SHC - Sotera Health: A Great Business At A Discount

2023-10-12 12:32:18 ET

Summary

- Sotera Health stock has declined 22% in the past six months due to concerns over guidance, rising interest expense, and fears about slower medical device sales.

- However, these concerns are overblown as Sotera's Sterigenics sterilization business continues to show strong growth and profitability.

- Sotera benefits from overall growth in the medical device and pharmaceutical industry and is not overly exposed to any particular category.

- Sotera has a very strong competitive moat and is attractively valued at just 13.5x 2025e EPS, a large discount to its main competitor.

While Sotera Health ( SHC ) stock surged earlier this year following the settlement of its ethylene oxide claims , shares have retraced some of these gains, having declined 22% over the past six months. Recent weakness appears to reflect:

- Concerns over a modest cut in full year guidance

- Rising interest expense (due to both rising rates and a higher debt burden following settlement payout)

- Fears over slower medical device sales due to increased use of diabetes drug treatment/weight loss medicines like Ozempic.

I see these concerns as overblown - while Sotera did cut guidance when it released 2Q23 results, its Sterigenics sterilization business continues to produce strong growth and profitability. Meanwhile, debt pay down coupled with EBITDA growth will allow Sotera to de-lever to 3x net debt to EBITDA (from current level of 4.2x) by 2025/26. Lastly, Sotera benefits from overall growth in medical device/pharma units and is not overly exposed to any particular medical device or category.

I believe Sotera shares have been unduly punished given the company's leading market position in a non-cyclical industry, prospects for outsized profit growth, and ability to de-lever in the medium term.

At $13.50, Sotera shares trade at just 13.5x 2025e EPS, an attractive absolute valuation and a meaningful discount to its closest competitor Steris ( STE ). Looking out a couple of years, I see 50-70% upside in Sotera shares and have been aggressively adding to my position on recent weakness.

Why I believe Sotera is a Great Business

{kind=link}

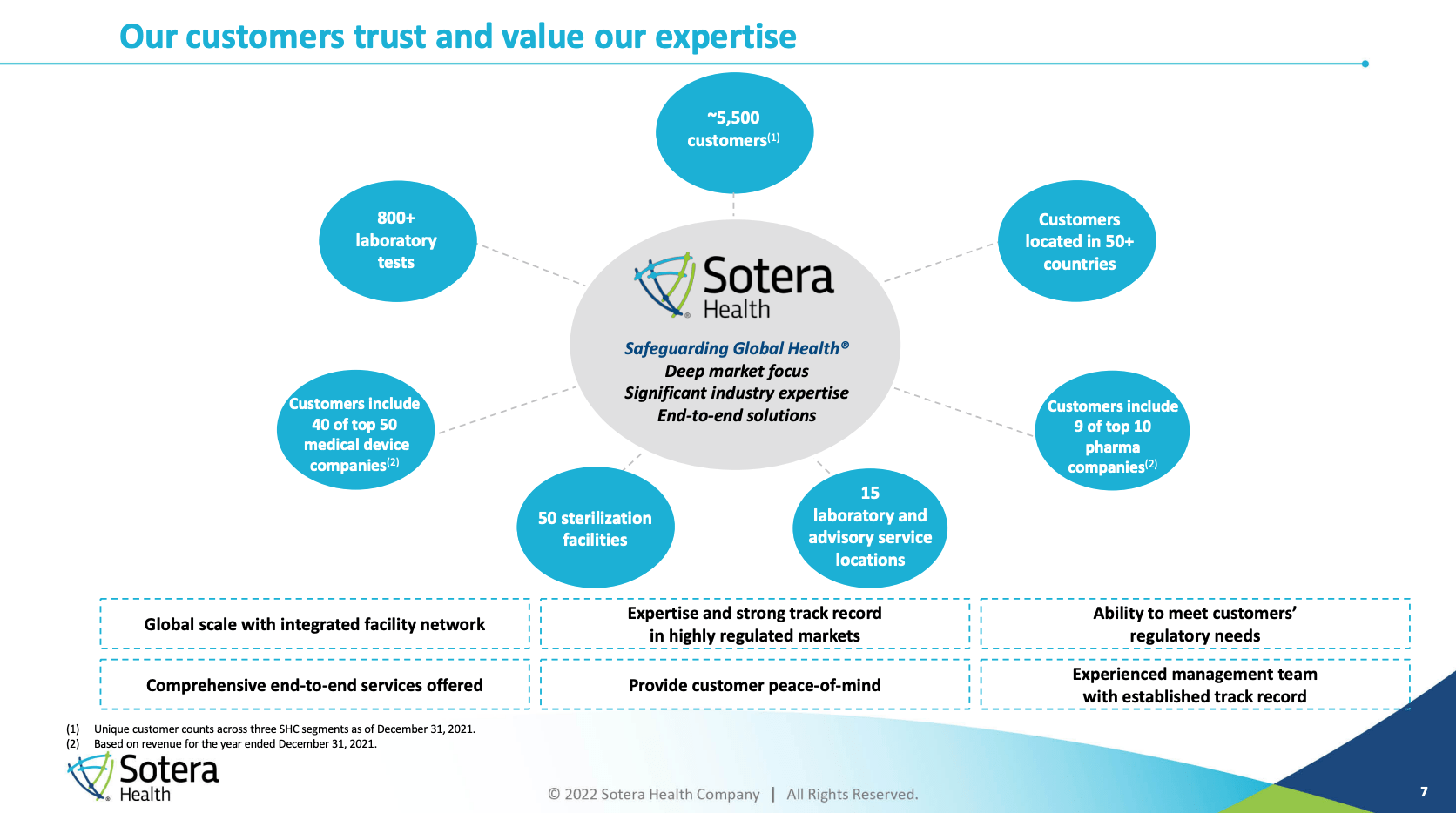

Sotera's Sterigenics business (67% of group EBITDA) is an outsourced provider of sterilization to medical device/pharmaceutical customers. The company counts 40 of the top 50 medical device companies and nine of the largest pharma companies as customers. I believe Sterigenics is an exceptional business:

- Favorable industry structure -Sterigenics is essentially a duopoly (combined 80% market share) with Steris Plc. This leads to rational competition and favorable pricing trends.

- Significant barriers to entry - Sotera provides sterilization services under multi-year contracts to nearly all of the leading medical device and pharma companies and has gained their trust over multiple decades. Not only does this provide revenue visibility but it also serves as a deterrent to potential competitors who would have to spend hundreds of millions of dollars to build a facility with no guarantee of customers/revenue. In addition, prospective competitors would need to prove efficacy and safety to both regulators and customers. Lastly, 80% of customers use more than one of Sterigenics 50 sterilization facilities (ensures consistency, compliance, and reduces complexity) which would cost billions to replicate. Given the long-term contracts and dominant market position of Sterigenics/Steris, any new entrant would likely have low facility utilization (whereas Sterigenics facilities essentially run 24/7 which helps to explain the segment's ~50% EBITDA margins).

- Sterilization is a mission critical, government mandated procedure that represents a small percentage of overall medical product/device costs. It has stable and growing demand.

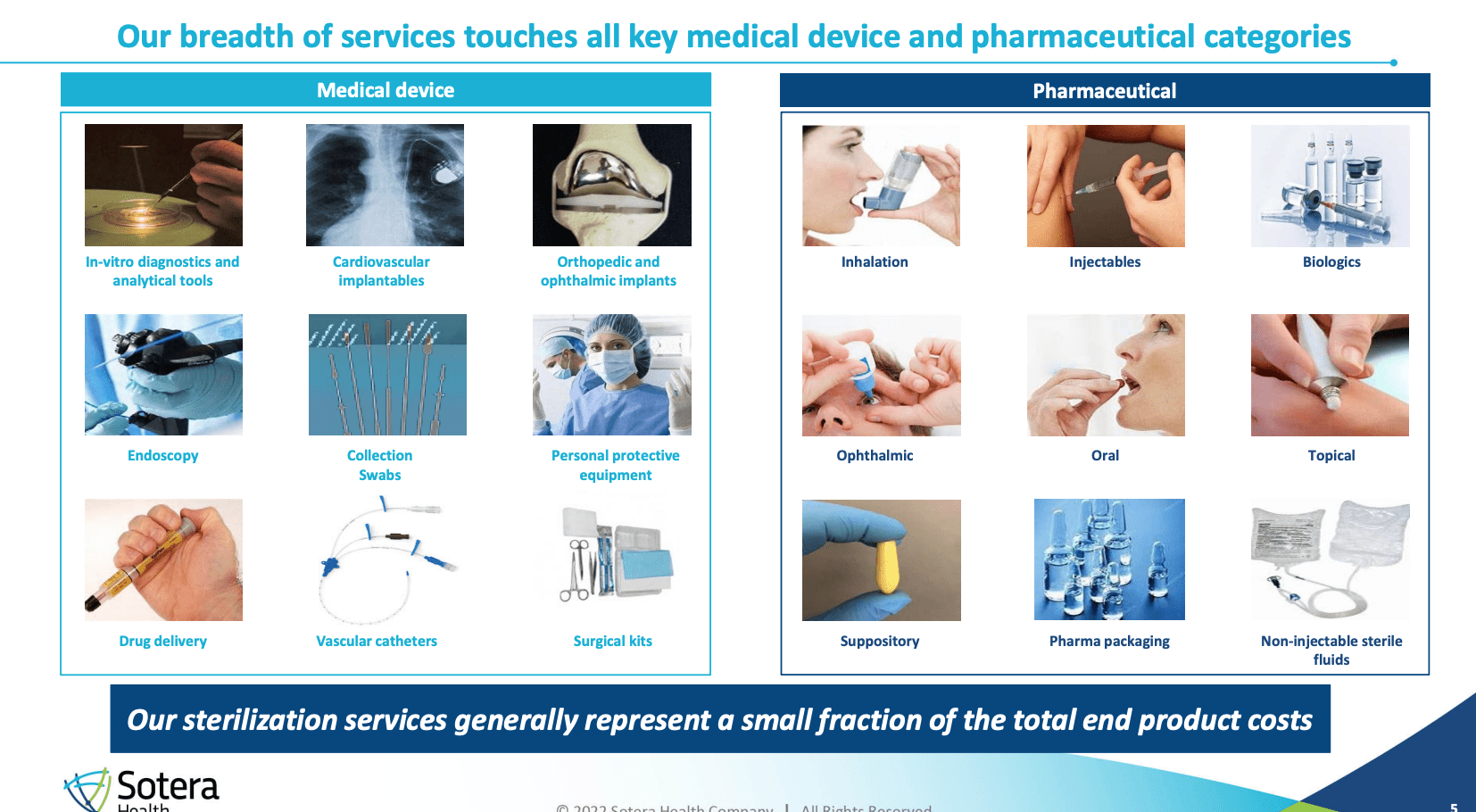

- Not dependent on any particular medical product/procedure/category. As shown below, Sterigenics sterilizes nearly every type of medical implant, device, kit, piece of equipment/gear, or pharmaceutical. Medical device makers are faced with risks associated with competition from new medical technologies and face the ongoing threat of reimbursement cuts from insurance carriers or Medicare/Medicaid. In contrast, Sterigenics sterilizes thousands of different products/devices and does not have outsized exposure to any particular category which insulates it from technological and reimbursement shifts.

{kind=link}

Sotera's Nordion segment (15% of EBITDA) is closely linked to the sterilization business. Nordion provides Cobalt-60 necessary for gamma sterilization. This is a highly defensible business operating under long term (multi-decade) contracts to extract and deliver material from nuclear reactors (heavily regulated). While the business is seasonally lumpy, it is competitively insulated (contracts, regulation) and exhibits strong long-term growth.

Nelson Labs (15-20% of EBITDA) is a provider of safety-related tests in microbiology and analytical chemistry to medical device/pharma companies, serving nearly 4,000 customers. Demand benefits from underlying growth in medical devices/pharma and increased regulatory complexity.

Valuation

Looking out to 2025, I expect Sotera to grow EBITDA 8% per year on the back of 5-6% annual revenue growth. Revenue growth is driven by:

Price- given the duopolistic industry structure and mission critical product nature, and relatively small percentage of total product cost to customers, Sotera has the ability to price ahead of overall inflation. I expect price increases of 3-5% annually.

Market unit growth- overall units should grow 2-3% annually benefitting from medical device/pharma growth driven by an aging population and continued medical advances.

Increased outsourcing -while most medical device/pharma companies use outsourced providers Sterigenics/Steris, some still operate in-house (which tends to be inefficient owing to lower facility utilization) and there is ongoing structural growth in outsourcing which should add 1% or so to annual growth.

All-in, this gets me to 6-9% revenue growth. Implicitly, I am assuming the low end (6%) of the range for revenue. Sterigenics (the bulk of the business) is largely a fixed cost business so I expect EBITDA growth to outpace revenue which conservatively gets me to 8% EBITDA growth.

Deducting depreciation, interest expense and taxes, I arrive at $1 per share in 2025 EPS. Given the exceptional quality of the business, I think Sotera should trade at a 20-23x EPS multiple, implying a 2025 fair value of $20-$23 per share, which implies 48-70% upside. It is worth noting that competitor Steris currently trades at 25x forward earnings suggesting my Sotera price target is achievable.

Conclusion

I believe Sotera is a fantastic business which is being unduly penalized by the market. Looking out a couple years, I see 50-70% upside in Sotera shares and have been aggressively adding to my position on recent weakness.

For further details see:

Sotera Health: A Great Business At A Discount