HSC - SP Plus: Fundamentals Say One Thing The Market Says Another

2023-06-01 17:00:27 ET

Summary

- SP Plus, a company that provides parking meter collection and other parking enforcement services, has seen strong growth in sales but a struggling stock price.

- Despite recent weakness in net income and operating cash flow, management forecasts significant growth in earnings per share and EBITDA for the 2023 fiscal year.

- The company's shares appear undervalued, and the author maintains a "buy" rating due to the positive outlook and attractive valuation.

I can't say for sure why, but I've always enjoyed writing about companies that have unique business models. Something about the novelty of a unique business appeals to me. You can imagine then why one of my favorite companies to write about is SP Plus ( SP ). For those who don't know, the company has a variety of services. But for the most part, it focuses on providing on street parking meter collection and other parking enforcement services. Examples of the 'other' in that statement include, but are not limited to, shuttle bus services, taxi and livery dispatch services, and more. In recent times, I have been quite bullish about the company. But over the past few months, the stock has really struggled. This is in spite of the fact that management is forecasting some rather attractive growth this year compared to last, and even though the stock is fundamentally cheap. Although current market conditions might deter some investors, I believe that these aforementioned facts are reasons why investors should consider the company an attractive opportunity.

Recent performance has been robust

The last article that I wrote about SP Plus was published in late January of this year. In that article, I talked about how the company had continued to post strong growth on both its top and bottom lines. But even in spite of that growth, shares were underperforming my expectations. But between the attractive growth and the low share price, I remained optimistic that the stock would outperform the broader market moving forward. And that was enough to lead me to rate the enterprise a 'buy'. Since then, the firm has continued to present me with a dichotomy. On one hand, fundamental performance continues to impress. But on the other hand, shares continue to underperform. Since the publication of the article, shares are actually down 1.6% at a time when the S&P 500 is up 4%.

{kind=link}

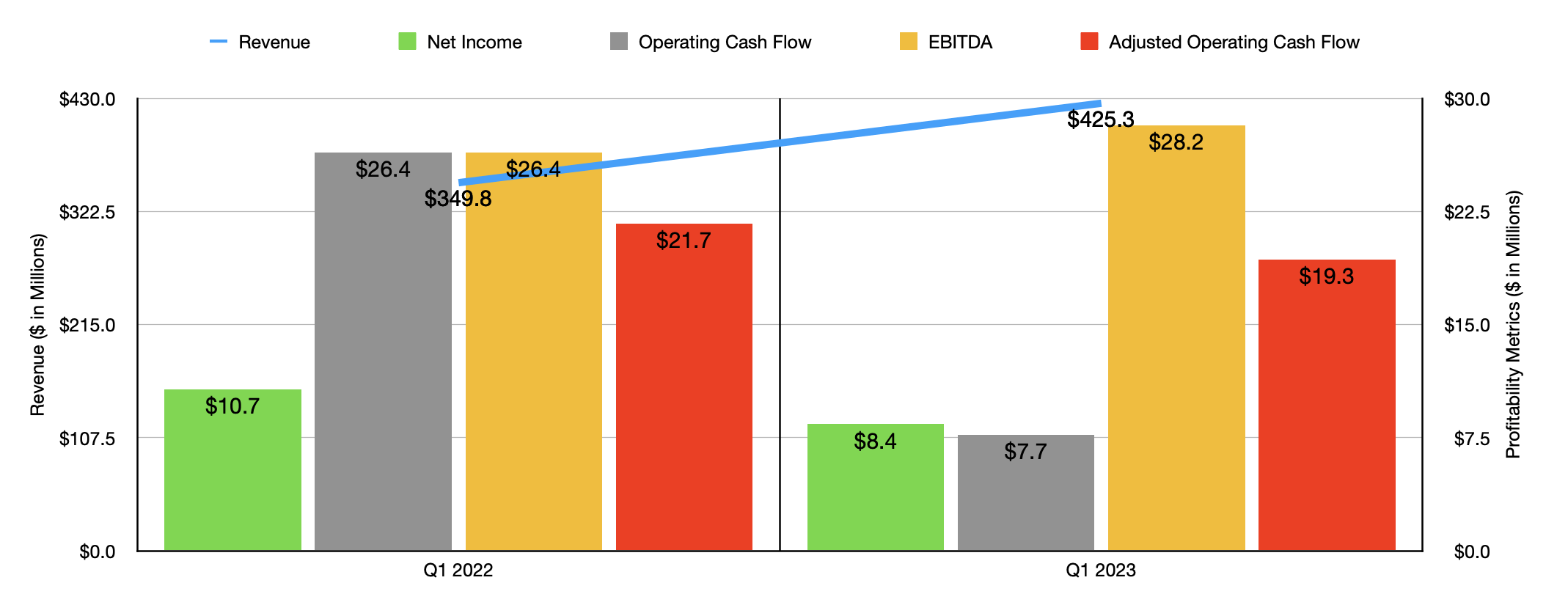

When I say that fundamental performance has been positive, I think it's important to note just how positive. Consider how the company performed during the first quarter of its 2023 fiscal year. During that time, sales came in at $425.3 million. That's 21.6% above the $349.8 million reported one year earlier. Most of this upside was driven by two primary activities. For starters, services revenue for management type contracts for the company jumped $26.3 million, or 21.6%. This was driven by an increase in volume related to its baggage delivery businesses and volume-based management type contracts, thanks to stronger business conditions more generally. Greater demand for aviation services, as well as new business and revenue from acquisitions, also helped the firm. Second, the company saw a nice improvement in reimbursed management type contract revenue. This was largely associated with some of the same factors that I mentioned for the other increase in sales.

Although revenue for the company increased nicely, the firm did experience a bit of weakness on its bottom line. Net income, for instance, came in at only $8.4 million for the quarter. That's down from the $10.7 million reported one year earlier. Operating cash flow also fell, dropping from $26.4 million to $7.7 million. Even if we adjust for changes in working capital, the metric would have dropped, declining from $21.7 million to $19.3 million. In fact, the only profitability metric that improved year over year in the first quarter was EBITDA. According to management, this came in at $28.2 million. This was up from the $26.4 million reported the same time last year.

{kind=link}

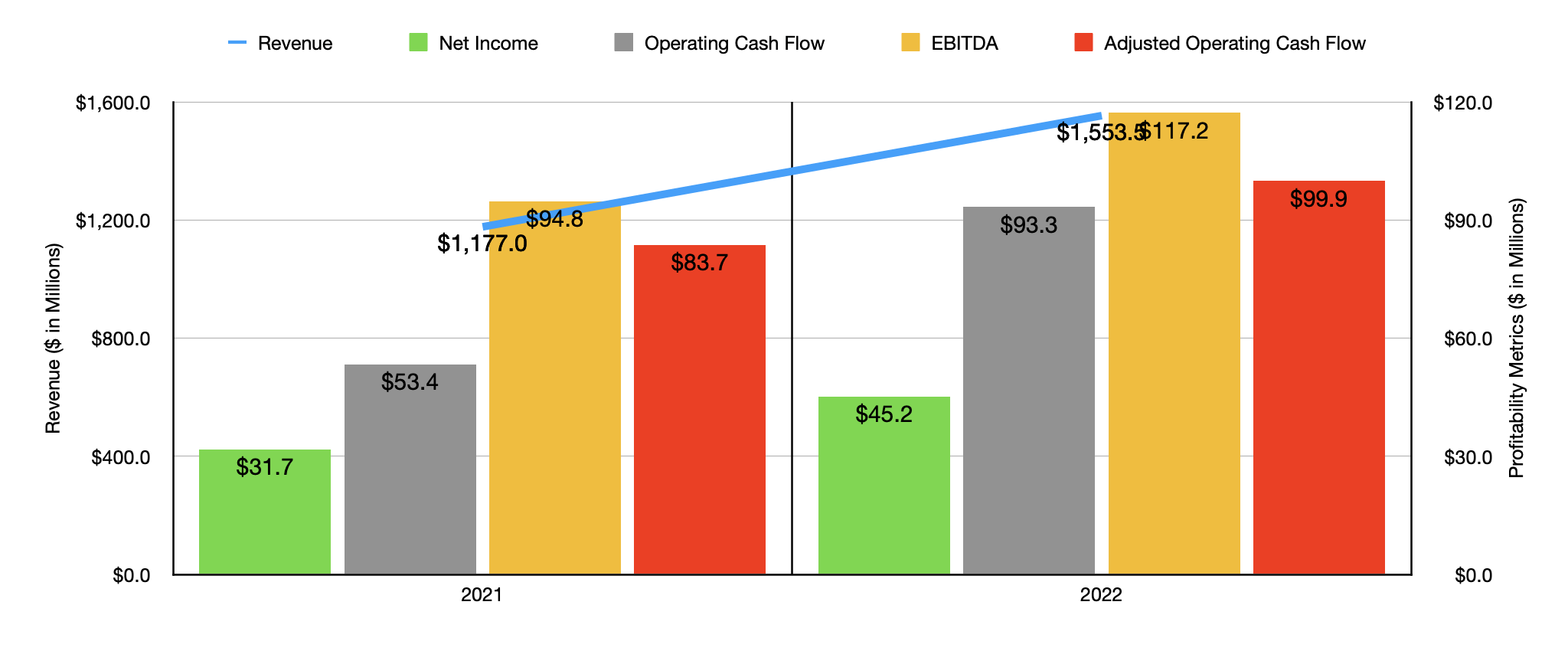

The nice increase in revenue for the company was not a one-time event. Although the decrease in profits was unexpected compared to what the company had achieved in the past. To see what I mean, we need to only look at the chart above, which looks at financial performance for both 2021 and 2022. Across the board, the company had a far better year last year than they did the year prior. Some investors may wonder if the weakness on the bottom line recently is indicative of the pain that lies ahead. But I would make the case that, more likely than not, this bottom line pain is truly transitory.

This isn't just me talking. This also comes from management itself. In its first quarter earnings release for the current fiscal year, the company said that this year is slated to be a great one for the firm. Unfortunately, management did not provide guidance when it came to revenue. But they did say that earnings per share should be between $2.70 and $3.20. At the midpoint, that would imply a net profit of $58.6 million. That's 29.6% above the $45.2 million reported last year. Meanwhile, EBITDA is forecasted to come in at between $125 million and $135 million. That stacks up nicely against the $117.2 million reported for 2022. No guidance was given when it came to other profitability metrics. But if we assume that adjusted operating cash flow should rise at the same rate that EBITDA is forecasted to, then we would expect a reading for the year of $110.8 million.

{kind=link}

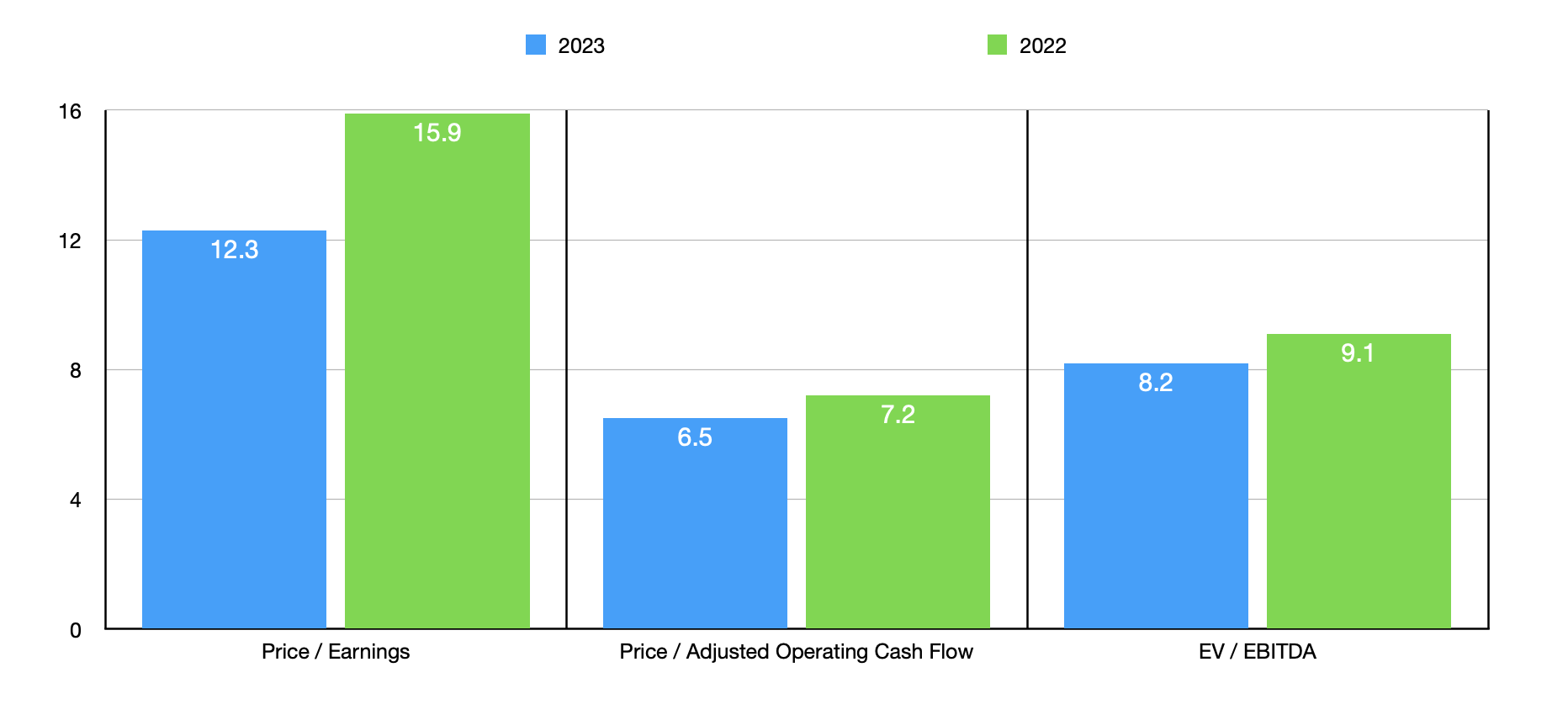

Assuming that these numbers come to fruition, the company looks quite cheap. As you can see in the chart above, the firm is trading at a forward price to earnings multiple of 12.3. The forward price to adjusted operating cash flow multiple is about half that at 6.5, while the EV to EBITDA multiple is about in the middle of the two at 8.2. These numbers are all more attractive than what we would get using data from 2022. But even using that data, shares look quite affordable. As part of my analysis, I also compared the company to five similar firms. As you can see in the table below, only one of the four companies that had positive multiples were cheaper than our prospect on a price to earnings basis. Using the price to operating cash flow approach, three of the five were cheaper, while using the EV to EBITDA approach, we end up with only two of the five being cheaper.

| Company |

| Price/Earnings |

| Price/Operating Cash Flow |

| EV/EBITDA |

| SP Plus |

| 12.3 |

| 6.5 |

| 8.2 |

| Heritage-Crystal Clean ( HCCI ) |

| 8.9 |

| 8.4 |

| 5.3 |

| Harsco Corp. ( HSC ) |

| N/A |

| 3.0 |

| 15.9 |

| CECO Environmental Corp. ( CECO ) |

| 21.9 |

| 21.1 |

| 12.3 |

| BrightView Holdings ( BV ) |

| 59.9 |

| 5.0 |

| 8.8 |

| Aris Water Solutions ( ARIS ) |

| 38.3 |

| 2.3 |

| 7.7 |

Takeaway

Truthfully, I feel a bit disappointed about how things have gone with SP Plus from a share price perspective in recent months. Even though the company experienced a bit of weakness in its bottom line, its overall financial condition is impressive and shares look incredibly cheap. Management is optimistic about what the 2023 fiscal year holds and, absent that change, I believe that the outlook for the company is positive. Given these factors, I've decided to keep the 'buy' rating I had on the company, even though the market has so far disagreed with me.

For further details see:

SP Plus: Fundamentals Say One Thing, The Market Says Another