AIG - Solid Underwriting And Higher Rates Make AIG A Buy

2023-09-08 10:42:08 ET

Summary

- AIG's shares have rallied since March and are now trading around the $60 target, with the potential to reach $70 in the next year.

- The company's financials have improved, with its highest level of earnings since before the financial crisis.

- AIG's investment portfolio is also benefitting from higher rates as it reinvests maturities.

Shares of American International Group ( AIG ) have enjoyed a steady rally since their March lows and are now trading around the $60 target I argued for last October . As such, it is an appropriate time to re-evaluate the stock to determine if shares should be sold or if the target should be increased. My review of the business has concluded that the company continues to improve its performance, and I believe shares can move towards $70 over the next twelve months.

{kind=link}

In the company's second quarter , it earned $1.75 in adjusted EPS; this was the company's highest level of earnings since before the financial crisis. It is obviously a much different company than back then, when it was a financial conglomerate that, in addition to standard insurance, owned and leased planes, insured complex financial instruments, and had expansive global operations. Today, the company primarily focuses on property and casualty insurance, with about 70% of the business in North America.

While the company's financials include results from its life and retirement unit, it is important to remember that the lion's share of these results come from Corebridge ( CRBG ) as AIG owns 65.3% of the company, which it spun out last year, in the final major step of its multiyear business simplification. It originally owned 78% of the company, but it sold $1.2 billion of stock in June. That remaining stake is worth just over $7 billion at current market prices.

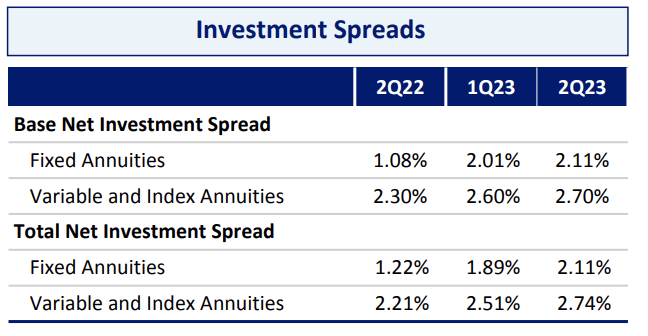

The results in this unit have been strong, which matters in so far as strong results should support CRBG's share price and the ability of AIG to monetize the asset. In its retirement unit, adjusted pre-tax income jumped 33% to $991 million with a return on equity of 12.2% even as alternative investments income fell 15%. This is because higher interest rates are allowing the company to earn wider spreads on annuities. When I value AIG though, I focus on the earnings of its fully owned business and then add in the value of its equity stake in CRBG.

{kind=link}

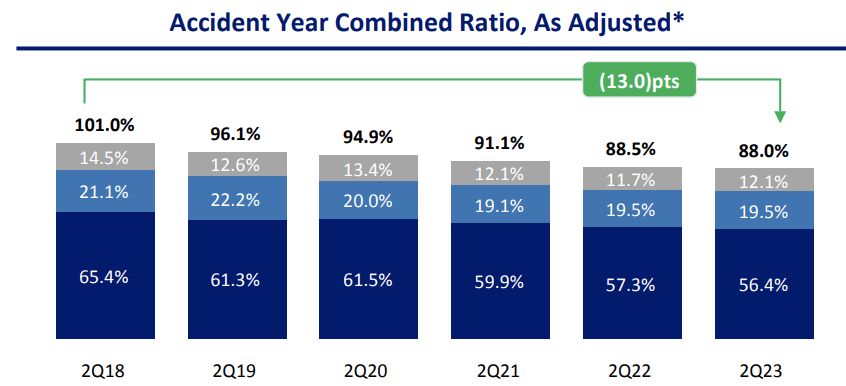

Last quarter, AIG reported a 10% growth in general insurance net premiums written to $7.5 billion. Its adjusted accident year combined ratio was 88%, a 50bp improvement from last year, a sign that tightening underwriting standards is flowing through to results. It has been a long road, but after five years of improvement, the accident ratio is in a healthy place, below 90%.

{kind=link}

My view has essentially been that after the financial crisis with its brand so tarnished, AIG aggressively priced policies to retain business, leading to poor underwriting results. As a reminder, a combined ratio of 100% means that paid claims equal premiums - this is financial breakeven. At 88%, the company is making 12 cents on every dollar of premiums it writes, a strong place to be in. AIG has made the transition from being a poor underwriter to a solid one. That it is now growing premiums written while maintaining a lower combined ratio is an encouraging sign that the brand has sufficiently recovered, and it can gain market share without having to undercut on pricing.

As an insurer, underwriting is just one of two ways a company earns a profit. The second is the investment of the premiums, and this is where higher interest rates are a tremendous tailwind, even more so than I expected last year, given the Fed raised rates 100bp further in the first half of the year.

Its general insurance portfolio has a duration of just under 4 years , and this short duration means it is able to redeploy significant amounts of its portfolio each year into higher-yielding investments, given the Fed's rate hikes. In fact, in its general investment account, the average maturity last quarter yielded 1.9%, and it is investing now at 4.69% on average. The portfolio's yield is up to 3.65% from 2.72% last year. On its general insurance portfolio, that is an extra $700 million of pretax income. If rates remain at current levels for the next year, there should be at least another $200 million tailwind.

While there has been concern about commercial real estate, particularly office space given the increase in remote work, less than 3% of AIG's portfolio is loans to office buildings and 78% of that is in the highest quality "Class A" buildings. As such, even if commercial real estate faces a significant downturn, AIG's exposure is quite manageable.

Essentially, AIG is generating about $2.6-2.8 billion in pre-tax underwriting income. Plus, assuming rates hold steady, it should earn about $3 billion in pre-tax investment income over the next year. That is $5.7 billion in pre-tax profits, less about $1.7 billion in corporate expenses, for about $4 billion in pre-tax profits, which can lead to about $4.05-$4.15 in EPS, over the next 12 months when excluding its retirement business.

However, it should be noted that some of its GAAP tax bill, which reduces EPS, can be credited against its deferred tax asset from losses in the past, leaving it with additional cash flow to buy back stock.

Indeed, AIG has been aggressively buying back shares. It bought back $554 million in stock in Q2 with another $400 million in July, leading the board to increase its authorization to $7.5 billion. AIG has been able to repurchase stock without endangering its balance sheet. Debt to capital has actually fallen over the past year to 31.6% from 32.8%. Its risk-based capital ratio is estimated to have ended the quarter in the 470-480% range, nearly 100 percentage points higher than Lincoln Financial ( LNC ), for instance.

With its strong capital position, AIG is well-positioned to return all of its earnings to shareholders via dividends and buybacks. As noted as well, it still owns 65.3% of Corebridge, and it will likely take a few years to wind down the stake to avoid selling too much too quickly and hitting Corebridge's share price. Still, the monetization of this stake will enable AIG to continue its meaningful share repurchase program, above and beyond underlying earnings.

Today, shares are trading at right around its $58.49 book value. Adjusting for its deferred tax asset and accumulated other comprehensive income (AOCI), the book value is $75.76. With higher reinvestment rates steadily increasing investment income and underwriting now generating steady profits, I view the stock as attractive around book value. I prefer to use a sum-of-the-parts valuation approach, though. At current levels, Its CRBG stake is worth about $10 per share. AIG also receives about $350 million in regular dividends from its stake, which is equivalent to about $0.40 of EPS, for a combined EPS of ~$4.50. At a 13x multiple, given the stability but slow growth of the earnings profile, that is about $58, plus $10 for its CRBG stake, or about $68 per share, or 0.9x adjusted book value.

Given the share count is likely to fall about 5% within the next year due to the buyback, I am targeting about $70 for AIG over the next twelve months. It should be noted that over time we will see the value of its CRBG stake and the associated dividend decline as AIG sells shares, but with proceeds going to reduce its own share count, the run-rate EPS of its general insurance unit will rise, providing a natural offset.

AIG has turned the corner from being a "turnaround story" to a solidly-run franchise. Higher rates are helping to compound the gains as investment income gradually and steadily rises. This combination, aided by aggressive share repurchases and a strong balance sheet, can lead to continued share appreciation. I would remain long AIG stock.

For further details see:

Solid Underwriting And Higher Rates Make AIG A Buy