SBSI - Southside Bancshares: Outlook Of Subdued Earnings Growth Appears Priced-In

Summary

- The management’s 9% loan growth target appears too ambitious. I’m expecting this target to be missed.

- I’ve reduced my margin estimate for 2023 following last quarter’s disappointing performance.

- The December 2023 target price suggests a small upside from the current market price. Further, SBSI is offering a modest dividend yield.

Earnings of Southside Bancshares, Inc. ( SBSI ) will likely increase slightly this year on the back of low loan growth. Meanwhile, the margin will likely remain unchanged this year following a mixed shift in the balance sheet positioning. Overall, I'm expecting Southside Bancshares stock to report earnings of $3.38 per share for 2023, up by 3.7% year-over-year. Compared to my last report on the company, I've tweaked downwards my earnings estimate as I've reduced my margin estimate. The December 2023 target price suggests a small upside from the current market price. Therefore, I'm maintaining a hold rating on Southside Bancshares.

Loan Growth to Decelerate but Remain Above the Historical Average

Although the loan growth rate declined sequentially in the fourth quarter of 2022, it remained quite impressive. The portfolio grew by 2.1% during the quarter, taking the full-year growth to 13.9%, which is well above the historical average. The growth rate also beat my expectations given in my last report on Southside Bancshares. Management is targeting loan growth of 9% this year, as mentioned in the conference call .

In my opinion, there's a good chance Southside Bancshares will miss the 9% target this year. Firstly, loan growth should be substantially lower this year compared to 2022 because average interest rates will be much higher this year relative to last year. Management also mentioned in the conference call that the loan pipelines are currently not as strong as they were this time last year. Furthermore, the regional unemployment rate is currently worse than the national average. Southside Bancshares mostly operates in the state of Texas, which reported an unemployment rate of 3.9% for December 2022.

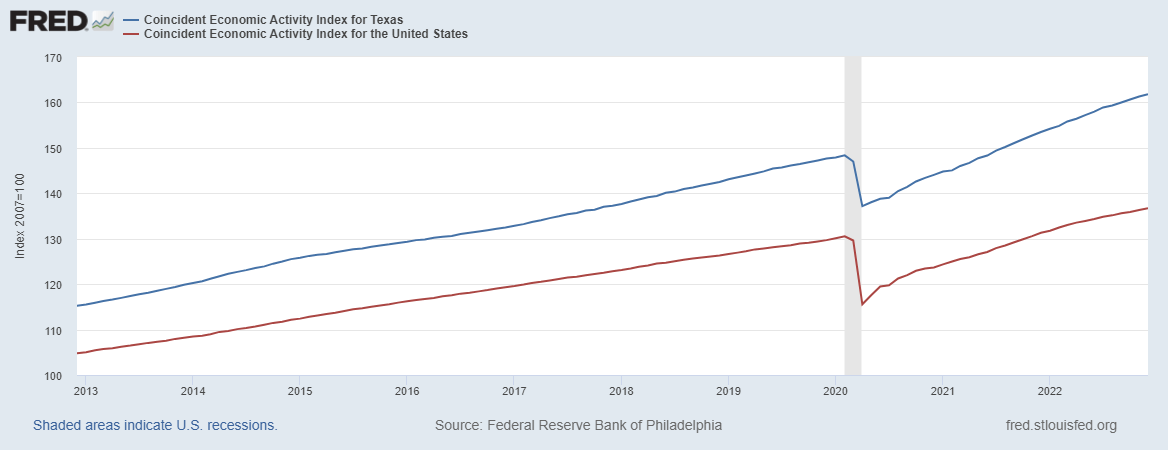

Despite the factors given above, I think loan growth will remain at an elevated level compared to previous years. This is because recent data shows that the economic activity in Texas is quite robust, especially when compared to the national average (see the difference in slopes of the trendlines below).

{kind=link}

Considering the factors given above, I'm expecting the loan portfolio to grow by 4% in 2023. Further, I'm expecting deposits to grow in line with loans. The following table shows my balance sheet estimates.

| Financial Position |

| FY18 |

| FY19 |

| FY20 |

| FY21 |

| FY22 |

| FY23E |

| Net interest income |

| 172 |

| 170 |

| 187 |

| 190 |

| 212 |

| 233 |

| Provision for loan losses |

| 8 |

| 5 |

| 20 |

| (17) |

| 3 |

| 4 |

| Non-interest income |

| 41 |

| 42 |

| 50 |

| 49 |

| 41 |

| 44 |

| Non-interest expense |

| 120 |

| 119 |

| 123 |

| 125 |

| 130 |

| 145 |

| Net income - Common Sh. |

| 74 |

| 75 |

| 82 |

| 113 |

| 105 |

| 109 |

| EPS - Diluted ($) |

| 2.11 |

| 2.20 |

| 2.47 |

| 3.47 |

| 3.26 |

| 3.38 |

| Source: SEC Filings, Author's Estimates (In USD million unless otherwise specified) |

In my last report on Southside Bancshares, I projected earnings of $3.40 per share for 2023. I've slightly revised downwards my earnings estimate because I've reduced my margin estimate.

My estimates are based on certain macroeconomic assumptions that may not come to fruition. Therefore, actual earnings can differ materially from my estimates.

Maintaining a Hold Rating Due to a Moderate Total Expected Return

Southside Bancshares is offering a dividend yield of 3.7% at the current quarterly dividend rate of $0.35 and an annual special dividend of $0.04 per share. The earnings and dividend estimates suggest a payout ratio of 43% for 2023, which is below the five-year average of 48%. Therefore, the dividend appears secure. Southside usually increases its dividend only once a year, so it's unlikely that the company will raise dividends again this year.

I'm using the historical price-to-tangible book ("P/TB") and price-to-earnings ("P/E") multiples to value Southside Bancshares. The stock has traded at an average P/TB ratio of 1.98 in the past, as shown below.

| FY18 |

| FY19 |

| FY20 |

| FY21 |

| FY22 |

| Average |

| TBVPS - Dec 2023 ($) |

| 17.4 |

| 17.4 |

| 17.4 |

| 17.4 |

| 17.4 |

| Target Price ($) |

| 31.0 |

| 32.8 |

| 34.5 |

| 36.2 |

| 38.0 |

| Market Price ($) |

| 38.8 |

| 38.8 |

| 38.8 |

| 38.8 |

| 38.8 |

| Upside/(Downside) |

| (20.0)% |

| (15.5)% |

| (11.0)% |

| (6.5)% |

| (2.0)% |

| Source: Author's Estimates |

The stock has traded at an average P/E ratio of around 13.3x in the past, as shown below.

| FY18 |

| FY19 |

| FY20 |

| FY21 |

| FY22 |

| Average |

| EPS 2023 ($) |

| 3.38 |

| 3.38 |

| 3.38 |

| 3.38 |

| 3.38 |

| Target Price ($) |

| 38.3 |

| 41.7 |

| 45.1 |

| 48.4 |

| 51.8 |

| Market Price ($) |

| 38.8 |

| 38.8 |

| 38.8 |

| 38.8 |

| 38.8 |

| Upside/(Downside) |

| (1.2)% |

| 7.5% |

| 16.3% |

| 25.0% |

| 33.7% |

| Source: Author's Estimates |

Equally weighting the target prices from the two valuation methods gives a combined target price of $39.80 , which implies a 2.6% upside from the current market price. Adding the forward dividend yield gives a total expected return of 6.4%. Hence, I'm maintaining a hold rating on Southside Bancshares.

For further details see:

Southside Bancshares: Outlook Of Subdued Earnings Growth Appears Priced-In