SNDA - Sonida Senior Living: Debt Restructuring Yet To Drive Inflows Reiterate Hold

2023-08-10 18:40:55 ET

Summary

- U.S. senior living bankruptcies have increased during the pandemic, impacting Sonida Senior Living's equity stock.

- The company's debt restructuring is indeed noted, but uncertainty remains about its ability to turn around operations.

- Market returns haven't responded to news of the debt restructuring announcement.

- Net-net, reiterate hold.

Investment Briefing

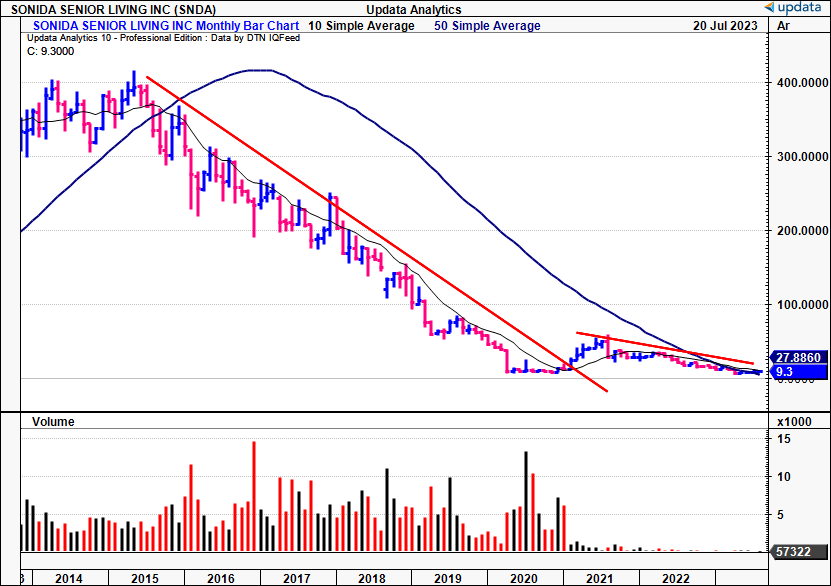

Readers will know that I have been fairly neutral on the investment outlook of Sonida Senior Living, Inc. (NYSE: SNDA ) since midway last year. The company's issues had begun well before this, however. You can see in Figure 1 month-on-month returns in SNDA's equity stock from 2014 to the time of writing. Imagine watching your equity being wiped out just about every month for the past 9 years straight. Completely uninspiring, and we can thank a whole tide of macroeconomic and idiosyncratic crosscurrents for this. I discussed plenty of these in my last SNDA analysis:

- U.S. senior living bankruptcies increased markedly during the pandemic. The interest-rate-sensitive sector pushed through more bankruptcies in 2021—'22 than the 5-years prior combined. This trend has continued into FY'23.

- Staffing costs for managed living and medical facilities is ~60% of the sector's OpEx. Reimbursement rates are increasing, for sure. But, they are stretching at a slower pace compared to wages.

- As mentioned, "it has been a profitless race to the bottom" in terms of operating margins. At the time of the last publications, ~90% of all U.S. nursing homes were at 3% operating margins, based on data from GrantThornton.

Shifting forward to the present and the major update to cover is the company's debt restructuring. This was absolutely critical for SNDA's survival as a going concern. There is now a more than exciting investment debate on our hands. On the one hand, SNDA still has a mountain to climb in order to attract sophisticated capital to its market value. There's no less pressure on capital markets from the inflation/rates axis, in addition to currency fluctuations. However—as our special situations/distressed investors will know—debt restructuring and the subsequent clarity can be lucrative. It all depends on how SNDA can rally the troops from here, and demonstrate to the market that, yes, capital is in fact valuable in its hands.

Keynes was believed to have said, "when the facts change, I change my mind", and the overarching question we now have is whether the investment facts for SNDA have changed enough for the market to change its mind on the company.

Moreover, to invest successfully, you need to think in terms of combinations and permutations. What is likely to happen, and how likely is it to happen? In that regard, the risk profile is still too great for my investment cortex to wrap itself around for SNDA. Uncertainty remains on the company's ability to turn around its physical operations, producing the required cash flow to see its market valuation rate higher over time. Plus the debt restructuring, in a way, simply kicks the can down the road.

In that vein, whilst there is potential on the speculative and special situations front, the element of uncertainty on probabilities is too high at the moment. Thus, I am compelled to maintain a hold rating on the company— for now. There is much to discuss and think about in that regard. Net-net, reiterate hold.

Figure 1. SNDA month-on-month equity performance, 2014—date

- Tight monthly closes for last 2 years, unable to catch a bid with each step lower.

- Volume basically dried up entirely compared to 2014—2020 range. No evidence of volume buying or selling, supporting neutral view.

- Prices compressed after enormous run-down from $400/hare to ~$10/share at the time of writing.

- Question is—is debt restructuring enough of a catalyst to reverse this picture?

{kind=link}

Data: Updata

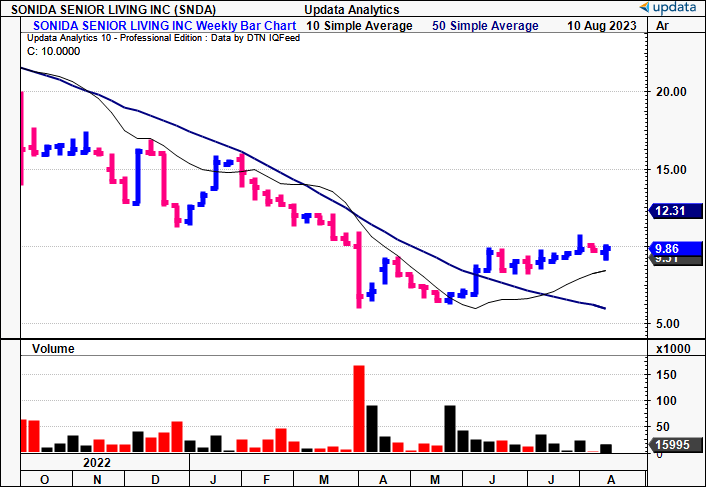

Figure 2. SNDA Equity performance this YTD.

{kind=link}

Data: Updata

SNDA Forges Financial Flexibility

As mentioned, the critical change to SNDA's investment outlook is in the form of its debt restructuring, announced on 29th June. In January this year, it had already completed the asset transfer of 18 total communities to Fannie Mae. This wiped $36.3mm in debt from the balance sheet.

1. Forbearance agreement and debt restructuring

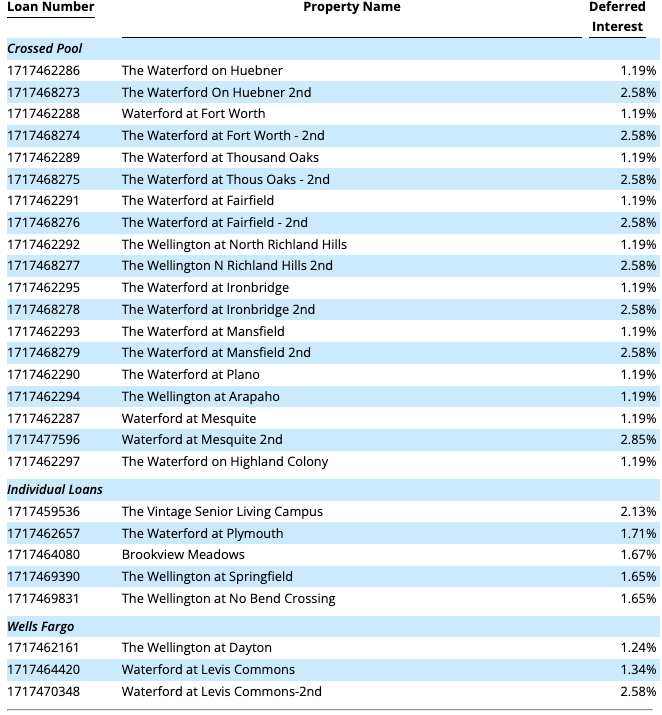

The firm then signed a comprehensive forbearance agreement with Fannie Mae in June. This marked the first of a 2-step process to completely restructure its debt obligations with the agency. Once completed, both actions will modify all SNDA's mortgage agreements with Fannie Mae. You can expect this to be completed by the end of Q3 2023, should all go according to plan. The company's schedule of deferred interest after the full restructuring is observed in Figure 3.

Figure 3. Schedule of deferred interest with respective properties

{kind=link}

Data: SNDA Forbearance agreement, retrieved from JUSTIA

This is no doubt a strategic move. Critically, the new-term sheet is expected to ensure the flexibility SNDA needs for operational growth and continue as a going concern. Without it, there was no certainty on either of those two factors in my opinion.

Under the terms of the Fannie forbearance agreement—starting from the June FY'23 payments—SNDA will make reduced debt service payments going forward. Also as part of the agreement, SNDA made a $5mm upfront payment, that was credited against the existing loan balances.

The subsequent loan modification will encompass the following points:

- All obligations—including all 12 loans due July FY'24—have extended maturities to December 2026, or beyond.

- The agreement also defers or waives all contractually required principal payments under the 37 Fannie Mae loans for 3 years, or until maturity. This move will produce $33mm of cash savings for SNDA until the tenor.

- Finally, SNDA is entitled to near-term interest rate reductions on all 37 assets under the agreement, resulting in a further $6.1mm in cash interest savings over the next 12 months.

SNDA expects to finalize the loan modification by September 30 this year. As part of the loan modification, SNDA will make a second $5mm payment on June 1st FY'24. This too will be credited against the consolidated loan balances.

Finally, under SNDA's agreement with Ally Bank, the covenants and the minimum liquidity requirement under its $88.1mm facility have been modified. This will be in situ for the next 15 months (now that we are ~3 months past the agreement date).

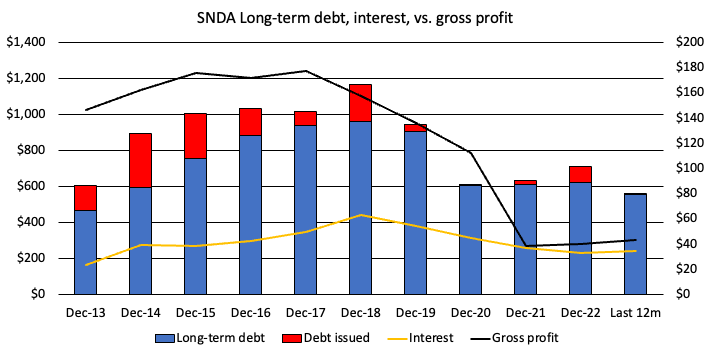

Figure 4. Note the rapid fall off in gross profitability from 2019. This started in 2017 on closer inspection. The issue being, debt servicing and interest expenses did not fall with this.

{kind=link}

Note: Interest payments calculated on long-term debt only. Debt issued is calculated as long-term debt only. (Data: Author, SNDA 10-K's)

I would also point out that SNDA has ~$41mm in series A preferred stock, paying an 11% annual dividend on this amount. This is accrued in arrears and cumulative, thankfully, at the discretion of the board.

2. Additional factors to bolster balance sheet

In a further bid to shore up its financial position, SNDA also secured a $13.5mm equity commitment from Conversant Capital —its largest shareholder. The shareholder has agreed to pay up to this amount, and will pay $10/share to do so— the current market price as I write. This commitment will be at the company's sole discretion to utilize, in part or in full, over the next 18 months.

SNDA retains the right to utilize Conversant's equity commitment, drawing on it in whole or in part. The company intends to draw $6mm in July, coinciding with the first $5.0mm principal payment to Fannie Mae. The remaining funds will be available to support general working capital needs or to fund the second $5mm loan paydown to Fannie Mae.

The question is whether this will have an impact on the SNDA share price. Note, the $10 is at the current market value. Hence, placing a number of orders at $10 on the price ladder has likely pushed it to that level in my view.

3. Breakdown of recent numbers

As a quick reminder, SNDA is due to present its Q2 FY'23 numbers mist likely at the end of this month. It did release Q1 earnings in May.

Occupancy and revenue per occupied room ("RevPOR") are the key metrics to scrutinize for SNDA. Thankfully for investors, there's been statistical improvements to both in FY'23. Average occupancy for the company's owned assets came to 84% in Q1, and management views this number as stretching up across 2023. Q1 revenues were also up 6% to $56.6mm for the quarter, bringing gains of ~750bps to net operating income ("NOI"). Management also project a 10% revenue run rate moving forward, on occupancy of 85%.

In addition, SNDA also clipped a 9.1% increase in overall rates, leading RevPOR 5.6% higher vs. Q1 last year. This is comprised of 1,500 leases, and the RevPOR was also up ~6% from Q4 FY'22. Thus, it is building momentum around its occupancy numbers.

Finally, the company printed $3mm in operating cash flow in Q1, a meaningful step of $4mm on the previous year. Critically, combined with the debt restructuring, if SNDA were to keep this pace of cash generation moving forward, it would be cash flow positive " for the first time in the company's recent history".

4. Leadership changes

In addition to the recent developments, SNDA announced several new executive hires and internal promotions. Some were made in June, some at the end of FY'22. The appointments are as follows:

- Carole Burnell, Dawn Mount, and Donna Brown have been appointed Vice Presidents of Operations, each responsible for overseeing one of the company's 3 geographic domains.

- SNDA welcomed Reanae Clark as Vice President of Business Development and Acquisitions. Clark will lead the company's revitalized growth initiatives across all markets in this role. She brings over 15 years of experience in the senior housing sector, with demonstrable experience on the investor side, and on the dealmaking side as an investment banker. She was recently part of the Orix Municipal & Infrastructure senior housing credit portfolio at Orix Corporation USA.

- Michael Karicher was appointed "Chief People Officer". He was formerly the executive president of HR at Remington Hotels/Ashford Hospitality.

- Finally, Jay Reed—formerly SNDA's VP of IT —has been promoted to Chief Technology Officer.

We now have a clear set of metrics to benchmark these new appointments against. The new executives certainly have more than an anthill to climb moving forward—it's more like Mt Everest.

Still, should this trek about the mountain be successful, then it places SNDA in a potentially attractive position to harvest rapid, and potentially steep equity gains.

Further considerations

As I write, you've got SNDA at $10.00/share, trading at just 0.3x forward sales , and 51x cash flows. Despite the enormous destruction in value described earlier, there are a couple of points to consider:

- The stock looks to have potentially found a bottom, finally. It has curled up off 52-week lows of $6 neat in May, and trades 66% higher off this mark.

- With this latest thrust, we now have potential upside targets to $12.50 on the point and figure studies below [Figure 5]. These are great in times of fundamental uncertainty as they show what the market is doing and removes the intra-trend volatilities. Hence, a break higher could get us to $12.50—a figure I am looking too with more seriousness. But we also have a downside target to $7, and the same logic applies.

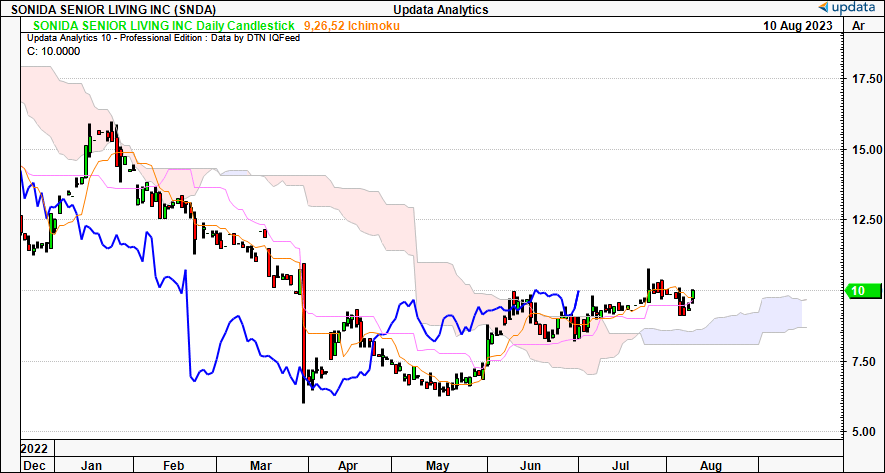

- In Figure 3, the daily cloud chart, you see the stock is trading above the cloud with the lagging line in situ. This powerful indicator suggests a trend may have gone from either bearish or neutral, to bullish. The break of the lagging line above the cloud (it is shown via the blue line) may or may not be a bullish point in my opinion. For example, a move higher (or lower) could be of potential significance because:

- It could activate the technically derived target of $12.50 (or $7 on the downside).

- Suggest the short-term trend is bullish (or bearish). With the daily chart, you are looking out to the coming weeks of trade.

- Thus, could throw off more near-term upside (or downside) targets.

As you can see, there are lots of "could's" in those assumptions. Hence, the way you'd play SNDA is more on the speculative side, looking for capital inflows after the debt restructuring takes full place, and attracting the special situations crowd who are looking for a sharp turnaround.

That does not align with my own investment tenets. I am searching for long-term cash compounders, where capital is more valuable in their hands than mine. I do appreciate the potential for event-driven gains (being a medtech and biotech investor, a bulk of the sector's stock returns are driven by just this). But there's an added element of execution risk that doesn't relate to things like pipelines, clinical assets, or study results. Instead, it is mostly operational, and macro-related. So to trade SNDA you'd need to think a shorter time frame and a potential selling point at much shorter duration than I prefer.

Remember, the job is to compound, or at least protect capital—not put it at risk on the downside. Hence, in my view, no matter all of the many 1000's of ways to skin a cat, as they say, I'd need more flesh to put on the skeleton of SNDA's investment case to rate it a buy right now. In that regard, SNDA is not currently investment grade in my opinion.

Figure 5.

Data: Updata

Figure 6.

{kind=link}

Data: Updata

Discussion

Events like debt restructuring and corporate turnarounds are ripe takings for those within the special situations crowd. I'm not so sure that accurately applies for SNDA just yet, though. Its negotiations with creditors have proven fruitful, extending terms and covenants for the company until 2026 and beyond. That is great. But the point is, it still needs to grow operations and produce more operating cash flows to service its obligations. Otherwise, we're at the same spot in 3-4 years' time.

SNDA thus needs to really prove itself from here. It must completely blow it out of the park in earnings and business growth. The new executives need to prove their weight in gold and deliver on the results. Most importantly, sentiment needs to improve in its equity stock to trade higher. Forget that happening without rigid evidence of the former two points.

Thus, the execution risk is still high at this point in my opinion. You could play SNDA on the special sits. front, and look for more near-term equity gains with risk management principles and risk controls in place. You'd be playing a more speculative game on this in my view, however. That doesn't align with my own investment tenets. Hence, I am reiterating SNDA as a hold for now, but I am watching very closely the company and its stock's next moves.

For further details see:

Sonida Senior Living: Debt Restructuring Yet To Drive Inflows, Reiterate Hold