SO - Southern Company: A Top-Tier Utility Yielding 4% Trading 16% Below Its Highs

2023-08-07 04:50:24 ET

Summary

- Southern Company achieves a major milestone with the launch of Vogtle Unit 3, becoming a leader in America's return to nuclear energy.

- The completion of Vogtle Unit 4 is progressing well, and the company is exploring opportunities in green hydrogen production.

- Despite challenges in the past, SO's commitment to reducing emissions and its solid dividend track record make it an attractive option for income-oriented investors.

Introduction

Georgia-based Southern Company ( SO ) is a utility I've always liked as a high-yield play. However, in the past two years, I started to put it on top of my list, as I believe it's one of the best utility companies money can buy.

The company just achieved a major milestone, as Vogtle Unit 3 has gone online, making the company a pioneer in America's (very slow) return to nuclear energy.

Given tremendous progress at Vogtle Unit 3, the company will soon be in a great spot with tailwinds from rising income and rapidly falling capital expenditures.

When adding the 4% yield and the decline in its stock price, leading to better valuations, I believe that income-oriented investors may benefit from taking a closer look at this regulated utility giant from the Peach State.

A Major Milestone

On August 1, the Energy Information Administration wrote a report on a major new milestone: the first new US nuclear reactor since 2016 is now in operation.

Energy Information Administration

Vogtle 3 boasts a capacity of 1,114 megawatts (MW), which is further enhancing the existing power generation capabilities of Plant Vogtle.

This facility, jointly owned by Georgia Power and three other utility companies, already houses two reactors with a combined capacity of 2,430 MW, which were brought online in the late 1980s.

As much as I like nuclear energy as a way to provide affordable and reliable energy, there are reasons why almost no new capacity was brought online since the early 1990s: costs and associated risks.

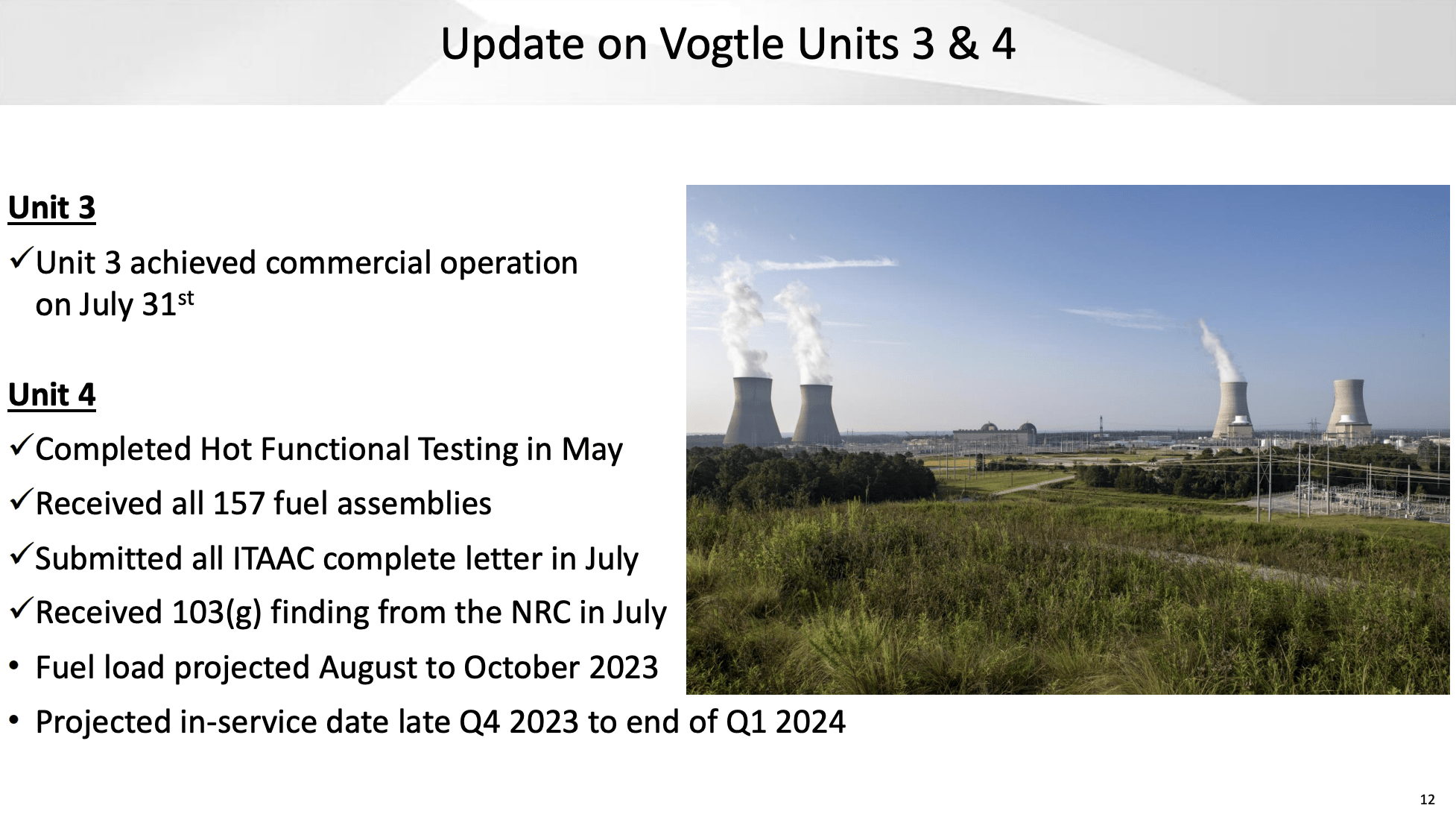

Construction of Vogtle 3 & 4 began in 2009, originally projected to cost $14 billion, and commence operations by 2016 and 2017.

However, the project faced significant delays and cost overruns, resulting in a revised estimated cost exceeding $30 billion!

With regard to Vogtle Unit 4, Southern Company said that it made substantial progress, including the completion of hot functional testing and the receipt of all 157 fuel assemblies, as well as the 103G finding from the Nuclear Regulatory Commission, indicating that the acceptance criteria for Unit 4 have been met.

{kind=link}

The company's current focus is on final testing and system turnover to prepare for the fuel load on Unit 4. The company projects that Unit 4 will be placed in service between the late fourth quarter of 2023 and the end of the first quarter of 2024.

Furthermore, the company is exploring options to use nuclear power to produce green hydrogen. I believe in the future of hydrogen and consider nuclear energy to be the best source to produce it.

However, for now, the company isn't very specific about its plans.

This is what Chris Womack, CEO of Southern Company, said during the 2Q23 earnings call when he was asked about Vogtle's role in green hydrogen production (emphasis added):

Let me say something quickly about hydrogen, and I'll let Dan touch on any rules from treasury. We're participating in a number of processes DOE has with hydrogen hub . So we're excited about that. As you may recall, we did a 20% blend at our Platt McDonough Gas site. So we're excited about all the technology activity and the considerations that are going on around hydrogen. We look forward to seeing if we can develop this market and get the pricing right, get the transportation of the product right and then we can find off-takers . I mean, so we're thrilled by the possibility and how Vogtle can continue to serve customers in Georgia. So there are a lot of aspects of hydrogen that we get really excited about. Clearly, there's a lot of work that's got to be -- that we've got to work through to get to that point to make it viably commercial -- commercially viable .

Essentially, these comments make sense, as we're in the early stages of commercial (green) hydrogen, which requires complex infrastructure, long-term contracts to make investments worthwhile, and so much more.

Additionally, the company is looking into non-nuclear renewables as it is assessing the benefits of investment tax credits and production tax credits.

{kind=link}

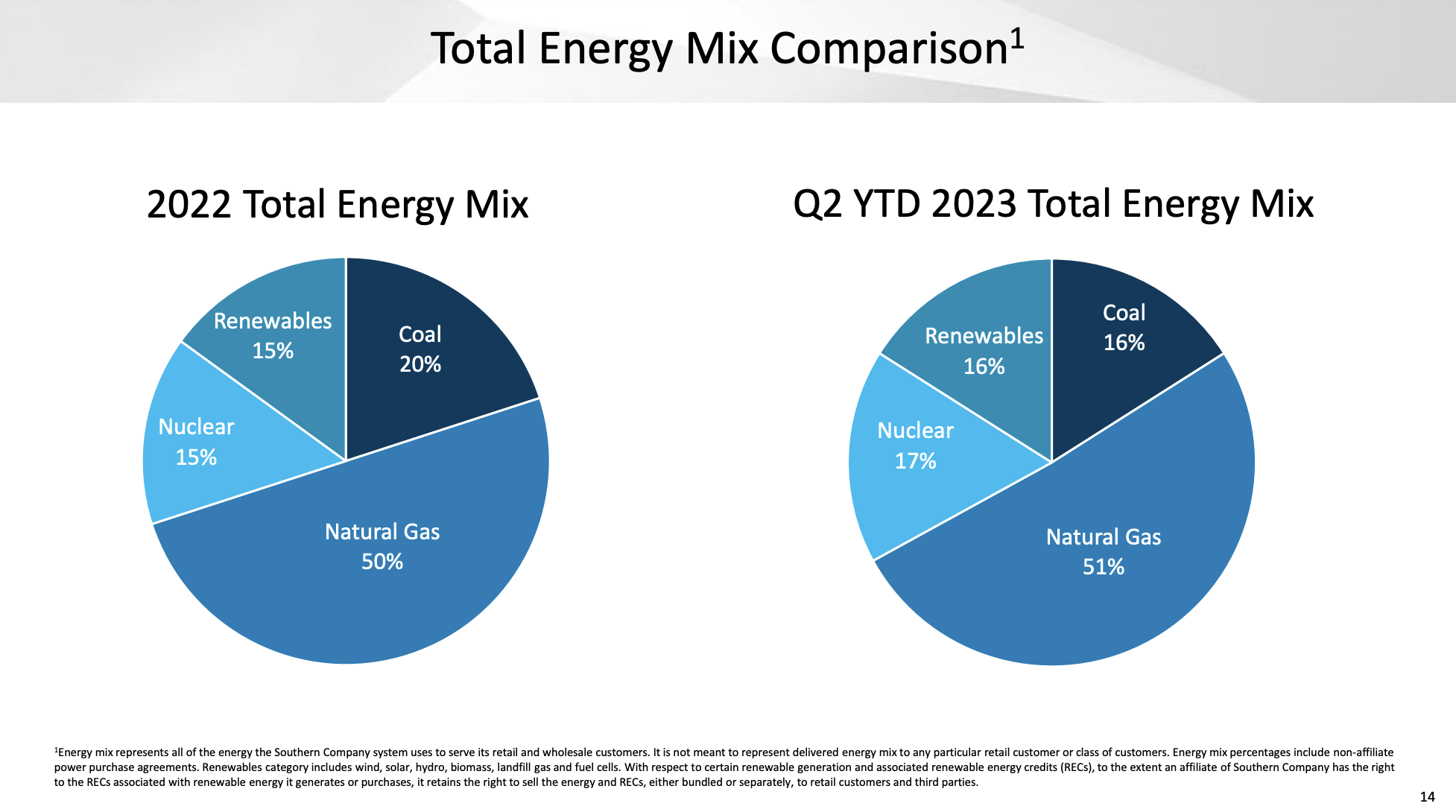

The company, which is expected to reduce its emissions by 50% in 2030 (versus 2007) and 100% by 2050, generated only 16% of its energy from high-emission coal at the end of the second quarter.

Half of its energy comes from low-emission natural gas. A third of its mix is completely free of emissions (ignoring the missions that come from the production of renewable energy technologies).

Shareholder Remains In A Great Spot

Because of the imminent completion of the Vogtle expansion, the company's capital expenditures are not expected to rise anymore. This year, CapEx is expected to peak at $8.5 billion, followed by a gradual decline to $8.0 billion in 2025.

This paves the way for a potential free cash flow surge of $1.4 billion in 2023E to $1.9 billion in 2025E.

At this point, I need to note two things:

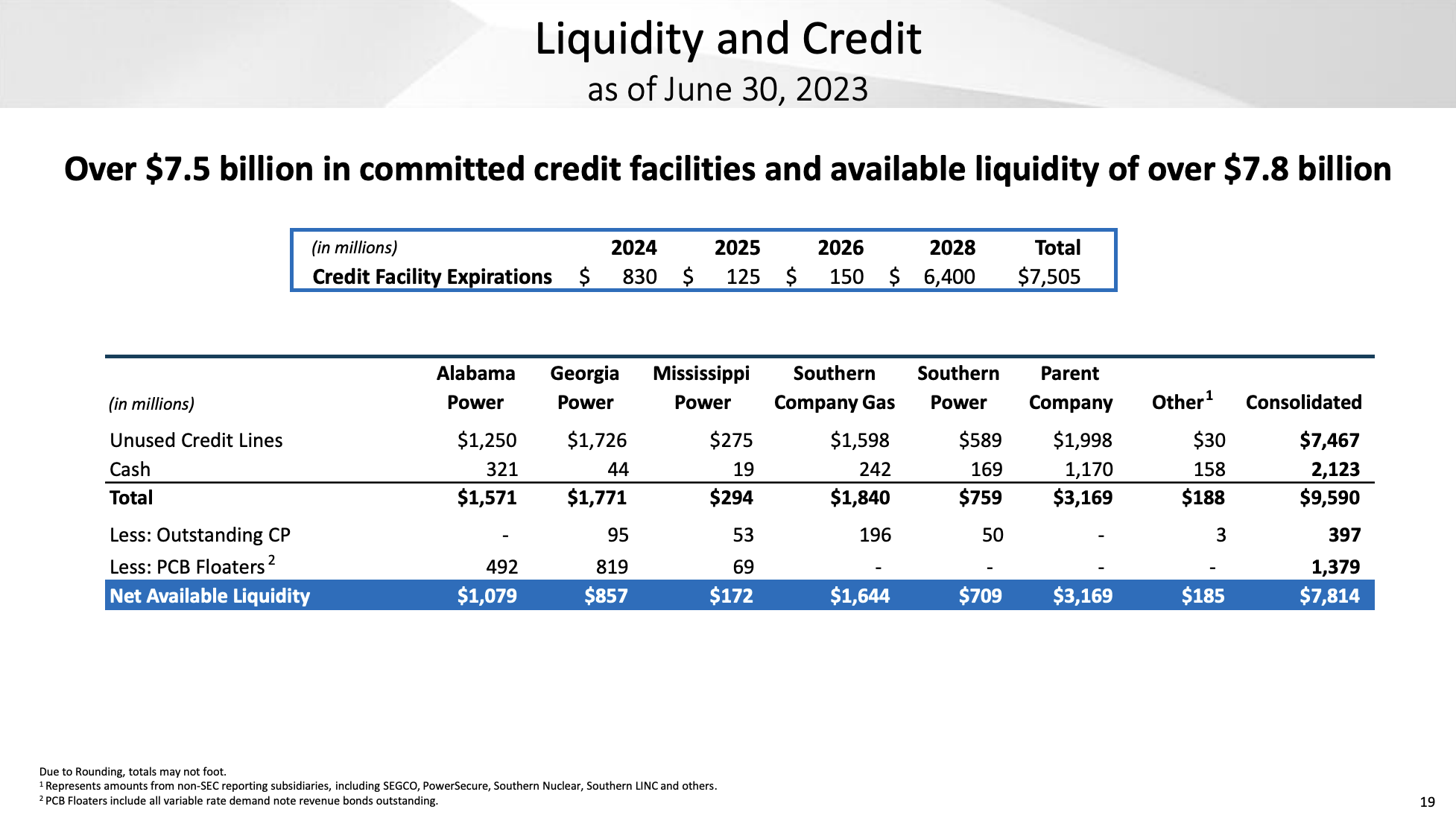

- $1.9 billion in 2025E free cash flow indicates a 2.6% free cash flow yield. This does not support the company's dividend of 4.0%, which means additional borrowing is needed - especially if accelerated investments in renewable energy or green hydrogen are required. This will likely boost net debt from $60.3 billion in 2023E to $64.8 billion in 2025E. However, this isn't a major issue as debt is used for value-adding projects. Hence, the net leverage ratio is expected to FALL from 5.9x (EBITDA) in 2023E to 5.3x in 2025E. Adding to that, the company has a BBB+ credit rating (one step below the A-range) and $7.8 billion in available liquidity - most of it from undrawn credit lines.

{kind=link}

- Point number two is related to free cash flow. Even though SO's free cash flow does not cover its dividend, at least it is reporting positive free cash flow. Almost all major peers are dealing with negative free cash flow, as investments in renewables and the accelerated retirement of coal plants are causing CapEx to skyrocket. Hence, the near-completion of Vogtle 3 & 4 and the massive long-term benefits that come with nuclear are reasons why I believe that Southern Company is one of the best utilities on the market.

The chart below shows the ratio between SO and the utility ETF ( XLU ) - including dividends.

After the Great Financial Crisis, SO was an underperformer. Elevated costs related to Vogte 3 & 4 caused uncertainty, and most money went into companies with more renewable exposure - like NextEra Energy ( NEE ).

Since the pandemic, Southern Company has started to consistently outperform its peers, which I expect to continue.

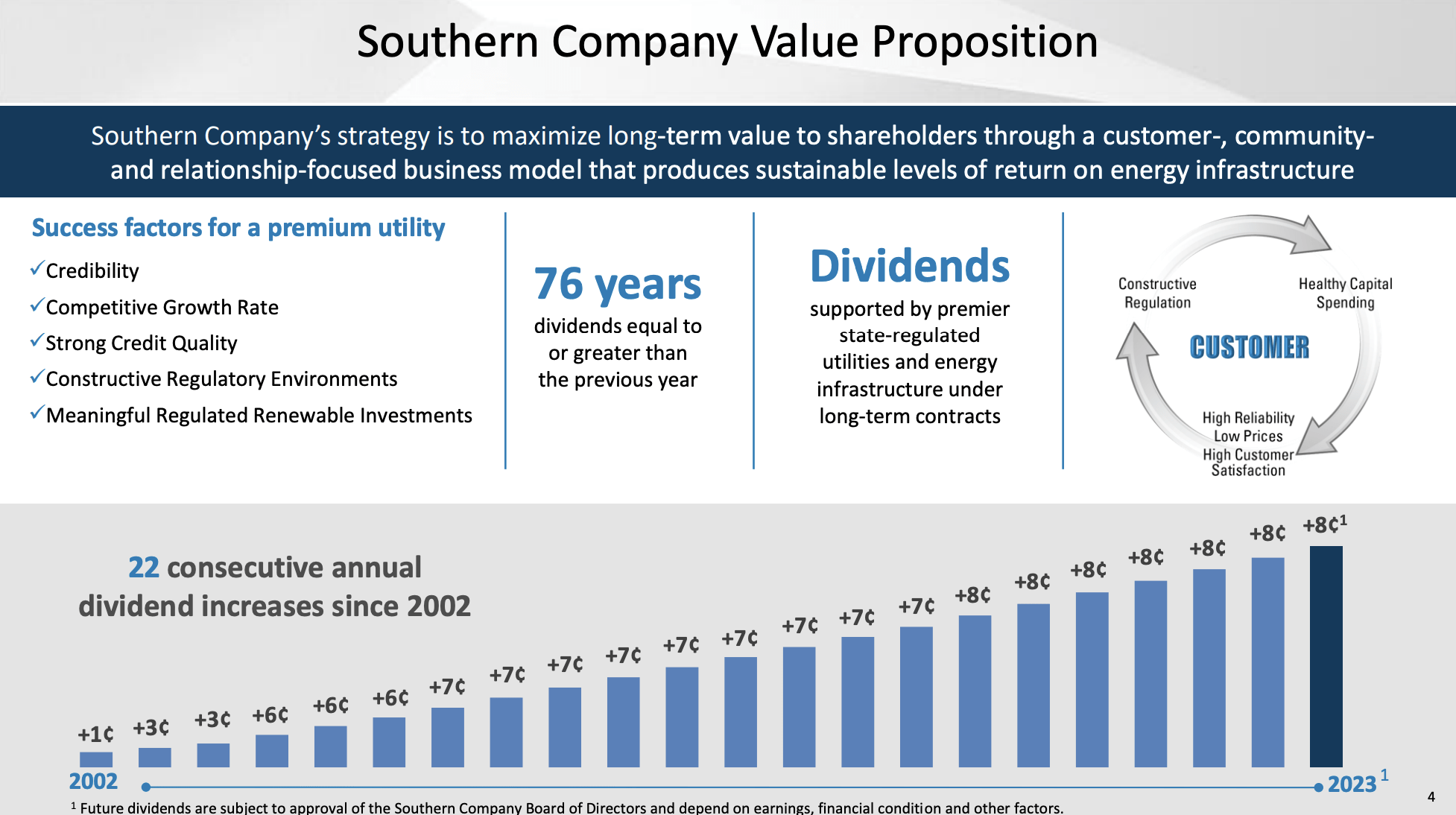

With this in mind, the company has a stellar dividend track record of 22 consecutive annual dividend hikes since 2002. The company hasn't cut its dividend for 76 years.

{kind=link}

- The current dividend yield is 4.1%. The utility ETF XLU yields 3.1%.

- The net income payout ratio is 87%. However, as discussed, CapEx requirements have pushed the cash payout ratio above 100%.

- Over the past five years, the dividend has been hiked by 3.2% per year - on average.

- On April 17, the company hiked its dividend by 2.9%.

- I do not expect dividend growth to accelerate meaningfully, which is OK, as SO's dividend growth is in line with its major peers and slightly above the Fed's inflation target.

Outlook & Valuation

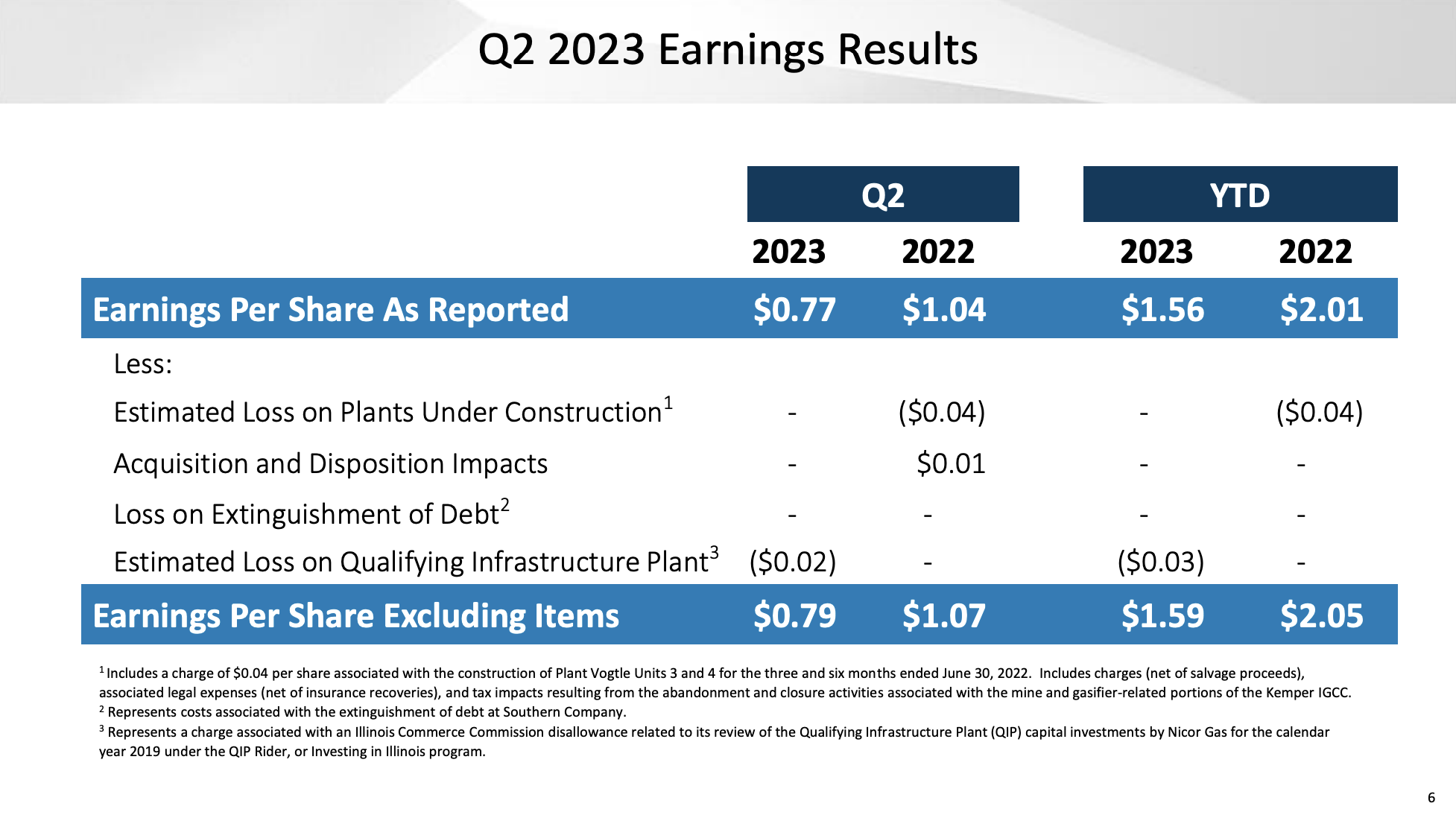

In the second quarter of 2023, Southern Company reported adjusted earnings of $0.79 per share, surpassing estimates by $0.04 but lower by $0.28 compared to the previous year.

{kind=link}

According to the company, several factors influenced this performance, including milder than normal weather conditions, higher depreciation, and amortization, interest expenses, changes in rates and pricing, along with lower income taxes and O&M expenses.

{kind=link}

The mildest weather on record during the first half of 2023 had a significant negative impact of $0.16 per share on earnings, which presents a major headwind for the full-year result.

Needless to say, Southern Company remains focused on cost management and maintaining safety, reliability, and customer satisfaction in the second half of the year. The adjusted earnings estimate for the third quarter of 2023 is $1.30 per share.

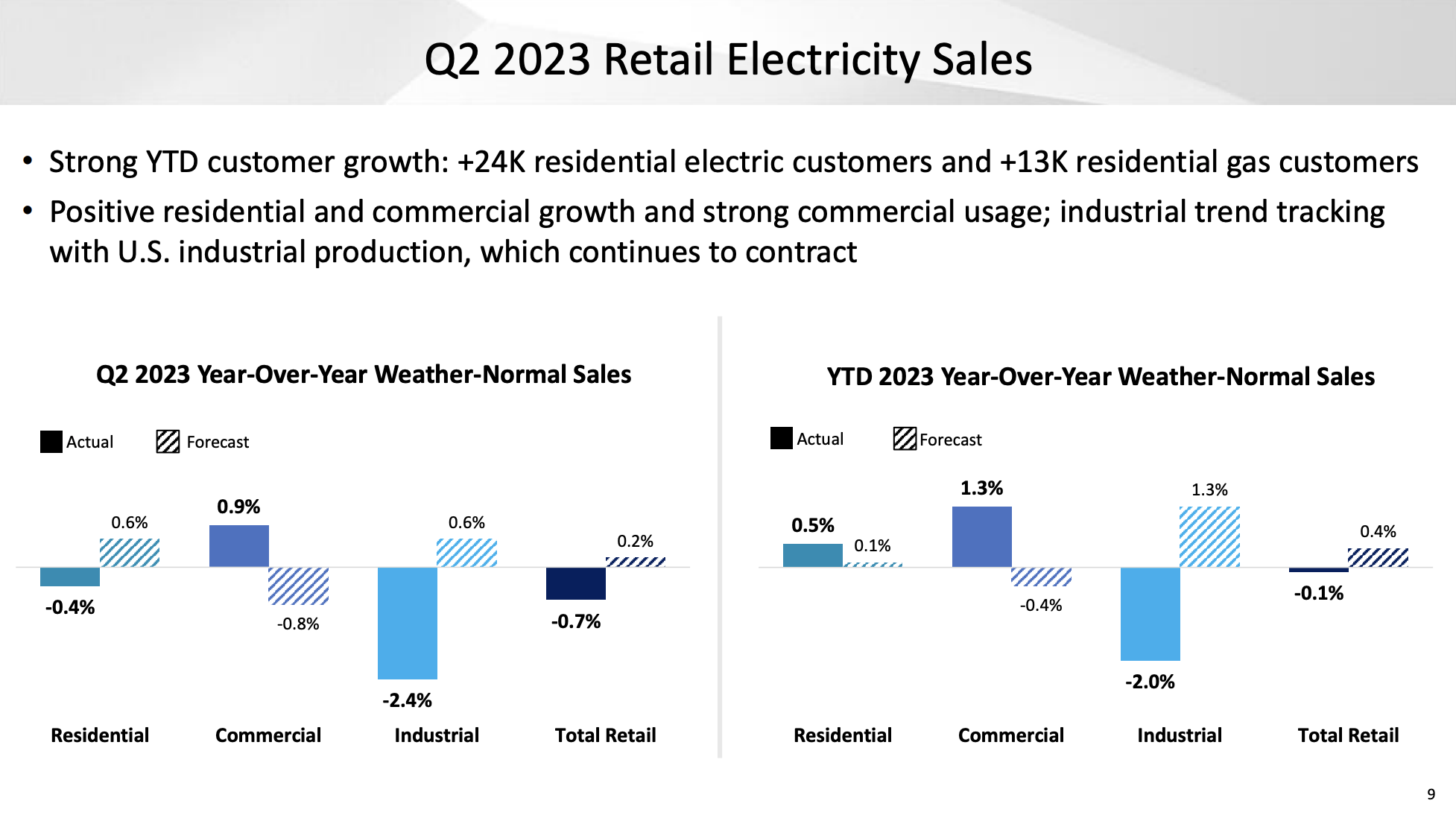

Year-to-date retail sales in 2023 have been in line with sales levels for the first half of 2022, with positive growth in residential and commercial sectors offset by lower industrial sales.

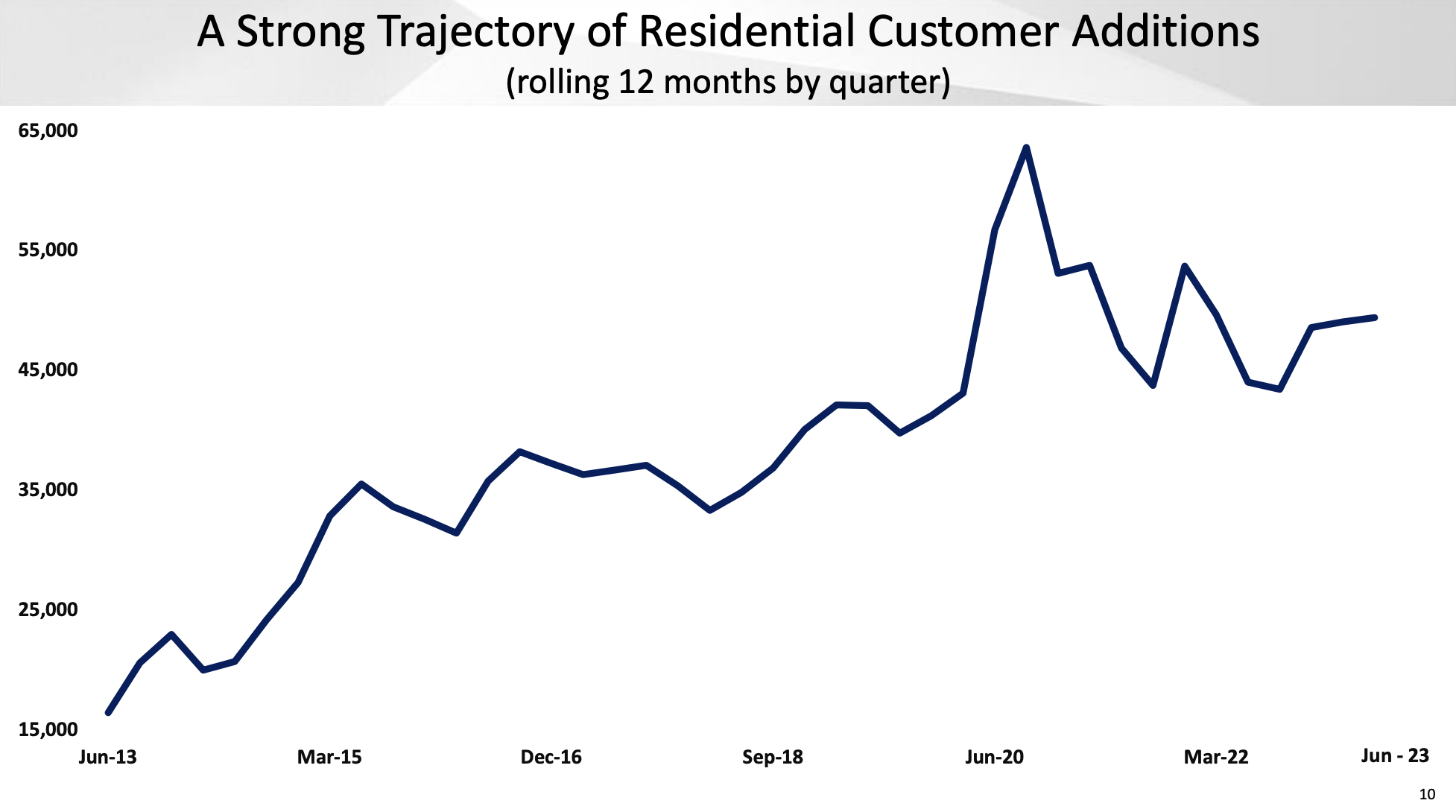

Southern Company added nearly 24,000 electric customers and 13,000 natural gas customers year-to-date, surpassing pre-pandemic levels.

{kind=link}

The company also sees a lot of future growth related to economic re-shoring to attractive states like Georgia. However, for now, these benefits are very limited.

Having said that, SO shares are 16% below their 52-week high and down 5% year-to-date.

Recent stock price weakness seems to be triggered by the belief that interest rates will likely remain higher for longer, which is bad news for so-called yield plays and stocks with elevated debt levels and financing requirements - even though SO's balance sheet is in great shape.

FINVIZ

The company is currently trading at 13.4x NTM EBITDA, which is a bit above the median sector multiple of 11.3x.

I believe this premium is warranted.

Analysts currently maintain a $73 consensus price target, which is 8% above the current price.

I agree with this target, maintain a bullish rating, and believe that SO is a good investment on weakness.

Takeaway

The Southern Company has recently achieved a significant milestone with the successful launch of Vogtle Unit 3, making it a leader in America's return to nuclear energy.

With this expansion, the company is poised for growth, benefiting from rising income and declining capital expenditures.

As an income-oriented investor, the 4% yield and improved valuations make SO an attractive option to consider.

Despite facing challenges in the past with cost overruns, the completion of Vogtle Unit 4 is progressing well, and the company is exploring opportunities in green hydrogen production.

The utility's commitment to reducing emissions and its solid dividend track record further bolster its appeal.

Though SO's free cash flow doesn't fully cover its dividend, its positive free cash flow sets it apart from many peers.

The recent outperformance against industry rivals and a stellar dividend history make SO a top utility pick in the market.

While recent stock price weakness may be a concern, the company's strong balance sheet and future growth prospects justify its premium valuation.

I remain bullish on SO and believe it's a good investment opportunity, especially during periods of weakness.

For further details see:

Southern Company: A Top-Tier Utility Yielding 4%, Trading 16% Below Its Highs