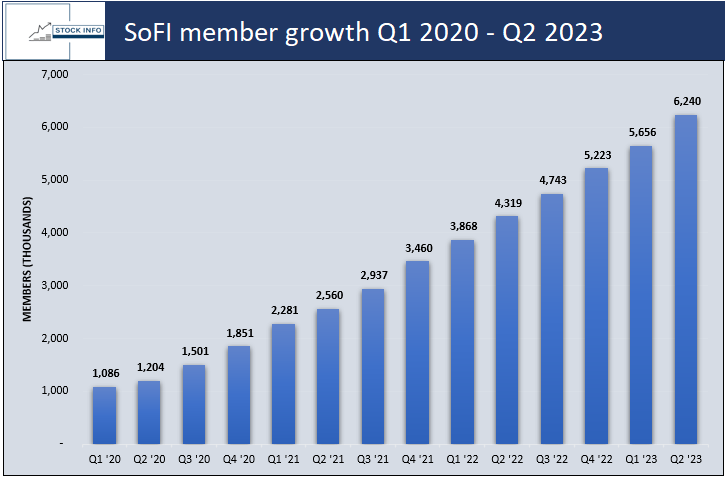

This can also be seen in their impressive member growth over the past few years.

{kind=link}

Unlike niche-focused fintech companies, SOFI aspires to serve as an all-inclusive financial solution provider. In this pursuit, it competes with neobanks like Chime and established institutions like JPMorgan ( JPM ), effectively combining the best of two worlds.

Underpinning SOFI 's strategy is a drive towards vertical integration, exemplified by its acquisitions of entities like Galileo and Technisys. These strategic moves underscore the company's ambition to create a holistic platform catering to a broad spectrum of financial services.

The goal is seamless integration and operational simplicity, streamlining the customer experience. However, while SOFI's ambitions in banking are promising, the competitive landscape is fierce. Although it can potentially serve smaller banks, it might encounter challenges in gaining traction among larger institutions already invested in similar solutions.

SOFI's Unstoppable Ascent: Leveraging Advantageous Interest Rates and Innovative Banking Approach for Market Domination

Let's step back and take a broader look at the macroeconomic landscape, specifically focusing on the interest rate set by the Federal Reserve. We know that the Federal Reserve has been hiking rates for the past year and a half, which has boosted many banks' earnings .

To provide context, higher interest rates are generally seen as advantageous for banks because they can boost their profitability by capitalizing on wider spreads between the returns they earn from investing customers' funds and the interest they pay out to these customers. However, what sets SOFI apart extends beyond this.

First and foremost, SOFI stands out due to its vertically integrated, digital fintech structure, in contrast to other traditional banks that opt for traditional physical branches. These banks focus less on the technological side of the business, which SOFI specializes in. Consequently, SOFI can offer checking and savings accounts at significantly lower costs, a benefit that becomes even more pronounced as the company draws in a substantial influx of new high-quality members with its relatively high credit score requirements .

With more members creating savings accounts and using their services comes numerous advantages to SOFI. For instance, it could provide a cost-effective funding source for its loans and give the flexibility to improve net interest margins by retaining loans on its balance sheet for extended periods. This is very different from their current strategy, where they mainly securitize and sell them to third parties, as is their primary method for generating profit.

If interest rates stay elevated, the inflow of members seeking attractive yields will continue strengthening SOFI's banking services. This positions the company to leverage its superior cost structure for improved operational efficiency. CEO Anthony Noto suggested during their Q1 2023 earnings call that there could be an even more significant catalyst even if rates were to decline. He indicated that SOFI's checking and savings account costs are presently lower than historical costs from a spread perspective. This translates to more cost-effective funding through deposits compared to previous warehouse lines. This means that the company's ability to offer competitive interest rates is rooted in its capacity to generate higher profits through its banking status.

If we look at SOFI’s net revenue, growth, and EBITDA in the figure below, we see much of what Noto is talking about during his earnings call. Between 2021 and the expected net revenue in 2023, SOFI sees it double in this period. In addition, their EBITDA and EBITDA margin have also increased significantly between 2021 and 2022 and are expected to more than double in 2023. This would make sense, as the market is currently expecting the FED to keep rates higher for longer .

Stock Info

We can also see the rapid growth in SOFI’s balance sheet since 2018, which has more than doubled in the past 5 years.

{kind=link}

In addition, Noto also hinted that when rates eventually start decreasing, SOFI could maintain higher rates than competitors, gaining more market share. This implies that SOFI isn't just gaining market share due to rising interest rates; it's strategically trying to be positioned to sustain this advantage by offering more appealing rates than competitors even as rates start to decrease. This remains to be seen, however.

Furthermore, the synergies of cross-selling various products to new members through a unified mobile interface – including checking, savings, investments, credit score monitoring, credit cards, lending services, and travel offerings – will solidify the loyalty of these high-quality members. This makes them less likely to switch to competing banks in the future.

It seems the CEO isn’t worried about the future consequences of lower interest rates, which otherwise have been very profitable for banks in the past year. The confidence that the company can function well and maintain growth in both a low and high-interest-rate market should be seen as very positive for potential investors.

Is SOFI’s loan portfolio too risky?

One of, if not the biggest, risk associated with SOFI is their loan portfolio. As we discussed earlier, many of the loans on SOFI's books are related to personal expenses or student loans.

This can be concerning - Unlike loans tied to assets like homes or cars, where the lender can take the property if payments are missed, personal loans lack this level of protection. When a mortgage isn't paid, banks can take the property back, and with auto loans, they can repossess the vehicles. Though there might still be some losses, selling those assets can help recover money. In contrast, if someone defaults on a $20,000 personal loan, the company has to absorb the entire loss with no recourse. This fundamental difference makes personal loans much riskier than secured loans.

The additional risk associated with personal loans is counteracted by charging notably higher interest rates than secured loans. This approach makes personal loans much more profitable for lenders than mortgages or other loans - given that borrowers meet their repayment commitments.

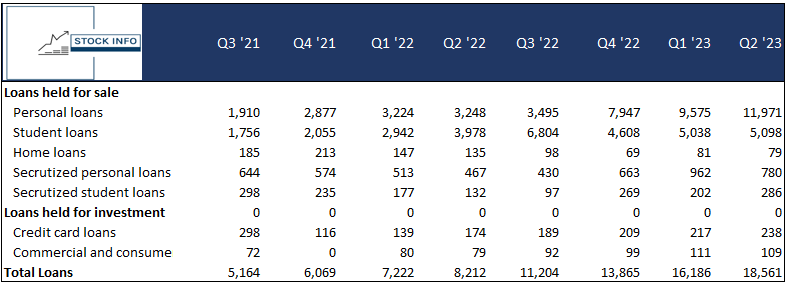

The table below illustrates the rapid expansion of SOFI's loan portfolio (in millions of USD), highlighting their focus on personal loans over the past couple of years.

{kind=link}

It's worth remembering that economic downturns and job losses often lead to an uptick in loan defaults – this is still a genuine risk in today’s economic environment. These defaults directly impact SOFI’s revenue, as they fall under noninterest income. This particular risk holds significant weight due to SOFI's identity, as they are still seeking incredible growth.

In the event of a severe economic recession leading to a spike in defaults, SOFI's financial health would suffer. As a result, SOFI might need to resort to cost-cutting measures to stabilize its operations, which could harm further development into Galileo. Such circumstances constitute a noteworthy risk.

In addition, it should also be noted how SOFI handles its delinquencies. Delinquency refers to loans with overdue payments. SOFI monitors and marks these delinquent loans 10, 30, and 90 days past the due date. When a loan is 30 days delinquent, 70% of its value has already been written off. At the 90-day mark, only 10% of the remaining principal is considered. These write-offs immediately impact SOFI's revenue in the quarter when they occur. Loan default happens at the 120-day mark of delinquency. At this point, the loans are entirely written off and handed over to collections, rendering them worthless to SOFI.

This is where the risk analysis becomes intricate, at least from my perspective. SOFI effectively manages delinquency risk by adhering to stringent credit standards. As mentioned earlier, SOFI has relatively high requirements for potential lenders. This sets them apart from peers like Upstart (UPST), which caters to borrowers with lower credit scores, and LendingClub (LC), which focuses mainly on borrowers with good credit. While SOFI isn't entirely immune to the potential for increased delinquencies and defaults, the quality of their borrowers should provide some protection against these risks, barring a significant economic downturn.

Moreover, SOFI's lending strategy is based on extending loans to individuals with available disposable income. This approach shifts the focus from reviewing past debt repayment history to evaluating how much extra money borrowers have to repay the loan. This forward-looking approach provides insight into the likelihood of future default. Naturally, if individuals experience a loss of income, defaults might increase due to their reduced cash flow. While this is a risk, I'll delve further into this aspect in the subsequent discussion.

There's also a prevalent belief that SOFI's default rates might increase if student loans become a major issue again, as many of their borrowers also have student loan debt. However, two factors should be taken into consideration. First, borrowers refinancing their student loans with SOFI have consistently managed those obligations. Second, SOFI already factors in this dynamic when assessing available disposable income. With student loan repayments set to continue in October this year, it will also impact SOFI’s earnings. Student loans make up a significant portion of SOFI’s loans held for sale, and as with any other loan, the risk associated with default on these loans will also resume.

It should be noted that CEO Noto already addressed this: "We perform a credit check. We examine all their financial obligations. Even if they have an existing student loan and aren't paying it now, it still shows up as a liability, and we factor that into their cash flow. So it shouldn't have any impact. The student loan was part of our overall decision-making process for personal loans and all the other debts at the time of financing. So it shouldn't directly affect things, assuming everything else remains equal."

The last part of the statement is what investors should be careful of. Student loans can be a significant financial burden for many Americans, and we have yet to see the consequences of payments resuming.

However, although an extra monthly obligation might strain borrowers and lead to more defaults, SOFI has already integrated this factor into its underwriting process. Hence, the direct effect on their loans should be manageable.

While we wouldn't go so far as to claim that this factor will have absolutely "no impact," it's essential to recognize that SOFI has proactively accounted for it in its risk assessment and underwriting practices. This implies that the effect on their loan performance should be limited, despite the potential "added burden on borrowers."

Growth and comparative analysis

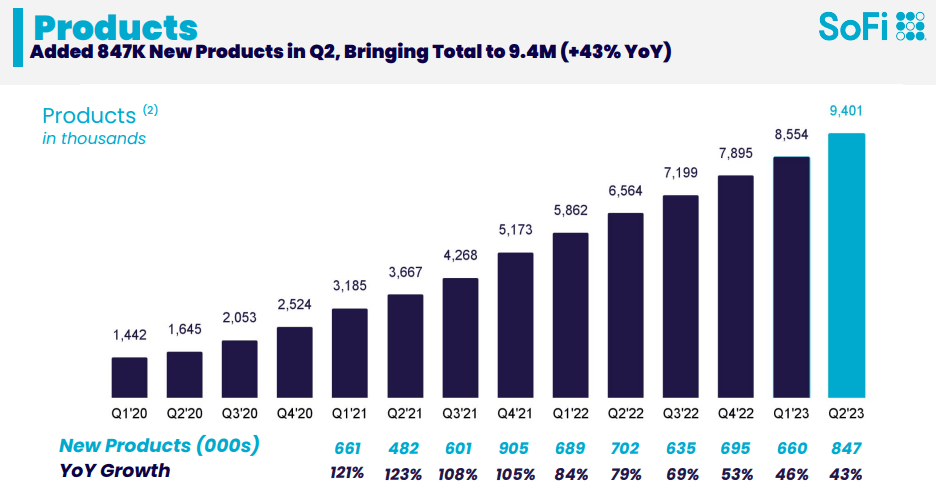

Besides SoFi Technology, one of their selling points for investors is their spectacular growth story. We saw earlier how much the number of members has grown, but if we look at how their products have grown, we see impressive numbers again.

{kind=link}

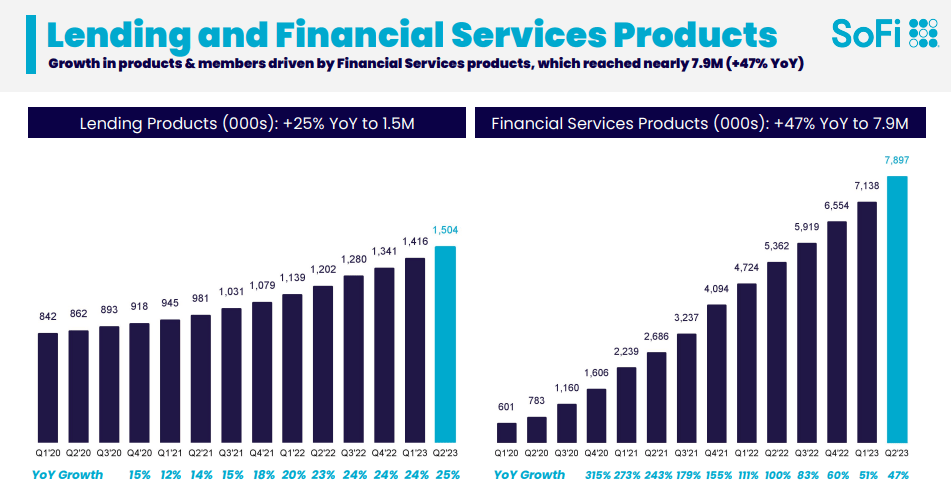

In addition, this can be seen in their lending and financial services products, which are not showing signs of slowing down yet.

{kind=link}

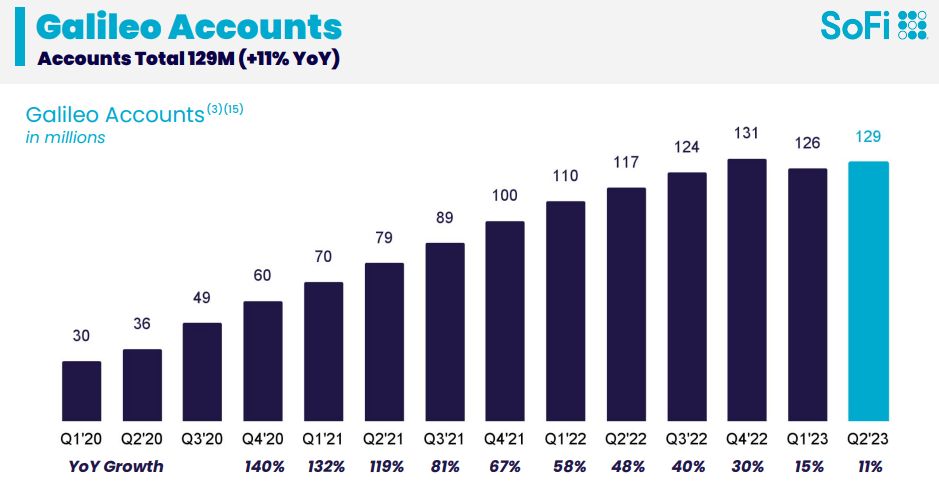

However, the number of Galileo accounts has shrunk between Q4 2022 and Q2 2023. However, it appears that it is on the upswing once again. As Galileo is more business-oriented, the number of accounts is more sensitive to the business environment. The business environment was somewhat rocky at the beginning of 2023, which could explain the account dip. In addition, as rates are set to decrease, business loans would become cheaper relative to now, which could bump up the number of accounts.

{kind=link}

Suppose we briefly look at some chosen growth and profitability metrics. Among the companies listed in the table below, SOFI stands out with remarkable revenue growth, exhibiting a substantial YoY increase of 47.4% and a promising forward-looking growth projection of 35.6%.

Over three years, SOFI maintains an impressive CAGR of 50.8%, surpassing most of its counterparts. In addition, its long-term growth over five years remains robust at 24.6%, although not as dominant as its 3-year CAGR. On the profitability front, SOFI faces challenges, showing negative returns on equity (-3.5%) and assets (-0.4%). This suggests potential hurdles in generating profits relative to its equity and efficiently utilizing its assets. In contrast, companies like CACC and OMF exhibit more substantial returns in these areas. SOFI may need to address this in conjunction with its growth trajectory.

Stock Info

Technical analysis

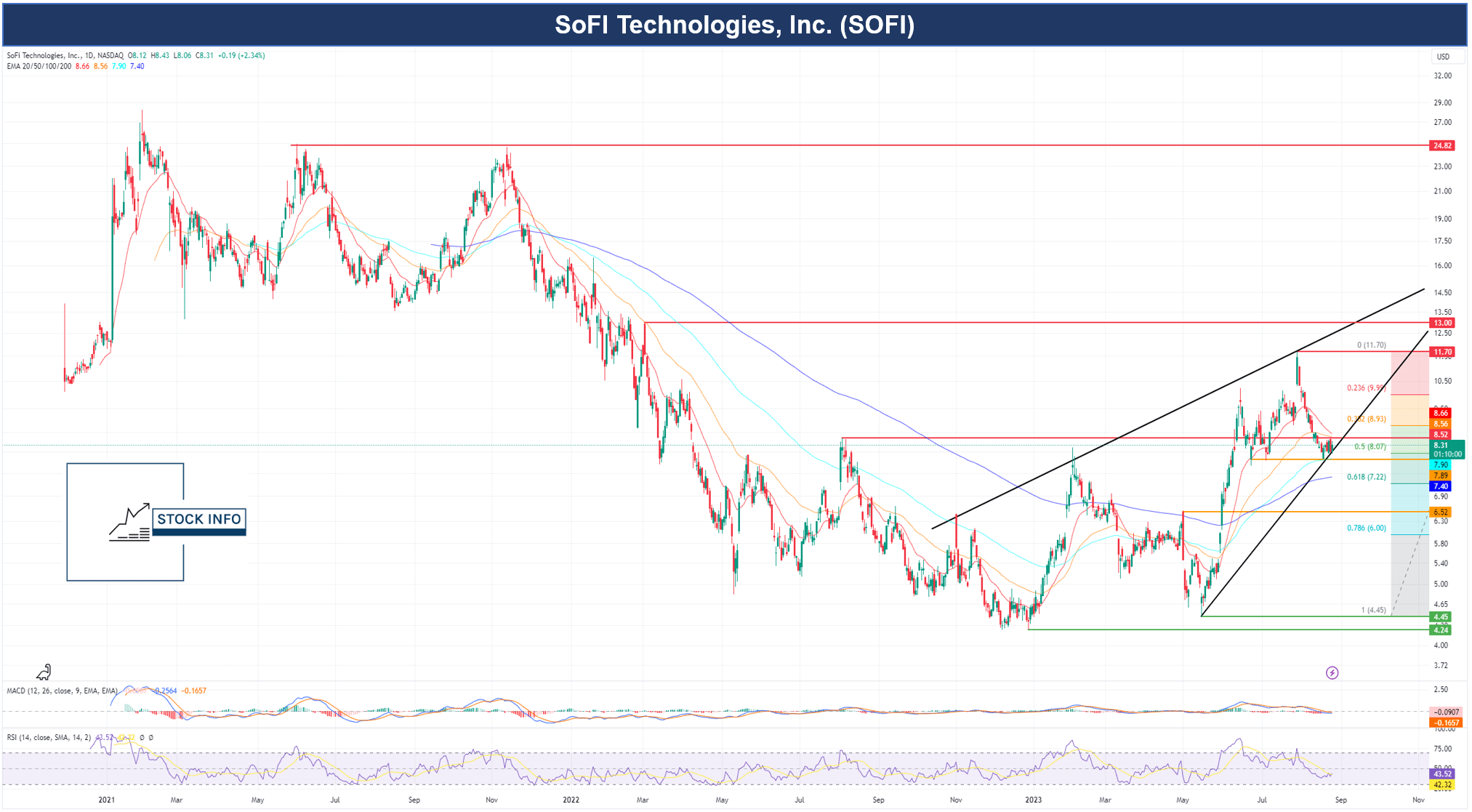

Let's take a look at SOFI’s chart since it went public. As mentioned earlier, SOFI was the name on the street when it went public. It closed its first trading day at $10.48 and reached an all-time high of $28.26 on February 1, 2021 – a nearly 200% increase in months. The stock swung between $24.50 and $14 for most of 2021 before falling to just $4.24 at the end of 2022.

Currently, the stock is trading around $8 after falling from $11.70 just three weeks ago. The stock is trading above its 200 EMA, meaning it has a relatively strong level of support at $7.40. In addition, it should also be noted that the stock touched and bounced at the 100 EMA at $7.89. The stock has been consolidating around the 0.5 Fibonacci number and has now touched a steep trendline. The stock still faces a relatively strong resistance at $8.52 from last year. Notice that the 20 EMA has yet to cross the 50 EMA, which could signal that the stock still has momentum behind it. In addition, the RSI is under 50, which is slightly oversold territory. This, combined with a MACD that is starting to turn upwards, means it is possible for the stock to rise again.

After the recent speech by Jerome Powell at the Jackson Hole symposium, it is interesting to see if this will shift the overall market sentiment more bullish than it has been this August. It could again help SOFI towards the $11 handle if it does.

If you are worried about the broader market sentiment right now, we suggest you might want to find an opportunity to open a position in SOFI at lower levels, around the $7 mark.

However, as we see it, the stock has found a comfortable consolidation level before it takes its next leg up. We, therefore, believe the stock is a buy at the current low $8 level.

{kind=link}

Conclusion

In conclusion, SOFI's customer-centric approach, diverse product portfolio, and digital foundation form the bedrock of its growth strategy. Through vertical integration and adaptability to changing interest rate landscapes, SOFI aims to establish itself as a resilient neobank.

Despite challenges in its loan portfolio and market volatility, the company's emphasis on risk management and technological innovation positions it for sustained success in the evolving financial landscape. We believe the current price level is a decent point to start a position in SOFI; however, broader market sentiment should be considered. We currently rate this stock a buy.

For further details see:

SoFi Technologies: The New Age Of Banking?