SOFIW - SoFi Technologies: Turmoil Ahead

Summary

- SoFi Technologies, Inc.'s Q4 revenue should come in around $426.5 million.

- SoFi Technologies stock is still grossly overvalued compared to peers and can fall further.

- Risk-averse investors may want to avoid SoFi Technologies, Inc. stock for now.

SoFi Technologies, Inc. ( SOFI ) is scheduled to report its Q4 results in two weeks, on January 30. Anxious investors will be closely watching how SoFi’s revenue gets impacted in the current recessionary environment. But, in addition to tracking the headline financial figure, investors must also pay close attention to SoFi’s liquidity ratios, its member count, product sales, segment financials, and management's outlook for Q1. These items will provide more color on the company’s operational positioning and are likely to influence where its shares will head next in the coming weeks. Let's take a closer look at it all.

Operating Metrics

Let me start by saying that SoFi Technologies, Inc.’s top brass has done a terrific job at growing their business so far, and also with procuring the bank charter to lower their lending rates further. FinTech is one of the toughest industries to crack, and SoFi’s management has done well to establish a strong footing in the space. But with the student loan moratorium being extended once again, and inflationary spending weighing down on disposable incomes for nearly all consumers in the U.S., SoFi’s business is bound to experience a slowdown. So, for investors, the first order of business should be to track SoFi’s user engagement metrics to gauge the severity of its sales slowdown.

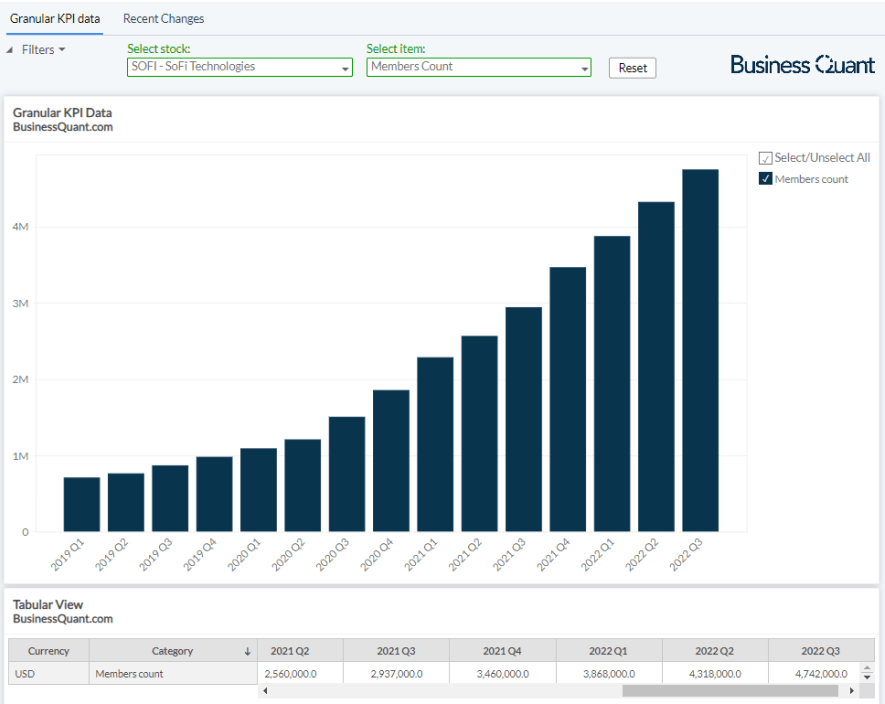

We can start by monitoring SoFi’s members count. It’s essentially the aggregate number of all the customers who have used any of SoFi’s products – spanning from student loans, personal loans, SoFi Money, Invest, Lantern Credit, Relay, Credit Card and At Work amongst other products – since the company’s inception. As it’s a cumulative total, it’s needless to say that the number is bound to only increase with each passing quarter.

{kind=link}

But pay particularly close attention to the pace of members growth. Its member base grew at a stellar 61% year-over-year in Q3, but note in the chart above how its growth momentum has been fizzling out of late. A further deceleration in its member growth trajectory would raise several questions such as:

- Maybe SoFi Technologies is succumbing to competitive pressures, with its rivals also acquiring bank charters offering to lower their lending rates?

- Is this a terminal decline, or just a seasonal fluctuation caused by the global macroeconomic downturn?

- How severe is this slowdown going to be, and how long will it last, if it’s seasonal?

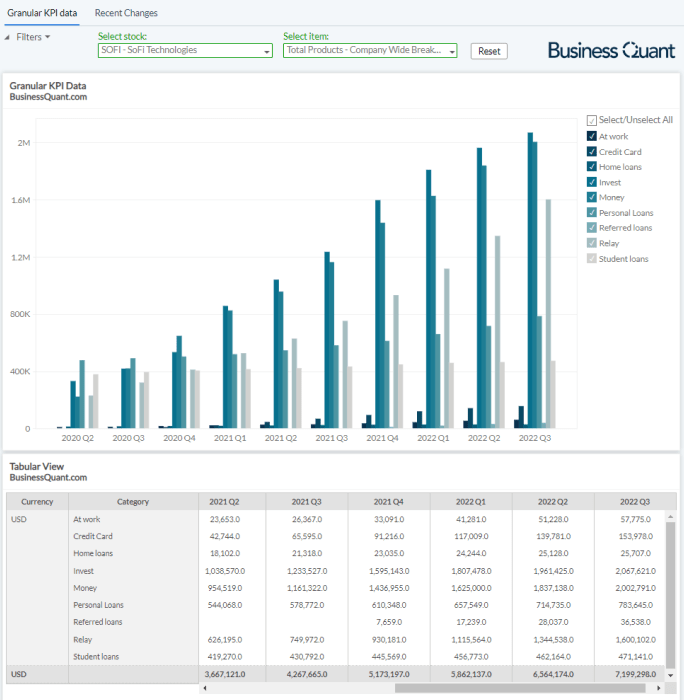

Having said that, we need to also monitor SoFi’s products count in its upcoming earnings report. This will provide us granular insight about which products are selling like hotcakes, which ones are growing at an average pace, and which ones are lagging behind and require immediate attention. For the record, this metric is basically the total number of products that SoFi’s members have subscribed to, since the company was founded. This is also a cumulative figure and is bound to only increase with each passing quarter.

{kind=link}

Note in the chart above how student loan products growth has remained muted for the past 2 years. As the U.S. government keeps extending the student loan moratorium, Federal student loan repayments have remained paused for the most part, and students have little reason to refinance them with SoFi. The status quo hasn’t changed much of late, so I expect SoFi’s student loan products growth to remain subdued in Q4 as well.

However, SoFi’s Invest and Money products have grown at a blistering pace in the last several quarters. I contend they’ll be wildcards in Q4 FY22 and Q1 FY23, as inflationary and recessionary pressures are restricting discretionary spending for households across the globe. So, until consumer behavior returns to normalcy, I believe these products will experience a slowdown.

With that said, let’s now shift attention to SoFi’s financials.

Financial Impact

The company had $5.95 billion in loans held for sale in Q4 2021, which swelled up to $10.9 billion at the end of Q3 FY22. If the demand for its loan book continues to dry up, with the Fed’s rate hikes driving creditors to higher rate-bearing debt, SoFi may have to inherit these loans and eat a loss. It won’t be able to offset or mitigate these losses since its already unprofitable. Such an event is bound to drag SoFi’s CET1 ratio (core capital divided by risk-weighted assets such as loans) lower, and it’s anyone’s best guess what this new low would be.

BusinessQuant.com

Another sequential drop of the same magnitude will practically land SoFi’s liquidity ratios at the minimum required levels and raise regulatory eyebrows. At that point, the discussion will shift from SoFi’s growth prospects, over to assessing the risk of dilution in order to recapitalize the bank, or how to sell off these loans in a fire sale. So, investors must closely watch SoFi’s liquidity ratios in its upcoming Q4 earnings report.

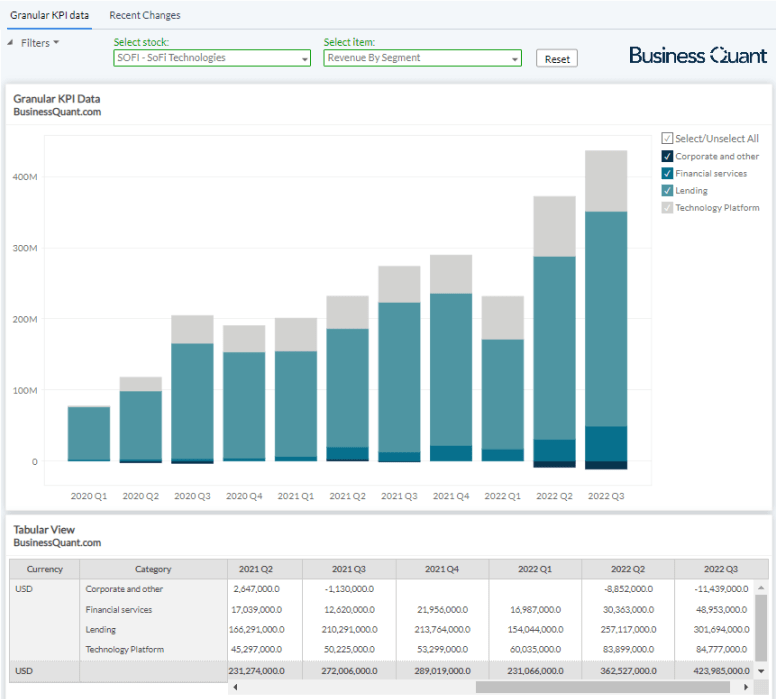

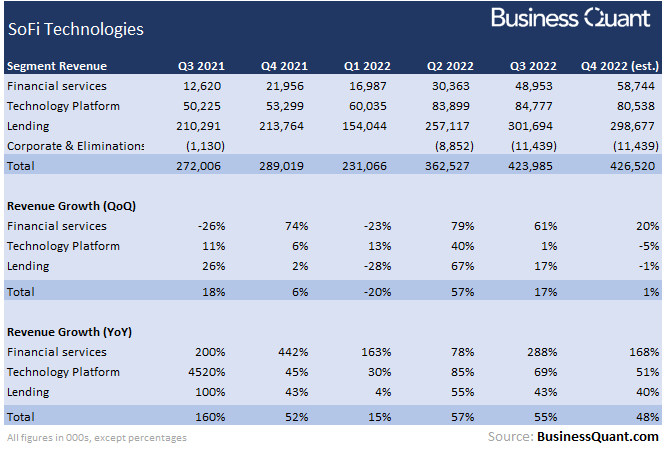

Having said that, SoFi classifies its revenue in broadly 3 segments namely financial services, technology platform and lending.

{kind=link}

Its lending business accounted for 67% of total revenue last quarter and includes the sales contribution from its personal, student and home loans. With rising interest rates amidst a recessionary environment, fewer consumers will be in the market to finance new homes. The student loan moratorium was extended recently so this business will also remain subdued in Q4 once again.

At the same time, more consumers will financially strained and tempted to originate personal loans in order to ride through these difficult times. So, there is an opportunity for SoFi to grow its lending business. However, SoFi itself might scale back on lending in order to prevent its balance sheet from getting too large, in the event it is unable to find buyers for its “loans held for sale” and liquidity ratios get dangerously low. So, I’m estimating SoFi’s lending revenue to shrink 1% sequentially, with revenues amounting to roughly $299 million.

Its Technology Platform includes the sale of Galileo platform. That is sold to enterprises for setting up their own financial products offerings. I expect this segment to drop 5% sequentially to $80.5 million, as enterprises across the globe are cutting down on their discretionary spending, at least until the macroeconomic situation returns to normalcy.

Lastly, SoFi’s Financial Services segment includes the sale contribution of SoFi Money, Invest, Credit Card, At Work and other such products. I expect the segment’s revenue to come in at $58.7 million, with its sequential growth decelerating to 20% in Q4. My rationale is that personal disposable incomes have been declining rapidly in the past few months, due to the rapid interest rate hikes and rampant inflation. This would limit the consumer spending of SoFi’s subscriber base, and whatever growth it will post will be through inorganic means (like market share growth bringing new customers) for now.

{kind=link}

This brings us to a company-wide revenue figure of $426.5 million for Q4 FY22. Coincidentally, my estimate is in-line with the Street’s revenue estimates that are currently spanning from $420 million and $435 million.

But having said that, we must also pay close attention to SoFi management’s outlook for Q1. Specifically speaking, are they planning to roll back their lending activity, how they’re planning to sell debt, and how their revenue might be affected in light of intensifying inflationary pressures and the recent student loan moratorium extension.

Final Thoughts

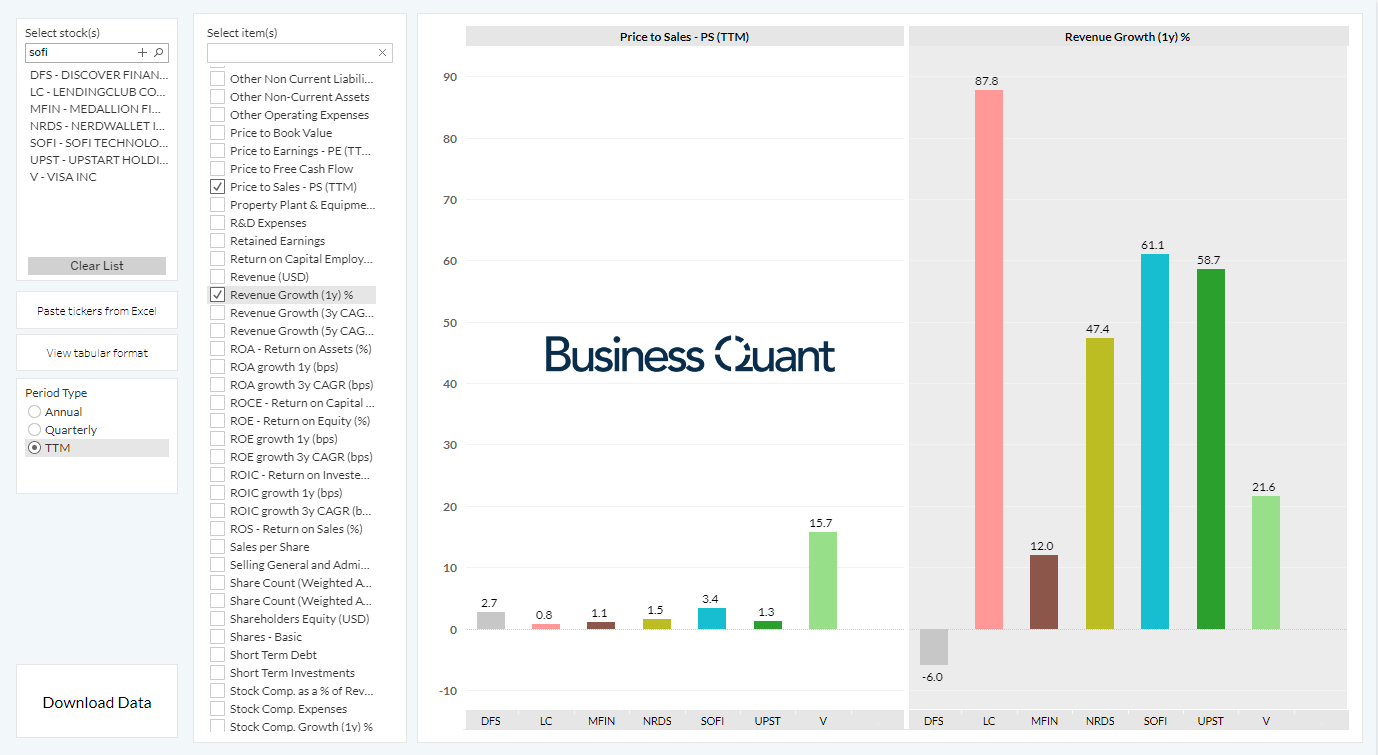

SoFi Technologies, Inc.’s shares are down 60% over the last year, but the stock isn’t necessarily a screaming buy. It’s trading at roughly 3.4-times its trailing twelve month sales, which is considerably higher than many of the other rapidly-growing companies in the space. So, risk-averse investors may want to avoid the stock for the time being, at least until it falls further to be valued more or less with other peers.

{kind=link}

But as far as its upcoming Q4 earnings report is concerned, I project its revenue to amount to $426.5 million. Investors may want to also keep tabs on its members growth, products growth, liquidity ratios, segment financials, and its management’s outlook for Q1. These items will better highlight SoFi’s near-term prospects and operational hurdles, and so, they’re likely to influence where its shares head next. For now, I rate SoFi Technologies, Inc. as a "Hold." Good Luck!

For further details see:

SoFi Technologies: Turmoil Ahead