SOHU - Sohu.com: A High Risk Reward Buy

2023-10-26 01:31:22 ET

Summary

- Sohu.com is facing weakening fundamentals due to a sluggish economy and a declining user base in its core game TLBB.

- The company has a massive cash balance and no debt, which is likely to help them through the current crisis.

- Sohu.com plans to rejuvenate its gaming portfolio with the launch of a new TLBB mobile game and expansion packs, which could stabilize its user base.

Investment Thesis

Sohu.com ( SOHU ) had been facing with weakening fundamentals amidst advertisers shying away due to sluggish economy and declining user base in its core game TLBB. We initiate with a cautious buy with a high risk reward as we believe the company's massive cash balance (5x the current market cap) and no debt which is likely to tide them through the current crisis. Despite that, we keenly look at the adoption of its revamped gaming portfolio and stability in its user base.

Company Background

Sohu is a leading brand in China across different sub-segments within Internet including online media, video, and games. Key brands include Sohu (Online media content and services provider) and ChangYou (Online game developer). The company primarily generates revenue via online advertising revenues through its gaming platform (~80%) as well as distribution services with a diverse portfolio of games including legacy Tian Long Ba Bu (TLBB) along with advertising (~14%) through Sohu's media and video platforms along with a real estate platform, Focus.

Historical Track Record

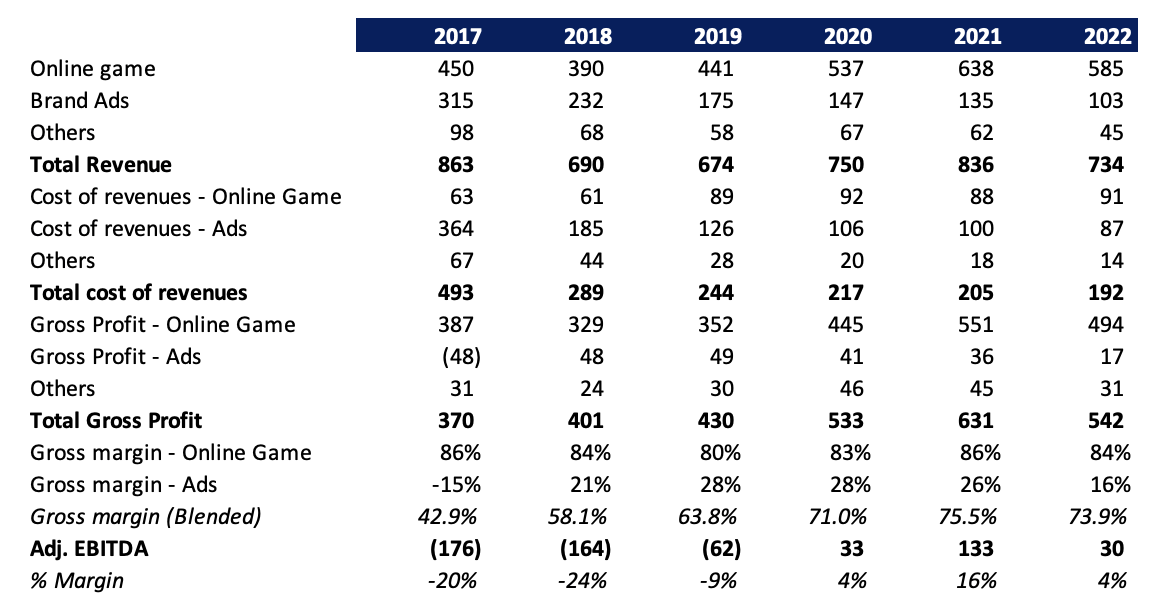

The company previously owned a search engine, Sogou, which it later sold to Tencent in 2021 for $3.5 bn. The company had volatile track record of earnings primarily as a result of persistent weakness in brand advertising. The decline was primarily a result of its shift to self-producing video content from the purchased content which has made them relatively profitable (gross margins trended upwards of 20% during 2018-21) but generated less user traffic and revenues. In addition, its online gaming business reported solid growth during 2020-2022 as a result of strict lockdowns in China which forced people to spend more time online on games. However, since the lifting of the COVID curbs revenues within its online gaming segment started declining as more people started going out. In addition, higher marketing spends within its online gaming segment had led to a decline in its EBITDA margins in 2022 from the highs of 2021 which did not require a 'customer-pull' strategy.

{kind=link}

Weakening Fundamentals

The company has reported a consistent decline in sales since last several quarters primarily as a result of its declining monthly active users within its online game TLBB and lack of any innovative features. Monthly active users have declined from 3.4 mn at the peak of COVID to 1.3 mn in mobile games.

In its latest quarter, the company reported a revenue decline of 22% YoY driven by broad-based decline across both brand advertising and online gaming segments. While the company has been able to maintain its gross margins, given the high marketing spends it has to incur for attracting customers, the company has reported operating losses amidst declining sales since past few quarters.

The company continues to expect weak Q3 with brand advertising revenues to decline by up to 18% YoY and online gaming revenues to decline by up to 27% as a result of continued decline in its paying accounts.

Taking a Holistic View

The company ended up with cash balance of ~$1.38 bn (including the long-term time deposits) down about $55 mn during the first half of the current year. This pales in comparison to the company's current market cap of under $300 mn as the Street views that the company is likely to use up most of its cash to fund losses. However, we believe even if the losses exacerbate, the company has a relatively long runaway compared to most of the companies. While we believe the gaming industry is rapid with fast technology advancements and the reliance on its legacy old games of TLBB could compel them to chasing users instead of attracting them and may lead to slow death.

The company has several plans going forward to rejuvenate its gaming portfolio including the launch of a new TLBB mobile, its next-generation TLBB product along with expansion packs and content developments which will be published by Tencent. It would be imperative to see if the company does see any stability in its user base going forward as a result of increasing engagement. In addition, it has been able to sustain gross margins and the user decline could well stabilize heading into 2024 as a result of new game features as well as core pipeline.

Valuation

Consensus analyst estimates 2024 revenues to stabilize at $627 mn as they believe the worst may be over for online gaming revenues which can improve going forward. We adopt a cautious view and expect NTM revenues in brand advertising to continue to decline in double digits with NTM revenue expected to be about $75 mn. In addition, we believe online gaming revenues to be ~$380 mn assuming a continued sequential decline in revenues by low double digits. This totals to about $455 mn in consolidated revenues for the next 12 months. Assuming a blended conservative gross margins of 70%, gross profit comes to be about $318 mn, and with higher marketing spends and increasing spends on product development, we estimate operating losses to the tune of $260 mn during the next twelve months.

We practically are not appropriating any value to Sohu's media business as a result of the strong competition from other players and its relative decline historically. Assuming a cash outflow to the tune of $260 mn over the next year, the company may well end up with a cash balance of $1.12 bn. We appropriate a discount of 80% to its cash balance assuming significant portion of its existing balance is going to be used up in funding its losses. This translates to $276 mn, which is near the company's current market capitalization. We believe the potential is there for significant upside but is fraught with risks till the time the company has been actually maintaining its user base and arresting a continued decline.

While we do not have exact peers for the company as a result of its unique business model focused on a geography, Chinese internet stocks currently trade around 0.3x with the exception of Weibo. We ascribe a 0.18x EV/ Revenue to its online gaming revenue segment, at a 50% discount to the larger peers, which translates to a value of $66 mn. Considering the existing cash balance, this translates to a cumulative value of $342 mn which is at a premium of about 25% to the current market price. We initiate with a Cautious Buy rating given the current risk reward.

Risks to Rating

Risks to rating include

1) Its inability to attract users can lead to a significant decline in its online gaming business

2) Technological advancements and new games can cause significant competitive pressure and make its game obsolete

3) Its operations in China are subject to significant regulatory and political changes and any adverse policies can impact growth

4) China's economic growth pressures can cause lower advertising revenues as well as a jump in operating losses

Final Thoughts

Sohu has declined about 40% over the past 6 months as a result of weakening fundamentals and a continued decline in its online gaming user base. Despite that, we believe the company's massive cash balance provides them a significant runaway to fund any operating losses and we expect the user base is likely to stabilize with the launch of its newly revamped TLBB Mobile game with Tencent. We initiate as a Cautious Buy with a high risk reward.

For further details see:

Sohu.com: A High Risk Reward Buy