AFMC - Soft Landing? Copper And Cardboard Say 'Not So Fast'

Summary

- The market does not believe the Fed.

- I think the market is pricing-in the pivot, well in advance.

- The price of copper is suggesting stickier inflation in the months ahead, contrary to market expectations.

- Demand for cardboard and paperboard is suggesting that growth is declining at a recessionary pace.

- Liquidity is coming from the Treasury General Account due to the Debt Ceiling debate.

Equities have performed superbly in 2023 thus far, with the Nasdaq posting its best January since 2001 . The S&P 500 is up more than 7% YTD, which is in stark contrast to last year's disastrous performance. The consensus view is that the Fed has all but secured a "soft landing" and that a pivot to monetary policy is imminent.

On Wednesday, the Federal Reserve raised the Federal Funds Rate by 25 basis points, as expected by the market. Chairman Powell was neither overly dovish or hawkish, but the market responded very bullishly.

I am skeptical of the market action. For one, I think that a soft landing is not the most probable outcome. Even if the Fed were to pivot tomorrow, the economy looks poised for further weakness. In fact, as I have pointed out before, a Fed pivot has often signaled the start of significant weakness during past recessions.

The best performing assets of 2023 have been the ones that performed the worst in 2022. While the S&P 500 is down 9.6% over the past year and up 7.5% over the past month, the Invesco QQQ ETF is down 18.8% over the past year and up 10.6% over the last month. The ARK Innovation ETF ( ARKK ) is down 47% over the past year and up 27.8% over the last month. Tesla ( TSLA ) is down 44.5% over the past year and up 40.6% over the past month. Carvana ( CVNA ) is down 93.7% over the past year and is up 114.5% over the past month.

These movements do not instill confidence for me in this recent rally. It has the characteristics of a liquidity and narrative driven bear market rally fueled by short covering. The narrative is that inflation has been licked, rates are soon to fall, and growth will return. I think this is presumptuous, and here's one reason why.

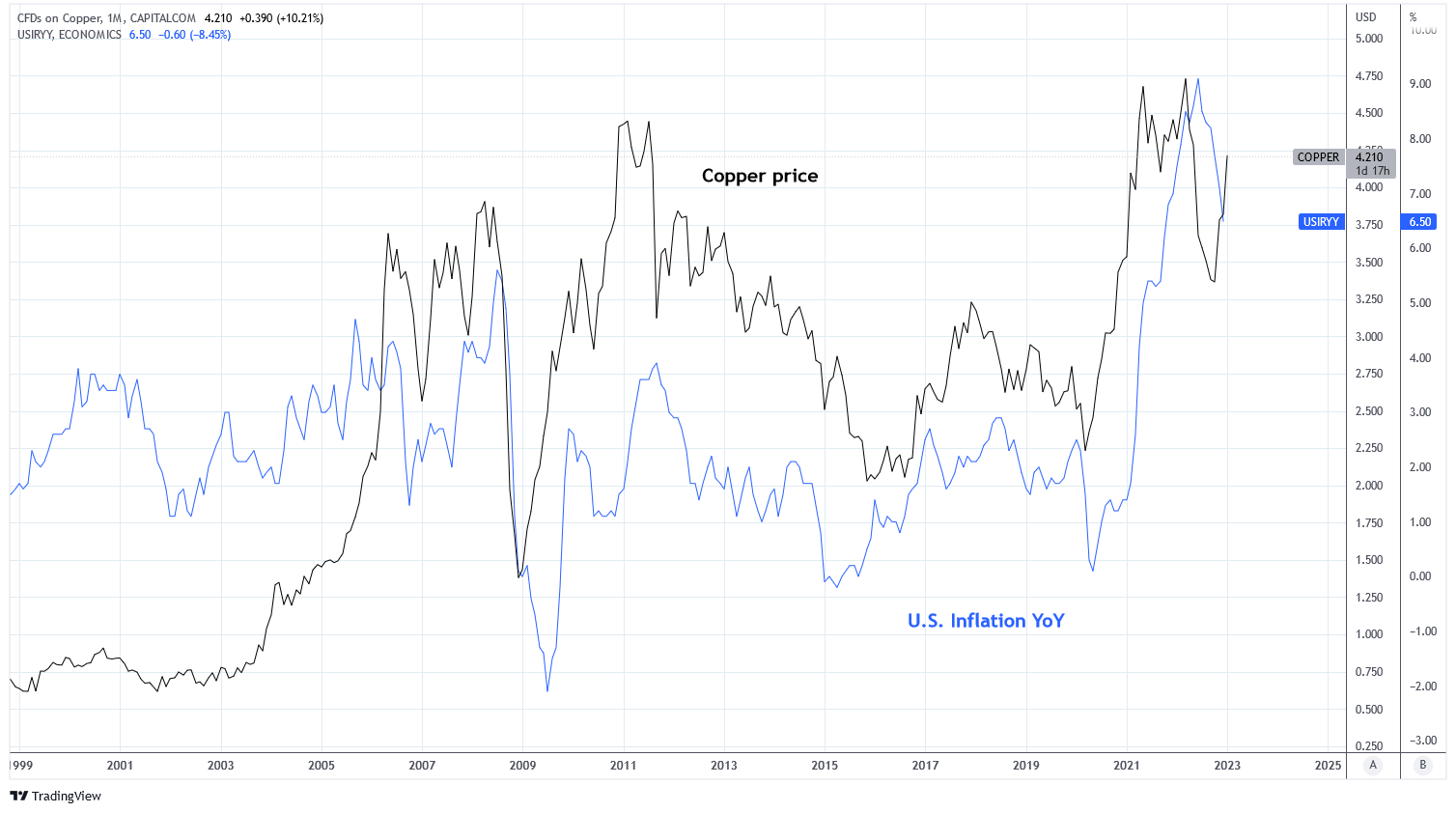

Copper is a valuable leading indicator of economic activity and inflation. Since last July, copper prices have been on a steady rise. Conversely, cardboard is a valuable leading indicator of economic growth and recession. Demand for cardboard has declined at an alarming rate that suggests growth is still slowing.

This implies that we are potentially facing the opposite of what the market expects. Instead of immaculate disinflation we may be closer to stagflation or classic recession. The market is looking forward to when the Fed is going to start easing again. This is why the price of gold has trended strongly higher since November. But I'm looking farther ahead, to what happens when the Fed cuts rates and thereafter.

Soft Landing

The effects of the current monetary policy tightening have yet to be fully experienced by the global economy. I've written many times before that this episode of tightening is one of the fastest in history and therefore we have not reached the full effect of that policy. Chairman Powell , in the FOMC press conference on February 1, 2023, agreed in his opening remarks:

We have covered a lot of ground, and the full effects of our rapid tightening so far are yet to be felt. Even so, we have more work to do.

Notably, the FOMC statement included a change from the December statement which raised the committee's target Fed Funds rate from 4.25-4.5% to 4.5-4.75%. The statement also changed from the "pace of future [rate] increases..." to the "extent of future [rate] increases..." I interpret that to mean that the committee expects to raise rates by 25 basis points until they reach the terminal rate they feel comfortable with. This is what Powell said about future rate hikes:

We continue to anticipate that ongoing increases will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time.

The market is not believing the Fed. Instead, the market is saying "Nope, you're done." The rate on the 10 year Treasury declined by 13 basis points as rates across the curve fell. The market implied forward Fed Funds curve for the next three years is well below the FOMC projections, including expected rate cuts in the second half of 2023. The pricing of assets, and particularly those that are very rate sensitive, is reacting strongly to these market expectations.

The Daily Shot (used with permission)

It is worth noting that the market implied rates has a very checkered history at predicting the direction of rate changes, as shown in the chart below. Powell made it clear during the press conference that he does not expect rate cuts in 2023:

...it’s a forecast of slower growth, some softening in labor market conditions, and inflation moving down steadily but not quickly. And in that case, if the economy performs broadly in line with those expectations, it will not be appropriate to cut rates this year, to loosen policy this year. Of course, other people have forecasts with inflation coming down much faster; that’s a different thing.

The Daily Shot (used with permission)

The market has good reason to expect a Fed pivot because economic data suggests that recession is impending. Aside from the yield curve inversions which typically forecast recession, leading indicators are in recessionary territory. The Conference Board US Leading Index has experienced an annualized decline that has coincided with each recession since 1960. If it were not for the inflation problem, I expect the Fed would have pivoted by now.

The Daily Shot (used with permission)

This is one the reasons why I think equities are rallying. Equities tend to perform well following a pause to rate hikes. According to data from the BofA, on average the S&P 500 has gained 14% over the 12 months following a rate pause. I think the market is forward-looking and the recessionary data is clear enough that after inflation prints peaked last year and the Fed stepped down its rate hikes to 50 basis points the market began pricing in the pause. Since October last year, the S&P 500 is up 17.7% in less than 4 months.

The Daily Shot (used with permission)

Copper

This brings us to our first indicator. The price of copper tends to lead U.S. price inflation by less than a year (see chart below). This is because copper is widely used in industry and often represents global economic activity. While inflation has apparently peaked, as did copper, copper prices have been rising since July 2022. It suggests that inflation measured by the CPI and PPI could face stickiness in the months ahead.

{kind=link}

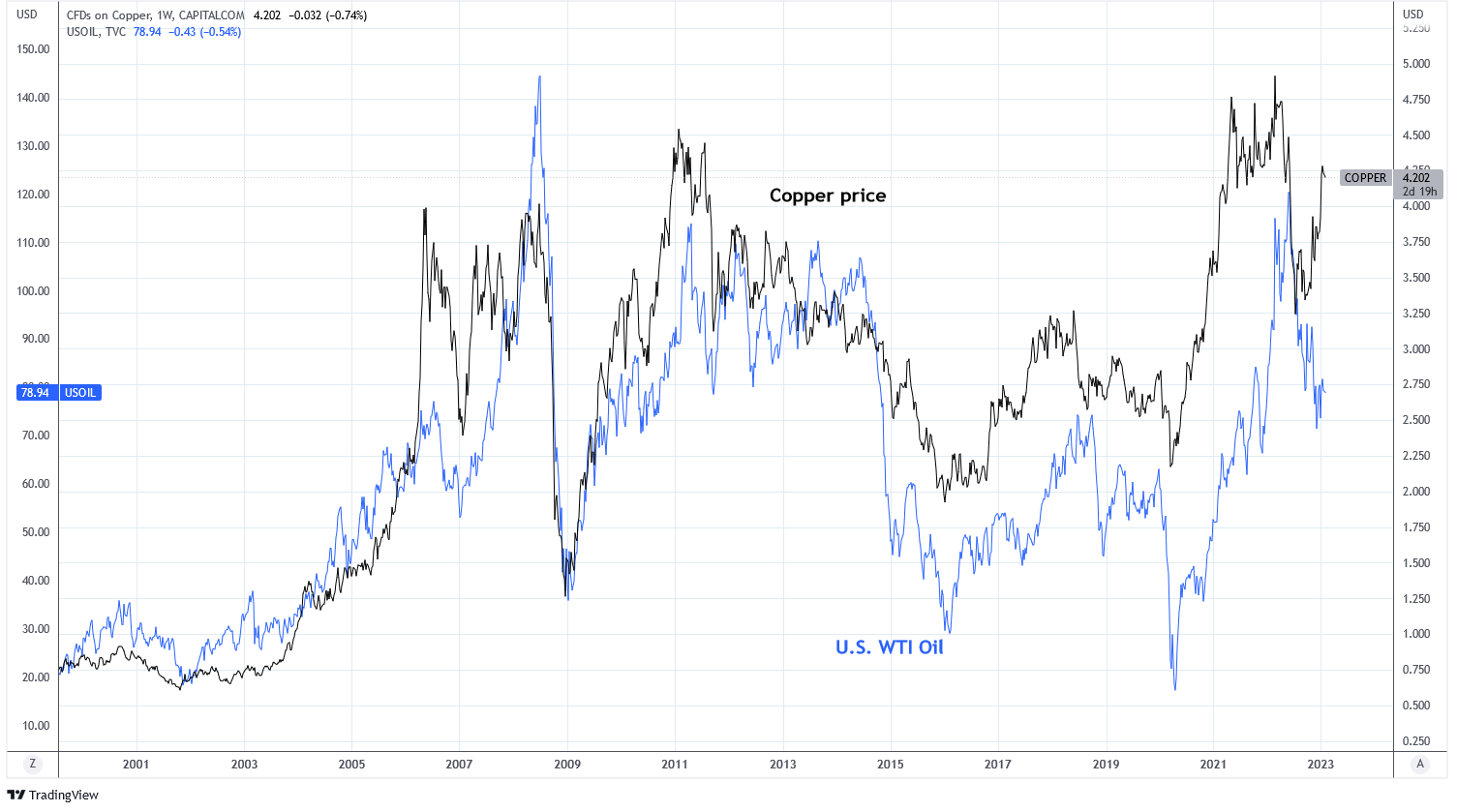

Changes in the price of copper tend to lead the price of oil by a few months. If copper is forecasting an increase in oil prices in 2023 that will have an adverse affect on inflation and the Fed's objective.

{kind=link}

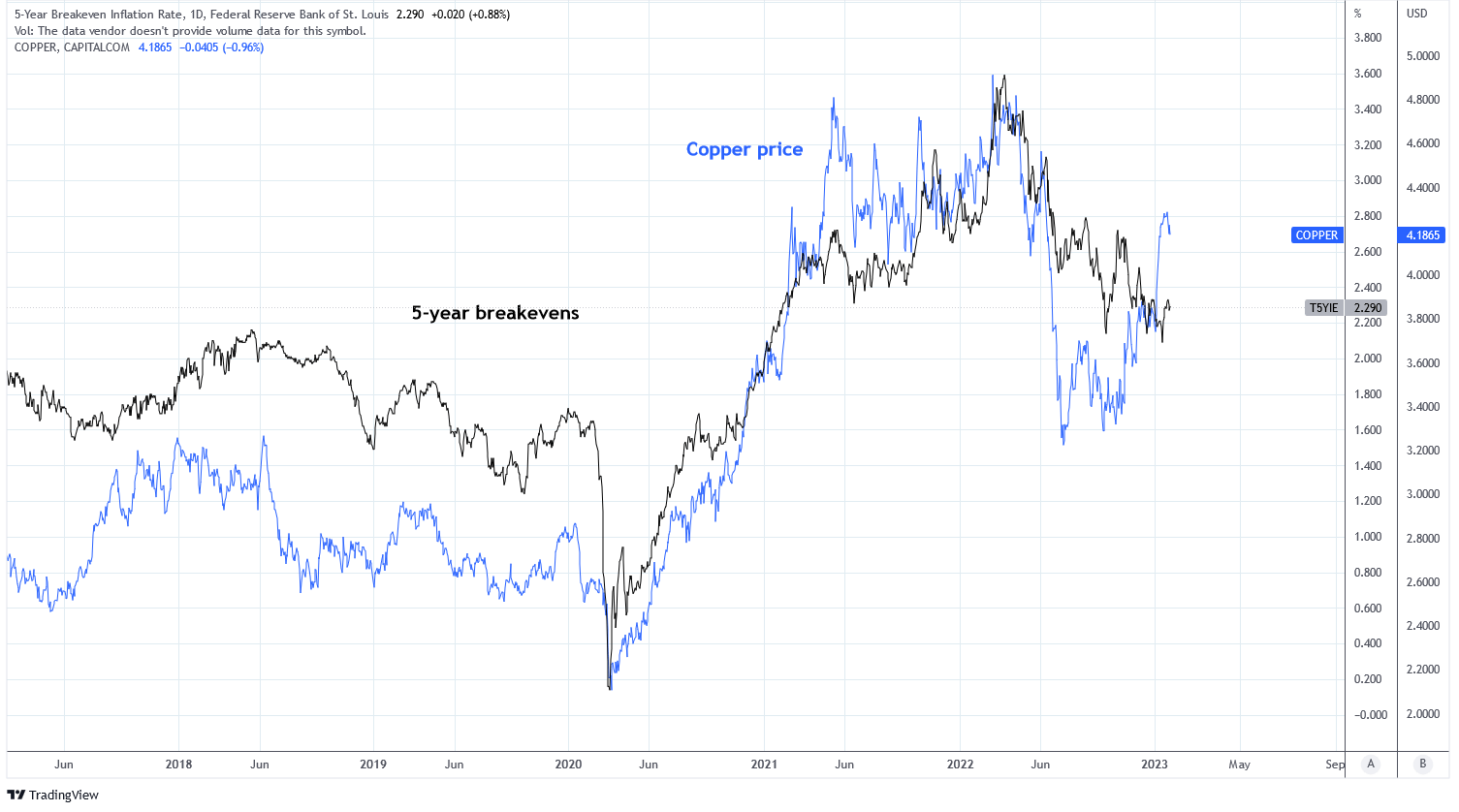

A disconnect has appeared between copper prices and inflation expectations, as represented by the 5-year Treasuries breakeven yield. Copper prices suggest that inflation expectations could be 40 basis points higher.

{kind=link}

I believe this uptrend in price inflation is beginning to manifest in index data, as the ISM manufacturing prices paid index recorded a measurable move higher in excess of expectations for the index to be at 39.5.

It's likely that commodities are experiencing a resurgence in price in response to the announcement of China ending its zero-covid policy and associated lock-downs. Copper prices truly began to rise in earnest around the time of the announcement in December 2022. There is much to be seen about how China's reopening impacts global growth and commodity prices, and if this trend is to be short-lived. For now, it means added pressure to keep rates higher for longer.

Cardboard (and paperboard)

Our second indicator tells another story. Data from Fibre Box Association shows that shipments of cardboard in the U.S. has declined by 8.4% QoQ in Q4 2022, the largest decline since 2009. Cardboard manufacturer operating rates are also the lowest since 2009. Paperboard shipments have not yet declined to levels that correlate with recession but if the trend persists that has the potential to change in 2023.

A significant drop in paperboard production often occurs following the start of recession. Paperboard production has already declined significantly in 2022.

Liquidity, Debt Ceiling, and Financial Conditions

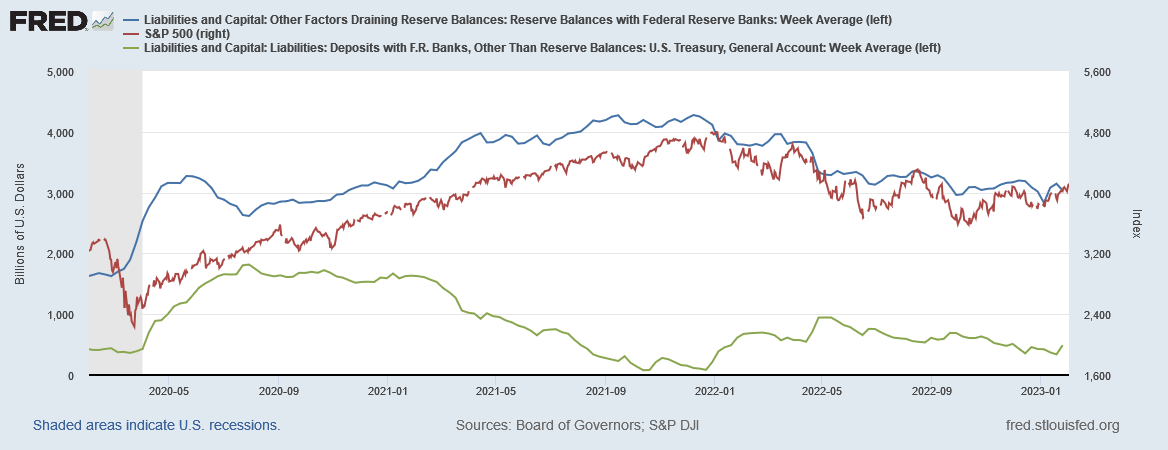

In addition to the reasons already discussed, I think equities are benefiting from another tailwind. Due to the ongoing U.S. Federal Debt Ceiling debate, the U.S. Treasury has needed to deploy cash reserves from its General Account to prolong its borrowing authority . This is essentially adding liquidity to financial markets and contributing to the easing of financial conditions. Until the debt ceiling issue is resolved, by raising it, this source of extra liquidity may continue to influence markets. The Fed is still expected to decrease its balance sheet by about $1 trillion in 2023, which Powell described as "significantly reducing the size of our balance sheet."

{kind=link}

Powell spoke at the press conference about how financial conditions are much tighter than they were a year ago. While it's true that financial conditions are tighter than January 2022, they have eased considerably since October. It would seem that the Fed would need financial conditions to be tighter than at present to achieve their inflation mandate.

Summary

The scenario that harms the bullish thesis most is one that includes persistent inflation and a steep decline to growth. That would result in a "hard landing" in contrast to the widely expected soft landing. The relationships between inflation and growth are intricate. If inflation persists, the Fed will be motivated to quell growth further. If growth plunges, it will resolve inflation at the expense of earnings.

The soft landing outcome is not impossible, albeit unlikely by my expectations. Given the risks, I think the market is premature to price in a pivot that could very well take longer than anticipated. I find it sorely ironic that the market is pricing in circumstances that force the Fed to pivot earlier than they want to, circumstances that would need to be more dire than the soft landing prescribes.

My portfolio remains positioned conservatively. Yields offered by U.S. Treasuries are attractive given the risks. The market and the Fed are staring at each other, waiting to see who blinks first. Eventually the Fed cooperates with what bond markets are communicating to them. But between then and now a lot can happen. Here's Powell's rebuttal:

The historical record cautions strongly against prematurely loosening policy. We will stay the course, until the job is done.

Market, your move.

For further details see:

Soft Landing? Copper And Cardboard Say 'Not So Fast'