TXN - SOXX: Semicon Industry 2023 - Full Steam Ahead

2023-03-14 04:03:53 ET

Summary

- We expect chipmakers' growth to recover by 19% on average driven by data center and automotive growth, the continued shift to 5G and a potential memory market recovery.

- For the top 5 foundries, we forecasted a lower average in 2023 of 11.2% with lower pricing growth and limited shipment growth supported by planned capacity expansions and projected capex.

- We expect the top equipment makers’ growth to slow down to 4% on average with planned top memory makers’ capex cuts and lower logic and foundry capex growth.

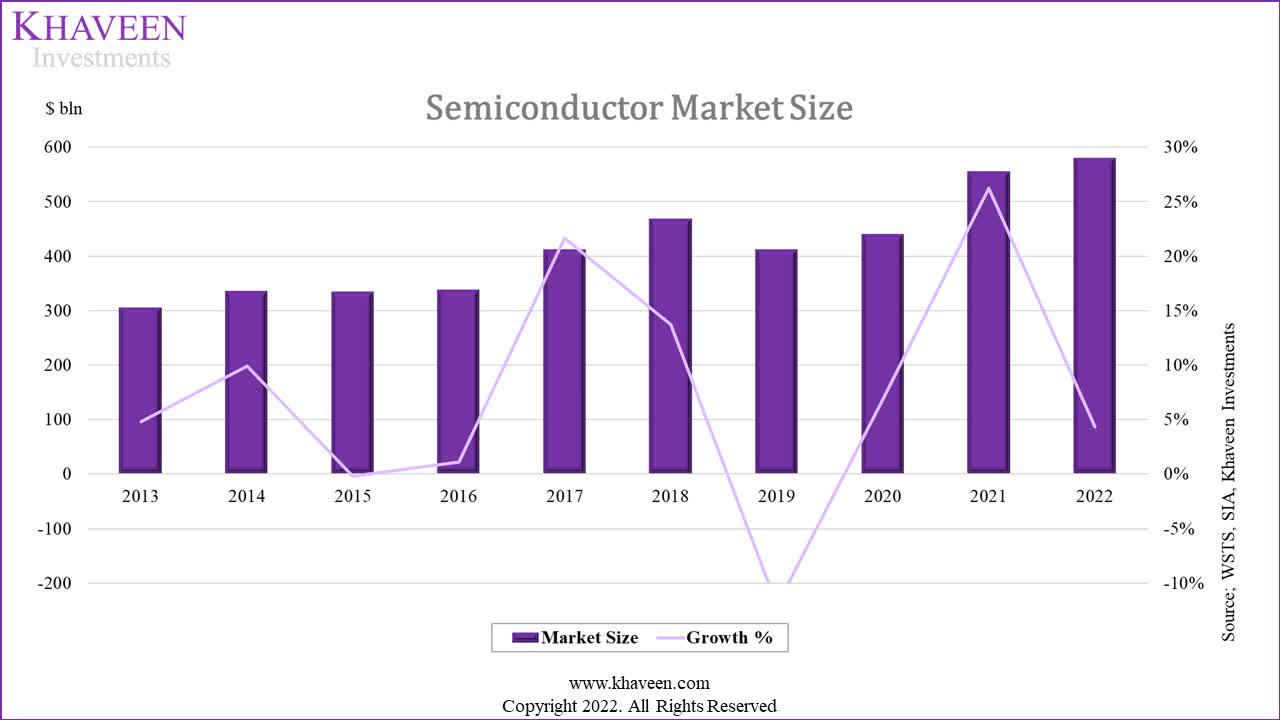

In this comprehensive analysis of the semiconductor industry, we conducted an in-depth review of the top 10 semiconductor holdings in the iShares Semiconductor ETF ( SOXX ), focusing on their performance in 2022 based on revenue. Our analysis delved into the revenue growth and outlook of the top 10 chipmakers for 2022, the top 5 foundry companies, and the top 5 semicon equipment companies for 2023, using our revenue forecasts as the primary basis for our determinations. Moreover, we identified the key factors affecting the growth outlook of each of the top chipmakers, foundries and equipment makers, as well as the principal factors driving the entire semicon industry. As seen in the chart below, the semiconductor market grew to over $580 bln in 2022 but is a slowdown compared to its high growth of 26.2% in 2022 and had a 10-year average of 7.6%.

SIA, WSTS, Khaveen Investments

{kind=link}

| Companies |

| 2021 Growth % |

| 2022 Growth % |

| Stock Price Change (2022) |

| Average Consensus Surprise |

| Type |

| Market |

| Country |

| Broadcom* ( AVGO ) |

| 18.0% |

| 22.5% |

| -15.97% |

| 1.2% |

| Chipmaker |

| DAO |

| US |

| Texas Instruments ( TXN ) |

| 26.9% |

| 9.2% |

| -12.34% |

| 4.7% |

| Chipmaker |

| DAO |

| US |

| Nvidia ( NVDA ) |

| 61.4% |

| 0.2% |

| -50.31% |

| 1.2% |

| Chipmaker |

| Logic |

| US |

| Qualcomm ( QCOM ) |

| 35.0% |

| 19.2% |

| -39.88% |

| 1.2% |

| Chipmaker |

| Logic |

| US |

| AMD ( AMD ) |

| 68.3% |

| 43.6% |

| -54.99% |

| 1.7% |

| Chipmaker |

| Logic |

| US |

| KLA Corp ( KLAC ) |

| 34.5% |

| 28.4% |

| -12.34% |

| 4.2% |

| Equipment |

| Equipment |

| US |

| Analog Devices ( ADI ) |

| 44.1% |

| 49.0% |

| -6.68% |

| 3.1% |

| Chipmaker |

| DAO |

| US |

| NXP Semiconductors ( NXPI ) |

| 28.5% |

| 19.4% |

| -30.62% |

| 0.9% |

| Chipmaker |

| DAO |

| Netherlands |

| Lam Research ( LRCX ) |

| 38.5% |

| 15.3% |

| -41.56% |

| 3.2% |

| Equipment |

| Equipment |

| US |

| Applied Materials ( AMAT ) |

| 32.8% |

| 8.6% |

| -38.12% |

| 2.1% |

| Equipment |

| Equipment |

| US |

| Average |

| 38.8% |

| 21.5% |

| -30.28% |

| 2.3% |

*2022 prorated based on Q1 to Q3 semicon revenue

Source: Company Data, Khaveen Investments

In 2022, the average revenue growth for the top semicon companies was 21.5%, lower compared to 2021 at 39%. This was led by decreasing growth from both chipmakers and equipment makers. By market type, half of the DAO companies had higher growth in 2022 including Broadcom (prorated from Q1 to Q3) and ADI which completed its acquisition of Maxim for $20 bln in September 2021 while all logic companies suffered lower growth. Nvidia had the lowest growth in 2022 among the top companies as its revenue growth was weighed down by a decline in its Gaming segment by 27% for the year.

Equipment makers also all had lower growth in the table including KLA, Lam Research and Applied Materials. Notwithstanding, the average revenue consensus surprise for the top holdings was positive at 2.3%, indicating better-than-expected results for the top companies. Astonishingly, the average stock prices of the top 10 semicon companies declined by 30% in 2022 which we believe is a huge mismatched decline as the industry revenues still grew massively by 22%.

Chipmakers' Growth Expected to Recover in 2023

| Chipmaker Companies |

| 2021 |

| 2021 Growth % |

| 2022 |

| 2022 Growth % |

| Our FY2022 Forecast |

| Market |

| Country |

| Broadcom |

| 20,380 |

| 18% |

| 24,968 |

| 22.5% |

| 7.72% |

| DAO |

| US |

| Texas Instruments |

| 18,344 |

| 27% |

| 20,477 |

| 11.6% |

| 8.60% |

| DAO |

| US |

| Nvidia |

| 26,914 |

| 61% |

| 27,897 |

| 3.7% |

| 4.50% |

| Logic |

| US |

| Qualcomm |

| 36,036 |

| 35% |

| 44,661 |

| 23.9% |

| 31.68% |

| Logic |

| US |

| AMD |

| 16,434 |

| 68% |

| 24,003 |

| 46.1% |

| 81.30% |

| Logic |

| US |

| Intel ( INTC ) |

| 79,024 |

| 1% |

| 65,349 |

| -17.3% |

| -6.80% |

| Logic |

| US |

| MediaTek (MDTKF) |

| 17,789 |

| 55% |

| 19,578 |

| 10.1% |

| 11% |

| Logic |

| Taiwan |

| Samsung ( SSNLF ) |

| 81,139 |

| 29% |

| 80,946 |

| -0.2% |

| 17.6% |

| Memory |

| Korea |

| Micron ( MU ) |

| 29,619 |

| 34% |

| 27,156 |

| -8.3% |

| 19.83% |

| Memory |

| US |

| SK Hynix |

| 33,287 |

| 35% |

| 38,140 |

| 14.6% |

| N/A |

| Memory |

| Korea |

| Average |

| 36% |

| 10.7% |

| 19.49% |

Source: Khaveen Investments

In terms of the top 10 chipmakers globally by revenue in the table above, we prorated the companies’ revenues from Q1 to Q3 to compare their performance. On average, the top chipmakers had a lower growth rate compared to 2021 of 10.7% from 36%. All companies had lower growth across all markets including DAO, logic and memory except for Broadcom. Intel was the only Logic chipmaker to have negative growth in 2022 as the company’s CCG segment revenue declined by 23% in 2022 as it was affected by the decline in the PC market. For the memory makers, Micron had the lowest growth in 2022 as its revenue was impacted by declining memory market ASPs in our previous analysis . The company with the highest growth rate was AMD which acquired Xilinx in Q1 of 2022.

Compared to our FY2022 forecast for the companies, the average growth of our forecast was higher at 19.5% compared to 10.7% for the prorated growth. This is as the prorated growth for Logic chipmakers such as Intel and AMD was lower than our forecast as these companies were affected by the PC market slowdown. Moreover, the memory makers such as Micron and Samsung underperformed compared to our forecasts as memory prices declined larger than expected as analyzed in our analysis of Micron.

We summarized our revenue forecasts for the top 10 chipmakers globally in the table below from previous analyses except for SK Hynix which we based on analysts’ growth consensus.

| Chipmaker Companies |

| 2023 Growth Forecast % |

| Broadcom Semiconductors |

| 11.3% |

| Texas Instruments |

| 11.7% |

| Nvidia |

| 23.2% |

| Qualcomm |

| 8.6% |

| AMD |

| 18.9% |

| Intel |

| 15.0% |

| MediaTek |

| 11.0% |

| Samsung |

| 33.0% |

| Micron |

| 23.2% |

| SK Hynix |

| 36.4% |

| Average |

| 19.2% |

Source: Khaveen Investments

Based on the table, we forecasted the average revenue growth to increase to 19.2% in 2023. We have a positive growth forecast for all companies across DAO, Logic and Memory markets. Moreover, for each of the companies, we identified its growth driver in 2023 from previous analyses:

- For Broadcom, we expect its semicon revenue (71% of total revenue) growth (11.3%) to be driven by its Networking segment which was its largest segment at 26% of its total revenue at a growth rate of 17.1% driven by its portfolio of ethernet switch chips, optics and custom ASICs targeting customers in data centers and enterprise markets.

- For Texas Instruments, we believe its revenue growth in 2023 (11.7%) to be supported by supply growth of 17.7% fulfilling demand and easing supply chain constraints as we expect the company to benefit positively from the CHIPS Act for its expansion in Sherman.

- For Nvidia, we expect its growth (23.2%) to continue to be driven by Data center segment which is its largest segment at 45% of total revenues with our forecast growth rate at an average of 33.6% supported by the cloud market growth driven by rising data volumes as well as its expansion into Enterprise AI software and data center CPU. Additionally, we see its growth in the automotive segment (2.1% of revenue) for its ADAS chips to grow at a forecasted rate of 22%.

- For Qualcomm, we expect its growth (8.6%) to be driven by the continued shift of smartphones to 5G for its Handset revenue (56% of total) but forecasted its growth lower in 2023 at 2.24% as we previously accounted for a conservative impact for the potential loss of Apple’s modem business. We also see its growth supported by its automotive segment (3.1% of revenue) at a rate of 42.9% and VR/AR revenue growth of 41.82%.

- For AMD, we expect its growth (18.9%) to be driven by its data center segment including its EPYC CPUs at a growth rate of 39.05% supported by continuous pricing and performance increases for its data center CPU products.

- For Intel, we forecasted its growth to recover in 2023 at 15% with positive growth for its CCG segment (52% of total revenue) at 8.7% as we forecasted positive pricing growth of 7.4% for its PC CPU ASPs despite a flattish shipment growth forecast of 1.2%. Additionally, we see its DCAI segment (29% of revenue) growth in 2023 increase supported by our server ASP forecast of 14.2% and shipment growth of 3.6%. Also, we see its Mobileye segment despite accounting for only 2% of revenue growth at a forecasted rate of 31.3%.

- For MediaTek, we previously analyzed the company and expect its growth of 11% to continue to be supported by its increasing adoption of 5G products by Chinese smartphone makers and forecasted it to grow at a long-term market forecast for smartphone AP.

- In our Micron analysis, we expect the company’s revenue to recover in 2023 at 23.2% as we believe a lower supply growth outlook compared to demand growth could support the memory market pricing. Moreover, based on our forecasted top memory chipmakers’ capex in 2023, we derived our supply projections for Micron lower than our demand growth estimates and forecasted its revenue growth for DRAM and NAND at 22.5% and 26.7% respectively.

- For Samsung, we expect the company’s growth at 33% supported by its memory chip business (25% of revenue) and benefit from the long-term drivers in the memory market as the leader in NAND and DRAM. Moreover, we expect its display LED segment (10% of revenue) growth to be supported by its high-growth automotive segment at a forecasted growth rate of 8%.

- For SK Hynix, we forecasted the company’s revenue growth based on its revenue breakdown: DRAM (70%) and NAND (23%) with our DRAM and NAND market growth forecast of 37.7% and 43.4% respectively as we expect supply growth to be lower than demand growth which could buoy market pricing based on our Micron analysis.

Foundry Market Slowdown Expected in 2023

| Foundry Market Revenue ($ mln) |

| FY2021 |

| 2021 Growth % |

| FY2022 |

| 2022 Growth % |

| Our FY2022 Forecast |

| Country |

| TSMC |

| 56,834 |

| 28.6% |

| 74,711 |

| 31.5% |

| 33.8% |

| Taiwan |

| Samsung* |

| 18,796 |

| 33.7% |

| 22,000 |

| 17.0% |

| 27.8% |

| Korea |

| GlobalFoundries ( GFS ) |

| 6,375 |

| 8.4% |

| 8,108 |

| 27.2% |

| 19.5% |

| US |

| UMC ( UMC ) |

| 7,660 |

| 30.1% |

| 9,212 |

| 20.3% |

| 9.2% |

| Taiwan |

| SMIC |

| 5,443 |

| 47.1% |

| 7,273 |

| 33.6% |

| 26.4% |

| China |

| Average |

| 29.6% |

| 25.9% |

| 23.3% |

*2022 based on prorated Q1 to Q3 2022 foundry revenue

Source: Company Data, Trendforce, Khaveen Investments

As seen in the table above, the top 5 foundries based on had a slightly lower average compared to 2021 but still grew strongly by double digits. TSMC, the market leader, had a higher growth rate in 2022. Besides that, GlobalFoundries and SMIC both also had an above-average growth rate for the year. In contrast, Samsung had the lowest growth rate and UMC had below-average growth. In comparison, our average FY2022 forecast for the top foundries was slightly lower than the prorated 2022 growth but still fairly in line growing by over 20%.

Furthermore, with the strong growth experienced by the foundries in 2022, we believe this could support the positive growth outlook for chipmakers in 2023 which we forecasted their growth to accelerate compared to 2022.

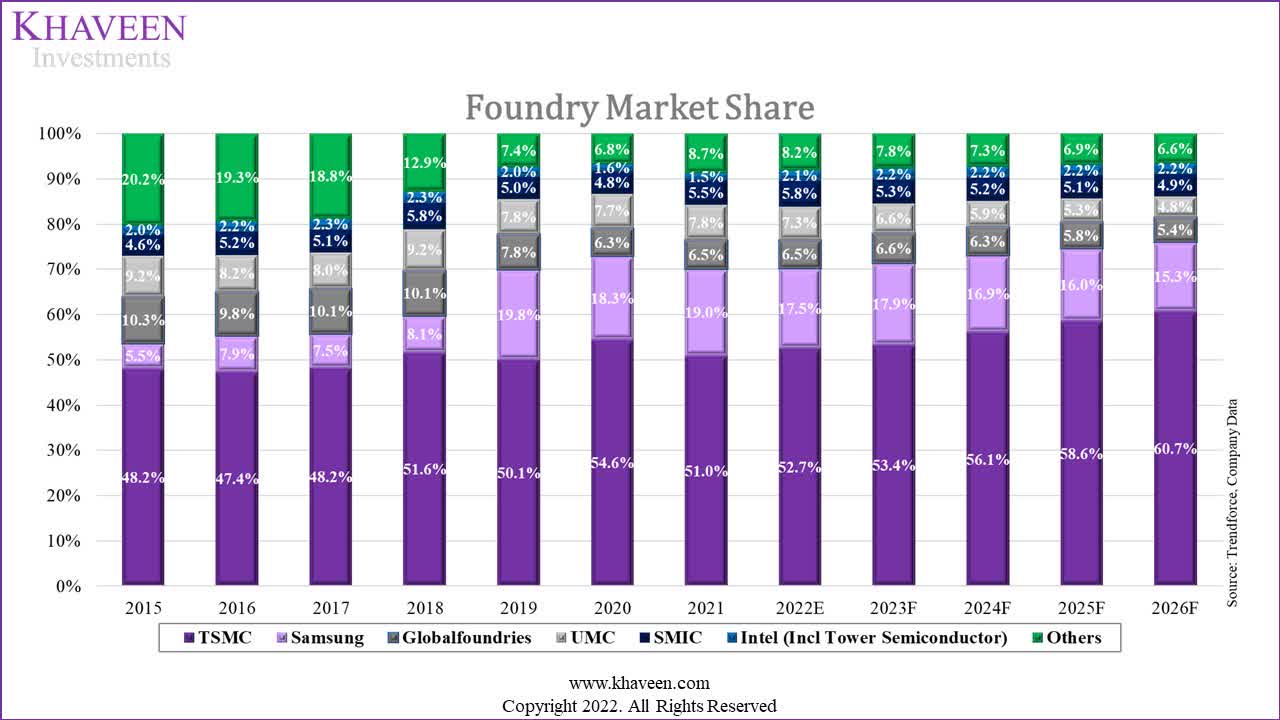

Trendforce, Company Data, Khaveen Investments

{kind=link}

Moreover, we analyzed the top 5 foundries in the semicon industry based on market share in the chart above. In terms of market share, TSMC retained its position as the leading foundry globally with a 52.7% share in 2022. This is followed by Samsung which lost its share in 2022 with a lower growth rate than the market. Besides that, GlobalFoundries and SMIC both gained share.

Furthermore, we compiled our revenue growth forecasts for the companies in the table below from previous analyses.

| Foundry Market Revenue ($ mln) |

| 2023 Pricing Growth % |

| 2023 Shipment Growth % |

| 2023 Growth Forecast % |

| TSMC |

| 4.5% |

| 10.19% |

| 15.1% |

| Samsung |

| 7% |

| 8.76% |

| 16.4% |

| GlobalFoundries |

| -0.6% |

| 17.4% |

| 16.7% |

| UMC |

| 0% |

| 2.8% |

| 2.8% |

| SMIC |

| 4.6% |

| 0.1% |

| 4.7% |

| Average |

| 11.2% |

Source: Khaveen Investments

Based on the table, we forecasted the foundries' growth to slow in 2023 with a lower average of 11.2% compared to 27.7% in 2023. In terms of the companies:

- For Samsung, we expect its foundry revenue growth to be supported by capacity growth of 8.76% and to benefit from the CHIPS Act with an estimated 39.4% share of subsidies as it plans to expand manufacturing in the US with planned investments of $192.1 bln over the next 20 years in Texas

- For TSMC, we forecasted its wafer revenue to grow by 15.1% in 2023 as we forecasted its capacity growth of 10.19% in 2023 based on our capex projections for the company and pricing growth of 4.5% based on the reported pricing growth of 3% to 6% in 2023 which is lower than the pricing increase of over 20% in 2022.

- For GlobalFoundries, we believe its growth to be driven by its partnership with STMicro (STM) for its European foundry expansion and we forecasted its capacity growth of 17.4% in 2023 as part of the European Chips Act.

- For SMIC, we expect the company’s growth to slow in 2023 with our forecasted capacity growth of 2.8% accounting for an estimated impact by the US trade restrictions of semicon equipment sales to the company which we previously estimated a revenue impact of 10.1% for the company.

- For UMC, we expect its growth to be only 2.8% in 2023 supported by capacity growth of 2.8% which we forecasted based on its planned capacity expansions in Taiwan and Singapore.

Overall, we expect the top 5 foundries to have a lower average growth forecast in 2023 of 11.2%. This is as we forecasted lower pricing growth for the companies. Additionally, as the foundries were operating at near maximum capacities in 2022, we forecasted limited shipment growth based on capacity growth supported by their planned capacity expansions and our capex projections. Also, in terms of planned expansions, most of the announced new facilities by TSMC, Samsung and Intel are only expected to be completed in 2024.

Lower Customers’ Capex to Impact Equipment Makers’ Outlook

| Semiconductor Equipment Market |

| 2020 |

| 2021 |

| 2021 Growth % |

| 2022 |

| 2022 Growth % |

| Our FY2022 Forecasts |

| Country |

| ASML ( ASML ) |

| 17,076 |

| 21,183 |

| 24.0% |

| 22,113 |

| 4.4% |

| 8.4% |

| Netherlands |

| Tokyo Electron ( TOELF ) |

| 12,428 |

| 16,319 |

| 31.3% |

| 16,595 |

| 1.7% |

| N/A |

| Japan |

| Applied Materials |

| 18,202 |

| 24,172 |

| 32.8% |

| 26,253 |

| 8.6% |

| 17.0% |

| US |

| Lam Research |

| 11,929 |

| 16,524 |

| 38.5% |

| 19,048 |

| 15.3% |

| N/A |

| US |

| KLA |

| 6,073 |

| 8,166 |

| 34.5% |

| 10,484 |

| 28.4% |

| 37.2% |

| US |

| Average |

| 32.2% |

| 11.7% |

| 20.9% |

Source: Company Data, Khaveen Investments

Finally, the average growth for the top 5 companies was significantly lower compared to the 2021 growth rate. All companies had lower growth while ASML was the only company among the top 5 to have negative growth. Moreover, compared to 2022, our FY2022 forecast growth for the equipment makers was higher. Companies such as ASML , Tokyo Electron and Applied Materials were impacted by supply chain disruptions in 2022 as covered in our previous analyses.

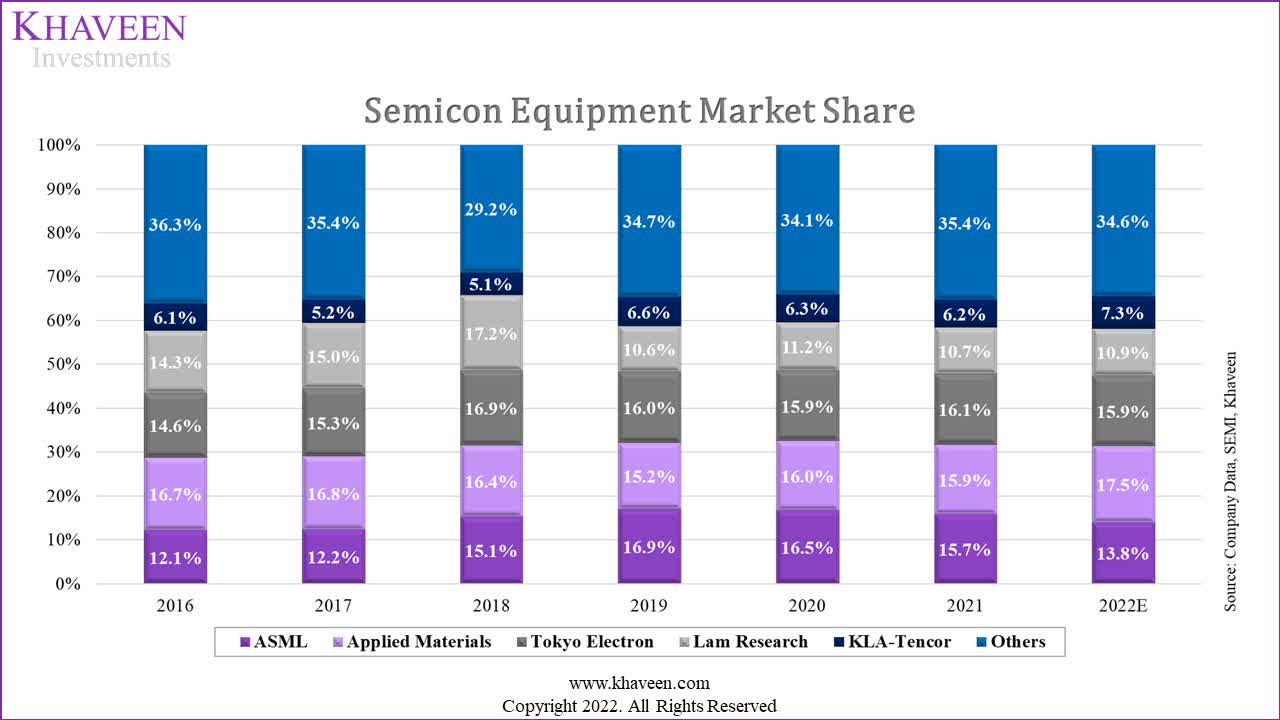

Company Data, SEMI, Khaveen Investments

{kind=link}

In terms of market share, Applied Materials had cemented its position as the leading equipment maker in 2022 ahead of Tokyo Electron and ASML. Additionally, both Lam Research and KLA gained market share with their strong growth rates.

| Memory Capex |

| 2021 |

| 2022 |

| 2023F |

| 2024F |

| 2025F |

| 2026F |

| Samsung |

| 16,060 |

| 13,435 |

| 13,435 |

| 13,435 |

| 13,435 |

| 13,435 |

| Micron |

| 10,589 |

| 12,067 |

| 8,273 |

| 16,677 |

| 17,513 |

| 19,229 |

| SK Hynix |

| 10,905 |

| 12,874 |

| 12,651 |

| 15,726 |

| 17,859 |

| 20,283 |

| Total |

| 37,554 |

| 38,376 |

| 34,359 |

| 45,837 |

| 48,807 |

| 52,947 |

| Growth |

| 2.2% |

| -10.5% |

| 33.4% |

| 6.5% |

| 8.5% |

| Foundry and Logic Capex |

| 2021 |

| 2022 |

| 2023F |

| 2024F |

| 2025F |

| 2026F |

| TSMC |

| 30,153 |

| 35,219 |

| 37,034 |

| 39,462 |

| 40,692 |

| 40,382 |

| Samsung |

| 4,730 |

| 3,957 |

| 3,957 |

| 3,957 |

| 3,957 |

| 3,957 |

| Intel |

| 25,167 |

| 25,050 |

| 25,000 |

| 30,370 |

| 31,979 |

| 33,329 |

| Total |

| 60,050 |

| 64,226 |

| 65,991 |

| 73,789 |

| 76,628 |

| 77,668 |

| Growth |

| 7.0% |

| 2.7% |

| 11.8% |

| 3.8% |

| 1.4% |

Source: Company Data, Khaveen Investments

We previously forecasted the top memory and foundry & logic chipmakers to forecast the growth of the equipment market based on the memory and foundry & logic segments. We expect the memory market customers' capex to decline in 2023 by 10.5% as Micron and SK Hynix announced their plans to cut capex this year. However, we expect the memory capex to recover to positive growth in 2024. Additionally, we expect Logic customers' capex growth to decline to 2.7% compared to 7% in the prior year with lower capex for Intel.

| Semiconductor Equipment Market |

| 2023 Forecast % |

| ASML |

| 8.5% |

| Tokyo Electron |

| 8.7% |

| Applied Materials |

| 1.0% |

| Lam Research |

| -4.4% |

| KLA |

| 6.1% |

| Average |

| 4.0% |

Source: Khaveen Investments

Overall, for the equipment makers, we expect the companies to have lower average growth for 2023 at 4% based on our previous analyses. For the top companies:

- In our ASML analysis, we expect the company’s growth to be supported by its Logic segment which accounted for the majority of its equipment revenue (70%) at 15.8% but was weighed down by its Memory segment with the planned capex cuts from memory chipmakers at a decline of 10.3% but only accounting for 30% of revenue.

- For Lam Research, we expect the company growth to decline by 4.4% in 2023 based on our Logic and Memory capex forecasts of 4.8% and -10.3% in 2023 respectively as the company’s memory segment is the largest representing 61% of revenue compared to logic at 39% of revenue.

- For Tokyo Electron, we believe the company’s logic segment which represented 52% of revenue could support its growth at 10.9% and outperform its memory segment growth in 2023.

- For Applied Materials, we expect the company’s growth to be flattish with a growth of 1% weighed down by its exposure to the memory segment which accounted for 34% of system revenue.

- For KLA, as the process control market leader, we expect its equipment revenue growth to be supported by the process control market growth forecast of 6.1%.

Overall, we expect the top equipment makers to have a lower average growth outlook in 2023 at only 4% as we expect the planned top memory makers’ capex cuts from Micron and SK Hynix to weigh down on their memory segment growth as well as a lower foundry and logic capex growth of 2.7% in 2023.

Risk: PC End Market Weakness

Following the decline in the PC market in 2022 with full-year growth of -16.5% for the top 5 PC makers by the IDC, the PC market is expected to continue declining in 2023 by the IDC at -6.5%. According to the IDC, the PC market is expected to...

continue to be challenged by macroeconomic headwinds, excess channel inventory, and high levels of saturation. - IDC

Based on the SIA, the PC end market is the largest market for semiconductors as it represented 31.5% of sales in 2021 followed by smartphones at 30.7%. Thus, we believe this could pose growth headwinds for the semiconductor industry in 2023.

Valuation

Overall, we expect the growth of chipmakers could recover in 2023 driven by several factors:

- Data center: We expect from our previous analyses the cloud infrastructure market growth to continue to be driven by increasing data volume at a forecasted rate of 30.5% through 2026 leading to our cloud market growth projection at a 5-year average of 38.1%, which we believe could continue benefiting companies such as Broadcom (networking), Nvidia (GPUs), Intel (CPU) and AMD (CPU and GPUs).

- 5G : In the smartphone market, we previously forecasted the continued shift towards 5G devices and forecasted the share of 5G shipments to continue rising to 58% in 2023 and 69% by 2025, which we believe is a tailwind for Qualcomm and MediaTek as we expect their growth to continue to be supported by the shift to 5G.

- Recovery in Market Pricing : For memory chipmakers, we expect the memory market to supply growth to be 9.5% and 19.8% lower than demand for DRAM and NAND respectively as Micron and SK Hynix scale back on expansion plans and we believe this could lead to a recovery opportunity for market pricing.

- Automotive : For automotive markets, we expect Qualcomm, Nvidia, and Intel to continue benefitting from the AV market growth at a forecasted CAGR of 31.3% with their ADAS product portfolios as well as DAO companies such as Texas Instruments in power semiconductors and Samsung in automotive LEDs.

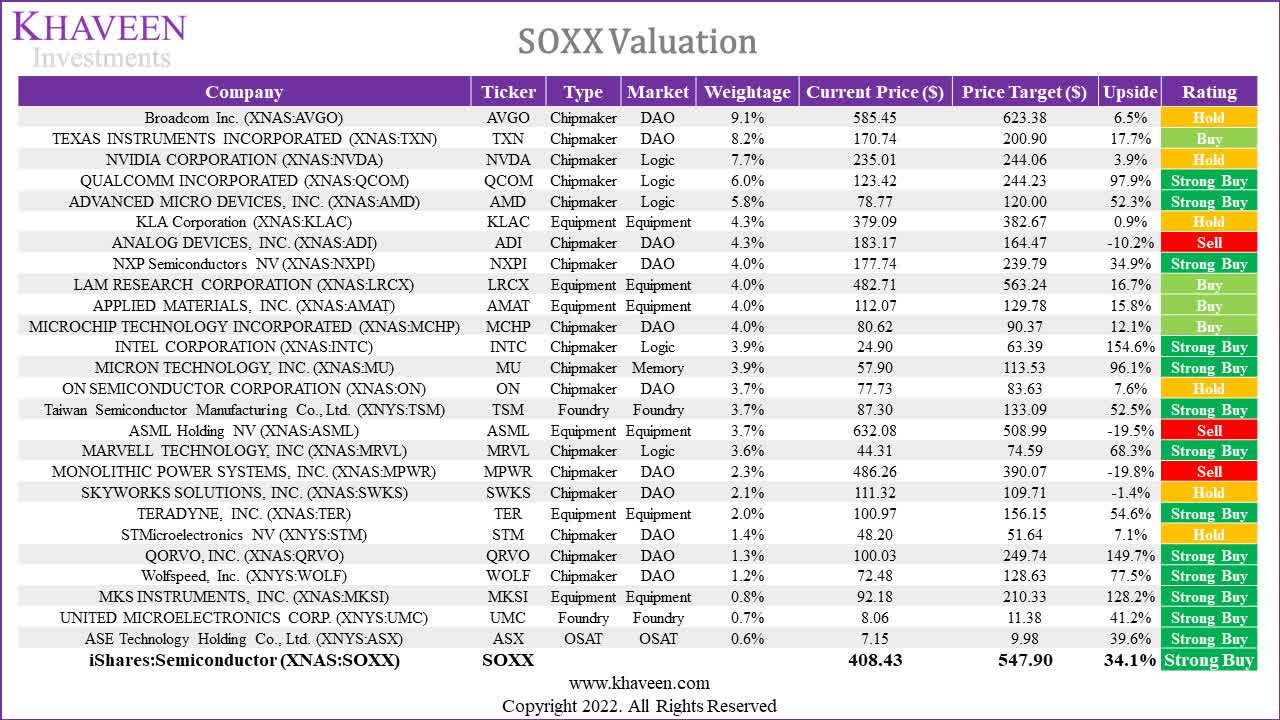

{kind=link}

To value the SOXX, we derived a weighted average upside based on the breakdown of its holdings and our price targets from previous analyses for companies that we covered and analyst consensus price targets for the remaining companies. Based on the chart, 67% of the holdings above have a rating of Buy and Strong Buy and 22% with a Hold rating. In terms of company type, 59% of chipmakers and 60% of equipment companies have a Buy and Strong Buy rating. Both TSMC and UMC have Strong Buy ratings. By chipmaker markets, 80% of logic chipmakers and 45% of DAO companies have a Buy and Strong Buy rating. Overall, we derived a weighted average upside of 34.1% for SOXX.

Verdict

In our analysis of the semiconductor industry, we conducted a comprehensive review of the top 10 semiconductor holdings in SOXX, examining their performance in 2022 based on their revenues. Our analysis revealed a mismatch between the decline in the average stock prices of the top 10 semicon companies, which declined by 30%, and the industry's massive revenue growth of 22%.

However, we forecasted the top chipmakers' growth to recover in 2023, with a positive growth forecast for all companies across DAO, Logic, and Memory markets. We identified several factors affecting the growth outlook of the top chipmakers, foundries, and equipment makers, and we believe that Broadcom's Networking segment has significant potential for revenue growth. We also see growth potential for Texas Instruments in 2023, through supply growth fulfilling demand and the CHIPS Act supporting its capacity expansion. We expect Nvidia's growth to continue to be driven by its Data center segment due to the rising data volumes in the cloud market and its expansion into Enterprise AI software and data center CPU. Qualcomm's growth is expected to be driven by the shift of smartphones to 5G. Lastly, our analysis of Micron, Samsung, and SK Hynix indicates that their revenue growth could be supported by a lower supply growth outlook compared to demand growth, which could buoy market pricing.

However, we forecast a lower growth outlook for the foundries in 2023 of 11.2%, as we expect lower pricing growth for the companies. Additionally, we expect the top equipment makers to have a lower average growth outlook in 2023 at only 4%, as we expect the planned top memory makers' capex cuts from Micron and SK Hynix to weigh down on their memory segment growth and lower foundry and logic capex growth in 2023.

Based on our price targets of the SOXX holdings, we derived an upside of 34.1% with a target price of $547.90 from the weighted upside of our price targets. Thus, we rate SOXX as a Strong Buy.

For further details see:

SOXX: Semicon Industry 2023 - Full Steam Ahead