NFE - Southwest Gas Grapples With Strategic Review And I See Limited Upside

Summary

- Southwest Gas Holdings, Inc. is a diversified gas utility with regulated and unregulated arms. There is a reasonable dividend and a long history of dividend raises.

- Southwest Gas management grapples with a strategic review and options to sell parts of the business while also taking on projects relating to a green future.

- There is some upside available, but given the relatively conservative dividend yield and the strategic review uncertainties, better options than Southwest Gas may exist.

In this article, we examine Southwest Gas Holdings, Inc. ( SWX ) and examine whether this is a buy. The business is diversified and there is some upside at normalized P/E levels, and it is making movements towards green and renewables. But there are also risks and challenges that we discuss.

The company is based in Nevada and has infrastructure and operations that span both regulated and unregulated businesses, providing growth opportunities that solely regulated utilities rarely have. Their regulated operations arm include the main Southwest Gas Corporation, with over two million residential, industrial, and commercial customers in parts of California, Nevada, and Arizona. The recent MountainWest acquisitions ( late 2021 ) added miles of interstate gas transmission over Utah, Colorado, and Wyoming. The Unregulated arm of the business is the Centuri Group that focuses on proving regulated utilities support in building and maintaining networks over North America with their expertise in infrastructure services.

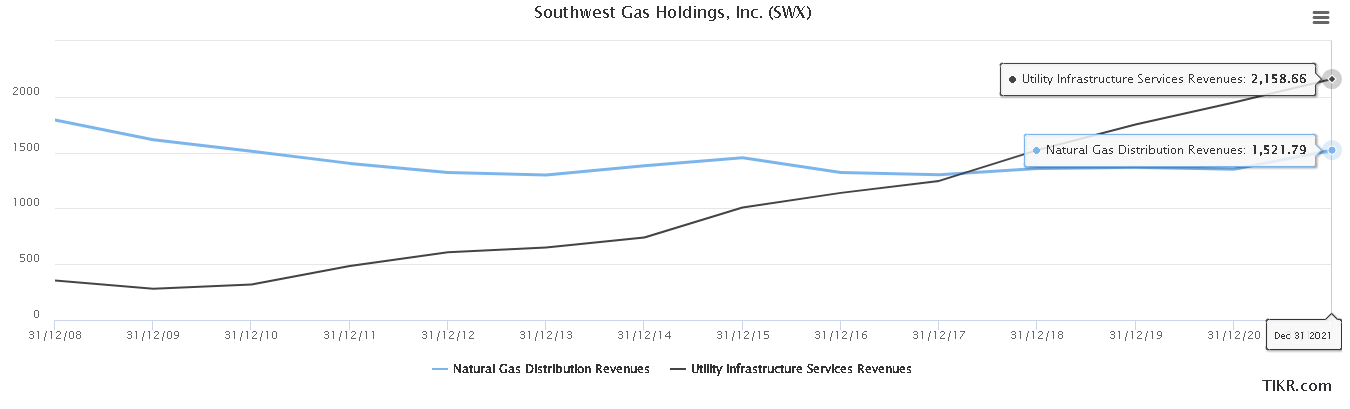

The mix provides crucial growth opportunities, with the utilities infrastructure services of Centuri providing strong growth opportunities, relative to the relatively flat distribution revenues (Figure 1).

{kind=link}

Next, we will look at some challenges facing Southwest Gas, with challenges from the diversified nature of the business, options for spinning off parts of the business, movements towards green power, and a final look at valuation and investment opportunities.

Recent challenges facing Southwest Gas Holdings

Let us dive into some challenges facing the company. They have been facing some profitability issues. Margins appear to be declining (Figure 2) - not falling off a cliff, but certainly, something for an investor to be mindful of and monitor in coming quarters/years.

Figure 2. Declining margins at SWX

Their operational performance seems to suffer at the same time, with other measures of profitability also under pressure (Figure 3). Again, this is something for an investor to be mindful of and monitor. In particular, I find the ROIC measure to be low, to begin with (see a comparison with peers, below) and so further declines are concerning.

Figure 3. Declining profitability at SWX

There are some concerns about the level of debt. The recent MountainWest acquisition required issuing additional equity and had a $2 billion cost and increased leverage. News of the acquisition of Questar Pipeline (then, now renamed MountainWest) led Carl Icahn to call for SWX to drop the acquisition . Icahn has a shareholder. And, of course, he is also keen on spinning off the infrastructure services (including construction) unit and improving the SWX balance sheet.

In October 2021, Fitch placed SWX on Rating Watch Negative following the news of the Questar Pipeline acquisition. In April 2022, Fitch downgraded SWX from BBB+ to BBB.

In 2022, there has been a strategic review , as outlined in the recent earnings call. In essence, which parts of the business should be retained and which spun off? This creates some uncertainty - which we return to later.

Why an income investor would like Southwest Gas Holdings

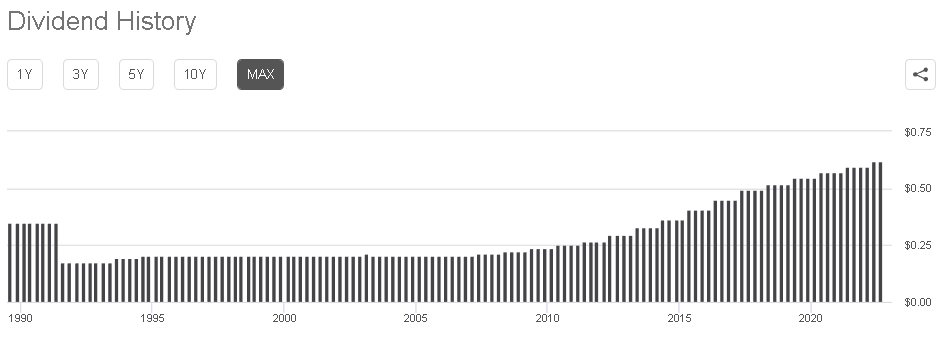

There is a lot to like here for income investors. Seeking Alpha notes SWX has a forward dividend yield of 3.01% and a five-year DGR of 11.74%. There is a very long history of dividend payments and increases in this case (Figure 4).

Figure 4. SWX's dividend increases and history (Seeking Alpha)

{kind=link}

Opportunities for Southwest Gas to explore green options

Southwest Gas operates in a diverse geographic area and this has provided the chance to explore opportunities with hydrogen. They noted on 13 September that they were beginning the Truckee Hydrogen Project :

Over an 18-month period, the Project will test a blend of 5% to 20% hydrogen with natural gas, flowing through plastic and steel pipelines. The hydrogen used in this test is created through the process called electrolysis which separates hydrogen from oxygen in water - a low- to no-carbon generating process that releases oxygen beneficially into our atmosphere and stores hydrogen for use, further reducing GHG emissions. This Project aims to provide critical data that will help the creation of the nation's first hydrogen-injection standard for natural gas operators.

In the short-term, I do not expect these types of projects to make much difference, but the projects will be crucial in the long term. There have been recent moves by some gas utilities to become 'more green' and embrace a lower carbon impact. They have achieved this by including hydrogen in the mix. For example, in early 2022, Chesapeake Utilities ( CPK ) experimented with a hydrogen and gas mix to reduce emissions in power generation. Doing this effectively will be non-trivial from an engineering perspective and much work will be required.

In contrast, SWX has some exposure to renewables through their infrastructure Centuri business, with $125 million of wind power projects lined up.

However, these are still limited steps in the right direction with a multi-year (decade!) timeframe for success. Can Southwest Gas go green - yes, but if this is important to you, would a pure renewable play be a better choice? (See, for instance, my coverage of Atlantica Sustainable ( AY )).

In this analysis, we can see that Southwest is a gas utility and a dividend payer that will never be as green as a pure renewable utility.

Peer comparison

For the comparison with peers, I've used a range of gas utilities:

- Chesapeake Utilities

- New Fortress Energy ( NFE )

- NiSource ( NI )

- New Jersey Resources ( NJR )

- Northwest Natural Holding ( NWN )

- ONE Gas ( OGS )

- RGC Resources ( RGCO )

- Spire ( SR ); I have previously covered Spire.

- UGI ( UGI )

In terms of valuation, Southwest Gas appears to be on the higher end of the valuation. Table 1 includes the top two metrics in each column bolded. We can see that SWX has one of the lowest EV/Sales levels, below the average of 3.8x. The EV/EBITDA is on the high side, coming in fourth at 14.7x, and a reasonable way above the average. The Price / Sales appears more favorable, where SWX again is one of the lower valuations, at 1.2x compared to the average of 1.7x.

Table 1. Southwest Gas compared to peers over multiple valuation metrics

| Ticker |

| EV / Sales (LTM) |

| EV / EBITDA |

| Price / Sales (LTM) |

| CPK |

| 4.8 |

| 13.7 |

| 3.6 |

| NFE |

| 7.6 |

| 41.1 |

| 5.6 |

| NI |

| 4.3 |

| 11.8 |

| 2.3 |

| NJR |

| 2.7 |

| 15.3 |

| 1.6 |

| NWN |

| 3.2 |

| 11.4 |

| 1.6 |

| OGS |

| 3.7 |

| 15.8 |

| 1.9 |

| RGCO |

| 3.9 |

| -22.5 |

| 2.2 |

| SR |

| 3.6 |

| 12.5 |

| 1.6 |

| SWX |

| 2.6 |

| 14.7 |

| 1.2 |

| UGI |

| 1.5 |

| 5.3 |

| 0.9 |

| Summary |

| 3.8 |

| 11.9 |

| 1.7 |

Source: Author, with data from Stock Rover

How does SWX stack up against peers in terms of other metrics? The answer is not particularly favorable most times. In Table 2, I present a comparison of some of the key metrics I focus on. The divine yield is attractive, yes, but is about average for this peer group. SWX has a good track record of dividend payments, while some of its peers do not. The final two columns give me pause for concern; I like the Piotroski F-Score as a fast method of assessing the viability of an investment. Here, SWX is quite lower than its peers with the lowest score of 3, below most of them that sit at 6 or 7. The ROIC is, similarly, lower than peers (as the second lowest value) with UGI having a much higher ROIC value.

Table 2. Southwest Gas compared with peers

| Ticker |

| Div. Yield |

| Consecutive Div. Growth Years |

| Piotroski F Score |

| ROIC |

| CPK |

| 1.7% |

| 10+ |

| 6 |

| 7.0% |

| NFE |

| 0.7% |

| 1 |

| 7 |

| 6.0% |

| NI |

| 3.3% |

| 5 |

| 6 |

| 5.8% |

| NJR |

| 3.3% |

| 10+ |

| 6 |

| 6.2% |

| NWN |

| 4.0% |

| 10+ |

| 5 |

| 5.0% |

| OGS |

| 3.1% |

| 7 |

| 6 |

| 4.1% |

| RGCO |

| 3.7% |

| 10+ |

| 4 |

| -6.7% |

| SR |

| 4.0% |

| 10+ |

| 6 |

| 4.7% |

| SWX |

| 3.1% |

| 10+ |

| 3 |

| 3.3% |

| UGI |

| 3.8% |

| 10+ |

| 6 |

| 13.2% |

| Summary |

| 3.1% |

| 10+ |

| 6 |

| 4.9% |

Outlook for Southwest Gas as an investment

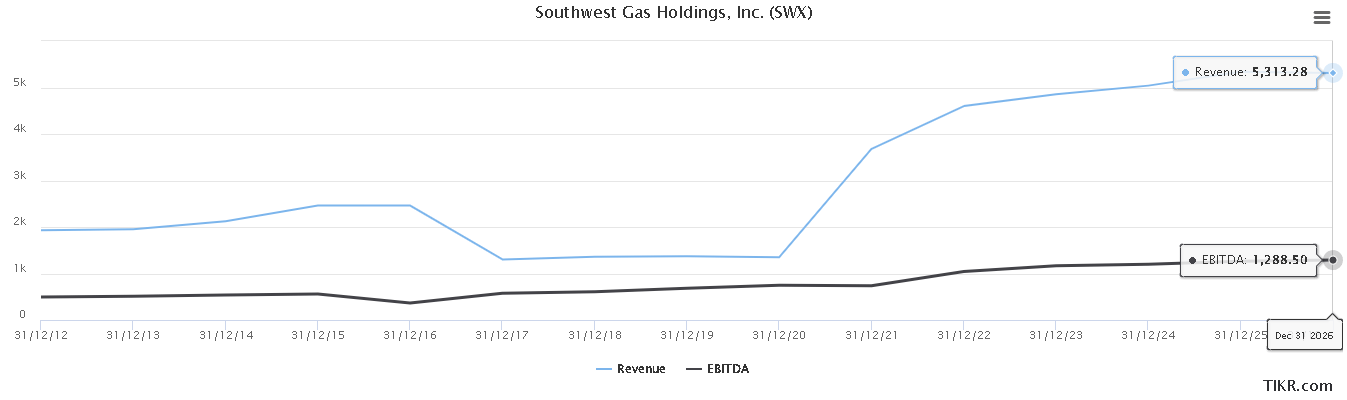

The outlook broadly looks positive for Southwest. Analysts expect revenue to rise in 2022, and then increase at a slower pace in 2023-2026 (Figure 5).

{kind=link}

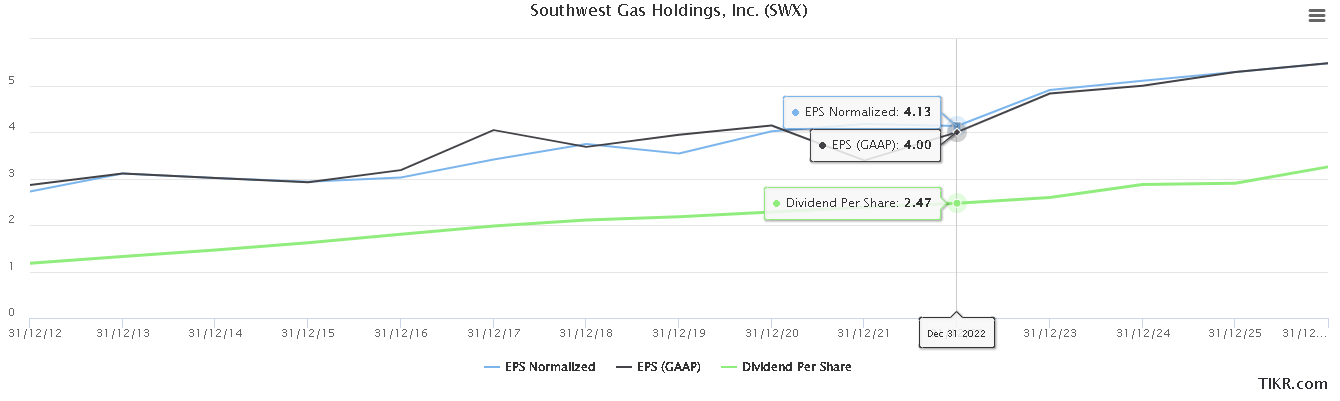

Analysts' expect dividends and EPS rises to continue in coming years (Figure 6). So, as an investment to generate income, SWX looks attractive.

Figure 6. Historic EPS and dividends and analysts' estimates presented beyond the vertical line (TIKR Terminal)

{kind=link}

Valuation for Southwest Gas and investment opportunity

To assess the valuation and opportunities for an investment in Southwest, I will turn to FAST Graphs as it allows me to use analysts estimates of earnings and expectations of a P/E multiple to assess likely returns if prices reach that multiple and that EPS level. This enables an assessment of likely outcomes, using consensus estimates and historically achieved P/E ratios to assess what would happen if prices move in line with the expectations.

The FAST Graphs analyst scorecard suggests an 85% hit (mostly!) or beat over both one-year estimates (at the 10% margin of error) and two-years (at the 20% margin of error). The analyst successes on the scorecard suggest that we can rely on the estimates in the following calculations.

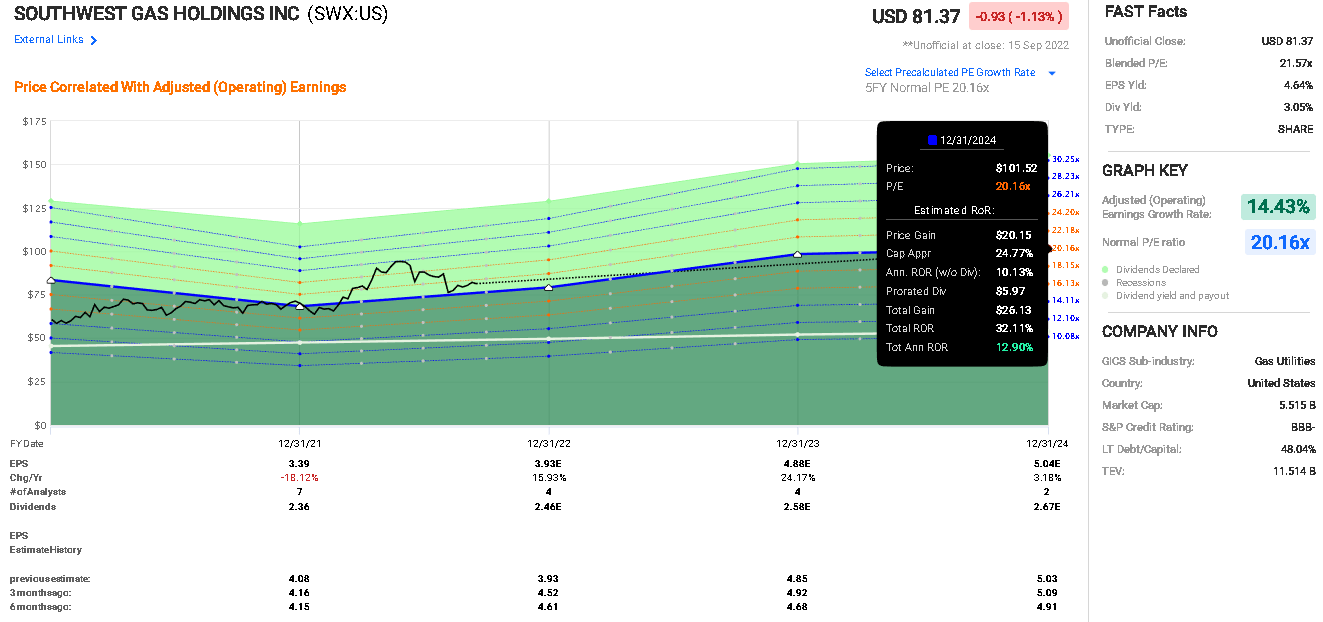

If prices continue to be at the normalized P/E of 20.16x (historical P/E over the last five years), then there is an upside and the FAST Graphs calculator suggests a total rate of return of 32%, an annualized RoR of 12.9% (Figure 7).

Figure 7. Analysts' estimates for EPS and P/E multiples allowing calculation of possible returns (FAST Graphs)

{kind=link}

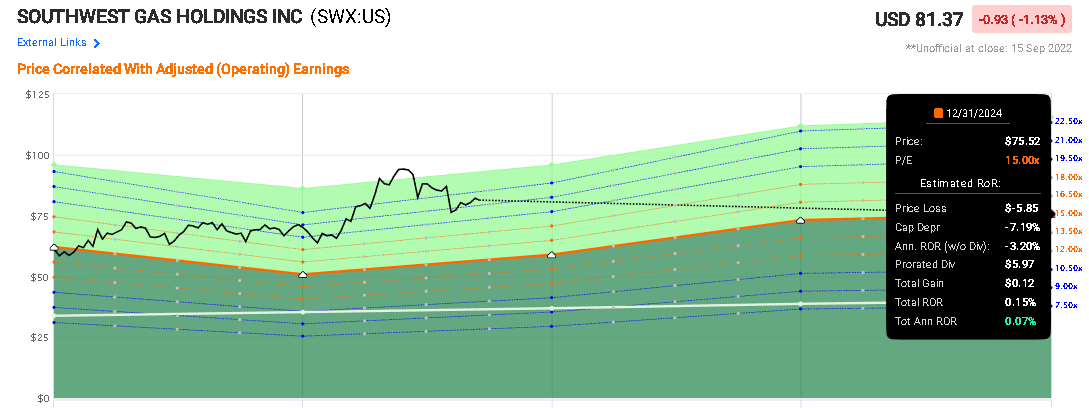

FAST Graphs enables us to evaluate different outcomes quickly and I often run more conservative scenarios. If the multiples contract and a P/E of only 15x is achieved at the end of 2024 (Figure 8), this implies a total RoR of 0.15%, or a negligible annualized RoR! This outcome is, in my opinion, conservative and it implies more upside than downside in this situation.

Figure 8. Analysts' expectations and outcome if P/E is only 15x (FAST Graphs)

{kind=link}

If the review process results in a spin-off of parts of Southwest, this would change the outlook.

A summary of my thoughts on Southwest Gas

Considering some of my recent analyses, I thought a brief summary section might be useful when my thoughts were for a Hold or tentatively edging into a Buy.

Business - diversification could offer stability - but does a utility benefit from this? A lower Piotroski F-Score than peers.

Valuation - no margin of safety but not over-priced. Some upside here is based on expected revenue growths if normalized P/E is maintained.

Financial safety - BBB rated; long history and careful management, but less (for example) interest coverage than peers.

Dividend - A reasonable 3% yield is about 2x the market average; dividend raises have been good over the last decade. The payout appears sustainable. But better options appear to exist.

Catalysts - none apparent as the strategic review is still in process. We should monitor this closely.

Recent moves - ongoing transition to Hydrogen - steps in the right direction, but these will take years to realize. This is still a gas utility.

Thesis

I went into this article and analysis looking first at the dividend and SWX as a potential income play with upside potential. I've found the company to be more diversified than I thought. Such diversification can benefit companies by smoothing out opportunities or swings in different sectors. Really, though, does a utility need this? Here, I wonder if the diversification adds complexity and no benefit (yes, I agree with Icahn). I will continue to monitor and assess the strategic review outcomes.

So - there is a reasonable dividend, but other peers have better dividend opportunities and appear to be in a better financial position, offering more stability. For instance, purely on dividend yields, I might consider UGI.

Is there some upside here? Yes, but I would suggest about the same for UGI.

There is some movement toward a green future but other gas utilities are doing this as well and it falls far short of simply investing in a renewable utility.

Finally, the upside here seems to be driven by revenue growths from utility infrastructure. If the review results in spinning off this segment, it will reduce the upside potential (through reduced future earnings) but may allow management to improve SWX's financial stability. SWX would be left with, arguably, a better and more focused utility in a better position, albeit with a dividend yield still lower than peers (Table 2).

The upside is reasonable but not great. There remains uncertainty with the strategic review, and the income opportunities are adequate, but better opportunities exist.

Therefore, I assess Southwest Gas as a Hold and suggest we examine other utilities.

I plan to monitor the review outcomes and assess the impact on future earnings and dividends.

Looking for an alternative in the utilities and gas space? Follow me and keep watch as I provide some coverage of options that may prove to be better picks and a better fit for your portfolio.

For further details see:

Southwest Gas Grapples With Strategic Review And I See Limited Upside