SSB - SouthState: A Sturdy Institution With Growth Potential But Limited Upside

2023-09-01 12:08:07 ET

Summary

- SouthState Corporation stock hasn't declined as much as that of many other financial institutions since earlier this year.

- This is a testament to its quality and continued growth, but there are downsides to it.

- Uninsured deposit exposure is higher than I prefer and shares are not exactly cheap.

Although I have really come to like the banking sector this year after the bottom fell out in response to the crisis that enveloped the industry in March, not every prospect that I have come across has been all that appealing to me. One particular firm that fits this description is SouthState Corporation ( SSB ). Relative to many of the other players that I have looked at in the space, shares did not fall all that much to begin with. In fact, the maximum decline was only 26.2%. Today, the stock is still down about 11.2% compared to where it ended February of this year at.

Even though the company is quite healthy, I do still believe that exposure to uninsured deposits is too high for my liking. On top of this, shares are nowhere near as cheap as the shares of many of the other players that are currently out there. Given this combination of factors, I have no problem rating the bank a "hold" at this time to reflect my view that shares will probably more or less match the overall market’s performance for the foreseeable future.

Not bad, but not great

Before we get into the fundamental data, it would be helpful to discuss to some extent what SouthState actually does. The financial holding company dates back to 1985. From its humble origins in Florida back then, it grew into a $5.5 billion behemoth with deposits totaling $36.74 billion. As of the end of last year, the institution had 251 branches in its network, touching states that included Florida, South Carolina, Alabama, Georgia, North Carolina, and Virginia. Through these locations, the company provides a wide array of services, such as deposit services, the lending of capital for commercial real estate purposes, the issuance of commercial and industrial loans, various consumer loans, residential real estate loans, and more.

There are other activities that the financial institution is involved in as well. For instance, it operates A correspondent banking and capital markets service operation that caters to nearly 1,200 small and medium-sized community financial institutions across the country. This particular line of business generates revenue on fixed income security sales, fees from hedging services, loan brokerage fees, consulting fees, and more. The company also has a wholly owned registered investment advisor and a full-service broker dealer. The company engages in other activities as well, such as the factoring, invoicing, collection, and other related activities under its CBI Holding Company subsidiary.

{kind=link}

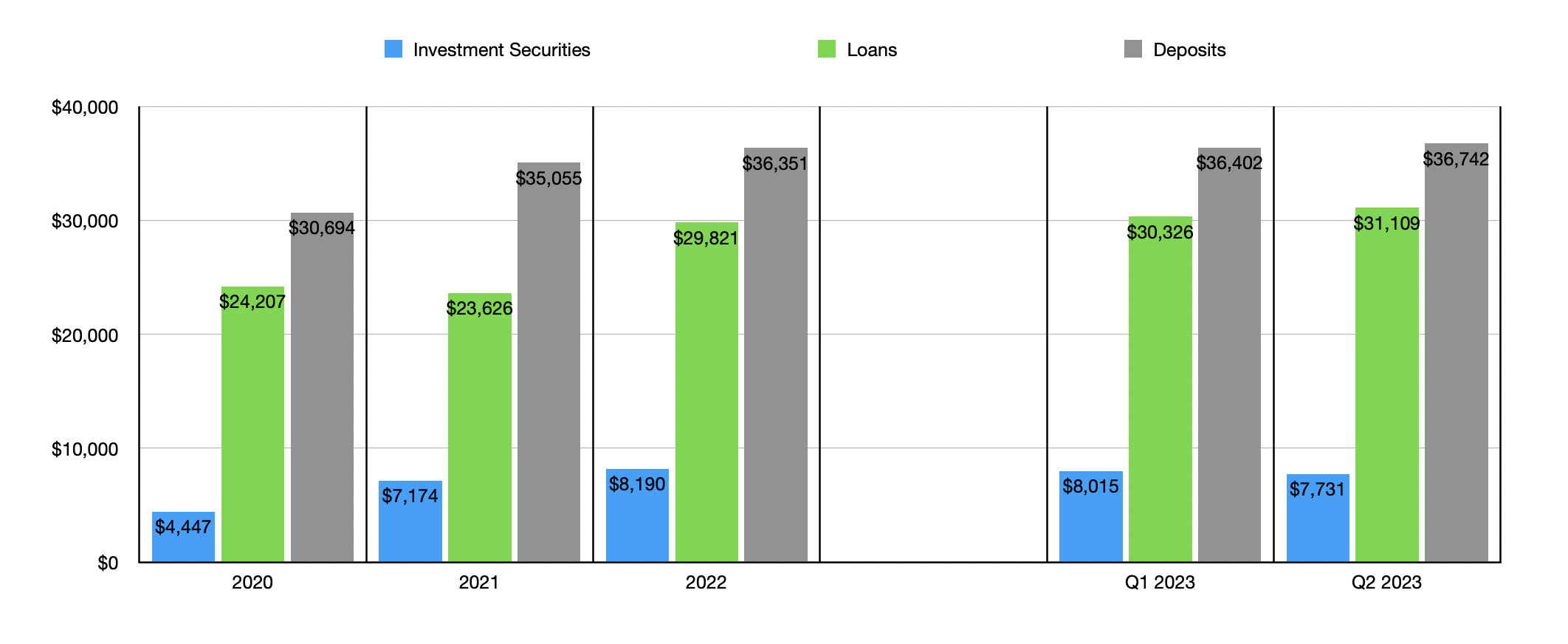

Over the past few years, management has done a good job growing the company's loan portfolio. Loans expanded from $24.21 billion in 2020 to $29.82 billion in 2022. Some of this growth was driven by organic means. However, a big chunk of it seems to be attributable to mergers that the company engaged in. In March of last year, for instance, the company acquired $2.4 billion worth of loans associated with a $657.8 million merger transaction that it engaged in. The great thing is that the value of loans has only continued to grow since the end of last year. By the end of the most recent quarter , they totaled $31.11 billion. This is on a net basis. Gross loans and the sum of loans that are available for sale increase this number to roughly $31.5 billion.

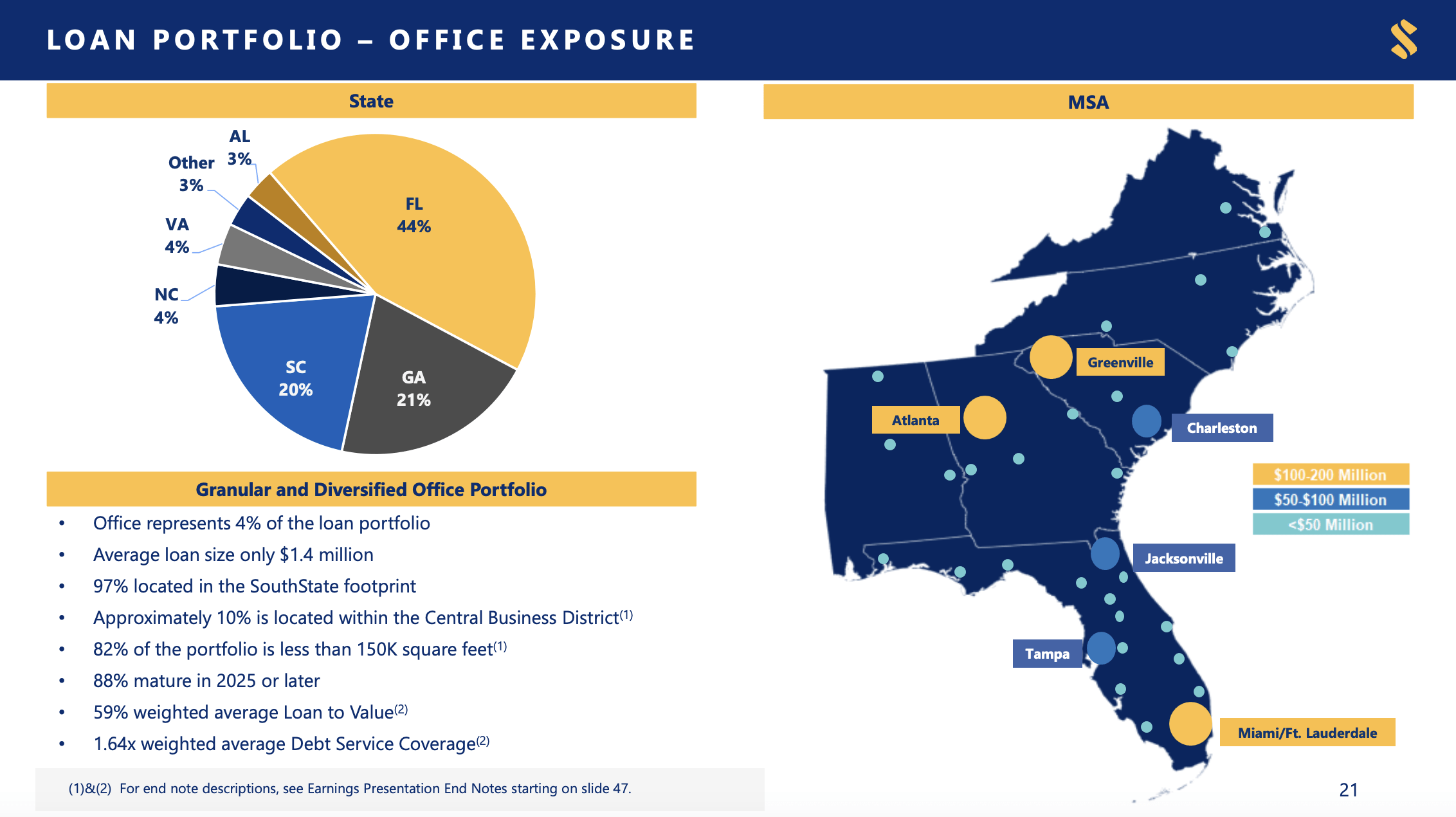

Another one thing that many investors are worried about in this space is the exposure that banks have to office properties. The good news for shareholders is that only about 4% of the company's loan exposure involves these types of assets. 44% of the loans, by value, come from Florida, with another 41% combined coming from Georgia and South Carolina. These are fairly attractive states for business, and the company also benefits from the fact that the weighted average loan to value ratio of these office loans is about 59%. If the bottom falls out on this type of real estate, that probably won't stop the company from taking a hit. But the overall limited exposure to office properties is great to see.

{kind=link}

Good portion of the firm's assets are also invested in various investment securities. This number has also increased as time has gone on. Back in 2020, $4.45 billion of its assets were dedicated to these types of securities. This figure nearly doubled to $8.19 billion by the end of last year. We have seen a decrease since then, but only modestly, with the value of investment securities totaling $7.73 billion as of the end of the most recent quarter. While the loans on the company's books could have varying degrees of risk, most of the investment securities on its books are incredibly safe. 72% by value are in the form of agency mortgage-backed securities. Another 15% falls under treasury, agency, and SBA loans. These are also quite safe. This is followed up by 13% that falls under municipal investments. Those, also, have a degree of safety to them that exceeds many other investment types. But they are not immune from loss. The good news is that 95% of the company's municipal portfolio is rated AA or higher.

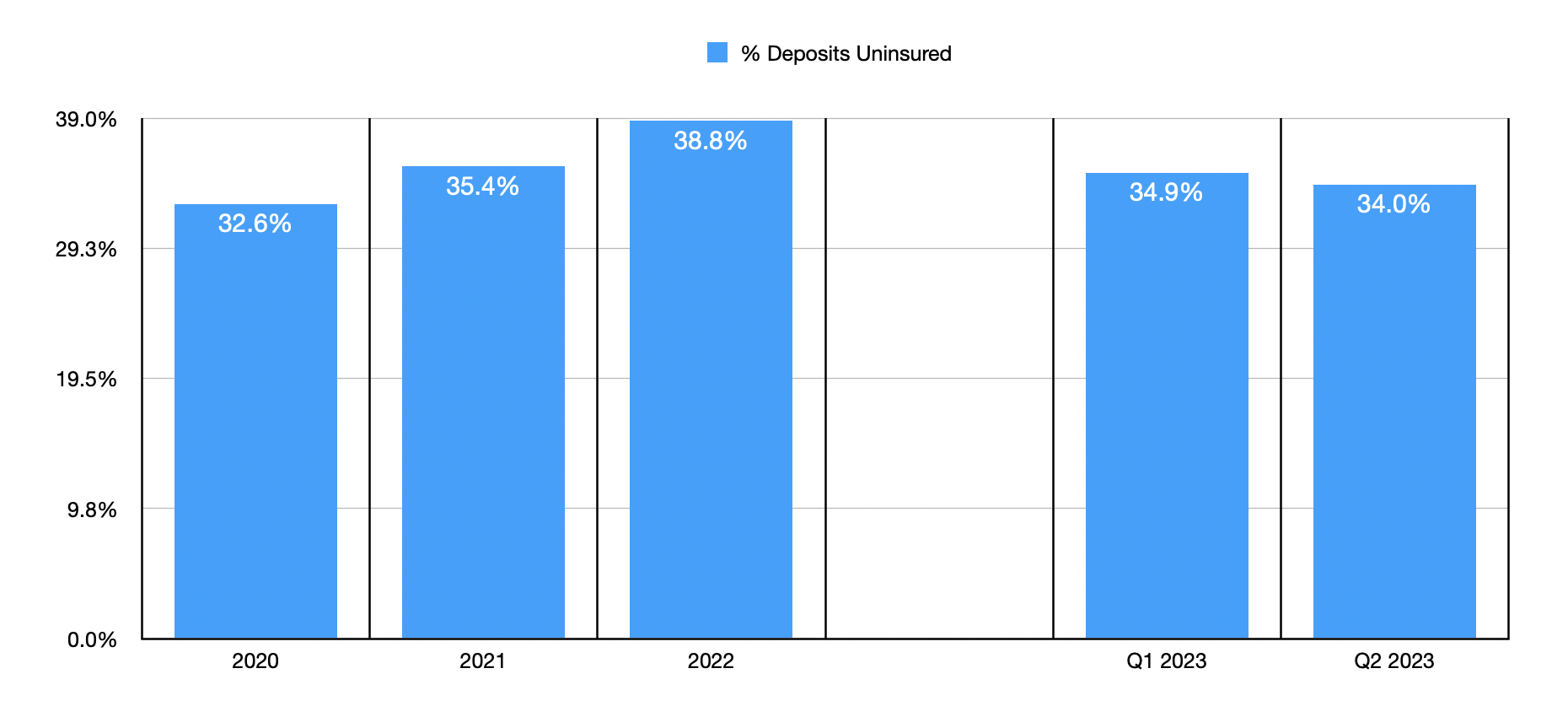

The increase in loans over time has only been made possible by growth in the company's deposits. These grew from $30.69 billion in 2020 to $36.35 billion in 2022. The company didn't even see a drop in the first quarter, with deposits coming out to $36.40 billion for that time before rising to $36.74 billion at the end of the second quarter. We have seen, however, a slight reduction in the percentage of deposits that are classified as uninsured. Total exposure was 38.8% of deposits at the end of last year. Today, that number is closer to 34%. That is still higher than I would like to see though. Generally, I prefer a number south of 30%. But the lower it is, the better.

{kind=link}

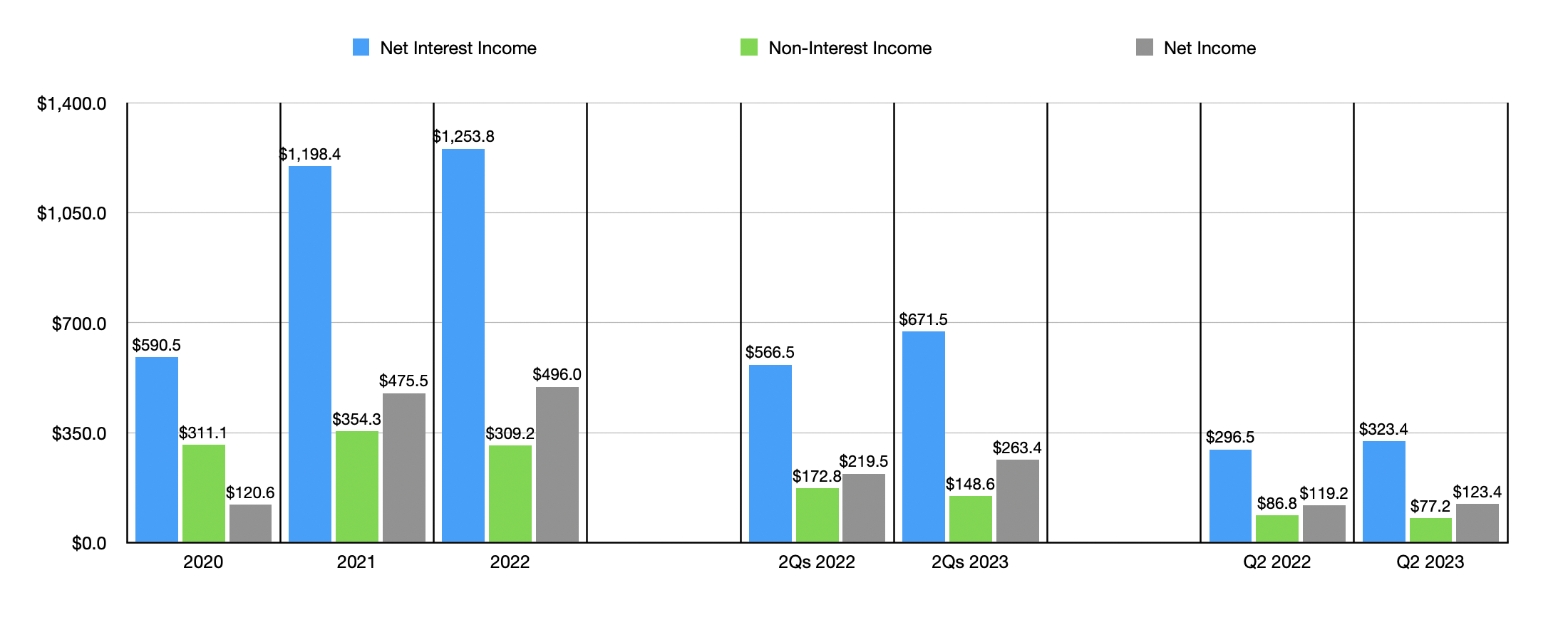

The growth that SouthState has experienced over the years has allowed its overall financial performance to improve drastically. Net interest income expanded from $590.5 million in 2020 to $1.25 billion in 2022. Non-interest income remained virtually flat in the low to mid $300 million range during this time. But even in spite of that, net income grew from $120.6 million to $496 million. Despite difficult market conditions, financial performance has continued to improve this year, with net interest income and net profits both rising in the first half of this year relative to the same time last year and also rising just in the most recent quarter on its own compared to the same time last year.

{kind=link}

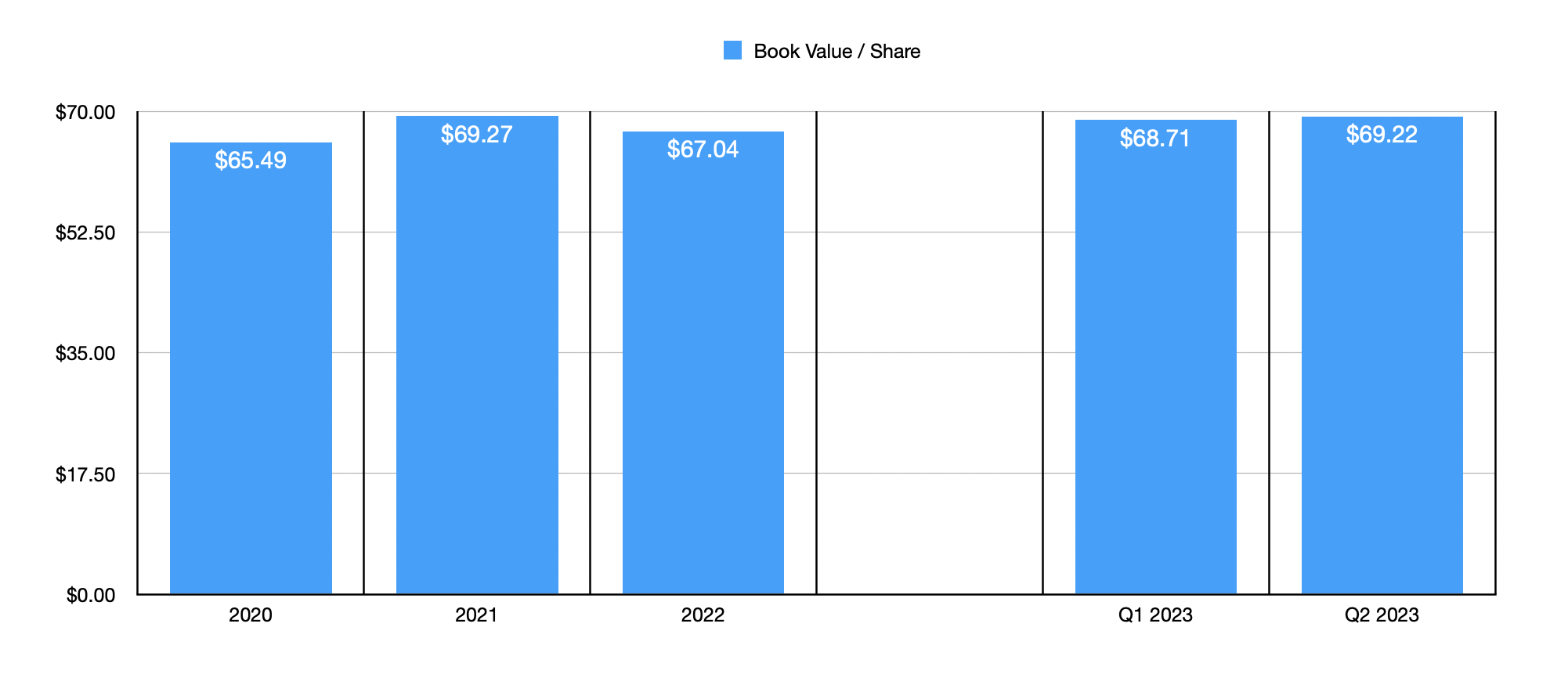

Strong performance has also resulted in modest growth in the company's book value per share. Back in 2020, this metric was $65.49. Today, it is about $69.22. But this brings us to the topic of valuation. With shares currently trading at $71.65, the company is being valued by the market at a 3.5% premium to book value. This is not awful by any means. But I have seen some banks that are healthy that are trading at meaningful discounts to book value. And when it comes to profitability, the same issue applies. Using data from 2022, SouthState is trading at a price to earnings multiple of 11.1. Some of the other banks that I have analyzed are trading at multiples ranging between 5 and 10, with some of these being rather healthy institutions.

{kind=link}

Takeaway

Operationally speaking, SouthState Corporation looks to me a great business. Management has done well to grow the firm, and that growth has continued even during times of chaos. For those focused on a quality operation that is trading at a premium compared to many other players like it, this is definitely a valid prospect. But for those who are more value oriented like myself, SouthState looks to be a bit pricey and its uninsured deposit exposure is higher than I would like it to be. Given these factors, I've decided to rate the company a "hold" at this time.

For further details see:

SouthState: A Sturdy Institution With Growth Potential, But Limited Upside