SO - Southern Company: Hold This Stock For Stable Dividend Yield

2023-10-11 16:06:01 ET

Summary

- The Southern Company has announced acquisitions of Solar Facilities, positioning itself to capture the growing demand in the renewable energy industry.

- The company's dividend payout and consistent growth make it an attractive stock for investors looking for stable and regular income.

- After comparing the forward P/E ratio of 17.03x with industry average P/E ratio of 16x, we can say that the company is fairly valued.

Investment Thesis

The Southern Company ( SO ) is a utility business in the southern United States. It also has a high dividend payout, which makes it an attractive stock to hold in the portfolio. It has recently announced acquisitions of Solar Facilities, which I believe can boost its growth in long-term, as these acquisitions can make it strongly positioned to capture the growing demand in the industry.

About SO

SO is a holding corporation that owns Southern Power Company, Southern Company Gas, and three traditional electric operating companies. The Southern Power Company deals with developing, constructing, acquiring, owning, and managing power generation assets and selling electricity in the wholesale market at market-based rates. It contributes 11.32% to the company’s total operating revenues. The Southern Company Gas mainly distributes natural gas in four states: Georgia, Illinois, Tennessee, and Virginia. It accounted for approximately 20.04% of the total operating revenues. The Traditional electric operating companies consist of three companies: Alabama Power, Georgia Power, and Mississippi Power . The traditional electric operating companies contributed approximately 68.64% to the company’s total operating revenue.

Financials

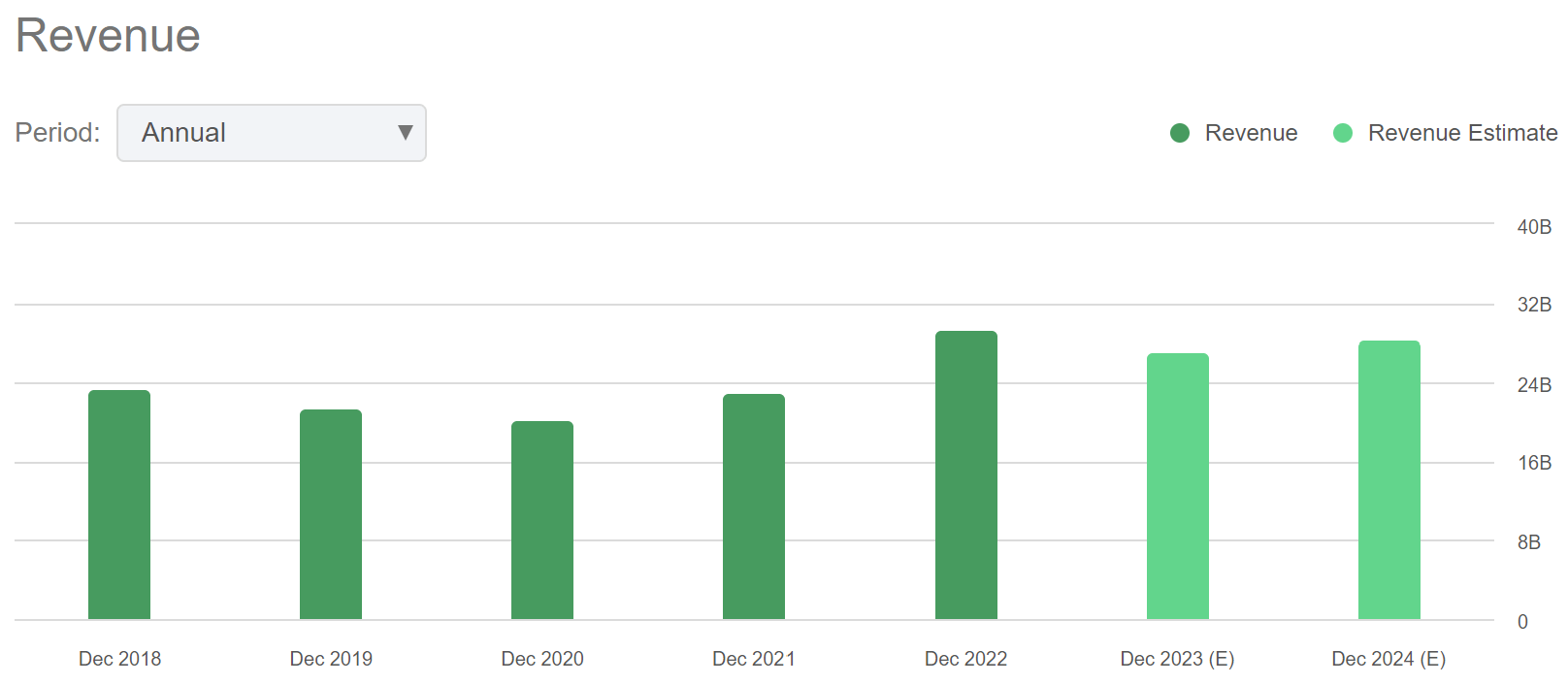

Revenue Trend of SO (Seeking Alpha)

{kind=link}

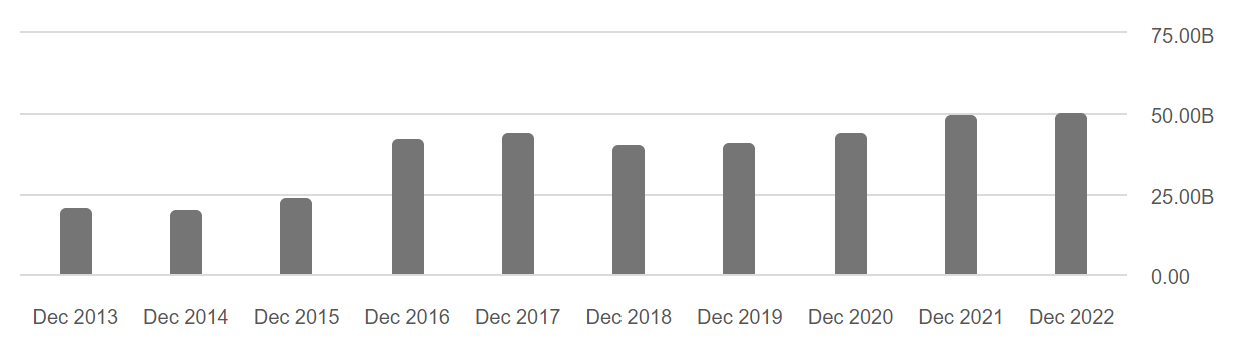

SO was experiencing a declining revenue trend from FY2018 to FY2020 due to low energy demand from residential, commercial and industrial customers. It reported revenue of $20.38 billion in FY2020 which indicates 3-year CAGR of -4.63% compared to $23.50 billion in FY2018.

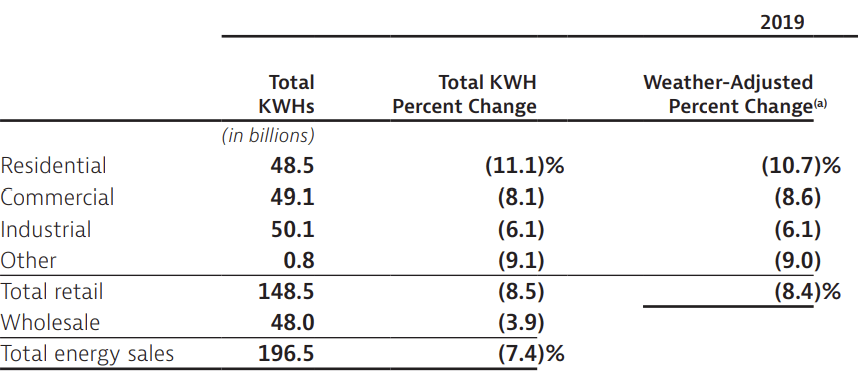

Decreasing Energy Demand in 2019 of SO (2019 Annual Report of SO)

{kind=link}

However, SO’s revenue growth rebounded in FY2021 with a revenue growth of 13.4% YoY compared to revenue of FY2020. Its growth was sustained in FY2022 with revenue of $29.28 billion which is 26.7% YoY growth compared to $23.11 billion in FY2021. This growth was mainly driven by supply chain disruption caused by the growth of customers . The company is still experiencing strong growth in the residential and commercial segment which is significantly countered by the low industrial sales and economic tightening cycle. The low industrial revenue is driven by dramatic declining energy usage of chemical sector and housing market clients. According to the company’s management, a 1% change in industrial revenue has an impact of only approximately $20 million, whereas a 1% variation in residential and commercial sales has an impact of more than $40 to $50 million. This shows that the net position of the company might be positive as the company is still experiencing a strong demand in the residential and commercial segments.

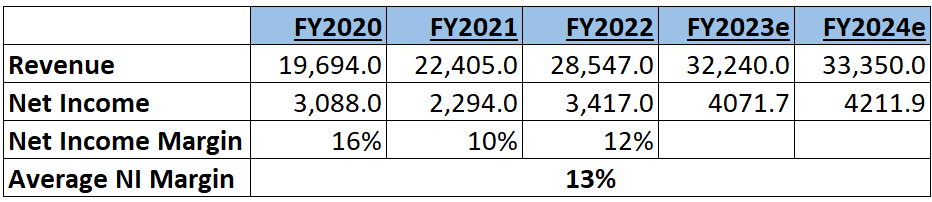

After considering all these factors, I think the company might experience a slight decline in revenue in FY2023 and FY2024 due to strong demand in residential & commercial segment and the acquisition of Solar Facilities of South Cheyenne & Millers Branch. According to Seeking Alpha data, the company’s revenue might be $32.24 billion and $33.35 billion in FY2023 and FY2024, respectively. After considering acquisitions and the net impact of residential and industrial sales, I believe Seeking Alpha’s estimates are accurate. The company’s 3-year average net income margin is 13%. I believe the company can maintain net income margin of 13% in the coming period as demand in the residential and commercial segments is still strong. The revenue estimate of $32.24 billion and $33.35 billion & net income margin of 13% give EPS estimates of $3.8 and $3.9 for FY2023 and FY2024, respectively.

Revenue and Net Income Estimates (Value Quest)

{kind=link}

Acquisition of Solar Facilities of South Cheyenne and Millers Branch

The global demand for renewable energy, particularly in the electricity sector, is rising significantly due to the aim of achieving net zero carbon emissions. In 2022, the electricity capacity additions experienced a record growth of about 340 GW . This growth is also fueled by supporting governmental policies such as the Inflation Reduction Act in the USA which has increased investment in energy transition. As per the International Energy Agency, renewable capacity additions are projected to surge by 107 Gigawatts, which can be the largest growth ever totaling above 440 GW in 2023 globally. In the second quarter of 2023, the US solar sector added 5.6 gigatonnes-direct current ((GWDC)) of capacity, up 20% Q2 2022. It is expected to reach 375 GWdc by 2028.

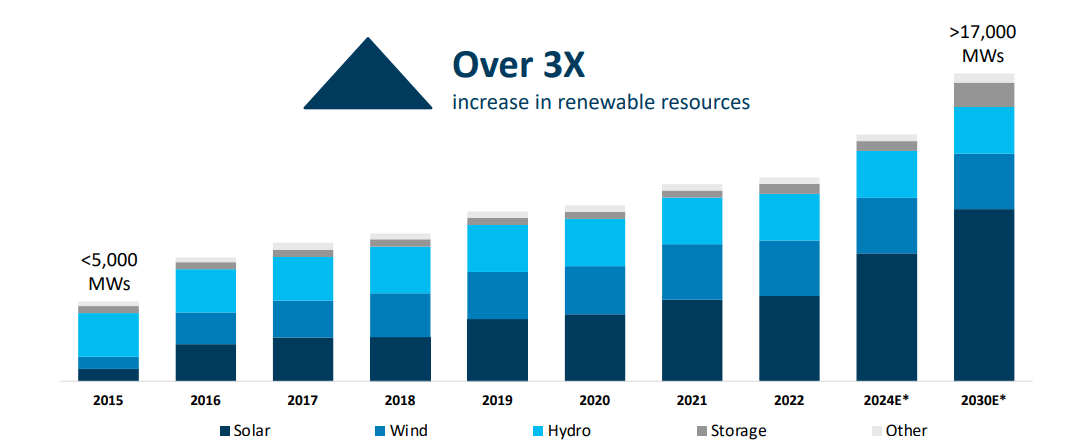

All these positive trends in the industry have created opportunities for the participants. Identifying these growth prospects, SO has announced the acquisition of the South Cheyenne Solar Facility in Wyoming. After this acquisition deal, the company’s solar electricity generation will rise to 2740 MW of solar generation. This will significantly help the company increase its renewable portfolio of clean-generating assets from California to Maine. It is expected to be operational in the first quarter of FY2024. This acquisition can generate approximately $600K in revenue annually as similar projects in past have generated revenue in same range. The quantitative impact of this project might seem relatively small as compared to its current revenue. However, I believe the long term impact of this acquisition might be significant as it can help it strengthen its wholesale business, expand its footprint in Wyoming, and make SO strongly positioned in the market by leveraging its increased renewable portfolio which can facilitate it to serve additional customers and increase its market share by addressing the rapidly growing industry demand. As per my analysis, acquiring such facilities can help the company enter long-term contracts and increase its portion of stable revenues by adding large customers to its portfolio. The existing customer base of the company is highly vast and I think this expansion can also give it a competitive advantage by creating a robust customer base.

In addition, it has also announced the acquisition of Millers Branch Solar Facility , which is a 200 MW facility, in the initial stage of development. The project can be operational from the fourth quarter of 2025. Further after the commencement of operations, Thermo Fisher Scientific will buy the 200 MW facility's electricity and renewable energy credits under a 20-year virtual power purchase agreement, which will be utilized to assist them in meeting its goal of net zero electricity by 2050. I believe this acquisition can also highly benefit the company by generating a stable revenue flow as SO has 20-year purchase agreement with the Thermo Fisher. This expansion can also be beneficial for the long term in creating additional revenue-generating opportunities for the company as it has the potential capacity to expand up to 500 MW which can help it to serve more customers. I believe with the assumption of South Cheyenne's revenue generation ($600k), Miller Branch's solar facility's potential capacity (which is 3.34 times bigger than capacity South Cheyenne's facility) can generate $2 million annual revenue.

Increase in Renewable Resources (Investor Presentation: Slide No: 18)

{kind=link}

Dividend Yield

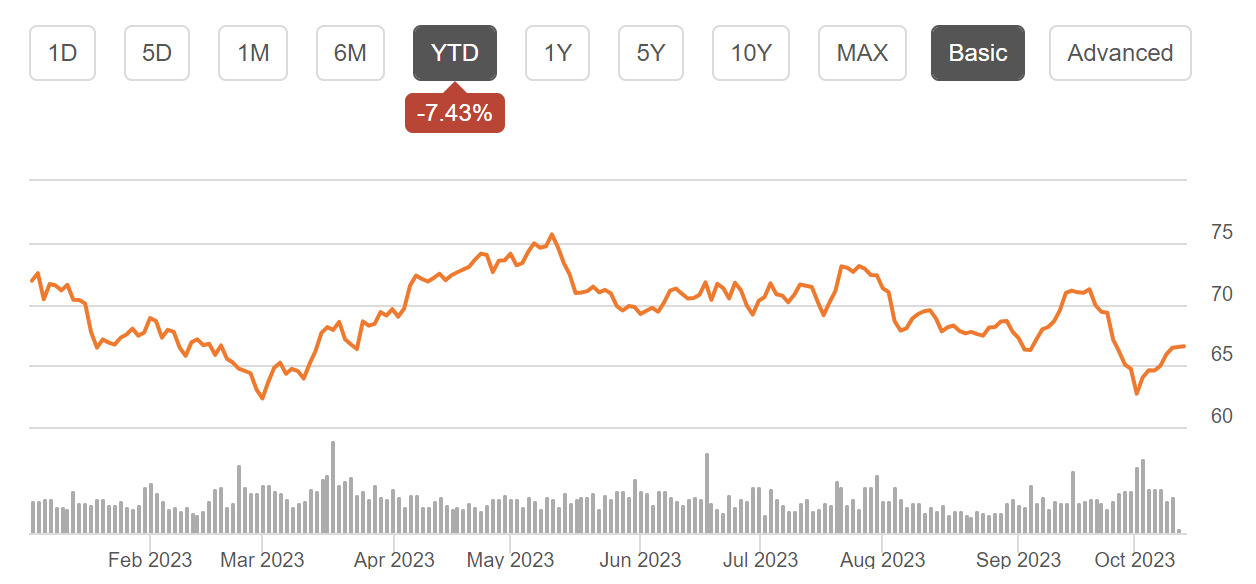

The company’s share price has declined from $71.9 to $66.4 which is a drop of 7.65% in ten months. The company’s valuation has been diminishing since last year due to a significant rise in the yield from risk-free assets. Currently, treasuries are offering yields of 4.63% and 5.01% on 5-year and 2-year bonds, respectively and sector median dividend yield of the utility sector is 4.18%. The rising treasury yields (yield of risk-free asset) make utility companies unattractive for risk-averse investors. Once the Fed’s tightening cycle starts moving towards its end, risk-averse investors can start investing in utility businesses to earn stable dividend yields.

Share Price History of SO (Seeking Alpha)

{kind=link}

SO has been paying dividends for last 33 years consecutively. The company has experienced consistent growth in its dividend payout which indicates its healthy positioning. It has increased its dividends for the 22 consecutive years since FY2002. The company’s long history of dividend payments shows that it is paying stable dividends in all economic conditions. In FY2022 the firm paid cash dividend of $0.66 in the first quarter. It paid $0.68 in each of the next three quarters. This dividend payout totaled $2.70 per share annually. The dividend yield on this payment was 4.07% compared to current share price of $66.4. It paid a $0.68 dividend in the first quarter of FY2023. It raised its payout to $0.70 in the second and third quarters. Observing the company's strong cash positions, I believe it can maintain its quarterly dividend of $0.70 in the last quarter as well which can make the annual dividend $2.78, representing a forward dividend yield of 4.19% compared to the current share price. As per my analysis, the company’s strong execution of its expansionary plans by acquiring solar facilities can help it increase its cash flows and grow its dividend payout in the future. The company’s forward dividend yield is 0.87% higher than the sector median dividend yield of 4.18%. SO’s 4-year average dividend yield is 4.04% which is 19.02% higher than sector median 4-year average dividend yield of 3.39%. The company’s 5-year average dividend yield is 4.22%. This appealing dividend yield makes the firm an attractive stock to hold in the portfolio. It can also be a good investment for risk-averse and retired investors who are looking for a stable regular income.

What are the Main Risks Faced by SO?

Rising Long-Term Debt:

The company has been experiencing a significant rise in long-term debt since FY2015. Currently, SO's long-term debt stands at $55.37 billion which is 76.4% of the company's market capitalization of $72.46 billion. The rising interest rates in the market can adversely affect the company's finances as it can significantly affect SO's interest expense which can put negative pressure on the profit margins of the company. If the interest rates continue to rise in the coming period, it can negatively impact the financial condition as it has huge long-term debt.

Long-term Debt Trend of SO (Seeking Alpha)

{kind=link}

Dependency on Global Supply Chain:

The company’s operations highly depend on the global supply chain to obtain materials, equipment, and other resources. The delivery of components and equipment that are necessary for the company’s operations can be impacted by global supply chain disruptions. If the global supply chain gets disrupted due to international tensions and regional conflicts, it can interrupt the company’s operations and can even lead to increased prices of essential elements which can further contract the company’s profit margins by increasing its cost.

Valuation

I am estimating EPS of $3.9 for FY2024 after considering tremendous growth in the renewable energy sector. These industry tailwinds have created opportunities for the companies operating in this sector. I believe the company is strongly positioned to capture the growing demand in the market as it has recently made two acquisitions which can help it to increase its market share and add more customers to its portfolio by leveraging its increased capacity of renewables. SO is also witnessing robust demand in the residential & commercial sectors which can outpace impacts of slow demand in the industrial segment.

If we divide EPS estimate of $3.9 with current share price of $66.4, we will get forward PE ratio of 17.02x. The comparison of PE ratio of 17.02x with sector median of 17.64x stipulates that SO is fairly valued. The company's primary competitors are:

{kind=link}

The industry average P/E ratio of electric utility industry is 16x. The comparison of industry P/E ratio of electric utility industry with the forward P/E ratio of SO indicates that the company is slightly overvalued. However, all the companies in this industry are significantly affected by the rising interest rates in the market. In the past, higher dividend-paying companies have frequently shown a significant connection between their payout rate and long-term interest rates. All else being equal, rising long-term rates of interest could result in considerable share price reductions for electrical utility companies. Currently, treasuries are offering yields of 4.63% and 4.62% on 5-year and 10-year bonds, respectively. The rising interest rates provide investors opportunity to earn the strong and stable income from risk-free assets which leads to decrease in the share prices of high dividend paying companies as people move their money from these stocks to risk-free assets. Therefore, all the companies in the electric utility industry are facing downward pressure which has resulted into low share prices and low P/E ratios. The United States Federal Reserve has announced that the interest rates might stay in the range of 5.25% to 5.5% throughout 2024 which shows that the electric utility might continue to face this negative pressure in the coming period. After considering SO's growth factors and industry P/E declines due to rising interest rates, I think the company is currently fairly valued.

Conclusion

SO is facing a surge in demand thanks to growing need for renewable energy. In my opinion the company is well positioned to meet this demand because it has recently acquired two facilities. This acquisition will allow SO to attract customers and boost its profits by utilizing its expanded portfolio of resources. However, it's worth noting that any disruptions in supply chain could have impact on SO’s operations and potentially affect its profitability. SO offers an appealing dividend yield and has a longstanding history of regular dividend payments making it an appealing stock for those seeking stable and regular income. Furthermore, considering the current valuation of the stock and comparison of its PE ratio with industry average, the company is fairly valued and investors can hold this stock for the stable dividend. Taking all these factors into consideration I recommend giving SO a hold rating.

For further details see:

Southern Company: Hold This Stock For Stable Dividend Yield