SFBQF - SoftBank Corp: A Cheaply Priced Bond Proxy

2023-06-11 21:41:21 ET

Summary

- Softbank Corp may have missed the mark on its headline numbers.

- But the underlying telco business remains robust.

- The implied cash generation potential from the latest mid-term plan signals further upside to an already elevated shareholder return yield.

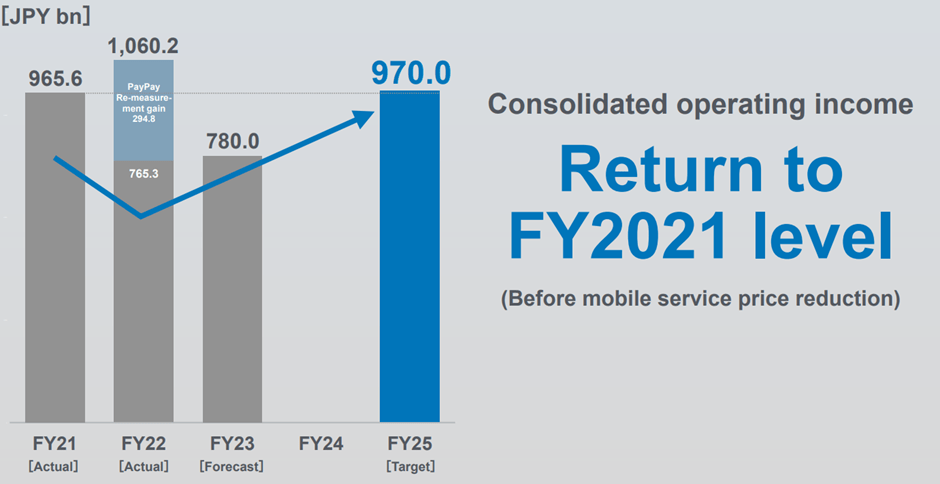

Softbank Corp ( SOBKY ), the domestic telco operating arm of Softbank Group ( SFTBY ), saw its headline full-year numbers fall short of consensus. This was largely down to weaker earnings at the non-core Z Holdings business (i.e., the holding company for Yahoo! Japan, messaging app Line, and payment company PayPay), though. The core telco operations remained resilient, underpinning a new mid-term operating profit target of JPY970bn and profits attributable to owners of JPY535bn. While these numbers are premised on a seemingly ambitious >1m net adds per year, the investments Softbank has made in its 5G network, as well as the earnings growth potential of PayPay, mean the P&L target is likely well within reach. Capital returns should also stay elevated – the telco capex cycle has peaked, boosting mid-term FCF generation and freeing up balance sheet headroom for a JPY86/share dividend payout. With the ~6% fwd dividend yield and the JPY100bn buyback implying a total return yield of ~7% (vs. ~0.4% for the 10-year JGB), Softbank Corp screens attractively as a bond proxy at the current price.

Examining the Underwhelming Headline FY Results and Guidance

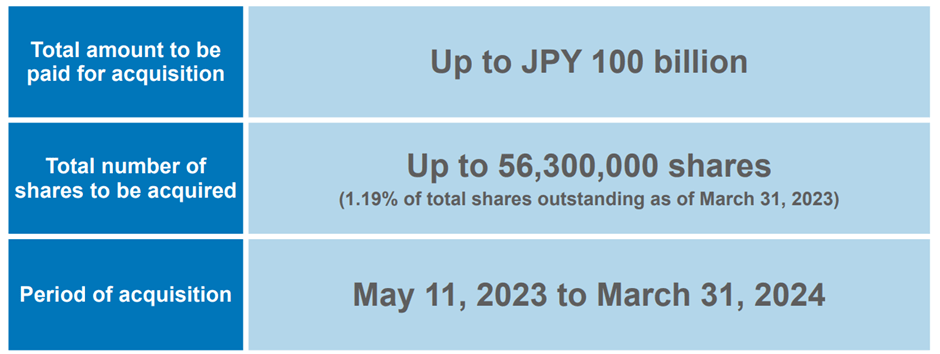

Headline full-year numbers (fiscal year ended March 2023) from Softbank Corp might have fallen short of consensus (operating profit of JPY1.06trn, EPS of JPY113/share), but much of the delta was down to P&L weakness at consolidated subsidiary Z Holdings and its other strategic investments. The core telco business was resilient, helped by broad-based strength across its consumer and enterprise segments. Key performance indicators were also steady for mobile, with net adds coming in at >1m (including for Y! mobile, LINEMO, and LINE MOBILE). Net additions were even stronger for smartphones at ~1.7m; alongside the low churn rate, subscriber gains from rival carriers over the last year appear to be stickier than expected. With adj FCF generation now at >JPY600bn, the dividend per share of JPY86 (consistent with prior years) has been supplemented with a JPY100bn buyback (>1% of the current market cap).

{kind=link}

Near-term guidance of JPY780bn operating profit and JPY89 of EPS also disappointed, though, as marketing and promotional spending will ramp up in the consumer segment. That said, mobile service revenues should get a boost from Softbank Corp’s aggressive subscriber acquisition strategy, as well as continued upselling onto bigger data plans over time. Also positive was the double-digit operating profit growth forecast for the enterprise segment, helped by lower subscriber acquisition spend and rising sales. Finally, the financial segment remains a potential source of upside as PayPay, helped by its massively expanded scale, moves closer toward breakeven. Potential cross-synergies, such as common IDs for the SoftBank ecosystem (Yahoo! Japan, LINE, and PayPay), also remain relatively untapped. On the other hand, there is a risk of further earnings weakness at Z Holdings (a key drag for the latest fiscal year results), so the guidance is probably fair on balance.

New Mid-Term Plan Highlights Cash Generation Potential

Alongside the full-year earnings release, Softbank Corp also outlined its new mid-term business plan headlined by profits attributable to owners of the parent (i.e., excluding effective interests of ~33% in Z Holdings and ~44% in PayPay) of JPY535bn (+13% per year). Additional financial targets include consolidated operating profits of JPY970bn (+11% per year), which nets out to a relatively conservative 4% per year EPS growth target.

{kind=link}

While the plan also hinges on >1m of yearly net adds, Softbank’s subscriber momentum over the last year (>1m of mobile net adds and ~1.7m smartphone net adds) suggests this is well within reach. Given management’s tendency to guide conservatively, I feel comfortable underwriting an inflection in mobile service revenues over the next year, along with enterprise continuing to grow at a steady double-digit % pace. Alongside the strong growth and operating leverage potential in the financial segment (mainly PayPay), where a mid-term breakeven/profitability scenario seems increasingly likely, Softbank Corp looks poised for upward revisions down the line.

{kind=link}

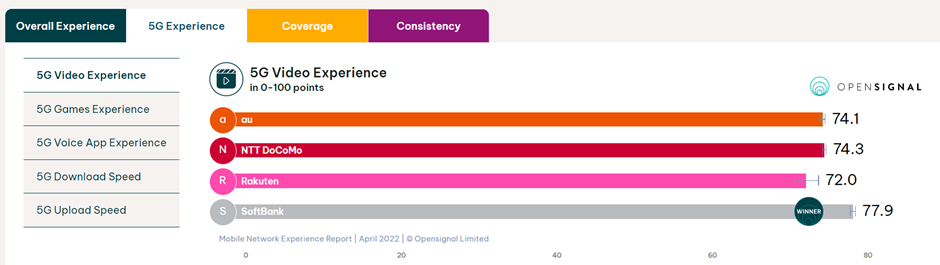

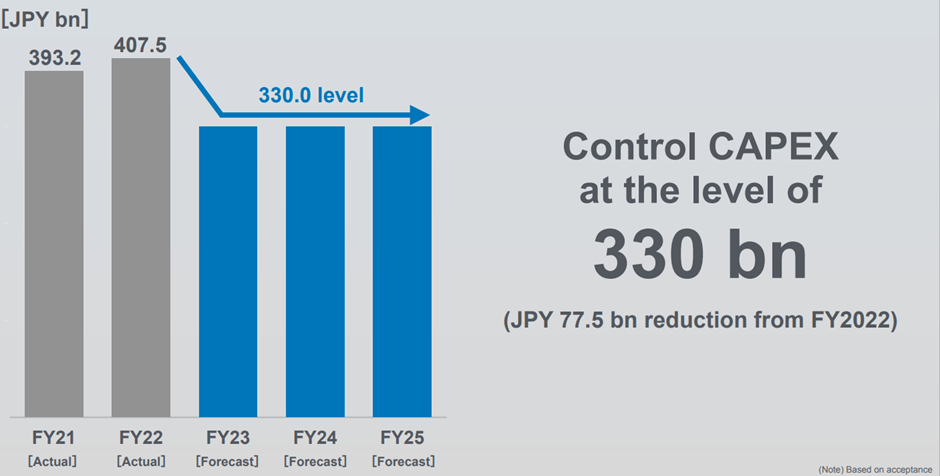

The cash flow and balance sheet sides will also get a boost from the wind-down of Softbank’s multi-year capex cycle. Having leveraged dynamic spectrum sharing (i.e., allowing for dynamic spectrum allocation between 4G and 5G without needing additional spectrum) to build out a high-quality nationwide 5G network with maximum coverage (currently >90%) and quality, the telco now has the best 5G experience in Japan (ahead in four out of five ‘5G experience’ categories per OpenSignal ).

{kind=link}

As a result, management is now targeting a lower telecom capex run rate of JPY330bn/year for consumer and enterprise. This should keep telco FCF well above JPY600bn/year, in turn boosting the dividend payout potential from here. With the current total return yield already up to ~7% (dividend and buybacks), well above the rest of the sector and well-covered by the underlying cash generation, the stock is poised to re-rate.

{kind=link}

A Cheaply Priced Bond Proxy

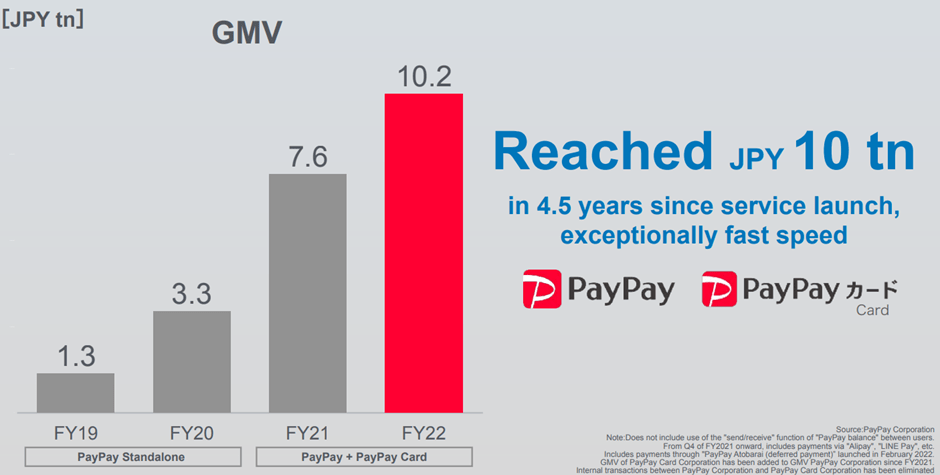

Softbank Corp’s headline FY results and forward guidance may have fallen short of consensus, but the updated mid-term plan targeting a steady low-teens % operating profit growth algorithm should give investors reason for optimism. Having invested in building out best-in-class 5G infrastructure, the company’s capex cycle will also be winding down, presenting upside to future FCF generation. Underwriting sustained earnings growth from the core telecom business and the fast-growing, capital-light PayPay business (gross merchandise value up to ~JPY10tn from ~JPY1tn in four years) doesn’t seem all that demanding here; hence, the JPY86/share dividend seems well-covered. Having underperformed the broader Japanese index YTD, the stock remains one of the few ‘cheap’ names at an undemanding ~7x EBITDA while offering an ~7% total shareholder return yield (dividend and JPY100bn of buybacks).

For further details see:

SoftBank Corp: A Cheaply Priced Bond Proxy