SLVYY - Solvay Could Split Itself In 2 Plenty Of Upside Likely At Just 4.5x EBITDA

Summary

- Solvay is a large chemical company considering splitting itself in an EssentialCo and SpecialtyCo.

- This is an attempt to create shareholder value, as the stock is currently trading at a single-digit P/E and a double-digit sustaining free cash flow result.

- I missed out on picking up a substantial position in Solvay in the past three years, but I will almost certainly buy on the next dip.

Introduction

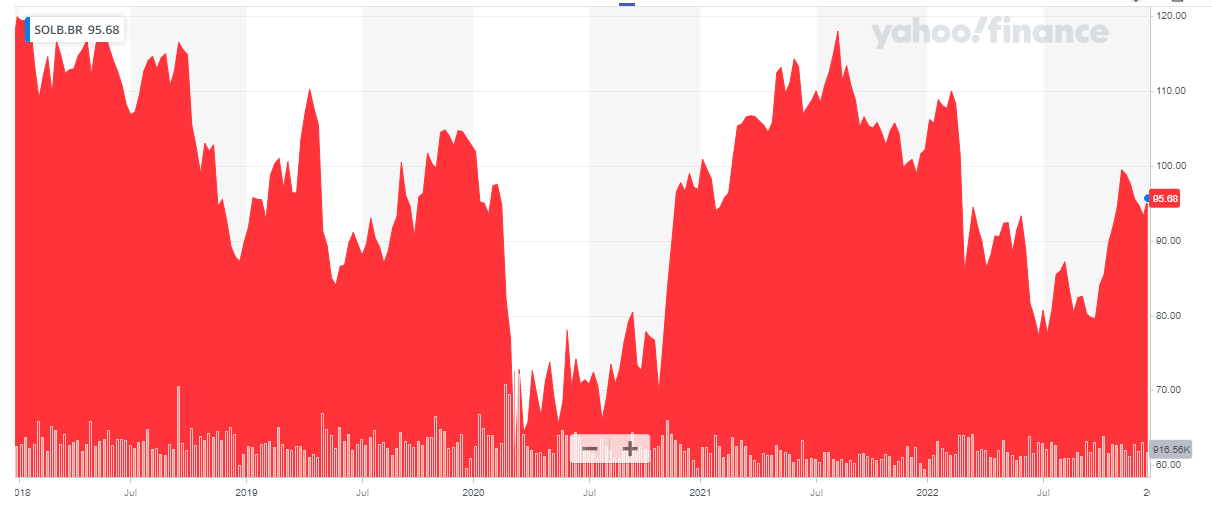

I try not to have too many regrets in life, but not picking up Solvay ( SVYSF ) ( SOLVY ) during the COVID-crisis now almost three years ago is one of them. The share price didn’t fall as deep as the share prices of competitors did and even in 2022, the year the European energy crisis was an important theme, Solvay performed much better than its peers in the European chemical sector.

{kind=link}

That being said, the share price is currently trading 15% lower than the last time I discussed Solvay here on Seeking Alpha , and it is trading pretty much at the same level it was at when I published an update article in 2019 .

Solvay’s primary listing is in Belgium, where it belongs to the BEL20 index of Euronext Brussels. The ticker symbol in Brussels is SOLB and the average daily volume exceeds 200,000 shares for a total dollar value of approximately $20M per day. As that clearly is the most liquid trading venue, I strongly recommend to use the Euronext Brussels listing.

On track for a very strong year

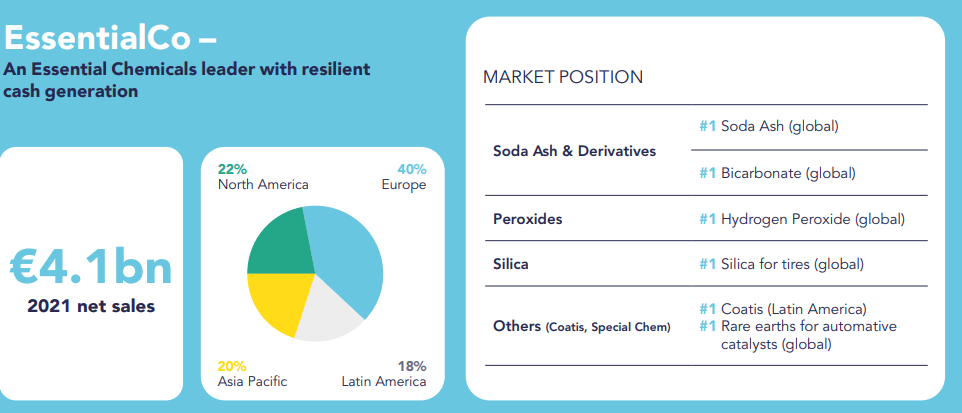

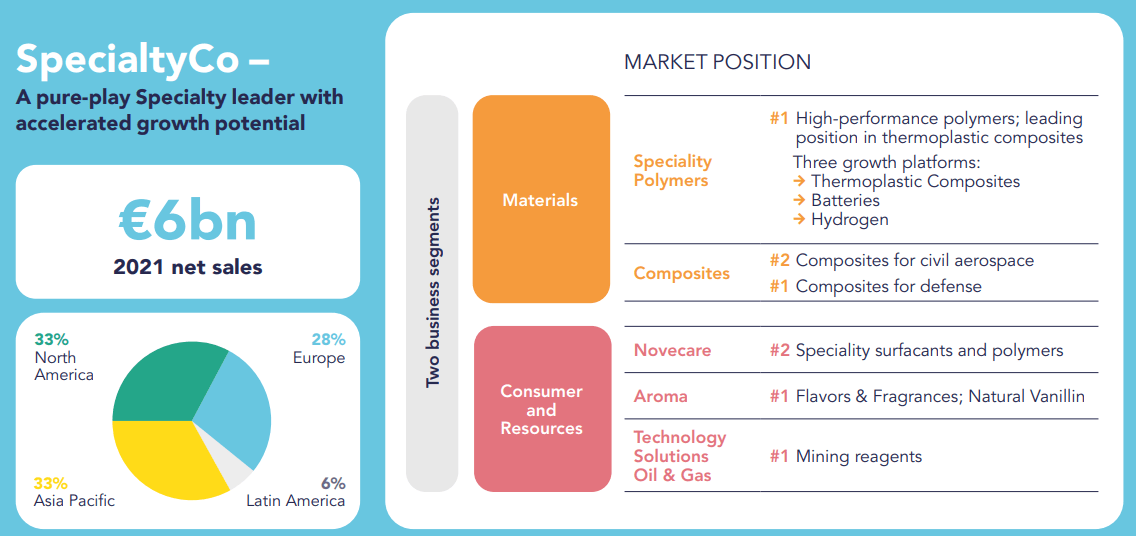

Solvay’s focus points are relatively easy to explain. The company’s financial performance is dominated by two specific business segments: ‘ EssentialCo’ and ‘SpecialtyCo ’ which is again separated into a materials and consumer & resources subdivision. Solvay is considering splitting itself up in two, with EssentialCo and SpecialtyCo operating as two separate entities. Nothing has been decided yet, but we will likely see and hear more about this in 2023.

{kind=link}

And throughout both divisions, there is one common theme: Solvay is either the market leader or ranks second in that specific market.

{kind=link}

As about 70% of its revenue (in 2021, but I’m not expecting huge changes) was generated outside of Europe and as Solvay has activities all over the world, it is pretty shielded from the fall-out from the Ukraine-Russia war, although it definitely does notice the impact as the cost of energy has not only gone up in Europe this year.

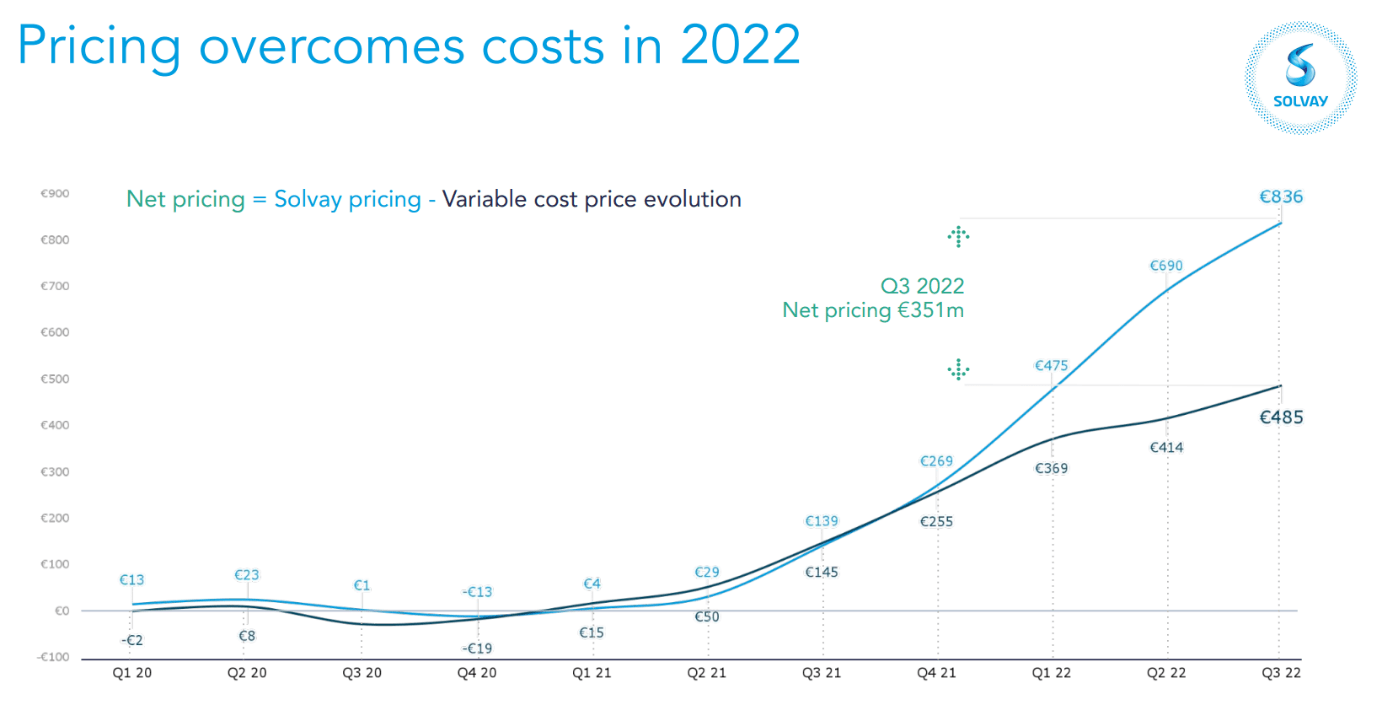

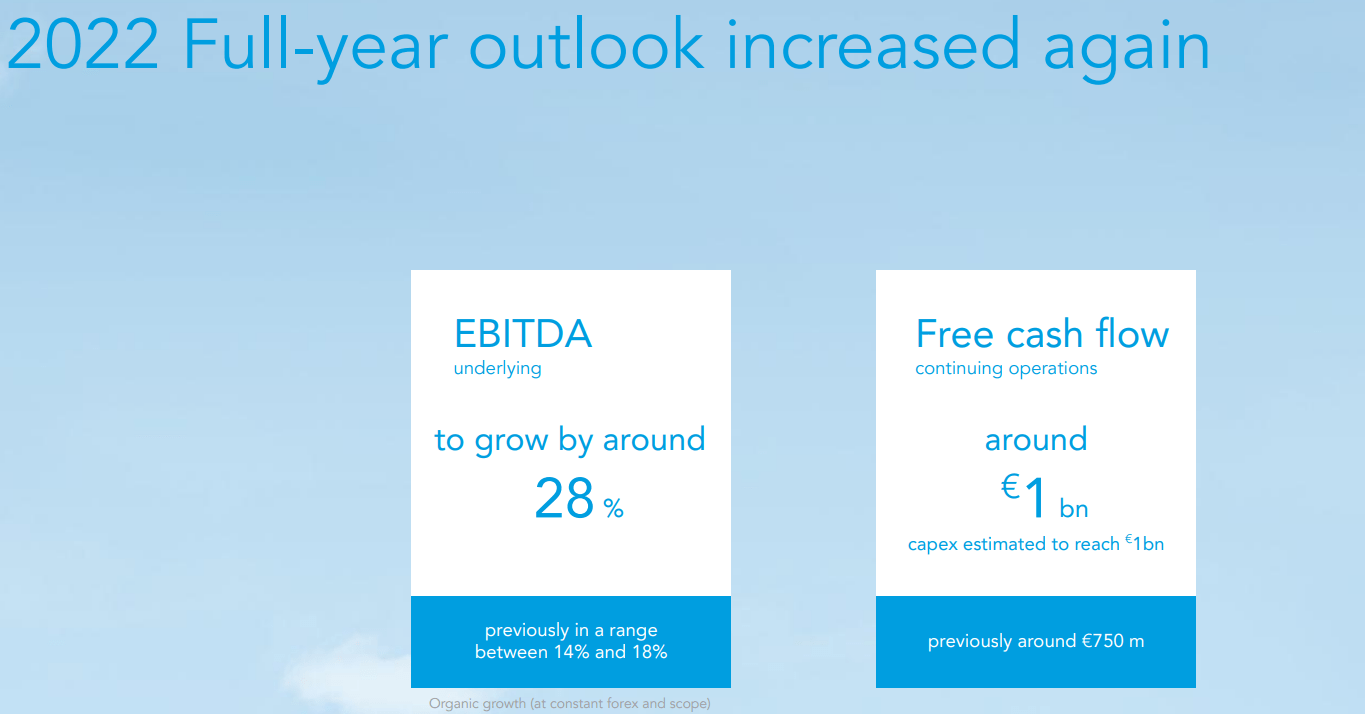

2022 will be an excellent year for Solvay, in my opinion, as the company was able to hike its full-year guidance again when it published its Q3 results.

The company’s Q3 revenue came in at 3.6B EUR, which resulted in a 9M 2022 revenue of 10.1B EUR. That already equals the total revenue generated in the entire financial year 2021. While a large portion of the revenue increase is caused by the impact of inflation, let’s keep in mind Solvay has been able to hike prices faster than the cost of the inputs has increased , which really shows how advantageous its position as number 1 or 2 in pretty much every market is.

{kind=link}

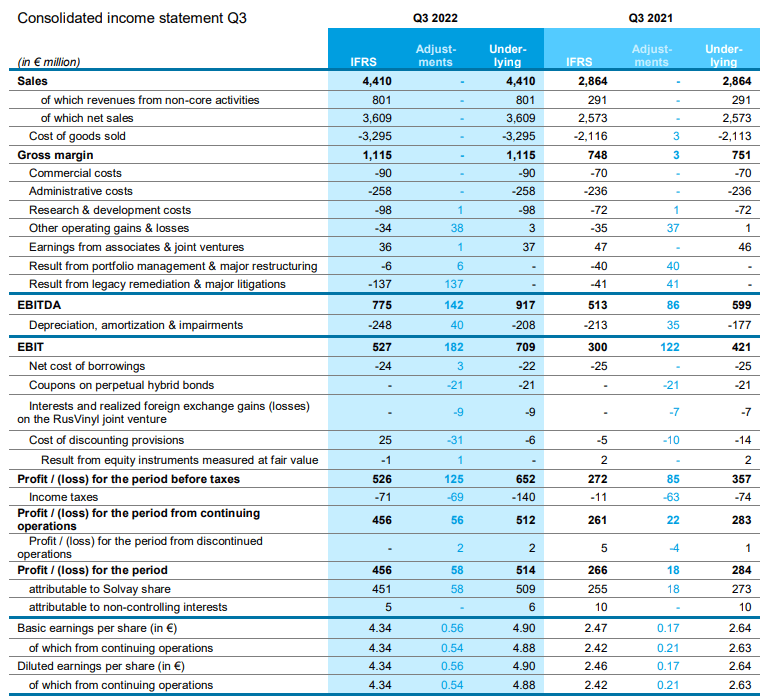

One element that sometimes makes Solvay difficult to understand it its reporting standard: it reports its results in an IFRS-compliant way, but it also publishes the ‘underlying’ results which adjust the company’s financial results for non-cash purchase price allocation accounting impacts. As Solvay continuously refers to its underlying results, I will include this in the financial discussion here, and the income statement below shows the adjustments made to the IFRS results to end up with the underlying result.

{kind=link}

While reported EPS for the third quarter was 4.34 EUR per share, the underlying EPS was actually 3.90 EUR per share as the 137M expense related to legacy remediation and major litigations was added back to the equation.

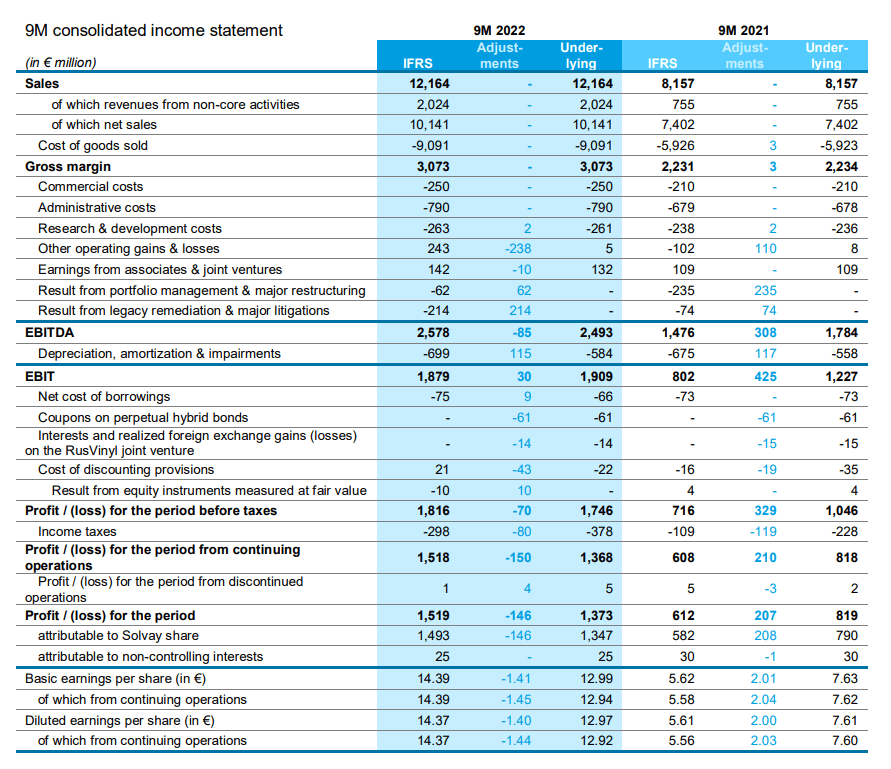

Looking at the 9M 2022 income statement, we see the underlying result was actually lower than the reported net income as the underlying EPS was 12.99 EUR per share versus the reported earnings of 14.39 EUR per share.

{kind=link}

The main culprit was that although the underlying pre-tax income was lower (1.75B EUR underlying versus 1.82B EUR reported), the tax bill was higher (378M EUR versus 298M EUR) due to certain adjustments and corrections in the financial results.

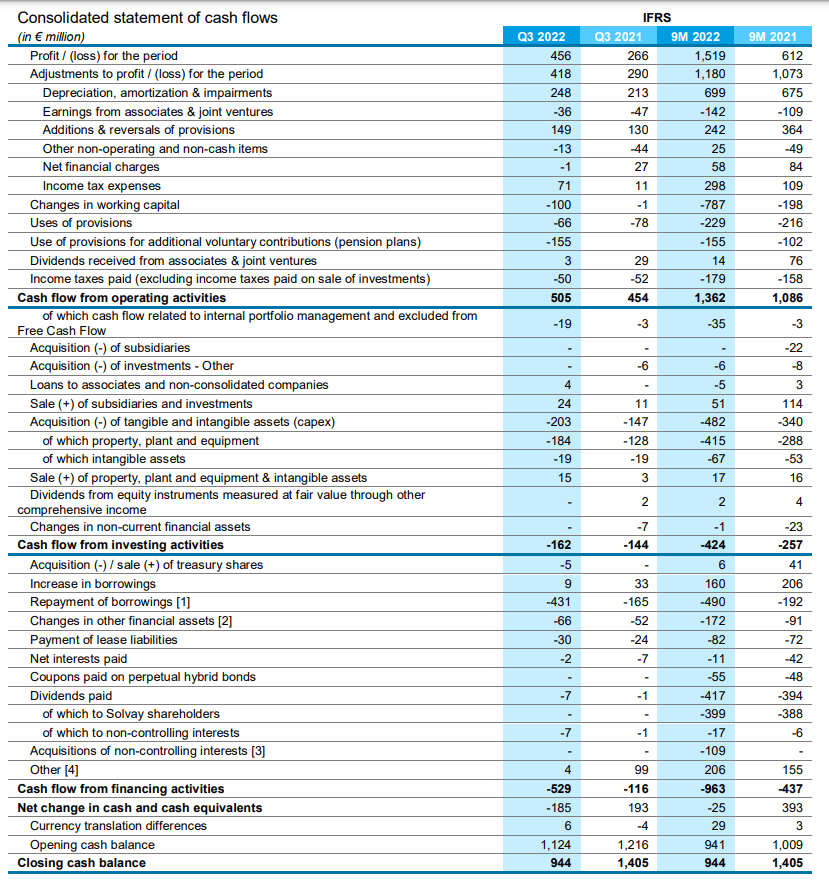

As I mainly like to judge a company based on its free cash flow result, it goes without saying I had a closer look at Solvay’s cash flows as well. I like how the company was able to scale up its capex as Solvay realizes it is on track for a very strong year (cash flow wise). This paves the way to increase the capital expenditures while still posting about a billion euro in free cash flow this year.

{kind=link}

In the first nine months of this year, Solvay generated 1.36B EUR in operating cash flow. Keep in mind this includes a 787M EUR investment in the working capital position, and it also includes just 179M EUR in cash taxes versus the 298M EUR the company owes based on its results.

We should also deduct the 17M EUR dividend payment to non-controlling interests and the 148M EUR in lease and interest payments (including the coupons paid on perpetual hybrid bonds).

This means that on an adjusted basis, the operating cash flow was 1.87B EUR. The total capex was just 482M EUR, resulting in a free cash flow result of approximately 1.4B EUR.

Looking ahead: 2023 and 2024 will be weaker than 2022

2022 clearly will be an excellent year for Solvay, but there’s very little doubt the Belgian company will not be able to repeat its excellent performance in 2023. And that’s fine: Solvay will already have made a very big step forward as the net debt is decreasing fast and creates a strong set-up for next year.

But first things first. When Solvay announced its Q3 2022 results, it hiked its full-year capex guidance to 1B EUR, and it mentioned it expected to report 1B EUR in free cash flow (which includes working capital changes).

This means the Q4 capex will be pretty high at roughly half a billion Euro, but this will all be ‘money well spent’: Solvay is simply pulling forward some of its anticipated growth investments. As the cash is pouring anyway, the company may as well spend it on projects it was already budgeting for, further down the road.

This means two things: first of all, the underlying free cash flow result adjusted for working capital changes will likely be higher than the 1B EUR in FCF Solvay is guiding for, and secondly, the total capex may be lower in the next few years. Perhaps not yet in 2023, but from 2024 on the capex will likely decrease again. But that’s the theory. If Solvay continues to find growth investments that meet its internal IRR and return hurdles, I see no reason why Solvay shouldn’t simply continue to invest in itself.

{kind=link}

The consensus estimate for the 2023 EBITDA is 2.6B EUR . That would be a 15% decrease compared to the 3-3.1B EUR Solvay’s EBITDA guidance implies. And that’s fine as this would still imply an EPS of approximately 10 EUR per share while the free cash flow result will be slightly lower, assuming Solvay will spend 1B EUR on capital expenditures next year as well.

The sustaining capex is likely substantially lower, which means the underlying sustaining free cash flow is likely closer to 1.2-1.3B EUR (based on a sustaining capex of 80% of the depreciation expenses).

Investment thesis

I don’t think there’s any rush to get into Solvay, but I do regret not picking up the stock in 2020 and even earlier this year. I think I have learned my lesson and will take advantage of the next weak moment. Keep in mind the EBITDA and net income in both 2023 and 2024 will likely be lower than in 2022, so perhaps the market may be negatively surprised by the 2023 guidance if it comes in below the 2022 performance.

In any case, Solvay appears to be attractively priced at less than 10 times earnings on a normalized EBITDA from next year on while the debt ratio will likely come in below 0.7 by the end of this year, resulting in Solvay trading at an EV/EBITDA ratio of approximately 4.5.

For further details see:

Solvay Could Split Itself In 2, Plenty Of Upside Likely At Just 4.5x EBITDA