SO - Southern Company Looks Interesting Yielding Over 4% Down 19% From Its Highs

2023-09-29 08:45:00 ET

Summary

- Utilities have become less popular due to the high yields offered by risk-free assets like treasuries and CDs.

- The Southern Company, a top-tier utility, has seen its shares decline but may become more attractive as rates start to decline.

- SO has a long history of generating dividends and is projected to have significant earnings growth, making it a reasonable investment option.

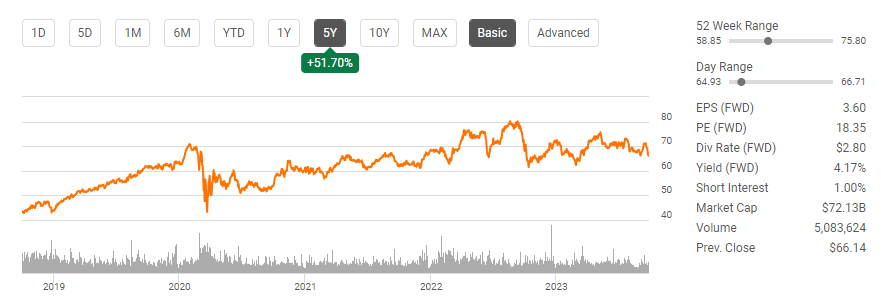

Utilities haven't been exciting, with Treasuries yielding over 4.5% on the 10-year and over 5% on the 2-year. The demand for utility companies has significantly diminished as the yield from risk-free assets has overshadowed dividend-oriented utility companies. Utilities used to be the flight to safety as utility companies have a stigma for stability due to their regulated industry and a haven for generating income. When you can generate over 4.5% on a 10-year note and exceed 5% on everything up to a 2-year note backed by the United States government, cash gravitates toward treasuries and CDs rather than taking on equity risk to generate a lower yield. Shares of The Southern Company ( SO ) have declined by almost 19% since exceeding $80 in the summer of 2022, pushing the yield past 4%. The Southern Company is the 2nd largest holding in the Utilities Select Sector SPDR Fund ETF ( XLU ) and has a dividend history that spans 76 years. While risk-free assets have a yield that exceeds The Southern Company, I believe now is an interesting time to consider this top-tier utility. I plan on adding to my position as we're headed toward the end of the Fed's tightening cycle, and eventually, utilities such as The Southern Company will once again generate a larger yield than risk-free assets.

{kind=link}

Utilities could continue to decline, but I see them becoming more popular next year and certainly in 2025

Utilities have never really appealed to growth investors as they operate in a heavily regulated industry. The prospects for growth are limited to the opportunities investors can find from technology companies. While utilities such as The Southern Company don't typically grab headlines, they have been an appealing sector of the market for dividend-focused investors. Utilities provide critical infrastructure and lack traditional competition as this sector is regulated by state, federal, and local agencies. In a yield-starved environment, utilities offered an alternative to low-yielding, risk-free assets, but with the Fed raising rates, money has found its way into treasuries, and utilities have become less exciting for now.

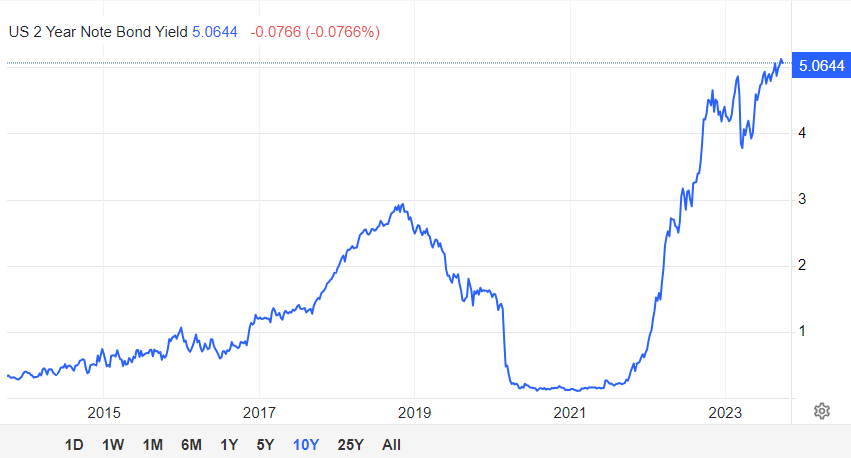

Over the past decade, the 2-year note had never yielded over 3% until the recent rate hikes occurred. The 2-year note spent the majority of its time under 2% and briefly rose above 2% in 2018, only to fall under a 2% yield in 2019. Since the Fed's tightening cycle started, the two-year yield has seen its increase from 0.22% in September of 2021 to 5.06% in September of 2023. Many income investors don't mind taking on risks from equities to generate yield as they are more focused on generating income rather than capital appreciation. When you can get 5% on your money risk-free, the idea of taking on risk to generate yield in the public markets isn't as attractive. Since utilities aren't going to win in a competition against the likes of Apple (AAPL), Tesla (TSLA), or Nvidia ( NVDA ) for capital being allocated for capital appreciation, these investments have suffered during the rising rate environment.

{kind=link}

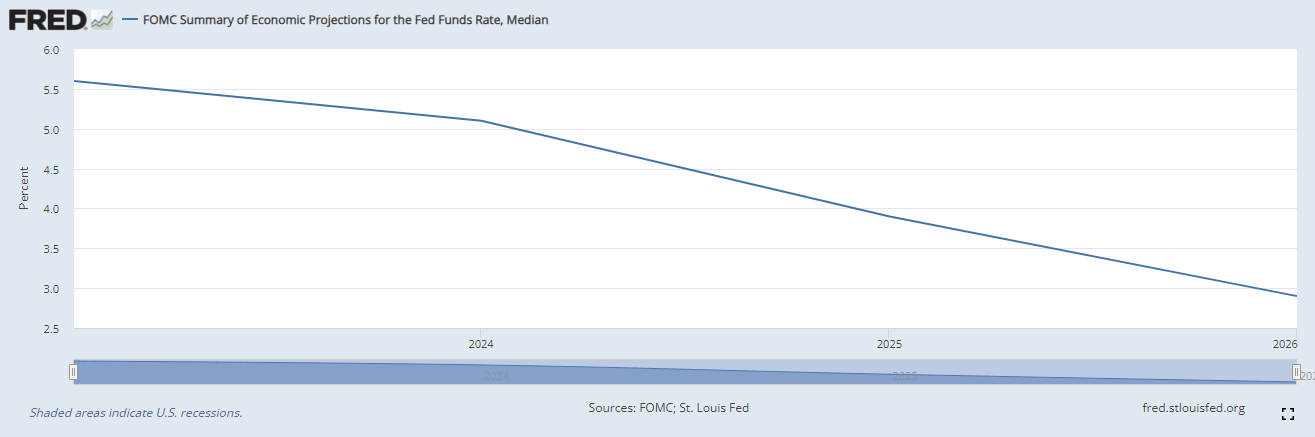

At the latest FOMC meeting, Jerome Powell indicated once again that the Fed will keep rates higher for longer. After the speech, the St. Louis Fed adjusted their projection for rate cuts. The St. Louis Fed is projecting that rates will be higher than anticipated in 2024, but we will start to see some rate cuts, which will eventually end up in the 2.9% area in 2026. Maybe we will see one more hike in November, but the end of the cycle is near, and while the projected cutting cycle has been pushed out, it's still expected to start in 2024.

{kind=link}

Whether we get another hike or not, I think utilities are going to start looking much more interesting going into the end of 2023. Capital has been locked up in short-duration CDs and treasury notes on the way up earnings 4% - 5.5% and a portion of them will be maturing as rates start to decline. As the Fed eases rates, the yields will fall on risk-free assets, making dividend stocks more attractive. My speculation is that strong utilities such as The Southern Company will come back into favor as short-duration yields decline. I think there will be a large segment of investors who locked up capital in risk-free assets, redeploying that capital into equities because there is a common theory that equities will rise as capital flows in from risk-free assets. When the 2-year gets back into the low 4% range, some investors will find it less attractive than The Southern Company because the dividend from Southern Company will continue to grow as rates decline.

The Southern Company has delivered 76 years of generating dividends for its investors

Income investors aren't just looking for yield; they're looking for reliability. The Southern Company has paid a dividend for 76 consecutive years and increased its dividend on an annual basis for the last 22 years. The Southern Company has been a staple of dependability while working its way toward becoming a Dividend Aristocrat. The appeal of generating a fixed amount of income will still be front and center for many investors as rates start to ease, and I believe the utility sector will be one of the primary areas investors look for yield as we move into an easing environment.

{kind=link}

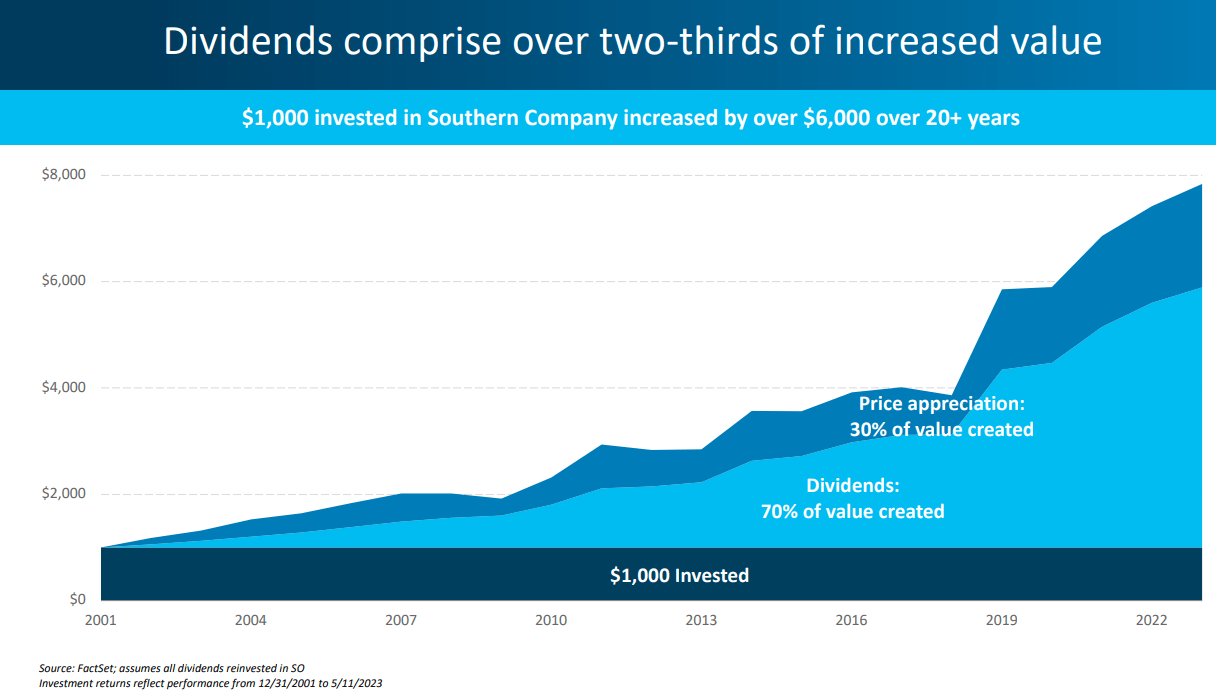

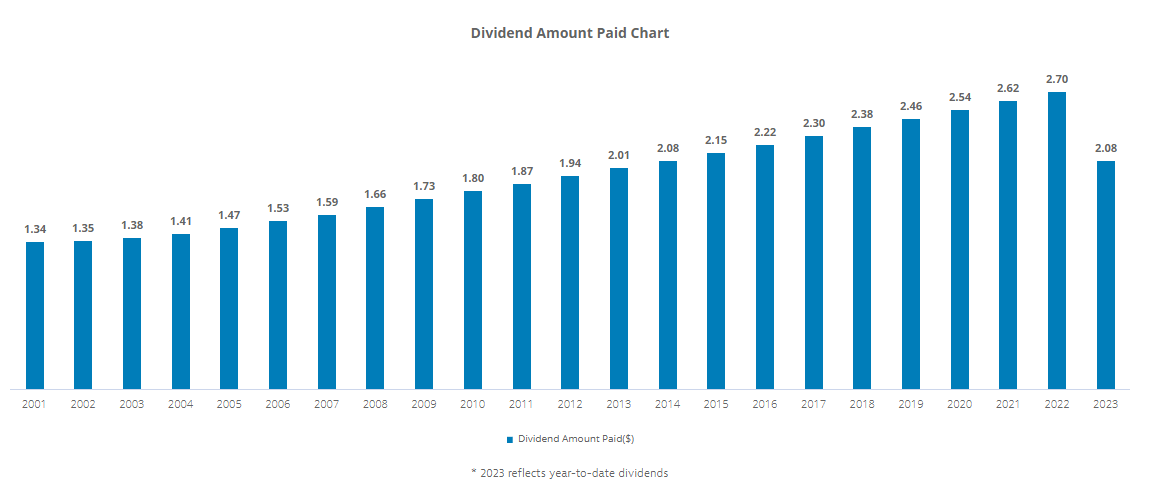

Since 2001, The Southern Company has paid $44.66 in dividends to its shareholders. These dividends have accounted for roughly 70% of the value created from its shares. The growing dividend has been a critical component, making a $1,000 investment grow by over $6000 over the past 22 years. Over this period, the dividend has increased by $1.46 (108.96%) from $1.34 to $2.80. Over the past 5 years, the dividend growth rate has been 3.18%, and the current yield is 4.17%. The Southern Company is a quintessential candidate to thrive as money comes off the sidelines due to the stability of its business and the growing income being generated. Sometimes boring companies can generate significant upside, and The Southern Company has proven that no matter what the economic cycle brings, it's an income-generating machine.

{kind=link}

The Street is projecting significant earnings growth for The Southern Company

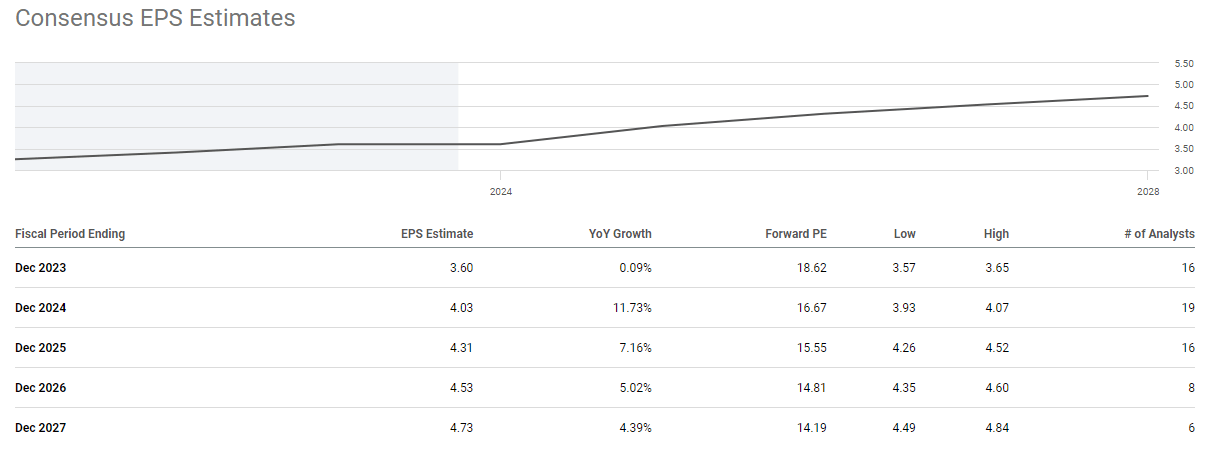

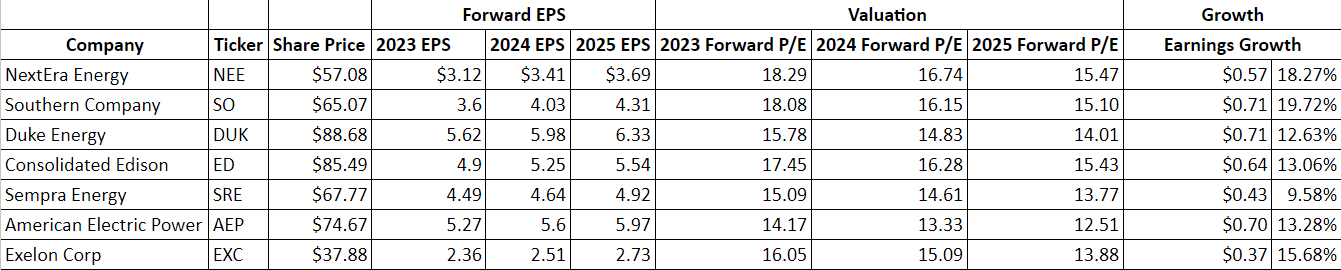

There are currently 15-20 analysts providing projections for The Southern Company's EPS estimates through 2025. While regulators protect its business, I am happy to see that the Street sees growth on the horizon. This is important as it will support future dividend growth and investing in future projects for them. The Street is expecting The Southern Company to generate $3.60 of EPS in 2023 and see 19.72% EPS growth through 2025. This is interesting because this puts their 2023 forward P/E at 18.08x, and its 2025 P/E at 15.1x. I am happy to pay under 20x this year's earnings and around 15x 2025's earnings for The Southern Company as its EPS and dividend continue to grow.

{kind=link}

I compared The Southern Company to several peers, and the valuation looks reasonable.

- NextEra Energy ( NEE )

- Duke Energy ( DUK )

- Consolidated Edison ( ED )

- Sempra Energy ( SRE )

- American Electric Power ( AEP )

- Exelon Corp. ( EXC )

The average utility company that I looked at will see 14.6% EPS growth from 2023 through 2025. The Southern Company has the largest EPS growth rate from its peers at 19.72%. They trade at the top of the range from a P/E perspective, as the peer group has an average 2023 forward P/E of 16.42x and a forward 2025 P/E of 14.31x. The Southern Company is trading at 18.08x 2023 earnings and 15.1x 2025 earnings. While these are low forward P/E levels compared to the market, I am comfortable with where The Southern Company is trading, given its history and value created over the past 2 decades.

{kind=link}

There are some risks to this investment thesis even though The Southern Company operates in a regulated industry

While The Southern Company operates in a regulated industry and everybody needs electricity, there are several risks that are outside of their control. The first risk to this investment thesis is from a value perspective. If the economy doesn't slow down, earnings expand in Q3, and projections for Q4 increase, then we could see the Fed not only raise rates in November but become more hawkish. The Fed isn't necessarily trying to cause a recession, but if a recession is a byproduct of increasing rates to reduce inflation, I don't think it will be a large enough deterrent to stop the hikes. The Fed was wrong about inflation being transitory and missed the boat on starting to increase rates, so I don't see them putting themselves in a position to have inflation rise again on their watch. If the Fed raises rates and keeps them higher for longer, it could extend the era of risk-free assets yielding over 5% and push them near 6%, which would cause even less of a reason to take on equity risk to generate income. This would hurt a recovery in utilities and make them less attractive in 2024.

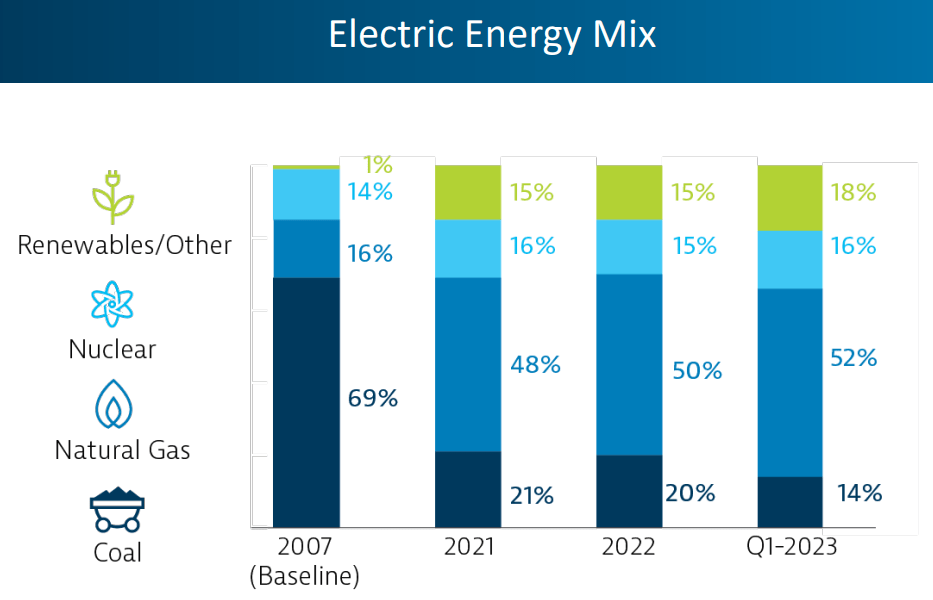

The Southern Company is one of the only utility companies to operate nuclear plants, and 16% of their energy comes from nuclear energy. The Southern Company is subject to complex and comprehensive federal, state, and other regulations. As regulation changes, it could create situations where they would need to address aspects of their business immediately or even curtail operations in certain areas. While changes to any business come at a cost, if new regulation impacts nuclear and additional safeguards are needed, this could be a large uplift for The Southern Company and cut into their projected EPS growth. Being protected by regulations is great, but being at their mercy creates a double-edged sword as it could come at a large financial cost.

{kind=link}

Conclusion

I have some capital in risk-free assets, and while I would consider rolling this capital into another short-duration CD or bond, I don't see this lucrative environment sticking around much longer on risk-free assets. I do believe that money is going to come off the sidelines and enter quality dividend companies that have a long history of paying dividends with annual dividend increases. I see The Southern Company as one of the beneficiaries of a changing investment landscape for income investors, as utilities will be at the top of the list as money comes back into the market. With 76 years under their belt of paying a dividend and 22 years of increasing their dividend, The Southern Company is certainly an outlet for income investors who want to get back into the market as the Fed's tightening cycle ends. I plan on adding to my position in The Southern Company as it's one of the largest public utilities in the country, and I think it will be a winner in 2024.

For further details see:

Southern Company Looks Interesting Yielding Over 4%, Down 19% From Its Highs