SHC - Sotera Health: Pricing Power Leading To Margin Expansion And Growth (Rating Upgrade)

2023-11-13 06:44:58 ET

Summary

- Sotera Health has shown strong revenue growth and margin expansion in Q3, driven by favorable pricing changes.

- SHC is investing profits back into the business and plans to increase investment for the next year to sustain growth.

- Despite challenging market conditions, management is confident in SHC's ability to continue growing.

Investment action

I recommended a hold rating for Sotera Health Company ( SHC ) when I wrote about it the last time , as I believed it to be fairly valued. The conditions for it to be rerated positively are for them to report better results that show a recovery in their business. Based on my current outlook and analysis of SHC, I am revising it to a buy rating. In the third quarter, SHC proved that its business has indeed recovered by posting revenue growth. On top of that, margins are expanding. Despite inflation challenges, SHC was able to pass costs down and drive its top line to grow. With management guiding FY23 revenue to grow, their confidence further bolstered my view on SHC.

Review

In November 2023, SHC reported robust third quarter results . The company reported consolidated revenues of $263 million, which represents 5.8% growth on a year-on-year basis. In addition, the adjusted EBITDA reported was $134 million, which grew by 7.3% year-on-year. Its adjusted EBITDA margins grew by 0.7% to 51% vs. the same period last year of 50.3%. On a 9 month basis, it stands at approximately 49%, which is extremely impressive in my opinion as it is able to earn up to half of its revenue as EBITDA.

Favorable pricing changes of 6.3% and favorable foreign exchange rate changes of 2.2% were the main drivers of the revenue growth reported in the third quarter. Moving down its consolidated revenue to segment levels, segment income increased 8.9% year-on-year to $93 million, and segment income margins increased by approximately 1.1% to 55.3%. The revenue growth and margin expansion were also driven by favorable pricing.

In order to fuel future growth, there are a few ongoing developments SHC is undertaking. Firstly, during the quarter, SHC completed a facility expansion project, with the customer product validation phase currently underway. Secondly, it is making enhancements to its ethylene oxide facilities in the U.S., which aim at ensuring best-in-class emission controls. In addition to these, management also anticipates that 2024 will see even more increased investment. I believe these investments serve as a catalyst for SHC’s future growth. In order to sustain and expand SHC over the long term, continuous investments have to be made in order to capture more market share. As of the third quarter, its revenue is growing robustly, and margins are expanding healthily to approximately 51% on an adjusted EBITDA basis. With such strong profit generation, it is wiser to reinvest this profit back into the business to grow it rather than letting it idle. In addition, I believe right now is the perfect opportunity to capture and seize the growth SHC is enjoying while it is still hot.

With these tailwinds in mind, I would like to discuss SHC’s outlook. Currently, the ongoing uncertainty with inflation has created headwinds for the general economy, and SHC is no exception. I expect these macro challenges to exert a little pressure on SHC’s revenue. My view is in line with management’s view as well. For FY23, SHC expects revenue to be between $1.035 and $1.055 billion, or a growth rate of roughly 3% to 5%. In terms of adjusted EBITDA, it is expected to be between $520 and $535 million, or a margin of approximately 51% based on the higher range of the estimates. This means that SHC is not expecting margins to be compressed by inflation, which suggests its strong pricing power. Overall, despite the economic challenges, SHC is growing its business strongly and continues to improve its margin. In addition, management is also confident that SHC will continue to grow in the future, further bolstering my confidence in them as well.

Valuation

I believe SHC can grow in the mid to high single digits for the following two years because of the following factors. Firstly, SHC showcased robust growth in the third quarter, with both revenue and adjusted EBITDA growing healthily. In my opinion, its ability to grow these despite the uncertain and challenging market conditions shows SHC’s business robustness. The growth was mainly driven by favorable pricing changes. With high inflation, this shows that SHC has power pricing and the ability to pass costs down, which allows them to expand their margins.

In addition to these, SHC’s is constantly improving and expanding its business using the profits they have generated. Management’s anticipation of more investment spending for the next year further bolsters my view that SHC will be able to maintain long-term growth. Despite the tough market conditions, management still anticipates mid single digit growth for FY23, and margins are expected to be retained.

{kind=link}

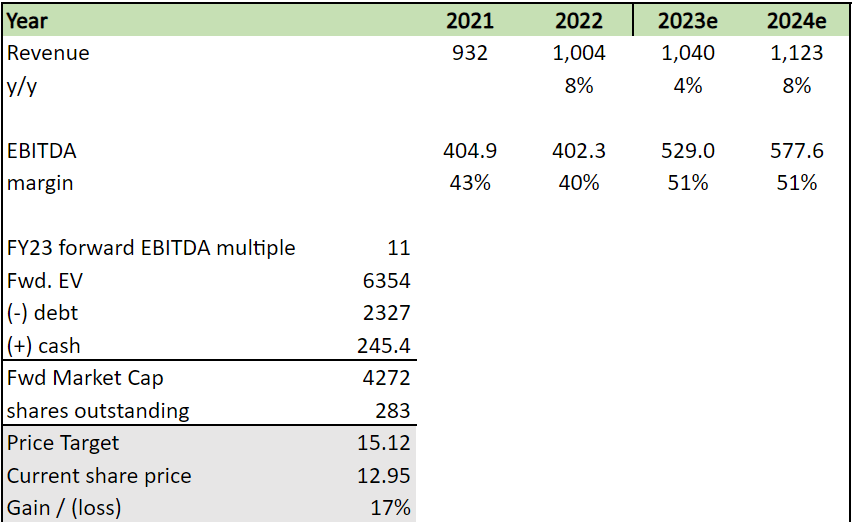

SHC is currently trading at ~11x forward EV/EBITDA. Its peers are trading at a median of 13.7x. Given that SHC’s approximately 45% TTM EBITDA margin is higher than peers median of negative 15% and in line 2024 growth outlook of 8%, SHC is outperforming its peers. Even at 11x forward EV/EBITDA, the implied gain is 17%. If SHC’s margins were to inch closer to peers' medians, I would see even higher percentage gains. On the back of these, I revise my rating to a buy for SHC.

Author's work

Risk and final thoughts

Risk to my buy rating stems from SHC's capital investment to expand its business. While these investments’ intention is to drive future growth, they also represent substantial capital commitments. There is a risk that the ROI on these investments might not be enough for investors, as the current high interest rate environment has significantly increased investors’ ROI demand. If these investments are diminishing the equity holder’s return, SHC will experience a contraction in its valuation.

In summary, SHC’s third quarter results have shown robust revenue growth and margin expansion despite a challenging market condition characterized by high inflation. In fact, inflation has been the driving force behind its growth, and this demonstrates its pricing power over consumers. In order to sustain growth, SHC is investing profits back into the business, with plans to increase investment for the next year. While the macro landscape is challenging, management is still guiding full year revenue growth, which shows their confidence in the business. With these, I revise my previous hold rating to a buy for SHC.

For further details see:

Sotera Health: Pricing Power Leading To Margin Expansion And Growth (Rating Upgrade)