CTRA - Southwestern Energy: Developing Markets May Offset Mid-Atlantic Weakness

2023-10-02 07:55:14 ET

Summary

- Southwestern Energy is recommended as a buy for speculative investors who expect stable or rising natural gas prices.

- SWN is particularly well-positioned to serve the much-expanding LNG export market.

- Dividend hunters should look elsewhere as the company does not offer a dividend.

- The Biden administration's proposed policies and regional restrictions on natural gas use impact the price of Southwestern's Marcellus (Appalachian) gas.

I am recommending Southwestern Energy Company ( SWN ) as a buy to a narrow group: speculative investors who expect natural gas prices to stay stable or rise.

Dividend hunters should look elsewhere. Nor does Southwestern Energy have a share buyback program at this time.

And investors should certainly be aware the Biden administration has proposed severe limitations on gas furnaces . Certain areas of the country-unfortunately including those near the Pennsylvania Marcellus reserves-are also discouraging natural gas use, most recently New York's future limits on gas stoves and furnaces.

All Marcellus producers have had a challenging several quarters, or even years. Southwestern Energy has adapted to the environment by:

- adding, and emphasizing Haynesville reserves

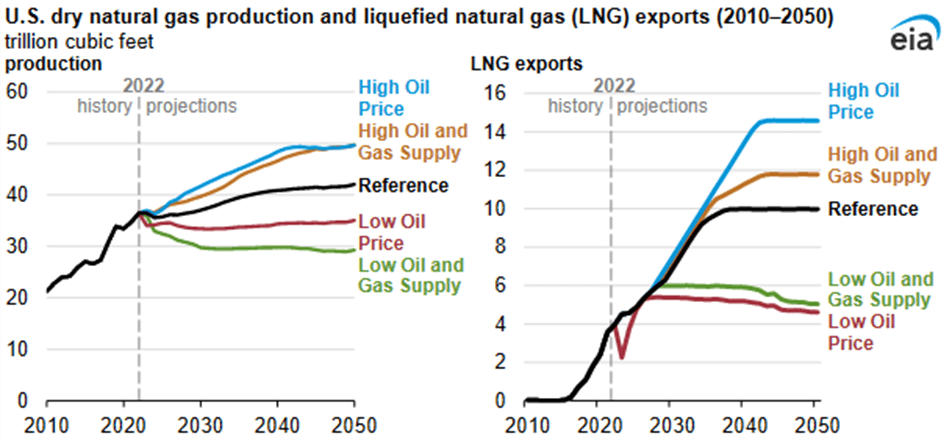

- contracting much of its Haynesville production for the expanding LNG export market. US LNG exports have grown from zero to an eighth (12 BCF/D) to potentially as much as a quarter (25 BCF/D by the late 2020s) of entire US gas demand, with even more export facilities proposed.

- focusing on debt paydown

- reducing Marcellus production where prices warrant

- reorienting capex toward the Haynesville

Gas drilling is quick: any perceived supply shortage is soon remedied.

However, there are also broader demand factors at work:

- Always the possibility of consumer rebellion-as has occurred in the UK-when governments tried to take away affordable energy

- Natural gas is lower-carbon and lower-emission than coal

- Operationally, as 24/7 coal plants are phased out, utilities are finding they need fuels with similar operational characteristics-nuclear and natural gas

- Only natural gas has the fast on/fast off characteristic needed to back up intermittent solar and wind. Intermittency can be such an issue that appropriate grid planning suggests a 1.1:1 ratio of gas generation capacity to wind and solar capacity.

- Utility-scale batteries have a four-hour output time limit

- Petrochemical demand continues and grows

- While despite the Russian gas cutoff Europeans are not likely to commit to 20-year contracts (only 5- to 10-year), the markets for China, India, Southeast Asia, and Africa remain very large. China, for example, uses a third of the energy per capita as the US; India uses a fifteenth.

LNG Exports

US LNG exports, once virtually zero, are now 12 BCF/D and are expected to double that within a few years. Because most LNG export facilities are on the US Gulf Coast, gas from the proximate Haynesville has been especially important to meet this new demand.

Projections from the EIA show the expected growth of gas production and US LNG exports.

{kind=link}

US Gas Production, Demand, and Prices

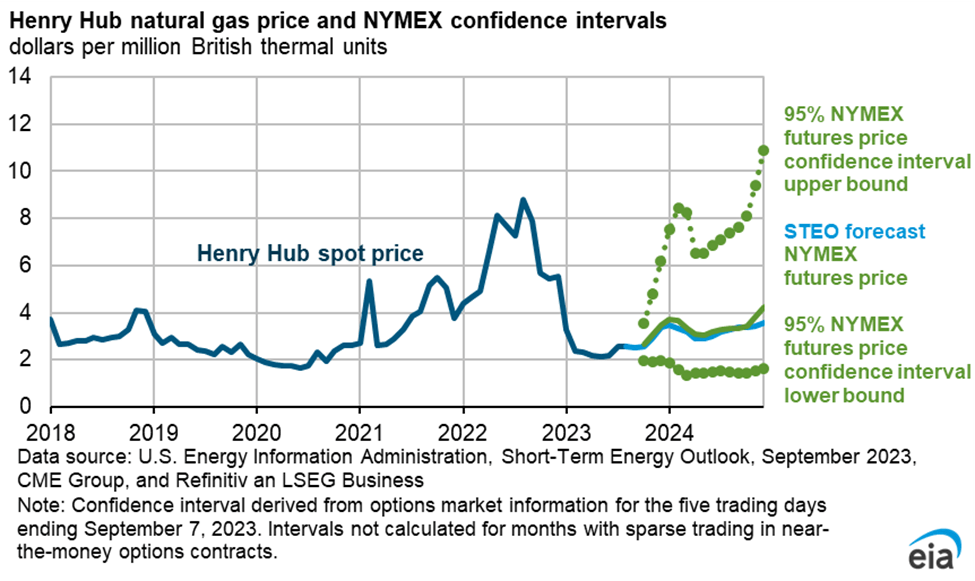

September 29, 2023, natural gas futures price for November 2023 delivery was $2.93/MMBTU at Henry Hub, Louisiana.

The EIA projects Henry Hub gas prices averaging between $3/MMBTU and $4/MMBTU through the end of 2024 in its 5-95 confidence interval.

As the EIA's spot price chart for New York and the mid-Atlantic frequently illustrates, Appalachian prices are typically well below those for Henry Hub.

For example, a recent chart shows a Louisiana gas price of $2.74/MCF but a mid-Atlantic gas price of $0.79/MCF, only a third. This is a potent illustration of the reason behind Southwestern's strategic move to grow Haynesville production while reducing or keeping static Marcellus production.

{kind=link}

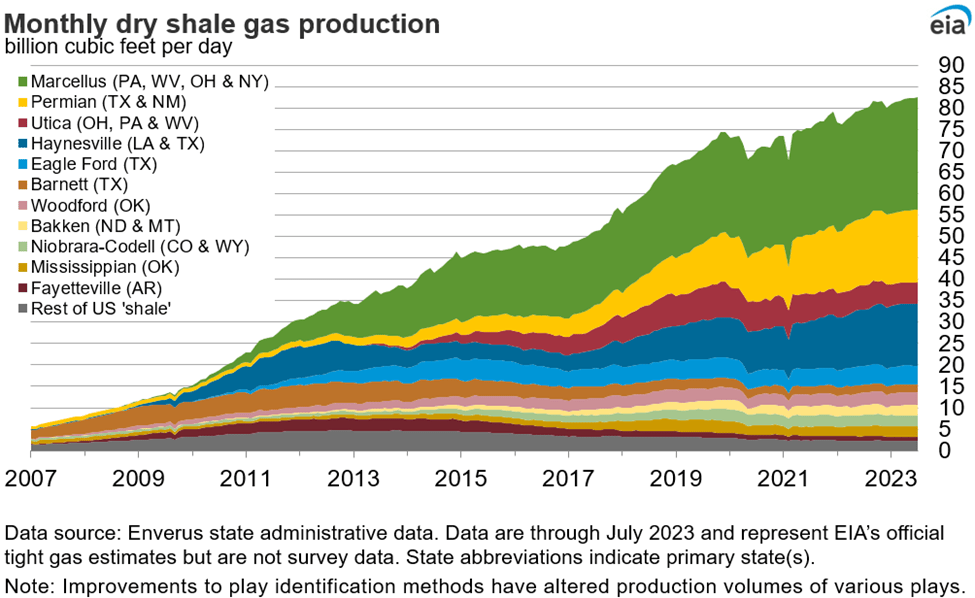

Total US dry natural gas production for the week ending September 27, 2023, was 101.2 BCF/D.

Appalachian gas volumes (the green-colored Marcellus and the rust-colored Utica) are estimated to be 35.7 BCF/day (DPR link) in October 2023, or more than a third of October's US gas production.

Haynesville gas volumes (the dark blue) are estimated to be 16.2 BCF/D in October 2023.

And note the growth in Permian gas volumes (yellow), much of it associated to an estimated 23.7 BCF/d.

{kind=link}

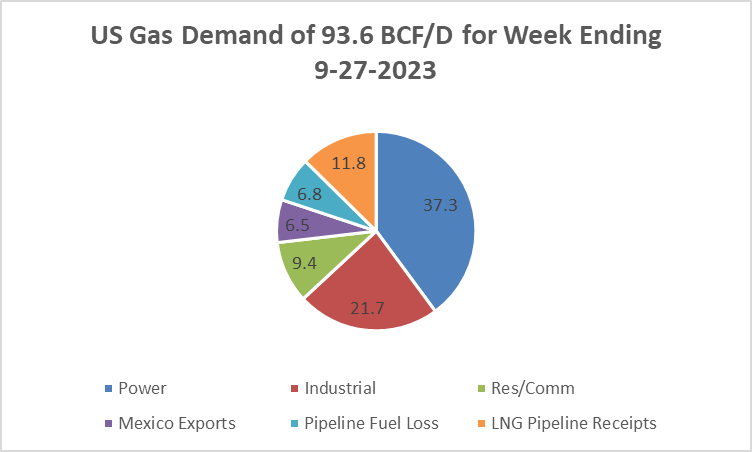

For the week ending September 27, 2023, US natural gas demand totaled 93.6 BCF/D. This varies considerably throughout the year depending on weather.

{kind=link}

Natural Gas Liquids

NGLs (ethane, propane, and butane) are used to make ethylene, a critical petrochemical building block, and for heating and drying. Southwestern Energy gets price uplift from its NGL production.

Southwestern Energy Second Quarter 2023 Results

In the second quarter of 2023 , Southwestern Energy's net income was $231 million or $0.21/share. Excluding a gain on derivatives and other one-time items, adjusted net income was $95 million. Adjusted EBITDA (a non-GAAP number) was $484 million and net cash from operations was $425 million.

Southwestern produced 4.6 BCF-equivalent (BCFe)/day, 86% (4.0 BCF/D) of which was natural gas and 106,000 BPD of liquids-mainly natural gas liquids (12%) and oil (2%).

Including the impact of derivatives, Southwestern's weighted average realized price was $2.33/MCFe for 2Q23. This compares to $3.04/MCFe for 2Q22.

The company said it "reduced full-year capital investment guidance by $200 million or 10% due to activity reductions, reduced inflation, and operational efficiencies."

Strategically, it is important to note that in 2Q23 the gap between Southwestern's Appalachian and Haynesville daily gas volumes shrank so that they are now nearly split at 54% Appalachia and 46% Haynesville. It is worth noting that the Appalachian volumes get price uplift from co-produced natural gas liquids and oil.

The company is actually reversing these percentages in capital expenditures, with 45% going to Appalachia and 55% to Haynesville.

And, Southwestern fits the above generalization on relatively poorer prices for Appalachian gas. In 2Q23, its natural gas discount to NYMEX, including transportation, was a steep $0.75-$0.87/MCF.

Strategy

The company's current debt goal is reduction to $3.5-$3.0 billion (from $4.0 billion), along with achieving investment-grade status.

It has fifteen years of core inventory in the Marcellus and Haynesville.

Important for future growth, its current LNG sales lead its Marcellus peers at 1.5 BCF/D, or 37.5% of its natural gas production. This suggests the company's strategic advantage in its Haynesville production.

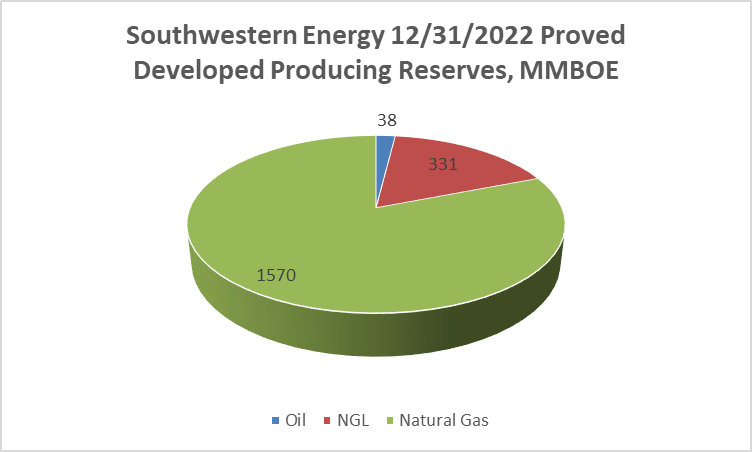

Reserves

Southwestern Energy's year-end 2022 total year-end proved reserves were 3.6 billion barrels of oil equivalent ((BOE)), 80% of which was natural gas. Its proved developed producing reserves, a smaller slice of the total, were 1.9 billion BOE. The mix for proved developed producing reserves is shown below.

{kind=link}

Because 2022 prices were higher than in 2021 and 2022, the PV-10 cash flow value of reserves increased 2x from 2021, from $18.7 billion to $37.6 billion for year-end 2022.

Since 2022 gas prices were extraordinarily high, the price component of the 2023 reserve measure, and thus the entire reserve value, is likely to be lower.

Competitors

Southwestern Energy is headquartered in Spring, Texas, north of Houston. Other gas producing companies with which it competes in Appalachia include Antero Resources ( AR ), Chesapeake ( CHK ), CNX ( CNX ), Coterra ( CTRA ), EOG ( EOG ) in the Utica, EQT ( EQT ), National Fuel Gas ( NFG ), Ovintiv ( OVV ), and Range Resources ( RRC ).

Southwestern Energy is like Range Resources but additionally has Haynesville (Louisiana) production.

Appalachian natural gas is at a disadvantage due to pipeline constraints to natural gas in Louisiana, Texas, and Oklahoma for meeting Gulf Coast industrial, power, Mexican export, and LNG export demand.

Haynesville competitors include several private companies as well as BP ( BP ) and Chesapeake.

As the large US Permian basin matures, more of its production will be gas and associated gas-rather than oil-which is already putting downward pressure on prices.

Governance

On September 1, 2023, Institutional Shareholder Services ranked Southwestern Energy's overall governance as an excellent 1, with sub-scores of audit (1), board (2), shareholder rights (1), and compensation (1). On the ISS scale, 1 represents lower governance risk and 10 represents higher governance risk.

Insiders own a very small 0.6% of the stock. On September 15, 2023, shorted stock as a percentage of float was 5.7%.

Southwestern's beta is 1.37. While more volatile than the overall market, this is unexpectedly low for an independent gas producer and reflects its hedging program.

On June 29, 2023, the four largest institutional stockholders, some of which represent index fund investments that match the overall market, were Vanguard (10.1%), BlackRock (8.8%), T. Rowe Price Associates (5.1%), and State Street (3.9%).

All but Vanguard are signatories to the Net Zero Asset Managers Initiative, a group that, as of June 30, 2023, manages $59 trillion in assets worldwide and which limits hydrocarbon investment via its commitment to achieving net zero alignments by 2050 or sooner.

Financial and Stock Highlights

With Southwestern's September 29, 2023, closing stock price of $6.45/share, market capitalization is $7.1 billion .

Given a 52-week price range of $4.57-$7.48/share, the closing price is 86% of the 52-week high and 78% of the one-year target price of $8.23/share.

Southwestern's trailing twelve months' ((TTM)) returns on assets and equity are exceptional at 27.7% and 146.6%, respectively. Trailing twelve months' EPS is an unusually high $5.09 for a rock-bottom current price/earnings ratio of 1.3.

TTM operating cash flow was $3.32 billion and levered free cash flow was -$103.5 million.

On June 30, 2023, the company had $6.5 billion in liabilities and $13.0 billion in assets making the company's liability-to-asset ratio 50%.

Of the liabilities, current liabilities, including derivative liabilities, are $1.9 billion. Derivative liabilities are down considerably from $1.3 billion on December 31, 2022, to $270 million on June 30, 2023. Long-term debt is $4.0 billion.

The ratio of debt to EBITDA is 0.6.

Analysts' average estimates for 2023 and 2024 EPS are $0.67 and $1.13, respectively, giving a forward P/E range of 9.7-5.6.

Southwestern does not pay a dividend.

The company's mean analyst rating is a 2.7, or nearer "hold" than "buy," from 33 analysts. At least one analyst considers the company significantly undervalued.

Notes on Valuation

The company's book value per share of $5.89, near its market price, suggests neutral investor sentiment.

With an enterprise value (EV) of $11.3.0 billion, Southwestern's EV/EBITDA ratio is an extraordinarily low 1.6, far less than the preferred maximum of 10 or less and so well into bargain territory.

So overall, Southwestern Energy has

- a market capitalization of $7.1 billion,

- an enterprise value of $11.3 billion,

- reserves with a PV-10 value of $37.6 billion at year-end 2022 (likely to be lower at year-end 2023) , and

- a balance sheet asset value of $13.0 billion .

Positive and Negative Risks

Investors should consider their natural gas and natural gas liquids price and demand expectations-in Appalachia with its limited takeaway capacity-and their natural gas price expectations for Haynesville as the factors most likely to affect Southwestern.

Inflation is high and is expected to stay so. This will affect Southwestern's costs including for drilling and financing.

Other risks are political and regulatory-particularly with the Biden administration, bankers including three of Southwestern's largest institutional investors, and several states on the East Coast-part of Southwestern's natural market--taking a race-to-zero-hydrocarbons posture.

Recommendations for Southwestern Energy

Due to the absence of a dividend, I do not recommend Southwestern to dividend-hunters.

The company earns excellent governance ratings and is prioritizing debt paydown. For those who expect higher natural gas prices on the Gulf Coast and have an eye on both increasing US LNG exports and increasing use of natural gas in the thermal stack for electricity generation-especially in the PJM region-Southwestern Energy could represent an opportunistic buy.

However, be aware that both the Biden administration and regions like New England and the mid-Atlantic (New York and New Jersey)-which are in the natural market area of the Marcellus--are actively discouraging natural gas use.

ir.swn.com

For further details see:

Southwestern Energy: Developing Markets May Offset Mid-Atlantic Weakness