NWN - Southwest Gas Holdings: Should Handle Weakening Consumers But Valuation High

2023-09-12 16:31:13 ET

Summary

- Southwest Gas Holdings, Inc. is a regulated natural gas utility that operates in Nevada, Arizona, and California.

- The company's stock has been performing poorly, but it is well positioned to deliver respectable earnings growth and is minimally impacted by consumer spending.

- Southwest Gas Holdings has growth prospects through population growth and rate base growth, but its dividend growth has been inconsistent.

- The company's balance sheet is reasonable, but the valuation seems stretched considering the lack of a dividend increase this year.

- It may be best to sit on the sidelines right now and wait for any dips in the share price before buying in.

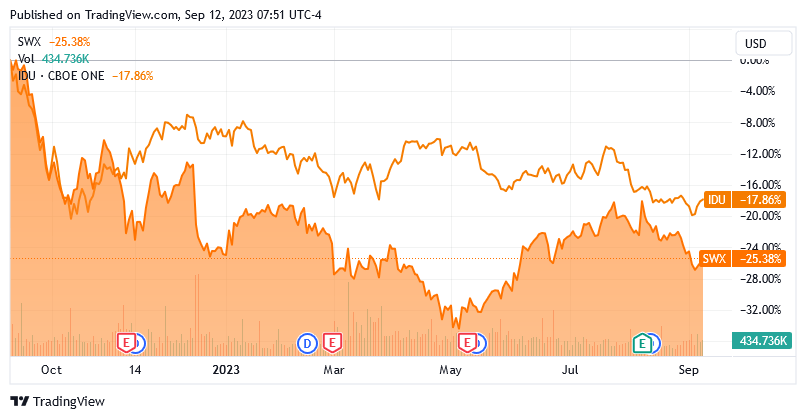

Southwest Gas Holdings, Inc. ( SWX ) is a regulated natural gas utility that operates in Nevada, Arizona, and California. Its most-known service area though is the city of Las Vegas, Nevada, and the surrounding area. The company also owns Centauri Group, which is an unregulated energy infrastructure company that operates throughout the United States. The utility sector as a whole has not been a very strong performer in the market recently, as rising interest rates have somewhat lowered the appeal of low-growth dividend-paying companies. After all, Southwest Gas Holdings only has a 4.04% dividend yield, so it is difficult to make a good case for purchasing that over a safe money market fund that yields 5% or higher. Southwest Gas Holdings has been performing especially poorly, as its one-year stock decline is substantially worse than that of the U.S. Utilities Index ( IDU ):

{kind=link}

This could prove to be a disappointment to many investors but there may be a few reasons to like Southwest Gas Holdings right now. In particular, the company is well positioned to deliver respectable earnings per share growth over the medium term, which when combined with the dividend should result in a very reasonable total return. In addition, there are numerous signs that American consumers might be at their breaking point, which could eliminate the one bright spot in the nation's economy and plunge the country into a recession. This would obviously have a very negative impact on the stock price and financial performance of any company that is highly dependent on consumer spending. Southwest Gas Holdings should only be minimally impacted by such an event, though.

As some readers may recall, I last discussed Southwest Gas Holdings back in July, when I presented the company primarily as a safety play with low growth. The dividend yield is quite a bit better now, though, and the company has released a more recent financial report, so it would be a good idea to revisit it today. Let us investigate and see how well this company is holding up and whether or not we need to revise our thesis.

About Southwest Gas Holdings

As mentioned in the introduction, Southwest Gas Holdings is primarily a regulated natural gas utility that serves Las Vegas, Nevada, Phoenix, Arizona, Tucson, Arizona, and the surrounding suburbs. The company's website includes the following description of its operations:

"Southwest Gas Corporation is engaged in the business of purchasing, distributing, and natural gas in portions of Arizona, California, and Nevada, serving over two million customers. Southwest Gas is the largest distributor of natural gas in Arizona and Nevada, serving large metropolitan areas including Phoenix, Tucson, and Las Vegas. In addition, Southwest Gas serves customers in portions of California, including the Lake Tahoe area, and the high desert and mountain areas in San Bernadino County."

The company is thus somewhat bigger than might be imagined considering that most of its service area is desert or other rather inhospitable terrain. With a customer base of over two million customers, it is one of the largest natural gas utilities in the United States. However, as I have pointed out in various previous articles, a utility's size does not affect its possession of certain characteristics. Perhaps the most important of these is that these companies enjoy remarkably stable cash flows over time. We can clearly see this characteristic in Southwest Gas Holdings by looking at the company's operating cash flows. Here they are for each of the past eleven twelve-month periods:

{kind=link}

Admittedly, this is not as good as many other utilities possess. After all, we do see some fluctuations as the winters of both 2021 and 2023 saw significant decreases in the company's cash flow. In particular, 2023 was especially bad as the company's operating cash flow was a negative $185.7 million:

{kind=link}

This is a trend that we have seen all throughout the industry though, as many natural gas utilities reported unusually weak cash flows this past winter. This was mostly driven by the fact that the winter of 2023 was one of the warmest on record in much of the United States. As a result, people consumed less natural gas than normal to heat their homes and businesses. A natural gas utility bills customers based on the amount of natural gas that they use during a given period of time so this situation would result in bills being lower than normal and by extension a sharp decrease in the company's revenue. That means that less money was available to cover its fixed expenses and make its way down to the bottom line profit and cash flow. This does not change the overall inference about the stability of the company's cash flows though, as we do still see quite a bit of stability between comparable quarters over time, excluding the one-off periods due to weather.

I explained the reasons for this general stability in my previous article on this company:

"The reason for this overall stability in any economic climate is that Southwest Gas provides a product that is generally considered to be a necessity for our modern way of life. After all, many people have natural gas heating systems in their homes and so they need the natural gas utility to supply fuel to keep them warm during cold days. As such, most people will prioritize making their utility bills ahead of making discretionary expenses during periods in which money gets tight."

There are certainly some reasons to believe that money is getting tight for many average Americans. For example, Michael Maharrey recently pointed out in a blog post at Schiff Gold that for the first time ever, more Americans are rolling over their credit card balances from month to month than are paying them in full. When we consider that the average credit card interest rate is at an all-time high, it seems very unlikely that people would willingly carry their balances unless their financial situation was extremely tight. The fact that this is coming even as total balances on credit cards increased by $45 billion between April and June alone only adds support for this conclusion. In addition to this, borrowers with outstanding student loans will need to resume making payments next month. That is estimated to result in discretionary income declining by an average of $350 per month for about forty million Americans. That will obviously add further strain to many households that appear to already be struggling to pay their bills and almost certainly have a detrimental effect on consumer spending, as well as on those companies that are highly dependent on consumer spending. This includes restaurant and hotel operators, technology companies with considerable consumer exposure such as Apple ( AAPL ), and possibly even subscription streaming companies such as Netflix ( NFLX ). After all, there are a lot of places where consumers are likely to cut back when they run out of money to spend.

Fortunately, investors in Southwest Gas Holdings should not really have to worry about this. After all, consumers are not likely to stop paying their heating bills as a way to save money. They will cut just about anything else in their budget first. Thus, this company could be a good way to avoid the worst of the damage from a collapse in consumer discretionary income and spending.

Growth Prospects

As I mentioned in the introduction, Southwest Gas Holdings has some growth prospects. This is a very good thing because investors are unlikely to be satisfied with mere stability. It is important that any company that we invest in grow and prosper with the passage of time.

Southwest Gas Holdings has two avenues for growth:

- Population Growth.

- Rate Base Growth.

In my previous article on Southwest Gas Holdings, I discussed how both Arizona and Nevada are experiencing fairly strong population growth. In fact, both of them are among the ten fastest-growing states in the country. As there is nothing more to add to my discussion in the previous article, I will not repeat my analysis here. The important takeaway is that these are the company's two largest markets and the population growth in these states should result in the company's customer base increasing. This means that more people will be paying their monthly gas bills and providing incremental revenue to the company.

The second way through which a utility company generates growth is by increasing the size of its rate base. As I explained in my previous article,

"The rate base is the value of a company's assets upon which regulators allow it to earn a specified rate of return. As this rate of return is a percentage, any increase to the rate base allows the company to increase the amount that it charges its customers in order to earn this specified rate of return. The usual way for a company like this to increase its rate base is by investing money into modernizing, upgrading, and possibly even expanding its utility-grade infrastructure."

In its second quarter 2023 conference call , Southwest Gas announced a plan to invest $2 billion into its infrastructure over the 2023 to 2025 period. This was somewhat disappointing, as the majority of the company's peers have now announced their spending and investment plans through the end of 2027. It would be preferable if Southwest Gas Holdings would follow suit and provide a five-year investment plan as opposed to the three-year plan that it actually provided. This is because the longer plans will give us better visibility into where the company's earnings should be several years down the road, and naturally the more information that we have to make our financial projections, the better decisions we can make about how to deploy our money.

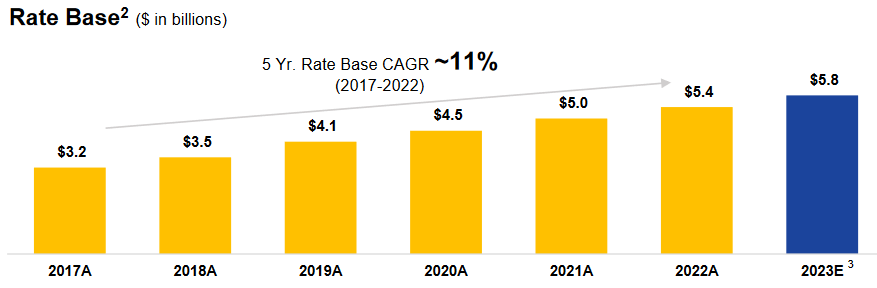

With that said, the company's plan as provided should allow it to increase its rate base at a 5% to 7% compound annual growth rate over the 2023 to 2025 period. This is unfortunately substantially less than the 11% compound annual growth rate that the company managed to achieve over the 2018 to 2022 period:

{kind=link}

The company's earnings per share growth should probably be in the same ballpark. When we combine this with the current 4.04% dividend yield, we can project an average annual total return of 9% to 11%, which is very reasonable for a conservative utility company. This total return is in line with what many of the company's peers should be able to accomplish, which should be reasonably appealing. This is especially true considering that Southwest Gas Holdings does have a higher yield than some other utility companies.

Financial Considerations

As I pointed out in my previous article on this company:

"It is always important to review the way that a company finances itself before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. That is normally accomplished by issuing new debt and using the proceeds to repay the existing debt. As this new debt is going to have an interest rate that corresponds with the market rate at the time of issuance, this process can cause a company's interest expenses to go up following the rollover in certain situations. As interest rates are currently at the highest levels that we have seen since 2001, this is a very real concern today. In addition to interest rate risk, we also have the fact that the company must make regular payments on its debt if it is to remain solvent. As such, an event that causes a company's cash flows to decline could push it into financial distress if it has too much debt. While utilities such as Southwest Gas usually have remarkably stable cash flows, this is still a risk that we should not ignore as bankruptcies have occurred in the sector."

One metric that we can use to analyze a company's financial structure is the net debt-to-equity ratio. As of June 30, 2023, Southwest Gas Holdings had a net debt of $5.1211 billion compared to a shareholders' equity of $3.4210 billion. This gives the company a net debt-to-equity ratio of 1.50 today. This is a bit higher than the 1.46 ratio that the company had the last time that we discussed it, which could be a bad sign. This is especially true as the increase in the ratio was caused by the company taking on more debt but not managing to increase its shareholders' equity. We should keep an eye on it to make sure that this situation does not get any worse.

Here is how the company's financial structure compares to its peers:

| Company |

| Net Debt-to-Equity Ratio |

| Southwest Gas Holdings |

| 1.50 |

| Atmos Energy ( ATO ) |

| 0.61 |

| NiSource Inc. ( NI ) |

| 1.65 |

| New Jersey Resources ( NJR ) |

| 1.59 |

| Northwest Natural Holding ( NWN ) |

| 1.22 |

| Spire Inc. ( SR ) |

| 1.54 |

As we can see, despite the increase in the company's net debt-to-equity ratio between the first and second quarters of 2023, the company still compares fairly well to its peer group. As such, it does not appear that the company is using too much leverage to finance its operations. We should not need to worry too much about the company's debt level right now, but we should also monitor it to make sure that it does not continue to increase going forward.

Dividend Analysis

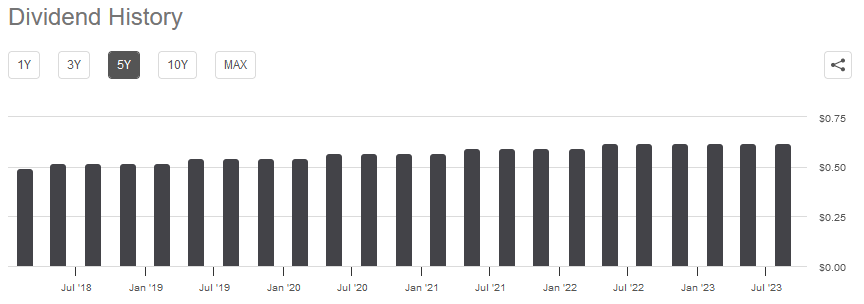

One of the biggest reasons why investors purchase shares of utility companies such as Southwest Gas Holdings is because of the incredibly high dividend yields that they tend to possess. Southwest Gas is certainly no exception to this, as the stock boasts a 4.04% yield at the current price. This is substantially higher than the 1.45% current yield of the S&P 500 Index (SP500) and is even quite a bit above the 2.67% current yield of the U.S. Utility Index. Southwest Gas Holdings also has a history of raising its dividend over time, although it has not been particularly consistent with that recently:

{kind=link}

As we can see, the company failed to increase its dividend in May, breaking its long-running streak of delivering annual dividend raises. That is incredibly disappointing, particularly considering that today's inflationary environment has stripped the purchasing power of the dividends that the company pays out. That is a very real problem for anyone who is depending on their portfolios to provide the income that they need to pay their bills or handle the expenses of daily life, which would be a group that includes most retirees. Indeed, it is quite possible that some people are opting to favor other utilities over Southwest Gas Holdings simply because of this.

As is always the case, it is important that we ensure that the company can actually afford the dividends that it pays out. After all, a static dividend is still better than the cut that will undoubtedly ensue if the company cannot afford its dividends.

The usual way that we judge a company's ability to pay its dividends is by looking at its free cash flow. In the twelve-month period that ended on June 30, 2023, Southwest Gas Holdings reported a negative levered free cash flow of $751.9 million. That is obviously not nearly enough to pay any dividends, but the company still paid out $169.1 million over the period. At first glance, this is likely to be concerning as it implies that the company cannot cover its dividends out of its internal cash generation capabilities.

However, it is not uncommon for a utility to cover its capital expenditures via the issuance of debt and equity. The company will then pay its dividends out of operating cash flow. This is done because of the incredibly high costs involved in constructing and maintaining a utility-grade infrastructure network over a wide geographic area. Unfortunately, we have some problems here as well. In the twelve-month period that ended on June 30, 2023, Southwest Gas Holdings only had an operating cash flow of $156.0 million. That is still not enough to cover its dividends, which has been the case for two quarters now. As such, the company either needs a significant increase in cash flows or a dividend cut in order to sustain itself.

Fortunately, the Farmer's Almanac is predicting that the upcoming winter will be colder than we saw last year. It is even projected that Texas will experience much colder temperatures than normal for that time of year. This could be a sign that the company's customers will require more natural gas to heat their homes than they did during the winter season of 2022 to 2023. If this proves to be correct, it could result in the increased cash flow that Southwest Gas Holdings desperately needs to sustain its dividends right now.

Valuation

According to Zacks Investment Research , Southwest Gas Holdings will grow its earnings per share at a 5.00% rate over the next three to five years. That is relatively in line with the company's own projections of its rate base growth, so it seems to be a fairly reasonable projection. This earnings growth rate gives the company a price-to-earnings growth ratio of 3.64 over the period. This is quite a bit less than what the company had the last time that we discussed it, which is not especially surprising. After all, the company's stock price has declined a bit over the past few months.

Here is how Southwest Gas Holdings' current valuation compares to that of its peers:

| Company |

| PEG Ratio |

| Southwest Gas Holdings |

| 3.64 |

| Atmos Energy |

| 2.59 |

| NiSource Inc. |

| 2.45 |

| New Jersey Resources |

| 2.67 |

| Northwest Natural Holding |

| 4.01 |

| Spire Inc. |

| 3.37 |

This is disappointing, as Southwest Gas Holdings currently appears to be more expensive than any of its natural gas utility peers except for Northwest Natural. We do see though that the companies with the highest yields are also the most expensive. This is perhaps not surprising, as most of these companies have similar total return prospects (earnings growth plus dividend yield is about 9% to 11% for all of them).

The fact that Southwest Gas Holdings failed to increase its dividend this year should discount it a bit relative to its peers that continue to grow their dividends though, since dividend growth will naturally result in a higher yield-on-cost after a few years. As such, it might be best to wait and see if Southwest Gas Holdings will decline further before buying its shares.

Conclusion

In conclusion, Southwest Gas Holdings is primarily a regulated natural gas utility that serves Nevada, Arizona, and parts of California. The company boasts the general stability that we typically appreciate with these companies, which could be a very good thing as it appears that American consumers are coming under increasing financial strain. The company's balance sheet is reasonable, but its lack of dividend growth and high valuation relative to its peers are major strikes against it. It may be best to wait for the shares to weaken further before buying.

For further details see:

Southwest Gas Holdings: Should Handle Weakening Consumers, But Valuation High