CECO - SP Plus: A Disconnect Between Fundamentals And Share Price Performance

Summary

- SP Plus continues to post strong growth when it comes to sales, profits, and cash flows.

- Even so, shares of the business have languished, likely because of broader economic concerns.

- But between this fundamental performance and how cheap shares are, the company makes for a compelling opportunity at this time.

In an ideal world, when the broader market rises, you would expect the companies that are most undervalued and healthy to see upside that is at least as great as the market, if not greater. But unfortunately, markets can be irrational from time to time, especially in the short run. One really good example of market irrationality in recent months, in my opinion, can be seen by looking at SP Plus ( SP ). This firm is a fairly diverse player, with operations centered around on-street parking meter collection and other parking enforcement services, as well as on-remote monitoring services, shuttle bus services, taxi and livery dispatch services, and more. Fundamentally speaking, the business has been doing quite well as of late. I also previously identified the firm as an undervalued play with attractive upside potential. For much of the time I have been following the company, my calls on it have proven to be right. But recently, the company has found itself underperforming the market. For investors who believe in the long-term outlook for the company, this could be a good time to consider buying in.

A niche play at a good price

Back in late October of 2022, I wrote an article discussing whether or not it still made sense to consider SP Plus as a valid opportunity. Up to that point, the company had continued to generate attractive fundamental growth and saw a nice increase in share price. The company was also flying high from a vote of confidence made by management when management announced that they were increasing guidance for 2022. Add on top of this the fact that shares of the company we're trading on the cheap, and I ultimately concluded that it made for a good ‘buy’ opportunity. Since then, however, things have not gone the way I would have anticipated. While the S&P 500 is up 6.9%, shares of SP Plus have generated upside of only 0.8%. Although this is disappointing, it is worth noting that since I first rated the company a ‘buy’ back in April of last year, shares are up 23.4% compared to the 8.5% drop the S&P 500 experienced.

{kind=link}

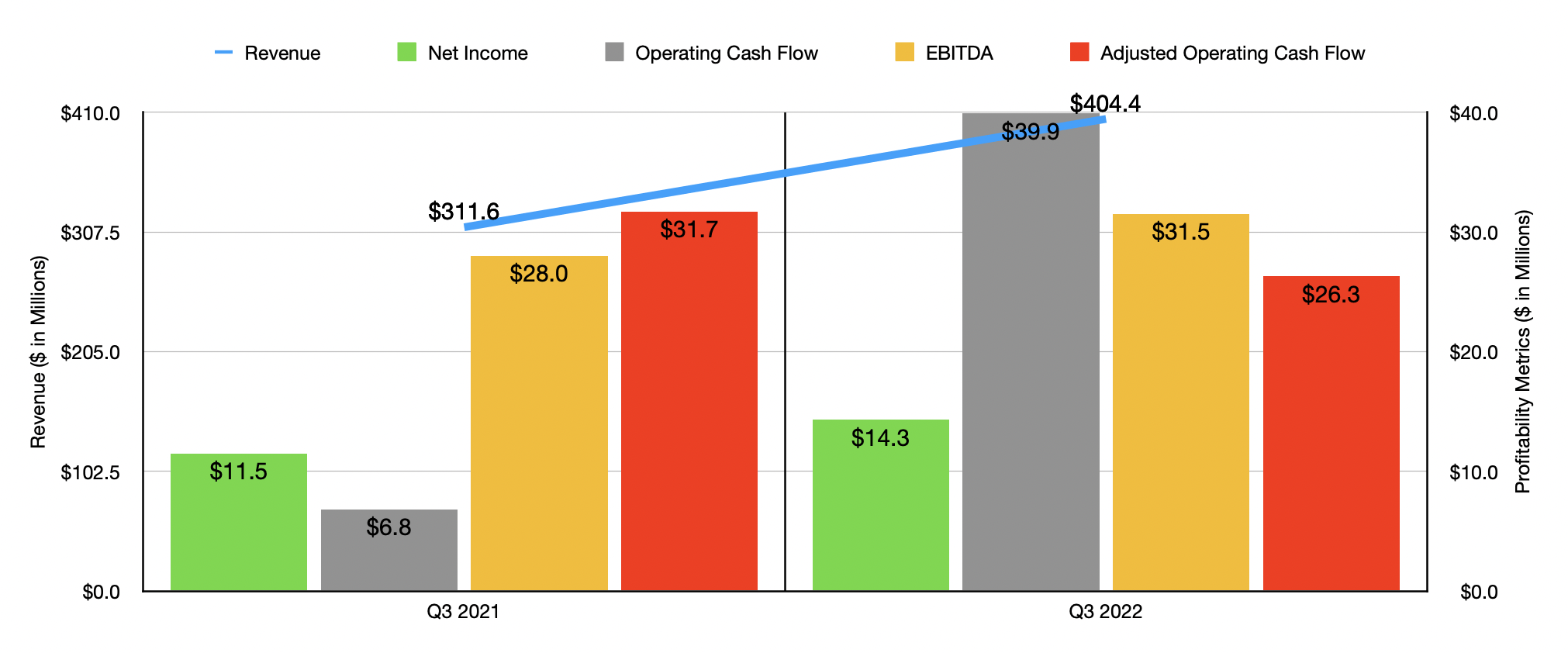

Based on the recent return disparity achieved in the market, you might think that fundamental performance generated by SP Plus was anything less than impressive. But this wouldn't be the case. Consider financial results covering the third quarter of the company's 2022 fiscal year. This is the only quarter for which new data is available that was not available when I last wrote about it. Sales during that time came in at $404.4 million. That's 29.8% higher than the $311.6 million reported the same time one year earlier. Services revenue for the company shot up 28.2% year over year, rising from $161.6 million to $207.1 million. The biggest improvement here came from service revenue associated with management-type contracts. This jumped by $33 million, or 32.4% overall, thanks largely to an increase in volume related to its baggage delivery businesses and volume-based management-type contracts stemming from improving business conditions. Higher volume related to other aviation services, as well as new business, also helped the company. Services revenue associated with its Aviation operations spiked 54.2%, largely as a result of airlines coming back to life following the COVID-19 pandemic. Under its Commercial operations, services revenue increased 17.9%. This demonstrates that other aspects of the company are certainly healthy.

{kind=link}

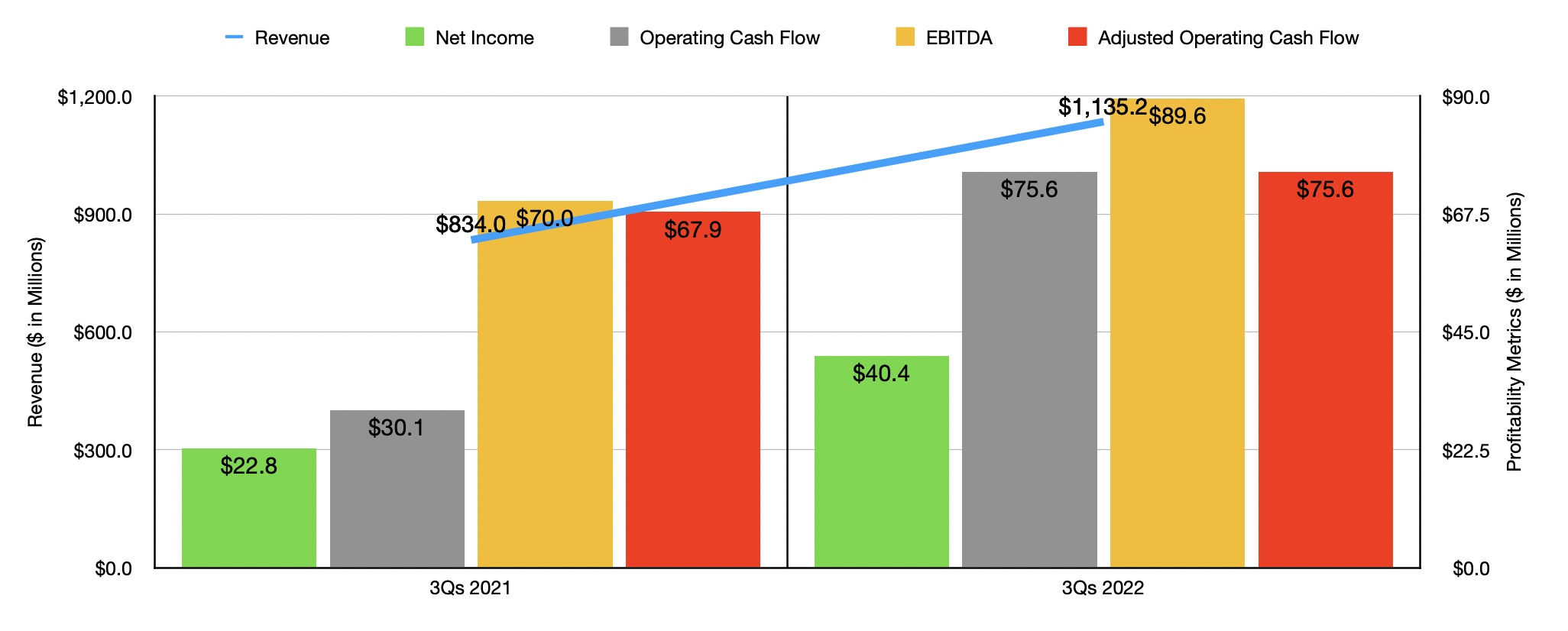

With the rise in revenue also came improved profitability. Net income of $14.3 million in the third quarter of 2022 beat out the $11.5 million reported the same time one year earlier. Operating cash flow surged, climbing from $6.8 million to $39.9 million. But if we adjust for changes in working capital, it would have worsened slightly from $31.7 million to $26.3 million. Fortunately, this was offset by EBITDA, which rose from $28 million to $31.5 million. The results experienced in the third quarter of 2022 were in no way a one-time thing. For the first nine months of 2022 in its entirety, sales came in at a robust $1.14 billion. This is 36.1% higher than the $834 million reported one year earlier. In this case, services revenue for the company expanded 36.3% year over year, while reimbursed management-type contract revenue jumped nearly 36%. With the rise in sales also came a rise in profits. Net income nearly doubled from $22.8 million to $40.4 million. Operating cash flow more than doubled from $30.1 million to $75.6 million. But if we adjust for changes in working capital, it would have risen more modestly from $67.9 million to $75.6 million. Meanwhile, EBITDA for the company expanded from $70 million to $89.6 million.

{kind=link}

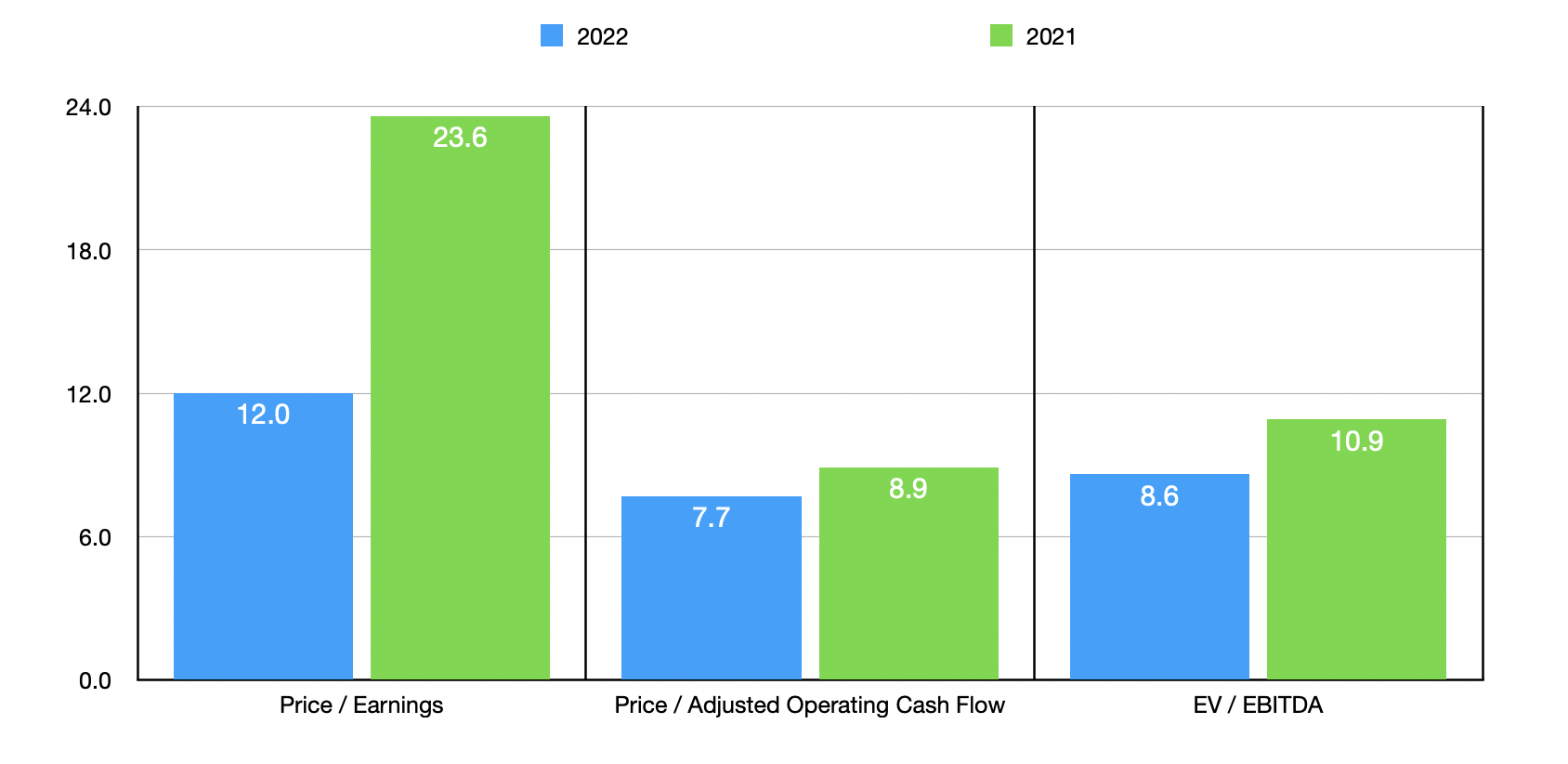

When it comes to 2022 in its entirety, management has provided a good deal of guidance . At present, the company is forecasting net income of between $60 million and $65 million. Operating cash flow should be between $90 million and $104 million, while EBITDA should come in somewhere between $115 million and $125 million. Using the midpoint estimates from these numbers, I calculated that the company is trading at a price-to-earnings multiple of 12, at a price to adjusted operating cash flow multiple of 7.7, and at an EV to EBITDA multiple of 8.6. By comparison, if we were to use the data from 2021, these multiples would be 23.6, 8.9, and 10.9, respectively. As part of my analysis, I decided to compare the company to five similar firms. On a price-to-earnings basis, the four companies with positive results ranged from a low of 11.6 to a high of 1,550. When it comes to the EV to EBITDA approach, the range for the five firms was from 7.3 to 18. In both cases, only one of the five companies was cheaper than SP Plus. Meanwhile, using the price to operating cash flow approach, the range was from 3.9 to 21.2. In this scenario, three of the five companies were cheaper than our target.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| SP Plus |

| 12.0 |

| 7.7 |

| 8.6 |

| Heritage-Crystal Clean ( HCCI ) |

| 11.6 |

| 10.1 |

| 7.3 |

| Harsco ( HSC ) |

| N/A |

| 3.9 |

| 14.3 |

| CECO Environmental Corp. ( CECO ) |

| 45.9 |

| 21.2 |

| 18.0 |

| BrightView Holdings ( BV ) |

| 47.9 |

| 7.3 |

| 9.2 |

| Aris Water Solutions ( ARIS ) |

| 1,550.0 |

| 4.4 |

| 10.2 |

Takeaway

Fundamentally speaking, SP Plus is doing really well for itself right now. In the long run, I expect that kind of performance to continue. This on its own makes the company a worthwhile prospect. But when you add on top of that just how cheap shares are on an absolute basis and how affordable they are compared to similar firms, I cannot help but keep the ‘buy’ rating I had assigned to it previously.

For further details see:

SP Plus: A Disconnect Between Fundamentals And Share Price Performance