SOI - Solaris Oilfield Is Well Positioned For Growth Ahead

2023-04-03 17:10:17 ET

Summary

- Solaris Oilfield Infrastructure reported its Q4 2022 results on February 22, 2023.

- The firm provides well-site equipment for hydraulic fracturing operations in the U.S.

- SOI has produced strong growth in revenue and operating income and appears well-positioned for further growth.

- My outlook is a Buy at around $8.90 per share.

A Quick Take On Solaris Oilfield Infrastructure

Solaris Oilfield Infrastructure ( SOI ) reported its Q4 2022 financial results on February 22, 2023, missing revenue and meeting EPS consensus estimates.

The firm designs and manufactures well-site proppant and fluid management systems for hydraulic fracturing well operations purposes.

SOI is well-positioned in the market with its top-fill system and integrated approach, which helps customers to save money and increase productivity.

My outlook for SOI is a Buy at around $8.90 per share.

Solaris Overview

Houston, Texas-based Solaris Oilfield Infrastructure was founded in 2014 to provide a range of oilfield service equipment products focused on the hydraulic fracturing process of extracting hydrocarbons from unconventional geologic structures.

The firm is headed by founder, Chairman and CEO William Zartler, who is also the founder and CEO of Aris Water Solutions, an oilfield service company that provides water solutions to fracking well-site operators.

The company’s primary offerings include the following:

-

Proppant management system

-

Sand loading system

-

Fluid management system

-

Autoblender

-

Automated control systems

-

Last mile management

Solaris’ Market & Competition

According to a 2022 market research report by Maximize Market Research, the global market for proppant (as a proxy for the proppant equipment market) was estimated at $8.34 billion and is forecast to reach $14.23 billion by 2029.

This represents a forecast CAGR of 6.9% from 2022 to 2029.

The main drivers for this expected growth are new technologies propelling the hydraulic fracturing industry to use more proppant in their well-site operations.

Also, ceramic proppants can outperform sand proppant as a specialty product in terms of stress and crush resistance.

The cost of ceramic proppant is around 50% higher than frac sand.

A breakdown of proppant type and related approximate market share in 2021 is shown below:

Global Proppant Market By Type (Maximize Market Research)

Solaris’ Recent Financial Results

-

Total revenue by quarter has risen per the following chart:

Total Revenue History (Seeking Alpha)

-

Gross profit margin by quarter has trended higher in recent quarters:

Gross Profit Margin History (Seeking Alpha)

-

Selling, G&A expenses as a percentage of total revenue by quarter have moved downward recently:

Selling, G&A % Of Revenue History (Seeking Alpha)

-

Operating income by quarter has risen significantly above breakeven in recent reporting periods:

Operating Income History (Seeking Alpha)

-

Earnings per share (Diluted) have also turned positive more recently:

Earnings Per Share History (Seeking Alpha)

(All data in the above charts is GAAP)

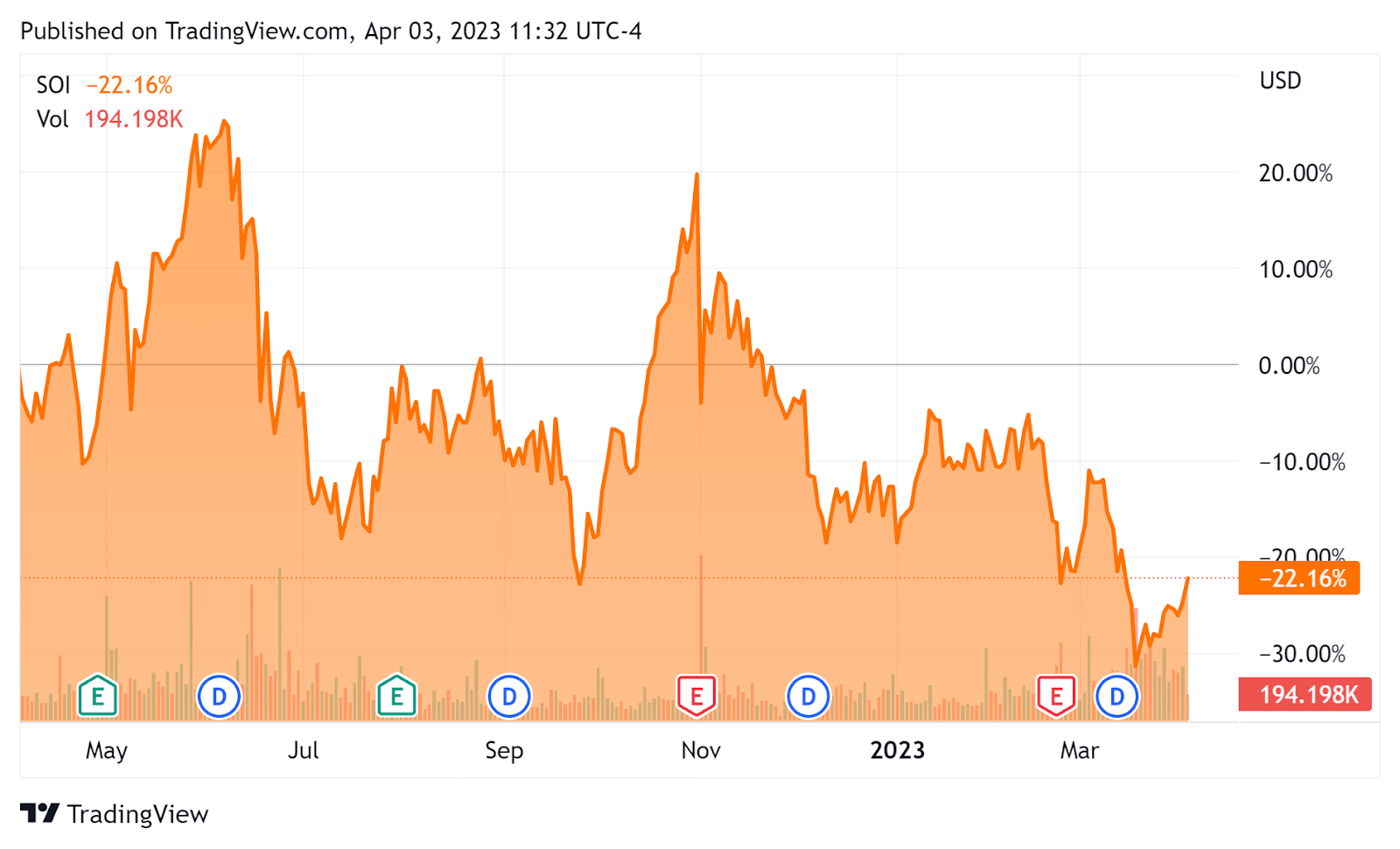

In the past 12 months, SOI’s stock price has fallen 22.16%, as the chart indicates below:

52-Week Stock Price History (Seeking Alpha)

{kind=link}

As to its Q4 2022 financial results, total revenue rose an impressive 83.2% year-over-year and gross profit margin increased by 3.1 percentage points.

SG&A expenses as a percentage of total revenue dropped markedly year-over-year and operating income has risen sharply in recent quarters.

Earnings per share have followed suit, rising materially in recent reporting periods.

For the balance sheet, the firm finished the quarter with $9.0 million in cash, equivalents and short-term investments and $8.0 million in total debt.

Over the trailing twelve months, free cash used was $13.4 million, of which capital expenditures accounted for $81.4 million. The company paid $6.1 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For Solaris

Below is a table of relevant capitalization and valuation figures for the company:

| Measure [TTM] |

| Amount |

| Enterprise Value / Sales |

| 1.3 |

| Enterprise Value / EBITDA |

| 5.3 |

| Price / Sales |

| 0.8 |

| Revenue Growth Rate |

| 101.0% |

| Net Income Margin |

| 6.6% |

| GAAP EBITDA % |

| 23.7% |

| Market Capitalization |

| $403,250,000 |

| Enterprise Value |

| $399,430,000 |

| Operating Cash Flow |

| $68,000,000 |

| Earnings Per Share (Fully Diluted) |

| $0.64 |

(Source - Seeking Alpha)

Future Prospects For Solaris

In its last earnings call (Source - Seeking Alpha), covering Q4 2022’s results, management highlighted its continued investment in its top-fill system and customer preference for this type of sand system, resulting in strong growth in this segment.

Leadership believes its approach of providing a full set of offerings ‘translates to more wells per frac crew and ultimately results in lower operating costs’ for its customers.

The company will likely prioritize its capital expenditures in the first half of 2023 to enable it to take advantage of opportunities as the year progresses.

Looking ahead, while management sees strong demand for its top-fill system, the firm is not immune to recent weakness in natural gas, as the Seeking Alpha one-year chart for natural gas futures shows below:

Natural Gas Futures History (Seeking Alpha)

{kind=link}

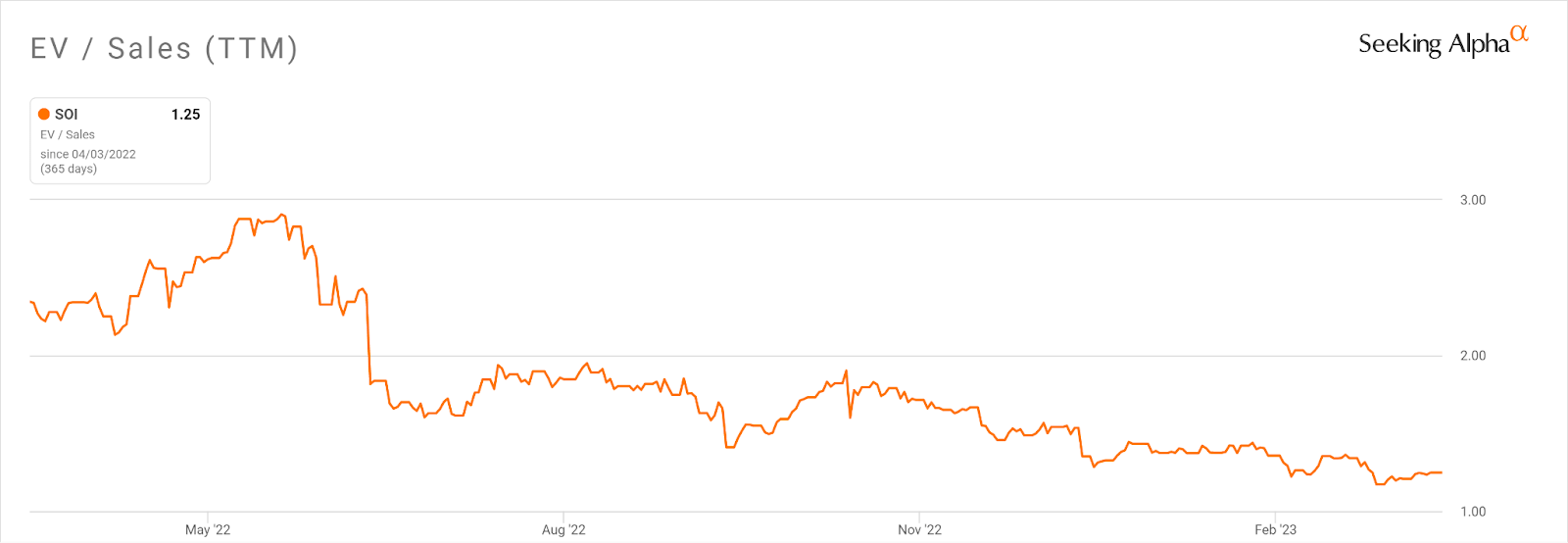

Regarding valuation, the stock has seen significant EV/Sales multiple compression over the past year, despite sharply improving revenue and operating income results:

EV/Sales Multiple History (Seeking Alpha)

{kind=link}

The primary risk to the company’s outlook would be a further decline in natural gas prices.

However, the stock was highly responsive to the recent OPEC output cut, rising over 4% on the announcement.

My bet is that natural gas prices have most of their drop behind them and that SOI is well positioned to take market share due to its more popular top-fill systems.

My outlook on SOI is a Buy at around $8.90 per share.

For further details see:

Solaris Oilfield Is Well Positioned For Growth Ahead