SO - Southern Company: A Solid Company With Bright Future But Overvalued

2023-05-23 02:33:01 ET

Summary

- Southern Company is forward-thinking and adaptive; it has grown revenue by 71.35% since 2013.

- They expect to experience a $700M improvement in operating cash flow once both units 3 and 4 of Plant Vogtle are online.

- With their fairly low annual returns, I view their forward P/E of 19.68x, forward PEG of 3.39x, and a forward EV/EBIT of 23.01x, as showing the company as overvalued.

- Because of recent price improvement, the company is now too far above fair value to recommend buying.

- I currently rate Southern Company a Hold.

Thesis

With the inflation reduction act providing long-term tailwinds for utilities, I believe the next couple of years represent an excellent time to become a long term investor. I have been searching for the ones with the most appealing financials.

I went into more detail about their forward thinking attitude in my last article, but I believe the moves Southern Company ( SO ) is making now is setting them up for long-term success. I have come to the conclusion that if shares can be purchased for a good price, they should be. Unfortunately, recent price appreciation has taken the valuation up above the point where I view SO stock as an attractive buy. I currently rate Southern Company a Hold.

Company Background

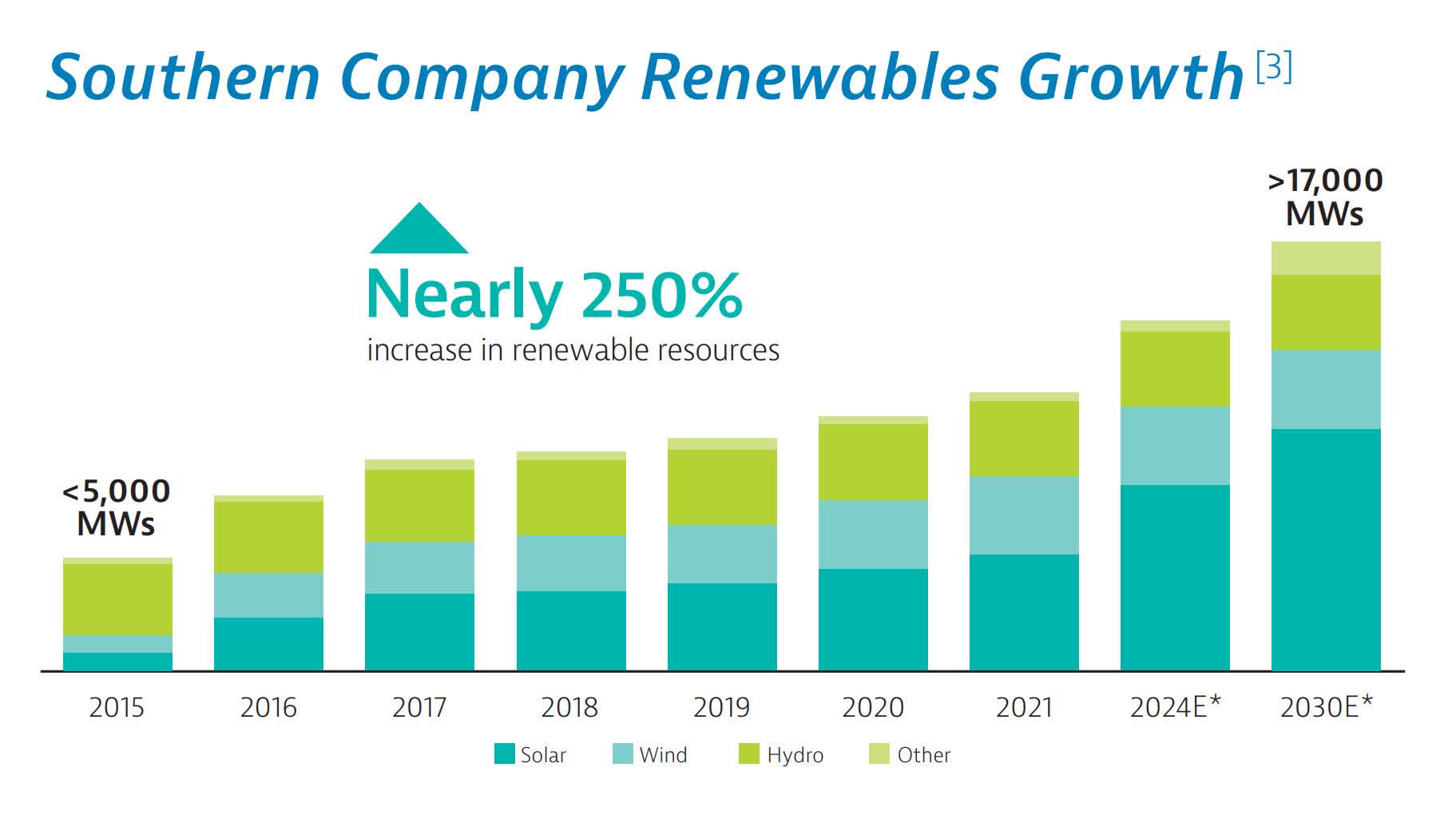

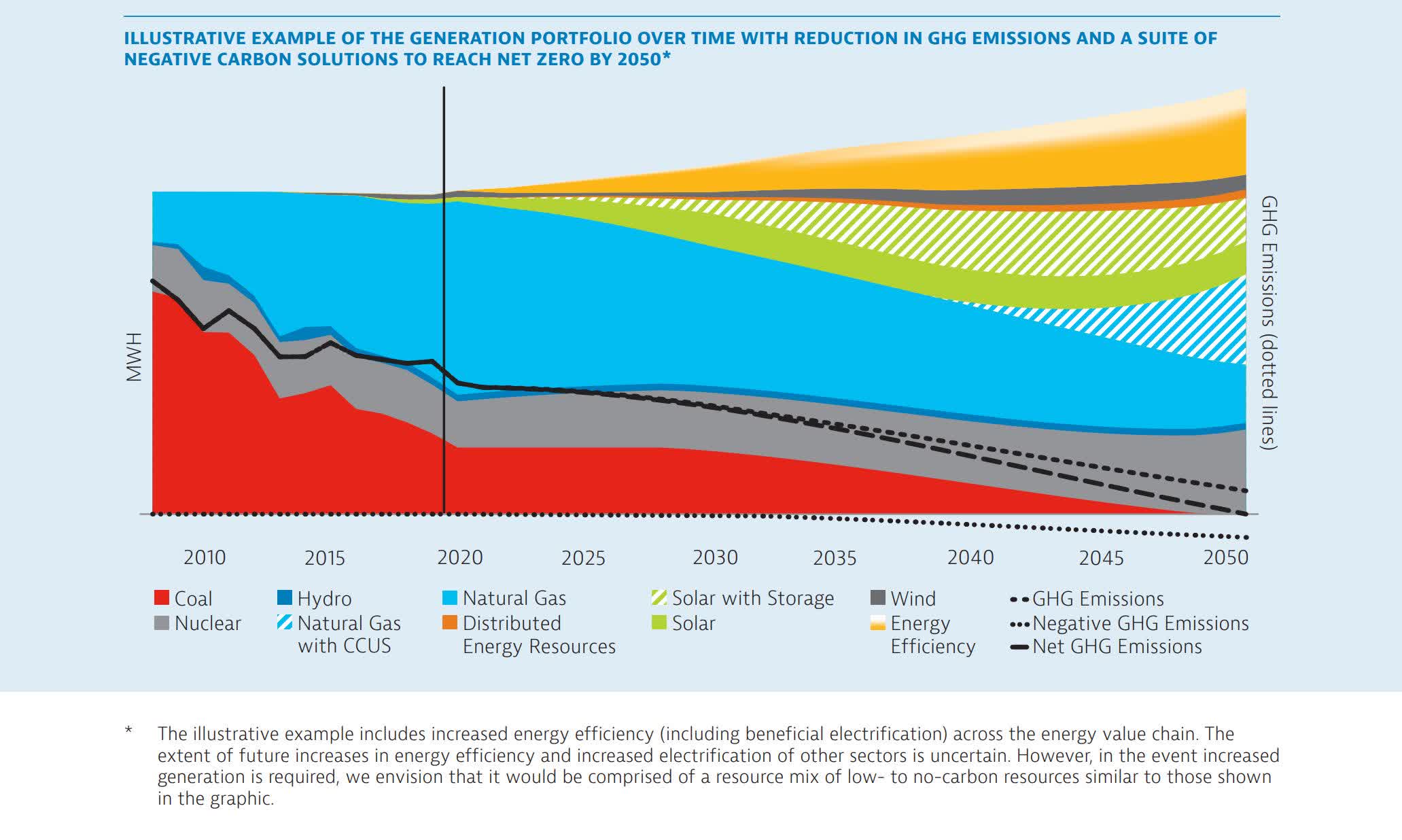

Southern Company is a gas and electric utility holding company based in the southern United States . Southern Company provides electricity and natural gas to over 9 million consumers. They include wind, solar, and nuclear in their portfolio and are on track to achieve their goal of reducing their greenhouse gas emission to 50% of 2007 levels by 2030. They plan to be net zero by 2050.

2022 Year In Review (Southern Company) 2020 Implementation and Action Toward Net Zero (Southern Company)

{kind=link}

{kind=link}

Southern Company has a culture of innovation. They joined GE in a joint project developing carbon capture technology. They are also developing a molten chloride reactor . They initiated a program to lower waste and losses from natural gas leaks. The company has earned high marks for environmental transparency.

Statements made during the most recent earnings call on April 27th indicate their adjusted EPS estimate for the second quarter is $0.75 per share. Most of the call focused on the progress they are making on Plant Vogtle Units 3 and 4. Unit 3 achieved initial criticality in March and was successfully synced to the grid in early April. They expect to be able to place Unit 3 into full commercial service in May or June of 2023. With Unit 4, hot functional testing was approximately 80% complete and they continue to project an in-service date between late fourth quarter of 2023 and end of the first quarter 2024. They stated they expect a $700M improvement in operating cash flow once both unit 3 and 4 are online.

Long-Term Trends

When looking at the projected CAGR's for all the separate sources the company keeps in its energy portfolio, they each have their own expected long-term growth rate. For the U.S. power market it's 5.6% . For solar it's 25.7% . For natural gas it's 7.2% globally. For hydrogen as a fuel it's 5.2% . nuclear is 4.8% , and coal is expected to have a CAGR of 1.97%.

For over twenty years now, I have been bullish on the long-term prospects of hydrogen as a fuel. Southern Company has entered into a coalition with several other utility providers to develop a hydrogen infrastructure. Several auto manufacturers are in the middle of developing vehicles which will create demand which these utility providers plan to meet with supply.

Financials

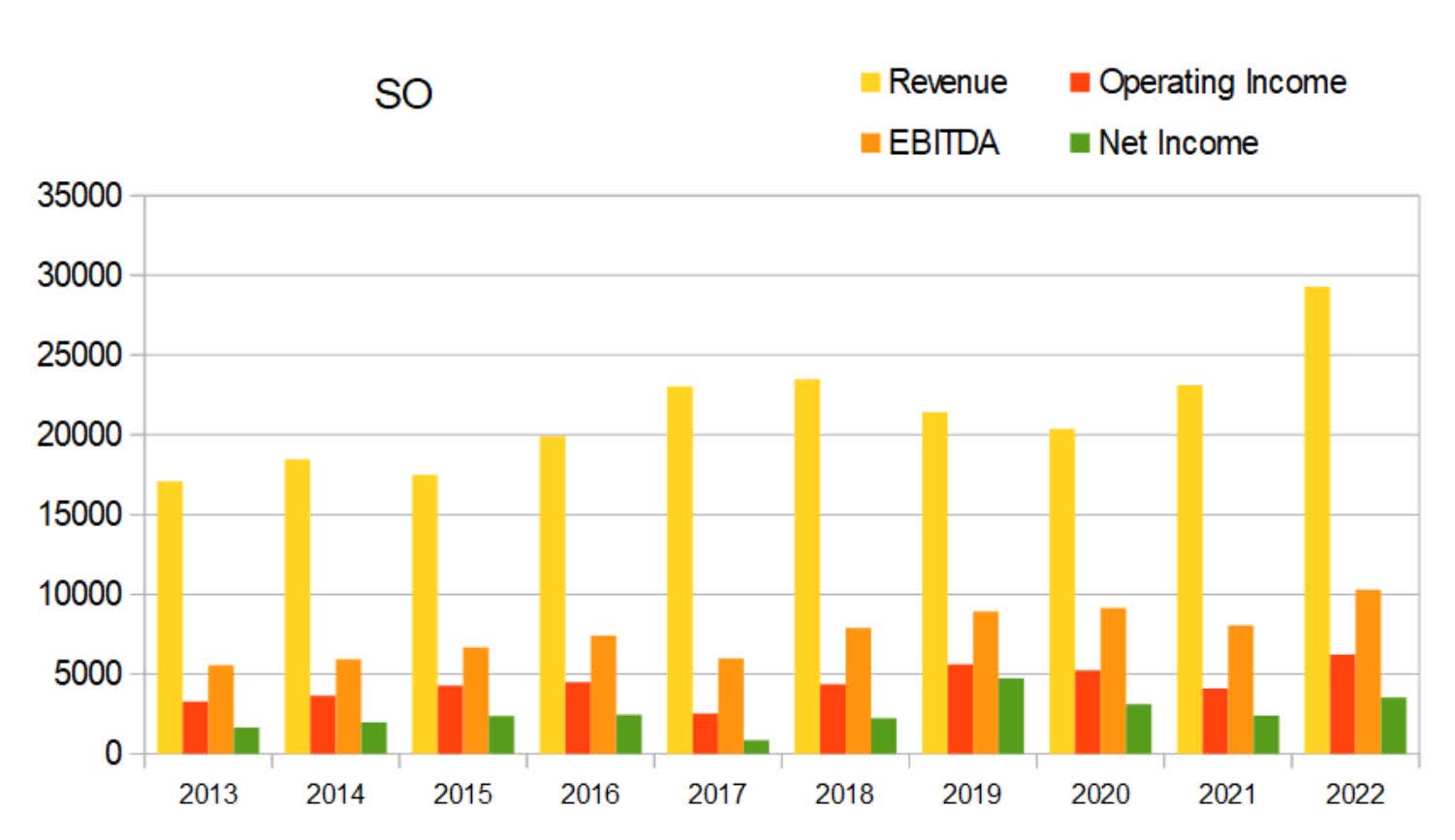

Looking over the company annually, they have growing revenue. In 2013 revenue was at $17.087B, by 2022 that had grown to $29.279B. This represents a 71.35% revenue rise.

{kind=link}

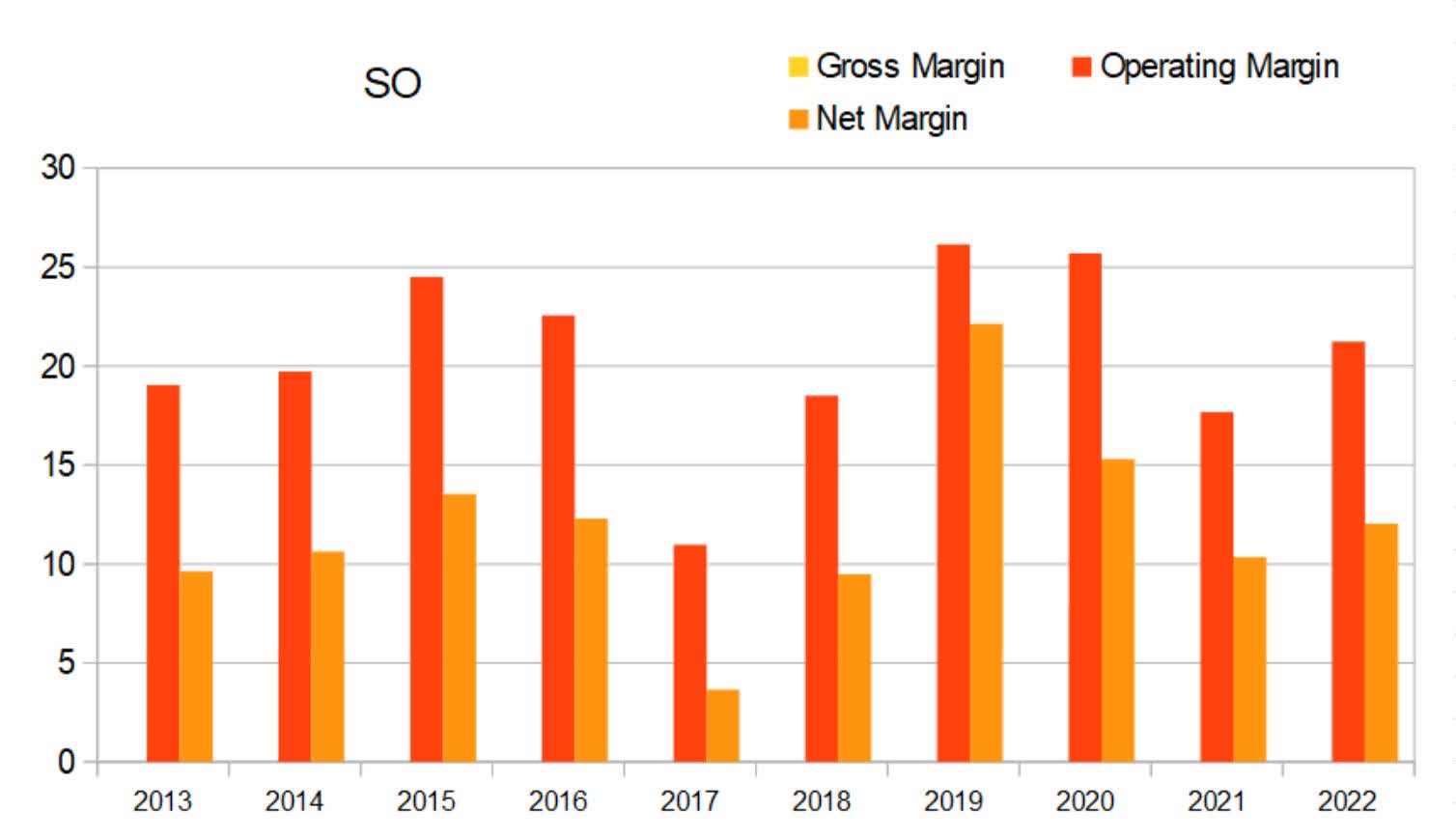

Margins contracted in 2017 and expanded in 2019. While ignoring these two outlier years, it appears that net margins have otherwise fallen between 9.47% and 17.66%.

{kind=link}

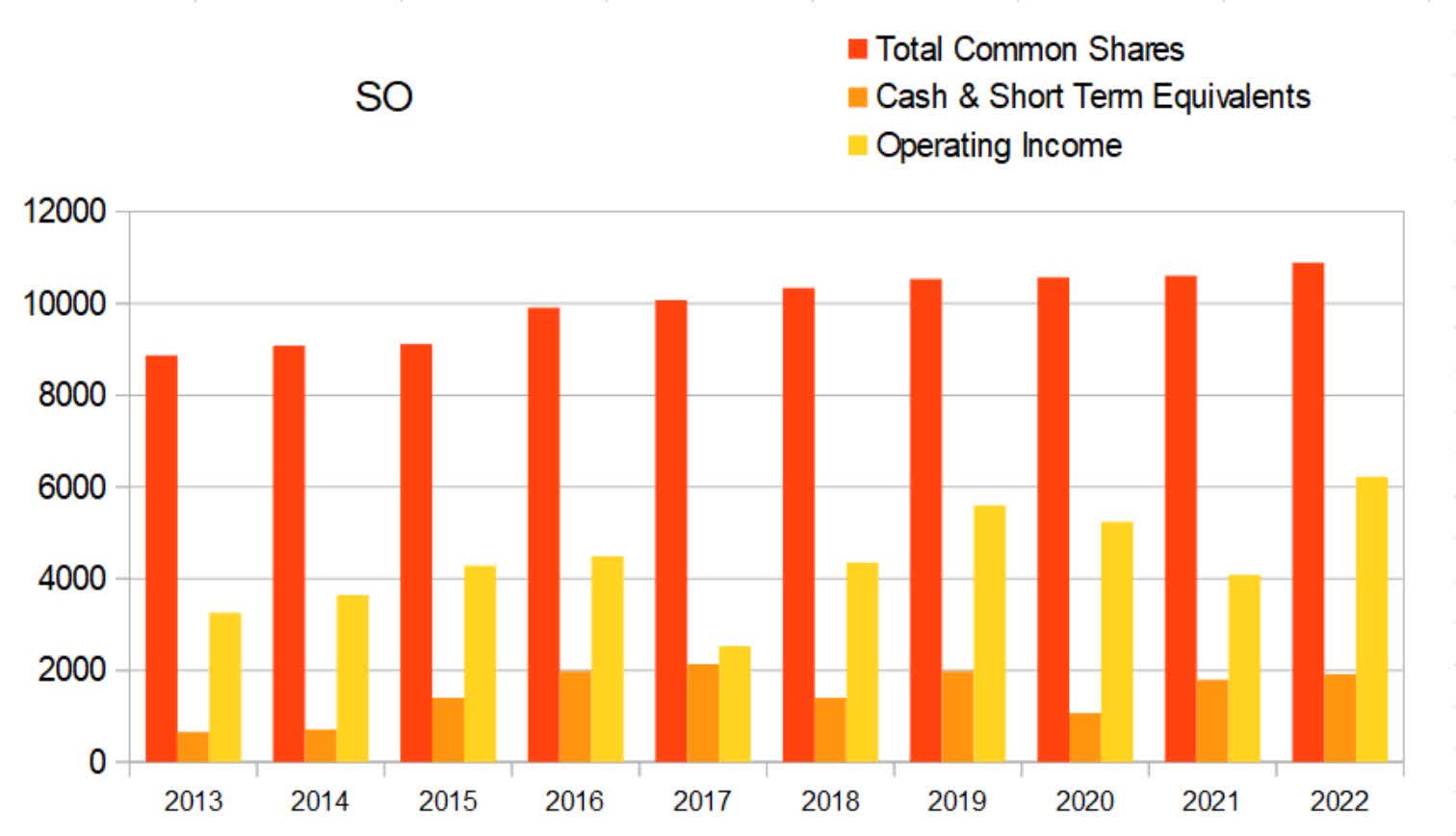

As of the 2022, they generated $29.279B in annual revenue and had $1.917B in Cash and Equivalents.

SO Annual Share Count vs. Cash vs. Income (By Author)

{kind=link}

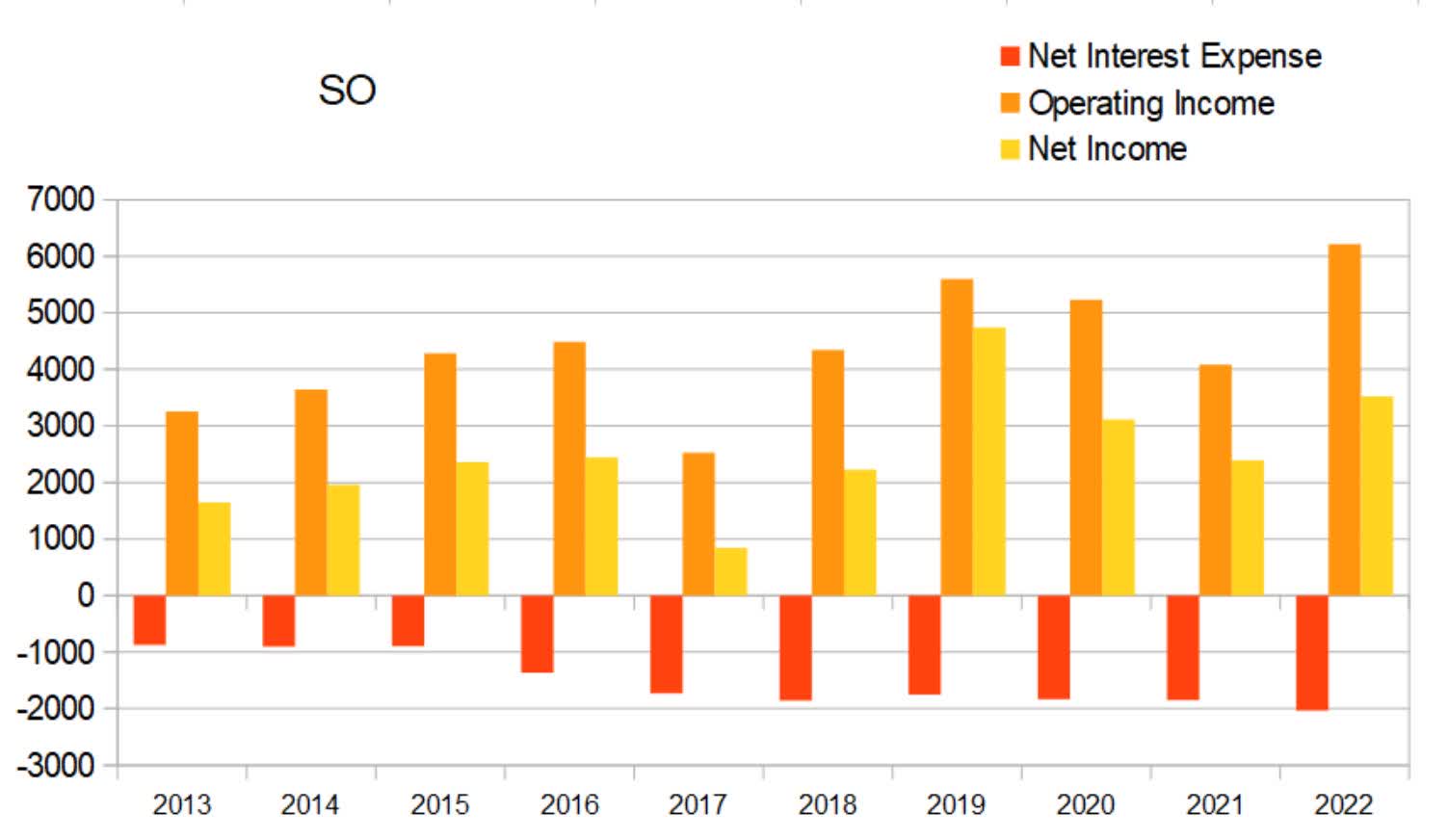

Their Net Interest Expense is consistently large. This is actually pretty typical for a utility.

SO Annual Net Interest Expense (By Author)

{kind=link}

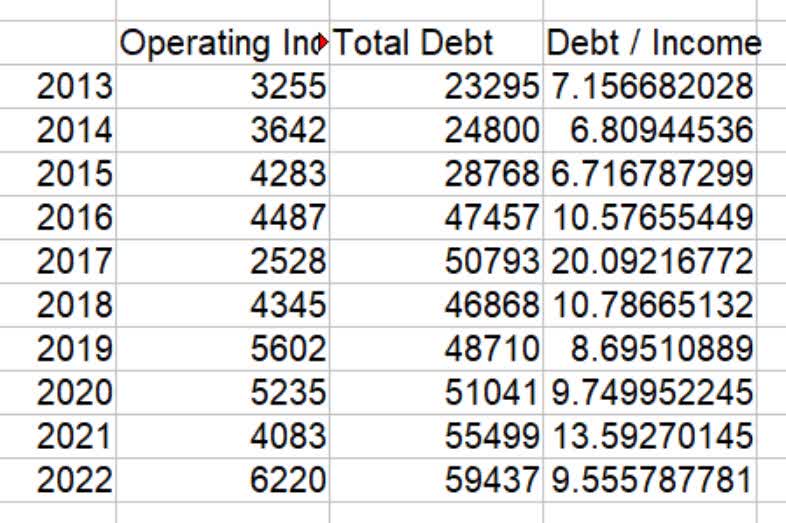

I usually look for Debt to Annual Operating Income ratios below 3x. However, with utilities I am used to seeing Debt to Annual Operating Income roughly ten times higher. This means that while this looks like a horrible debt to income ratio, it consistently comes in well below 30x. For a utility provider 9.56x is actually considered fairly healthy.

SO Annual Total Debt / Operating Income (By Author)

{kind=link}

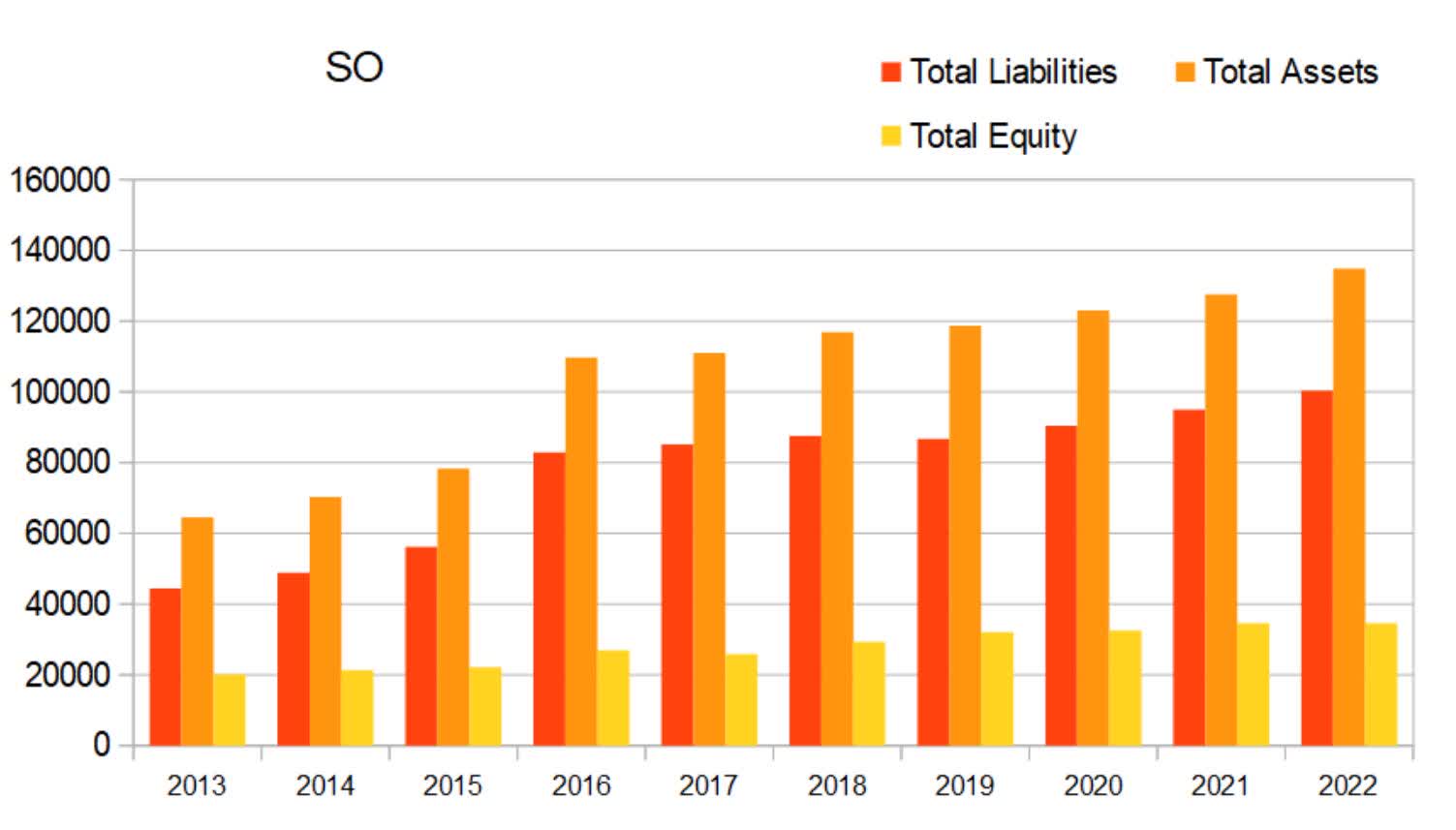

Annual total equity is slowly and steadily rising.

SO Annual Total Equity (By Author)

{kind=link}

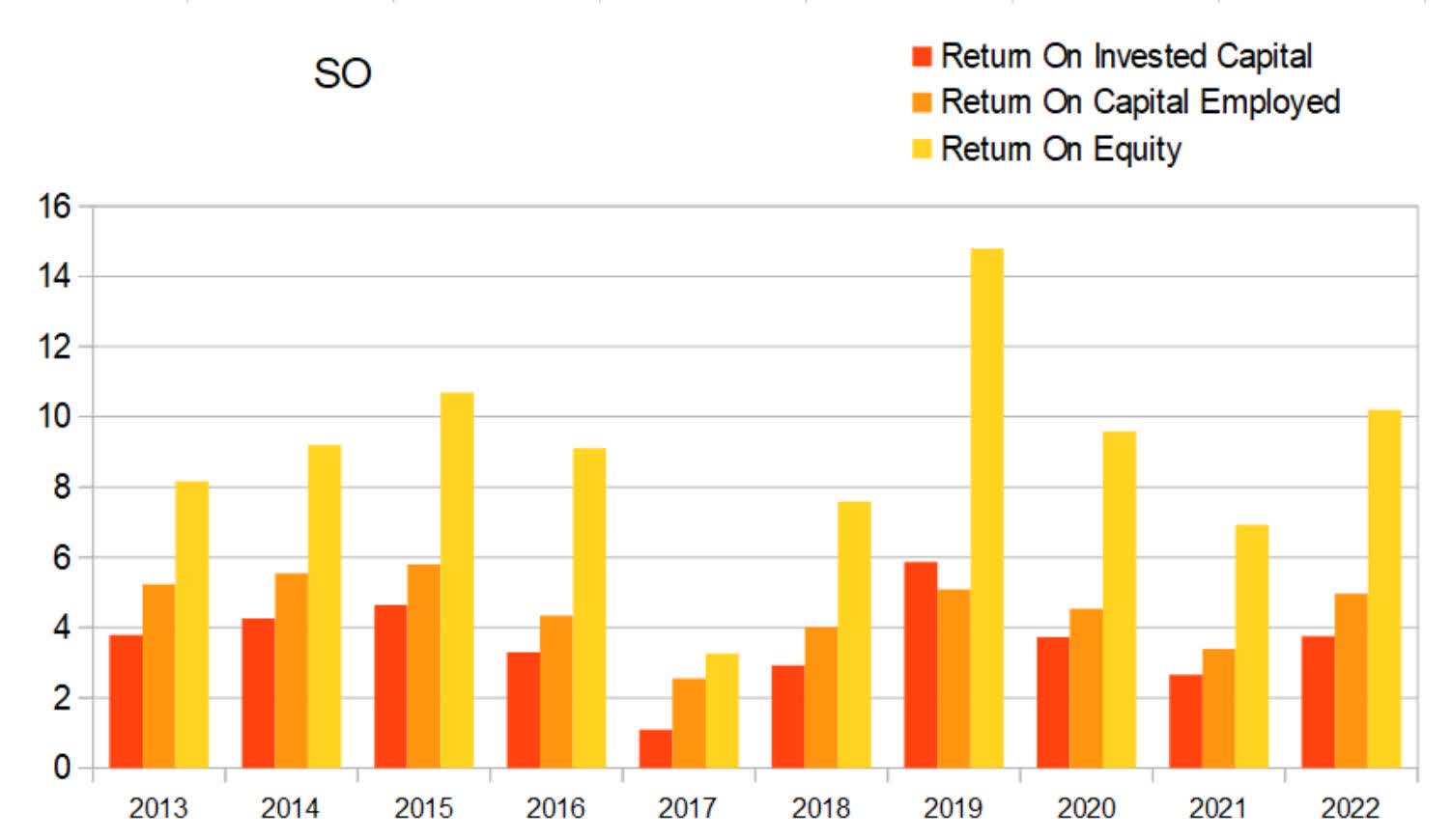

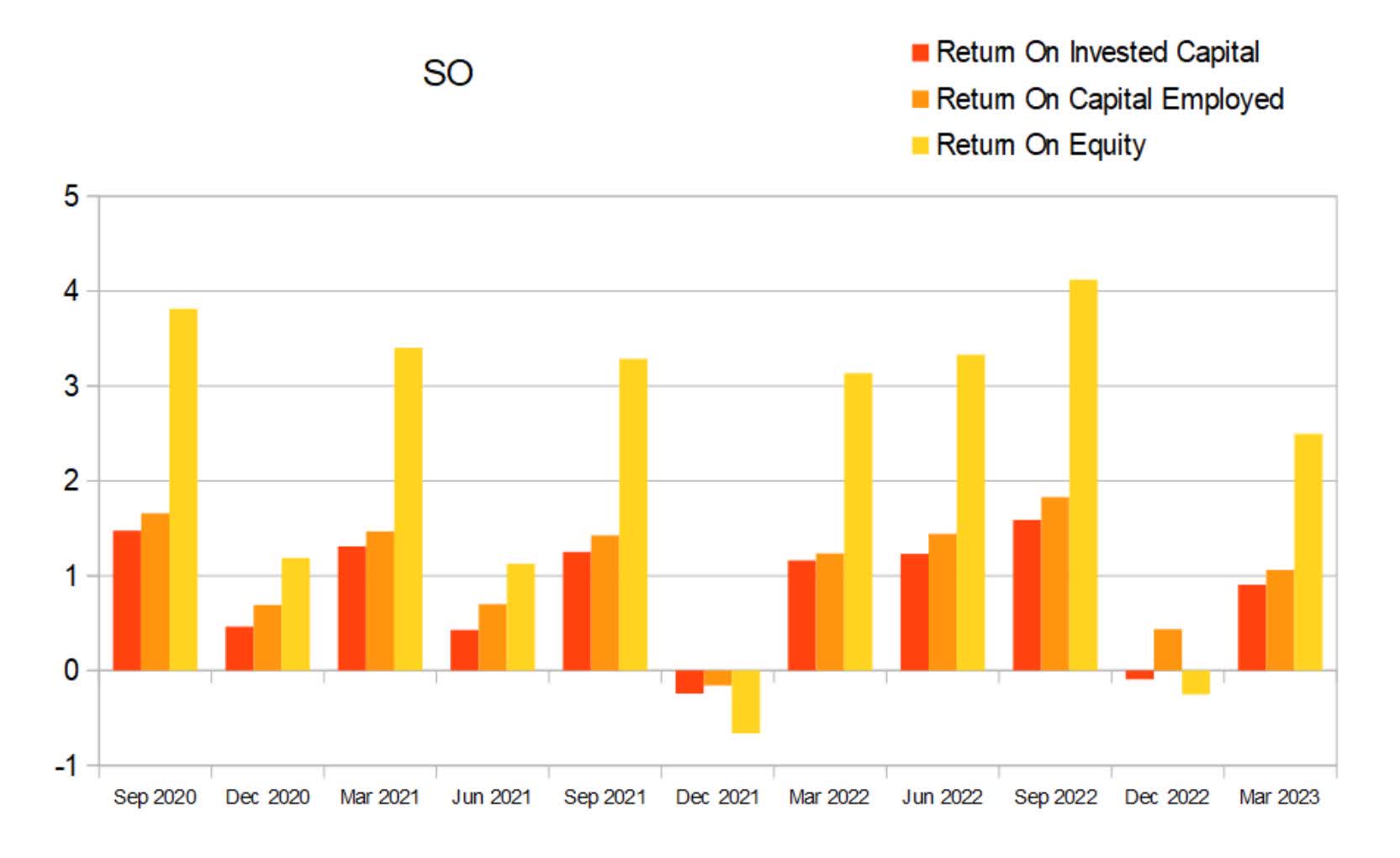

Their return values are consistently positive. The same dip in margins that occurred in 2017 also affected their returns. I usually want to see these values at or above 10% on an annual basis before I would consider buying a company. This is another one of those places where utilities are considerably different from most other types of companies; high debt and low returns are both normal. Because the services they provide are considered needs, their income is incredibly sticky. While utilities are not known for high returns, they are considered one of the more stable and reliable industries a person could invest into.

{kind=link}

Looking at their numbers on a quarterly basis, it becomes clear the company is affected by seasonality. Digging into their financial statements revealed that Southern Company typically experiences elevated maintenance costs and lower revenue every Q4.

SO Quarterly Returns (By Author)

{kind=link}

Quarterly margins during the other three quarters are strong enough that they more than cancel out their poor performance every Q4.

SO Quarterly Margins (By Author)

{kind=link}

Their operating income includes the seasonal maintenance costs. The company does not seem to experience significant drops in cash due to their poor Q4 values.

SO Quarterly Share Count vs. Cash vs. Income (By Author)

{kind=link}

Instead of looking for 10% on an annual basis, I usually want to see the average of these three values at or above 2.4% on a quarterly basis before I would consider buying. Again, with utilities, the standards for what can be considered attractive is atypical.

SO Quarterly Returns (By Author)

{kind=link}

Valuation

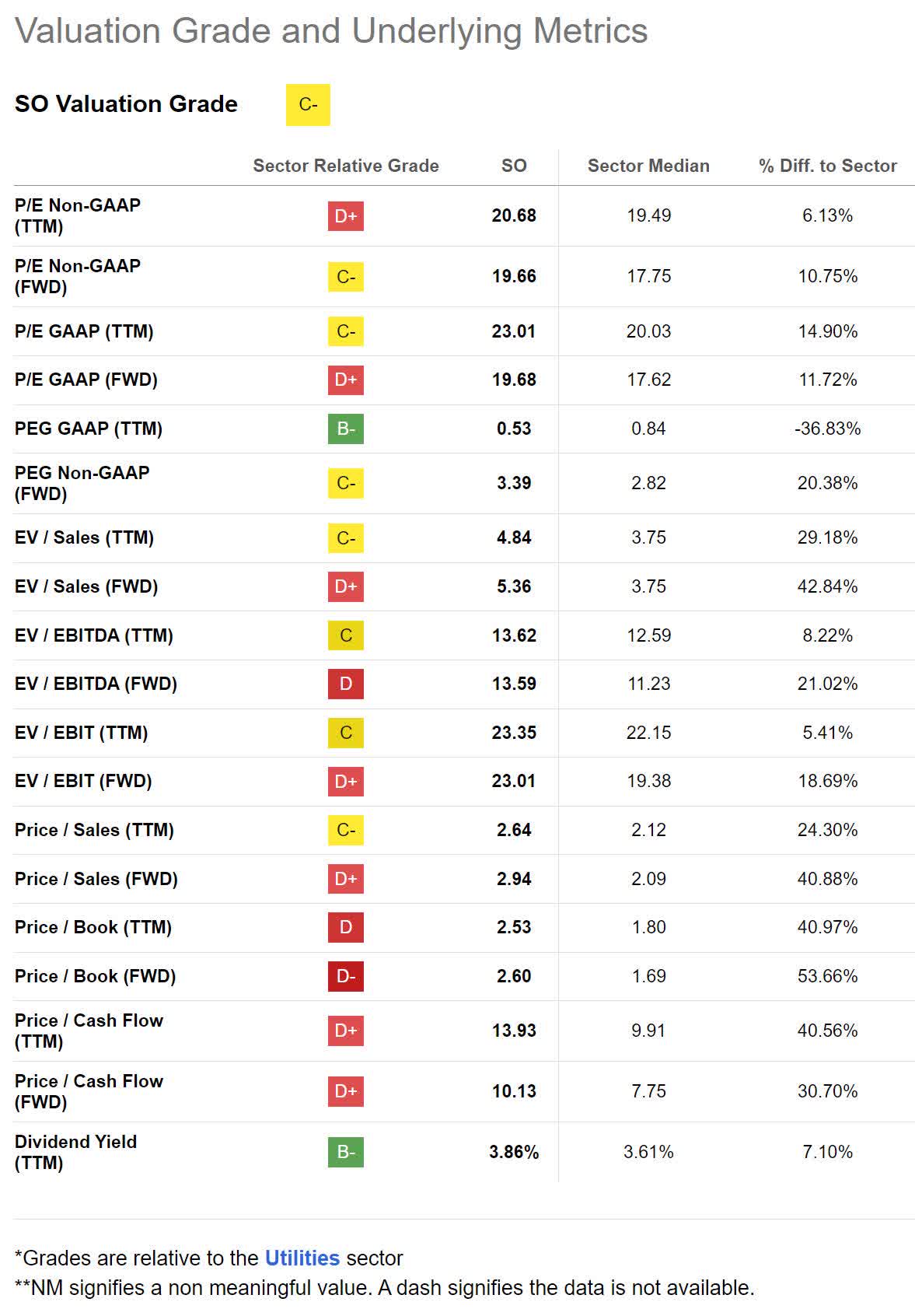

As of May 19th 2023, Southern Company had a market capitalization of $77.87B and traded for $71.41 per share. With their fairly low annual returns, I view their forward P/E of 19.68x, forward PEG of 3.39x, and a forward EV/EBIT of 23.01x, as showing the company as overvalued.

{kind=link}

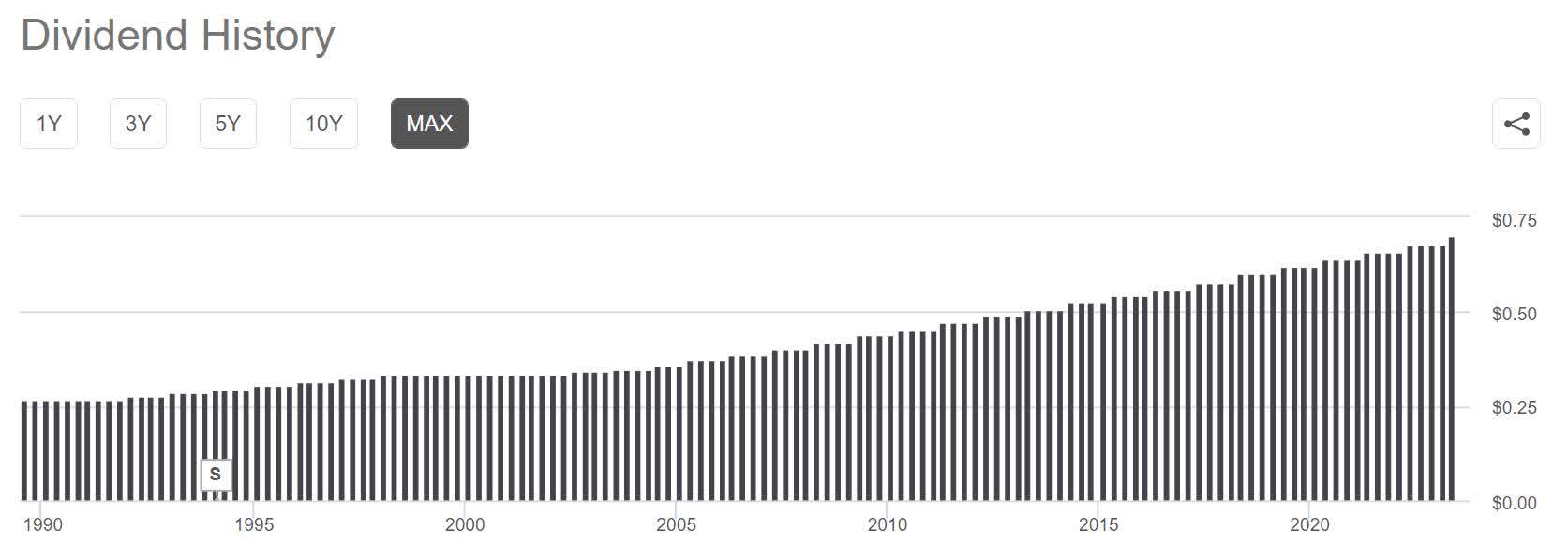

Southern Company has paid a dividend which was equal to or greater than the previous year, every year all the way back to 1948. Over the last 10 years, they have maintained dividend growth at a CAGR of 3.32% . Using today's annual dividend of $2.78 per share, a dividend growth rate of 3%, a discount rate of 9%, and assuming they can maintain this dividend growth for 20 years, a discounted cash flow calculator produces a fair value estimate of $42.30 per share. While using a discount rate of 9%, the company currently appears to be overvalued.

SO Dividend History (Seeking Alpha)

{kind=link}

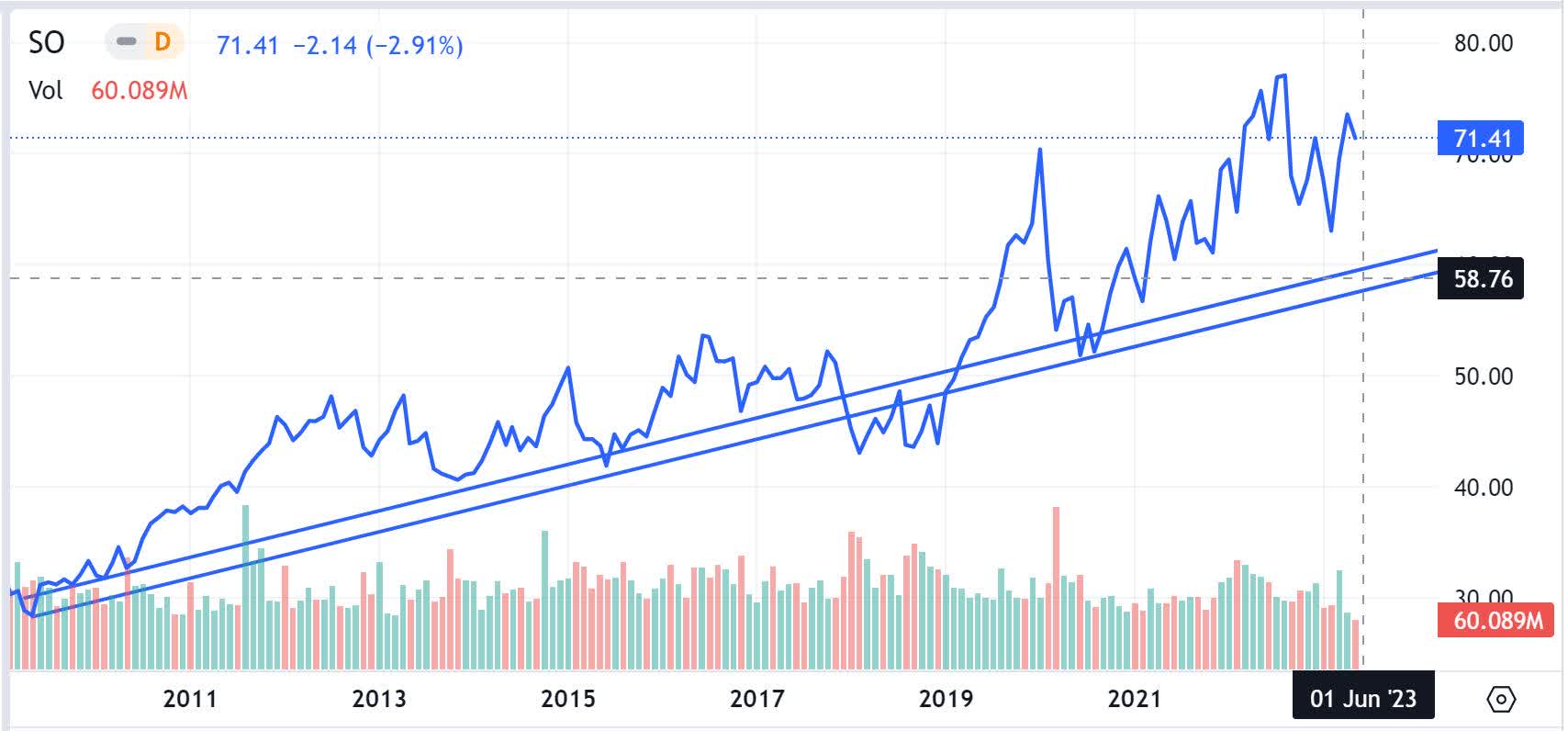

I have been accused of using too high of a discount rate when evaluating utilities in the past, so let's instead derive one from the chart. Since they began steadily increasing their dividend around 2005, their chart took on new behavioral characteristics. It formed its next low in 2009. In 2017, the company experienced a significant margin contraction before returning to normal. This has produced a clear ascending zone of liquidity on the chart which gives us a visual estimate for fair value.

SO Chart (TradingView via Seeking Alpha)

{kind=link}

Varying the discount rate, while keeping all the rest of the discounted cash flow calculator values the same, allows us to guess-and-check into what the market thinks a fair discount rate for this stock is. A discount rate of 6.8% produces a fair value estimate of $58.65 per share.

Risks

This company is slowly transitioning its portfolio and there is a chance that they experience unforeseen problems during the asset update, or that the resulting portfolio ends up being less lucrative than they anticipate.

The Inflation Reduction Act is helping utilities modernize. Although unlikely, if it were repealed or portions of it were revised, the tailwinds all these separate utilities are relying on might go away.

Natural disasters and malicious intent both perpetually threaten our energy grid. I expect that most disruptions will be temporary and have only a small chance of causing lasting damage to the financial health of the company.

Catalysts

Starting around 2005, the dividend began steadily growing. It is possible that restructuring their portfolio improves revenue and margins to the point that they increase their rate of dividend growth.

If the coalition the company is a part of manages to make the hydrogen infrastructure a reality, it will grant Southern Company an additional income stream. While I doubt the news of its completion will cause a significant revaluation, it should positively affect their financials and provide long lasting tailwinds.

Conclusions

Overall, Southern Company is a solid company with a bright future. Once they finish bringing units 3 and 4 online, their costs will go down while their revenue should go up. Their financials should improve significantly.

When I previously gave a Buy rating for Southern Company, they were only slightly overvalued. Price has since appreciated to the point where I have to change that to a Hold. While this is still an appealing long term investment, I wouldn't consider buying until price falls back below $65 per share, and wouldn't buy with significant size until price falls below $60 per share.

For further details see:

Southern Company: A Solid Company With Bright Future, But Overvalued