NVS - SomaLogic: Revising Down To Hold On Earnings Asset Factors

2023-06-18 04:24:59 ET

Summary

- SomaLogic presents with a lack of fundamental, sentimental, and valuation factors to suggest a price change.

- I've revised my investment thesis to hold, due to the firm's Q1 results, revenue headwinds, and a market valuation of 0.8x book value.

- I am looking for $80mm in 2023 turnover, a decrease on the previous year.

Investment Summary

Following a sharp selloff in the equity stock of SomaLogic, Inc. ( SLGC ) I'm paring back my rating on the company to a hold until we obtain further clarifications. I had urged clients to buy the company at $3.56 back in February based on a number of catalytic factors. To name a few:

- Economics of the underlying proteomics market, forecast to grow at 13–16% compounding rate into 2030.

- The collaboration with Group 42 Healthcare to fulfil its proteomics demand, plus the contract extension with Novartis ( NVS ).

- Market generated data indicating buying support from large accounts, recent breakout on chart.

- Price target to $6–6.30.

Moving to the present day, investors have yet to pay a higher market price for the company. It has re-rated ~30% lower since the publication, and at this point risk management and capital preservation are more important than any speculative buy thesis. In that vein, I believe it is prudent to pare back my rating to hold on the stock, in order to observe coming developments from the sidelines. This will help view the market's expectations on SLGC at a higher view, to make more objective investment reasoning. Net-net, revise to hold.

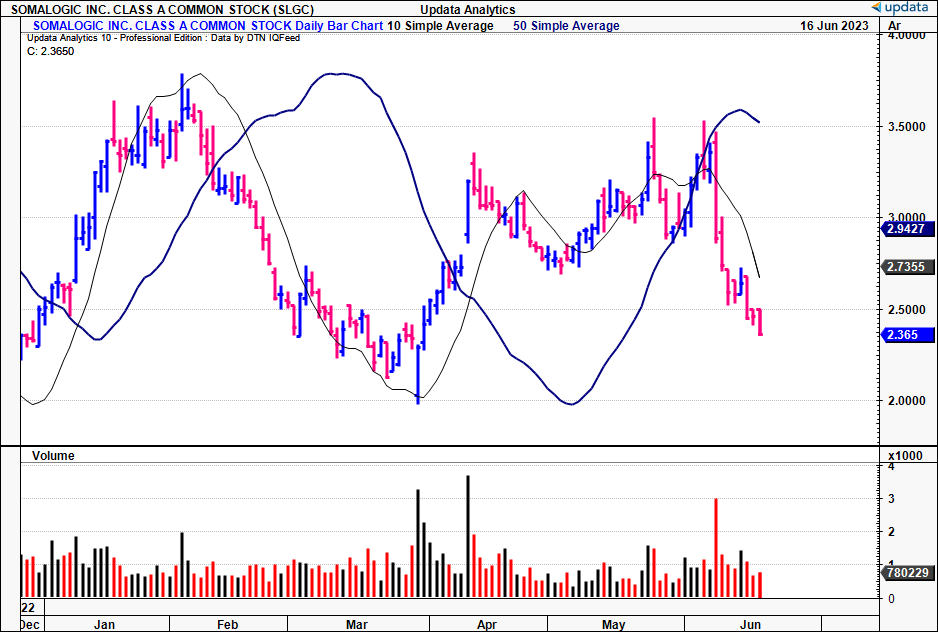

Figure 1.

{kind=link}

Critical Facts to Thesis Change

There are multiple factors, ranging from SLGC's latest numbers, to the market's positioning in the company that has changed the investment thesis. In first principles, there is a lack of fundamental, sentimental and valuation factors to suggest a price change. Last publication I spent a great deal of time. Covering the company's core offering, the potential differentiators, and the proteomics market outlook. In this analysis, I will hone in more on the company's financials and sentiment.

1. Sentiment revising lower

A change in market or investor sentiment is one of the 3 or so critical factors needed to drive a company's price higher. Add fundamental and valuation factors, and maybe systemic factors, to this. With SLGC findings show sentiment is quite weak at the moment. Why?

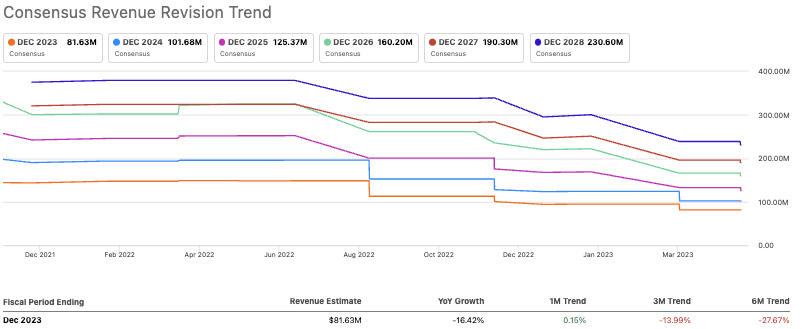

One, there have been 4 revisions to the downside from analysts over the last 3-months on SLGC's revenues. The consensus has $81mm in turnover for the company, increasing to $101mm in FY'24. Moreover, scaling back further, the down revisions have been in situ since August last year. If sell-side analysts are revising their targets lower, it is one clear source to say sentiment is also shifting lower on the sell side.

Figure 2.

{kind=link}

Two, options market activity demonstrates investor neutrality as well. Like analyst targets, options markets provide direct insight to sentiment by showing explicitly the aggregate positioning of those with actual money at risk. On August '23 contracts, the chain is stacked with puts at $2.50, suggesting investors are looking to provide a ceiling to which they can sell their SLGC stock at should it divert lower. This tells me the market does not expect further upside, otherwise it would be positioning for the same.

Third, momentum is down, with the stock trading below key moving averages across all time frames. This would tell me that key psychological levels, being the 10, 50, 100 and 200DMA's, aren't being met and instead price is pulling away from these levels. If price says anything about investor sentiment, the directional trend here is telling.

2. Q1 results analysis:

SLGC's pulled Q1 turnover of $20.4mm last month, an 11% YoY decrease, on adj. EBITDA of negative $36mm. It burnt $120mm in cash to achieve this result, and expects another $120mm going forward. This result was expected both internally and by the market, and so wasn't overly punished.

A key factor driving revenues is the company's primary offering, its proprietary SomaScan Assay. SLGC has designed it to detect and measure of protein biomarkers in a single sample of blood or other bodily fluid. The company says it can p rovide 7,000 highly reproducible measurements of circulating proteins in the test– the largest number reported for any proteomic assay. It all boils down to getting more assays out there, then pushing the cost down to do this.

On that tone, I would highlight the following points:

- Q1 gross margin came in 10 percentage points lower at 39.6%, compared to 49.3% last year. That's a notable snip to profitability. The margin haircut was put down to customer mix– mainly the assay services completed for the Human Technical Institute ("HTI") during the quarter. As a potential tailwind, SLGC expects gross to return to the historical c.50% range as customer mix shifts back in future quarters.

- Total OpEx was up 8% to $48.3mm, underlined higher by R&D investment, which increased slightly from $13.8 mm in '22 to $14.1 mm in Q1 FY'23. The operating loss was $39mm for the quarter.

- Additionally, it lost ~$1.3mm of leverage to at the SG&A line, with $34.2mm booked for the quarter. Management aim for FY'23 OpEx of $170 mm.

Despite the decline in revenue, if you exclude the $3mm NEB licensing revenue from the Q1 FY'22, growth was actually was 2% YoY. I'd also highlight the company's commitment to doubling the number of sites running its SomaScan assay in their own laboratory by year-end, demonstrating its long-term growth strategy. It had 8 sites in this capacity on the books by the end of Q1, with $2.55mm average quarterly revenue/site ($10.2mm annualized).

There are numerous investment implications that are gleaned from the company's latest results. I would categorize these as follows:

- Customer Expansion and Revenue Growth: The company has bold aspirations to double the number of sites using SomaScan in their own labs by yearend. In Q1 it clipped $2.55mm average revenue/site on 8 sites doing this as mentioned. If it were to maintain this cadence, you'd be looking at $40mm in FY'23 turnover on 16 labs, around 50% of the year's revenue forecast. I'd expect to see $3-$4mm per site as a bullish factor.

- Gross margin back to 50%: I also mentioned the plan to return gross margins back to the 50% plus range. This would be welcomed. To do this, it has priority on shifting its customer mix towards higher margin names. It will need to do this too– 40% gross isn't sustainable in my view, and presents a risk with the company's COGS at $110mm in the TTM.

- Expenditure reductions: To this point, management did make note of its efforts to cost management going forward. It projects cash burn of ~$120mm or less for the year, which would bring on-balance sheet cash to $318mm.

Collectively, these results are mixed in my view. There aren't sufficient growth levers to say the company will outpace consensus view points. Nor is there talk from management on the same, with projection of $80mm in turnover for FY'23, calling for a decrease of 17.5%.

Valuation and Conclusion

The market has priced SLGC at 0.8x book value, 62% discount to the sector. This is telling. If you're looking at an investment on asset factors and earnings power, well SLGC has no earnings, and the market values its net assets at a discount to their book value.

The question is whether there is reason to believe the market is wrong in its expectations. In my view, I don't believe it is. Consider the new points we've added to the thesis so far– decreasing sales, contracted gross margin, projected revenue downsides.

And so the main point is this: without the presence of additional fundamental or sentimental catalysts, it is difficult to see the market paying higher than this. Investors are selling at these prices too, and at the 0.8x multiple, it appears that no price is being paid to hold SLGC with a set of strong hands. This is supportive of a neutral view.

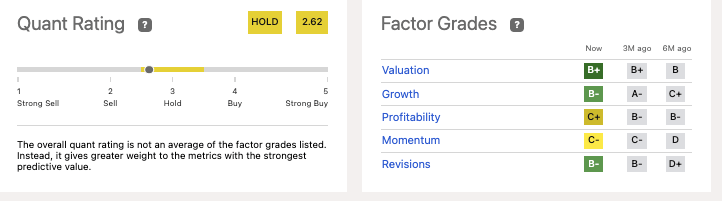

These findings are supported by objective data found by the quant system , as seen below. It finds the valuation discount attractive, but is turned off by momentum (sentiment) and profitability factors, in-line with my assumptions. I would say these data add a layer of confidence to the hold thesis.

Figure 3.

{kind=link}

Net-net, the updated data in SLGC's investment facts justify its re-rating to a hold in my view. There are unanswered questions on its gross margin, and revenue downsides in FY'23-'24 may compress these further. I cannot urge clients to buy such a deteriorating setup, not in the presence of such other golden opportunities elsewhere. In that vein, revise down to hold.

For further details see:

SomaLogic: Revising Down To Hold On Earnings, Asset Factors