SVYSF - Solvay: There Will Be Dis-Synergies And More Leverage

2023-11-07 14:50:26 ET

Summary

- Solvay SA is planning to split its businesses into Solvay (commodity) and Syensqo (specialty), incurring upfront and perpetual costs and being a juncture where they will grow leverage.

- We think it's anti-economical and lacks value-add, as most European chemical companies already have a mix of specialty and basic chemicals businesses which are easily parsed.

- Solvay has a lot of electronics, automotive, and aerospace exposure, with the aerospace business uniquely showing growth due to the rebound in travel.

- There are cycle risks, but that goes for peers too who trade at higher multiples. Solvay has historically had this discount.

- While we aren't a special fan of the split, we like Solvay's assets and will look for which company comes out cheaper after split day to possibly place our bets.

Solvay SA ( SVYSF ) is planning to split its businesses, and it's going to be a done deal very soon. There isn't a great reason for it, and it will incur costs both up front and perpetual. It also serves to increase aggregate leverage. This business was not difficult to understand prior to this split. Almost all chemical businesses have commodity and specialty exposures, and it is easily handled by institutional equity researchers. This will not work magic. Solvay's issues have been that it's been in unlucky markets since the beginning of COVID-19. It's a high profile chemicals player in Europe and will get recognition when appropriate. The split is just anti-economical as far as we can tell. However, Solvay has always traded at a discount and we do like that. We don't think this split will change that, because as said, Solvay has been properly studied by equity researchers before, but the volatility could give us a moment to come into a business with maybe some extra timing-based margin of safety.

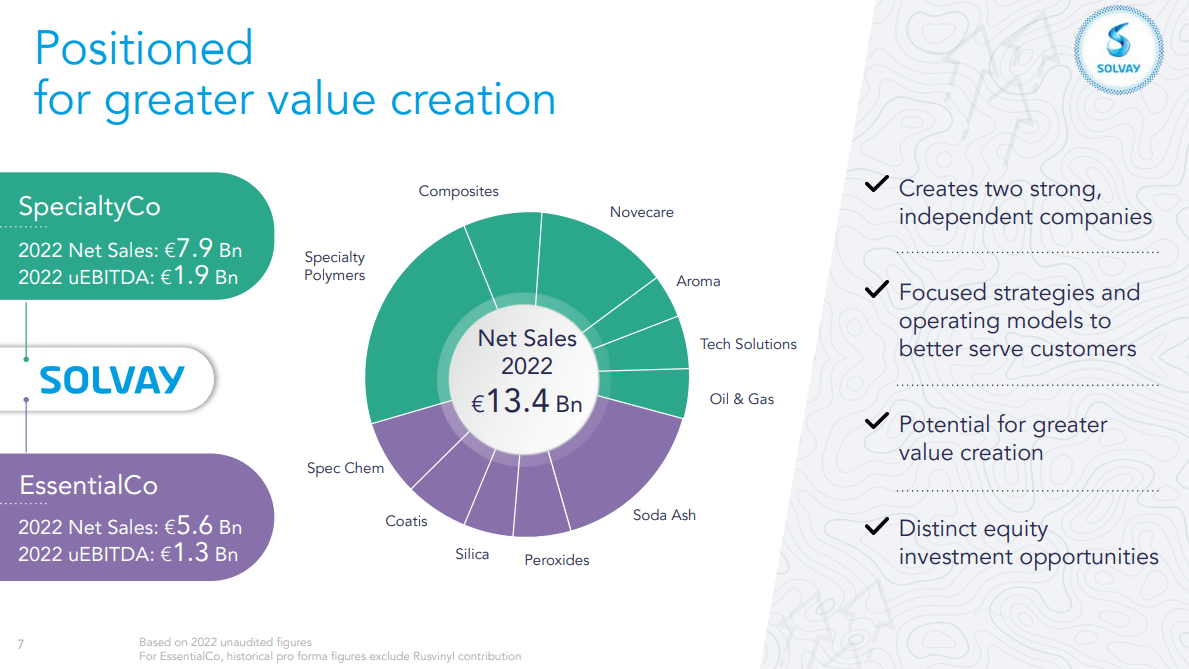

A bit on the split

It's worth discussing the split a little. Ultimately, it wants to create a more specialised company and a more commodity one .

{kind=link}

Division (Presentation on Split)

Aggregate debt is going to increase. They are going to lay more debt on the commodity company.

{kind=link}

Capital Structure (Q3 Pres)

There are going to be dis-synergies split more or less equally between the businesses, suggesting it is related to fixed backend costs. The total amount is going to be around 60 million EUR, around 2% of the current run-rate EBITDA figure. Not that insignificant. There are permanent losses in cash flows for the companies, and the only thing really to gain is to have two separate businesses so that investors can have more pureplay selections on the markets. Miller-Modigliani tells us that this is meaningless, which it is, since almost every single European chemicals companies has a mix of specialty and basic chemicals businesses. It's easy to follow, and institutional equity researchers already have a perfect mapping of how specialty each European chemicals company is and apply multiples accordingly. They also have a mapping of each company's respective end market exposure. Splitting truly has no value add, it's just action for the sake of action.

Solvay has a lot of electronics exposure, a lot of automotive exposure, and a lot of aerospace exposure. It is also a little over 50% specialty. Historically, it has traded at a pretty reasonable discount from peers with similar specialty levels. It trades at almost half the multiple of Akzo Nobel ( AKZOF ) which is smaller on electronics and agriculture but much higher on construction. Solvay has a nice business mix, and its aerospace exposure, some of the highest margin exposures it has, is at least growing thanks to a rebound in travel from the pandemic depression.

Recent Results

Everything else is being struck quite dramatically. While aerospace was up by 4.5% organically in sales , limited by supply chain issues from an even better showing, everything else is down. Soda ash is down on lower glass and construction demand, even batteries were down on destocking trends. Automotive was alright, but electronics, oil and gas, and consumer products were down thanks to a combination of lower commodity prices, destocking and general economic pressure.

{kind=link}

Highlights (Q3 PR)

Commodity exposures, things like mining separation, agro, electronics, building and construction, are all doing poorly. Only the aerospace business is doing fine. Volumes are the problem too, not just pricing. Marginality has actually been quite stable which is impressive, but volumes have hit utilisation profits quite hard.

Bottom Line

Solvay is always quite cheap. We actually like the company as a combined entity. It is more specialty than average in Europe and has always been an interesting value. In the last years, the direction has been troubled. Major issues firstly in the aerospace exposures, and now general commodity deflation and destocking plays poorly for them.

While we don't see the point of the split, we still think that Solvay is probably attractively valued on balance. As said, they trade at half the multiple of Akzo. That is a start to be attracted to an aggregate exposure of the companies.

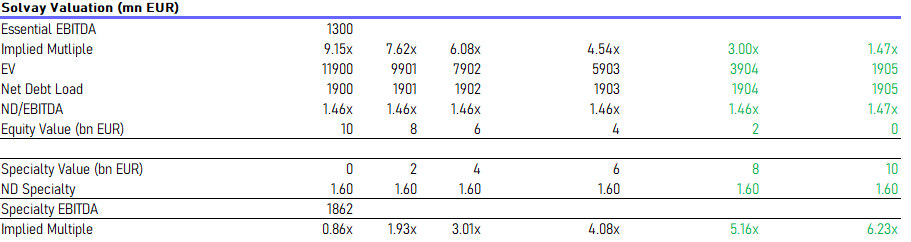

EssentialCo, or the commodity exposure, will be more indebted than the SpecialtyCo. We know that the combined market caps of the companies should be the same after the split, unless markets are shockingly inefficient, and therefore can plot a table of implied values.

{kind=link}

The green highlighted numbers are the ones that represent a post-split scenario where we would begin to be overweight the commodity exposure, whereas the black numbers are where post-split valuations would indicate that the specialty exposure is more efficient. The commodity exposure should be at lower implied multiples post-split than the specialty exposure by every logic. The constraint on this little thought experiment was that the aggregate market caps should be the same before and after the split, since we assume that it's not creating value.

In reality, both exposures are quite cheap in all the scenarios as the aggregate business is already at a relatively low multiple, but this chart will help us choose which to focus on.

The primary risks are that the aggregate business remain cyclically exposed. However, volatility around the split could present some interesting opportunities, so we will follow carefully on the first days of Solvay and Syensqo trading separately.

For further details see:

Solvay: There Will Be Dis-Synergies And More Leverage