SPTN - SpartanNash: A Margin Expansion Play

2023-11-22 09:51:52 ET

Summary

- SpartanNash's stock has performed poorly in the past year despite efforts to improve operations that have already achieved some results.

- The company operates with very thin margins that have gone well below a long-term average in 2022. A reversal in margins would improve the bottom line significantly.

- Further margin expansion from 2022 lows doesn't seem to be priced into the stock, providing investors with potentially high upside.

SpartanNash ( SPTN ) wholesales food products and operates brick-and-mortar stores. The company’s already thin margins have seen pressures in the past couple of years, deteriorating the bottom line as the company’s growth in real terms seems non-existent. Currently, SpartanNash is focusing on improving operations through multiple initiatives to recover the margin, which already has resulted in a partial recovery in margins. Still, the stock price doesn’t seem to have faith in a recovery, as SpartanNash’s stock has performed poorly in the past year:

{kind=link}

One-Year Stock Chart (Seeking Alpha)

SpartanNash’s Operations

SpartanNash wholesales food products and operates retail supermarkets. Of the segments, wholesale is SpartanNash’s most dominant part of the business with around 72% of revenues in 2022 according to the company’s Q3 presentation . The company wholesales to independent and chain grocery stores, retail brands, ecommerce clients, and military exchanges. On the retail side, SpartanNash operates 144 retail stores.

The company is most prominent in the northeast side of the United States in states such as Michigan, Wisconsin, Ohio, and Indiana, with operations also in nearby states and a third-party partnership with Coastal Pacific Food Distributors further away in California. The company’s geographical focus is a strategic decision to have efficient supply chains and overall distribution – in wholesale distribution, building an extensive network provides a significant amount of efficiencies.

A Margin Trajectory Reversal Is Needed

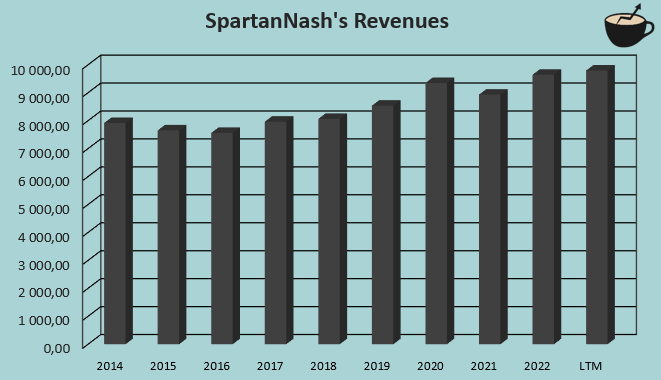

SpartanNash has achieved a very modest growth in past years. From 2014 to trailing figures as of Q3/2023, the company has achieved a compounded annual growth rate of 2.5% in revenues:

{kind=link}

Author's Calculation Using Seeking Alpha Data

The growth seems to be mostly on pace with inflation – SpartanNash can’t really be considered a growth stock despite a good growth of 8.0% in 2022. The company seems to have a larger focus on maintaining and optimizing current operations, rather than doing rapid expansion.

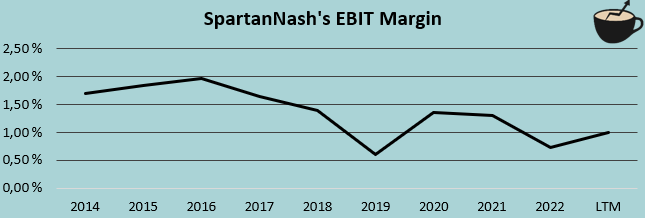

In my opinion, SpartanNash’s most critical factor is the company’s future margins. SpartanNash has historically operated with very thin margins, typical for wholesale operators. Worryingly, the already thin margin has seen pressure in recent years – the company’s average EBIT margin from 2014 to 2020 was 1.5%, but currently only stands at 1.0% with trailing figures.

{kind=link}

Author's Calculation Using Seeking Alpha Data

As the EBIT margin is very thin, the drop of half a percentage point represents a third of SpartanNash’s prior margins; a reversal of the trend could signify very much higher earnings. I see a potential margin recovery as a significant possible catalyst for SpartanNash’s stock.

The margin has already started recovering – the trailing EBIT margin is already up from a 2022 figure of 0.7%. In the recently reported Q3 results, SpartanNash’s EBIT margin rose year-over-year from a level of 0.8% to 1.1%. The margin still has room for improvement through SpartanNash’s operational initiatives.

SpartanNash’s Margin Initiatives

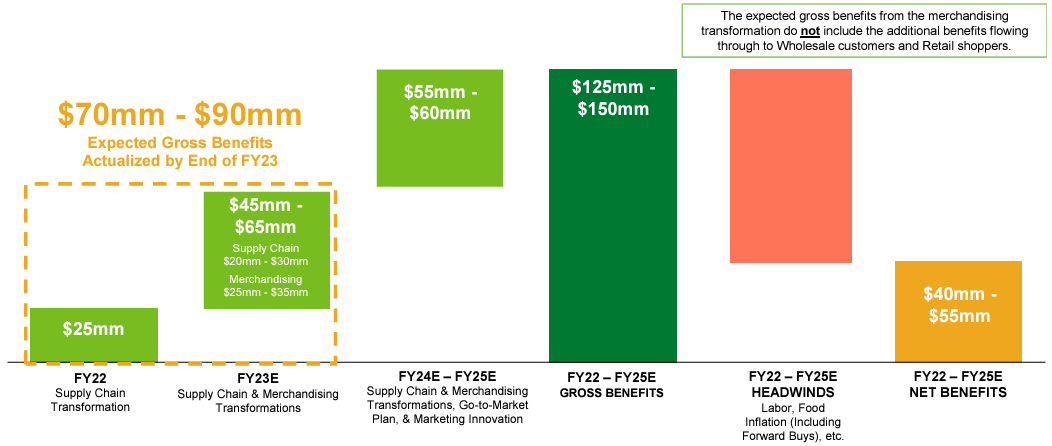

SpartanNash is focusing on its margins through a good cost management and improved operations. The company is naming supply chain and merchandising transformation, go-to-market plan change, and marketing innovation as ways to improve the bottom line:

{kind=link}

Cost Initiatives and Drivers (SpartanNash Q3 Presentation)

From FY2023, SpartanNash seems to be expecting benefits of $55 million to $60 million in costs through the initiatives. To me, the initiatives seem well thought-out. In the company's Q3 earnings call , CEO Tony Sarsam commented the following concerning the cost management:

" This [cost management] program is accelerating our customer-led capabilities in the following areas: one, simplifying the assortment using advanced analytics; two, showcasing the power of our OwnBrands; three, reducing cost to serve in our warehouses and stores; four, improving in-stocks for shoppers; and five, creating an easier to navigate planogram. "

Most notably in the quote, the improvements in assortment from analytics and warehouse and store cost reductions seem like promising alleys to improve profitability. I would believe that the cost initiatives are likely to realize, although it is unsure if they will be completed at the communicated level resulting in such extensive savings.

If achieved, the communicated improvements of $55 million to $60 million would signify a very good growth in SpartanNash’s bottom line - with a trailing EBIT of $97 million, the cost cuts would result in a massive upside to earnings. Investors should keep a very close eye on the company’s cost side going forward, monitoring the progress on the communicated initiatives.

Valuation

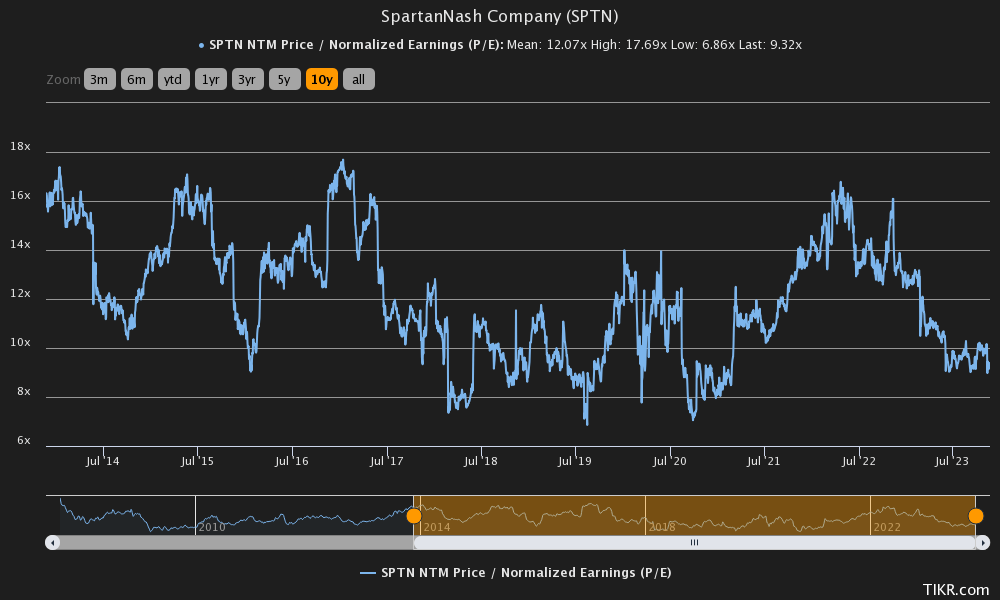

Currently, SpartanNash trades at a forward P/E of 9.3, below the stock's ten-year average of 12.1:

{kind=link}

Historical Forward P/E (TIKR)

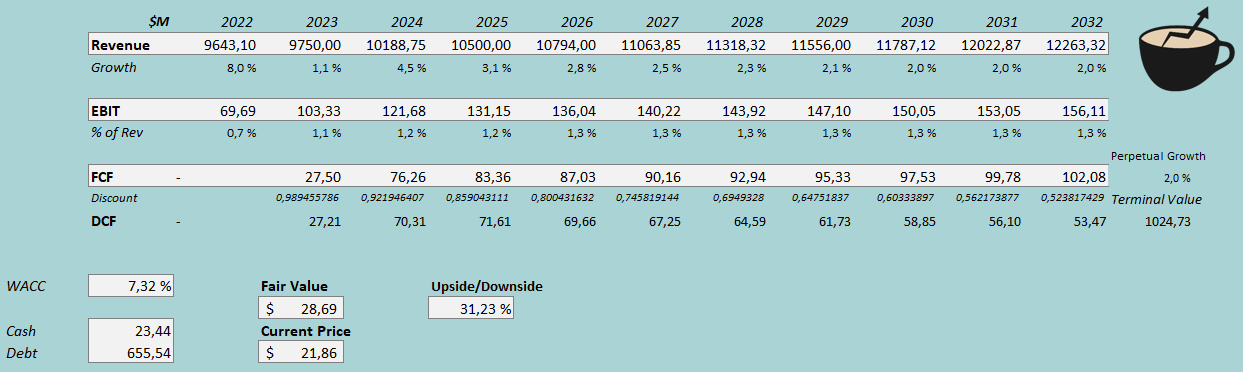

To get a better understanding of SpartanNash's valuation, I constructed a discounted cash flow model. In the model, I follow SpartanNash’s guidances for 2023 and 2025 in terms of revenues – for the years, I estimate revenues of $9.75 billion and $10.5 billion respectively, in line with SpartanNash’s communicated figures. After 2025, I estimate the growth to slow down in steps into a perpetual growth rate of 2%. The estimated growth is in line with SpartanNash’s history – I don’t see any significant catalysts that could significantly alter SpartanNash’s revenue performance from the company’s history.

For SpartanNash’s EBIT margins, I estimate some leverage as the company focuses on improving operations. From a 2023 estimate of a 1.1% EBIT margin, I estimate 0.2 percentage points of operating leverage into a margin of 1.3%, achieved in 2026. I believe that this estimate is a fair baseline assumption for the company at this point – the achieved figure could still be lower due to inflation, or higher if the improvements are executed very well. SpartanNash has a mostly good cash flow conversion, although the company’s capital expenditures are currently rising due to the initiatives.

With the mentioned estimates along with a cost of capital of 7.32%, the DCF model estimates SpartanNash’s fair value at $28.69, around 31% above the stock price at the time of writing. If SpartanNash continues to execute on margin expansion into near its historical levels, the stock seems to have a significant undervaluation.

{kind=link}

DCF Model (Author's Calculation)

The used weighed average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

In Q3, SpartanNash had $9.3 in interest expenses. With the company’s current amount of interest-bearing debt , SpartanNash’s annualized interest rate comes up to 5.66%. SpartanNash uses a good amount of debt in its financing – I estimate that the company’s long-term debt-to-equity ratio will be 30%.

For the risk-free rate on the cost of equity side, I use the United States’ 10-year bond yield of 4.44% . The equity risk premium of 5.91% is Professor Aswath Damodaran’s latest estimate for the United States, made in July. Yahoo Finance estimates SpartanNash’s beta at a figure of 0.66 – grocery stores and food wholesale is quite defensive, making SpartanNash’s operations mostly stable despite a high amount of debt. Finally, I add a small liquidity premium of 0.3%, crafting a cost of equity of 8.64% and a WACC of 7.32%.

Risks

The investment case for SpartanNash doesn't come without risks. Most importantly, the company's margin initiatives failing could signify a very poor result for investors - with an EBIT margin of 1.0% in 2024 and forward, my DCF model would indicate a downside of -20% for the stock instead of the significant upside. The cost improvements that could result in higher margins are met with headwinds due to inflation, making the margin recovery uncertain - higher buying prices and overall cost level could hit SpartanNash's bottom line significantly, making the investment case volatile.

Although I believe that SpartanNash's debt is on a healthy level considering the company's mostly stable operations, the company's held debt should be noted. With trailing figures, interest expenses cover around 39.4% of SpartanNash's operating income - a rise in held debt, rising interest rates for the company, or lower earnings would quickly eat away shareholders' equity value due to the leverage.

Takeaway

As an investor in SpartanNash, I would keep a close eye on the company’s margins in the future. Improved margins could signify a very good return for investors in a couple of years. On the other hand, if the margins don’t improve, the stock doesn’t seem too appetizing at the current price. With a baseline long-term EBIT margin estimate of 1.3%, the stock seems to have a good amount of undervaluation – at the moment, I see SpartanNash’s risk-to-reward quite favorable, constituting a buy rating at the current price.

For further details see:

SpartanNash: A Margin Expansion Play