USFD - SpartanNash Company: Still Attractive On Growth Though An Emphasis On Retail Would Be Wise

2023-04-05 10:08:47 ET

Summary

- SpartanNash Company has had some mixed results recently, though sales and some cash flow figures have fared well.

- The stock also looks cheap, both on an absolute basis and relative to similar firms.

- Management is focused on growth, but the real opportunity will come from the firm's Retail operations if management focuses there.

Whether it's food that you eat at home, or food that you eat at a restaurant, the journey that the product in question takes from where it originates to where it ends is a fascinating one. In a sense, that journey represents the massive improvement that the human race has come over the past few centuries. We have gone from subsistence living to something far greater. And along the way, we have developed massive networks to help to drive costs down while simultaneously resulting in even greater capacity for the production of food. One of the companies that's focused heavily on food distribution, both from a wholesale perspective and a retail perspective, is SpartanNash Company (SPTN).

Although the past year or so has not been particularly great from a shareholder return perspective, the company has outperformed the broader market. This outperformance can be chalked up to continued revenue growth and mixed but generally positive cash flow data. I would make the case, however, that the firm's outperformance can continue for the foreseeable future. At the moment, shares of the company are cheap on both an absolute basis and relative to similar firms. And moving forward, management's growth plans should help to create additional value for investors. Ultimately, I remain bullish on the company from a fundamental perspective. Though I also feel compelled to point out that the real growth opportunity comes from an emphasis on the firm's Retail operations.

Great performance and cheap shares

The last article that I wrote about SpartanNash was published in the middle of February of 2022. Over a year ago, I recognized that the company had a nice track record when it came to growth, even though the 2021 fiscal year had proven somewhat difficult. The attractive cash flows generated by the company, as volatile as they could be, resulted in shares trading on the cheap. This led me to be bullish about the company and to rate the business a 'buy' to reflect my view at the time that shares should outperform the broader market for the foreseeable future. Since then, the company has done just that, even if the performance has not been ideal. While the S&P 500 has dropped 7.4%, shares of SpartanNash have seen downside of only 4.9%.

{kind=link}

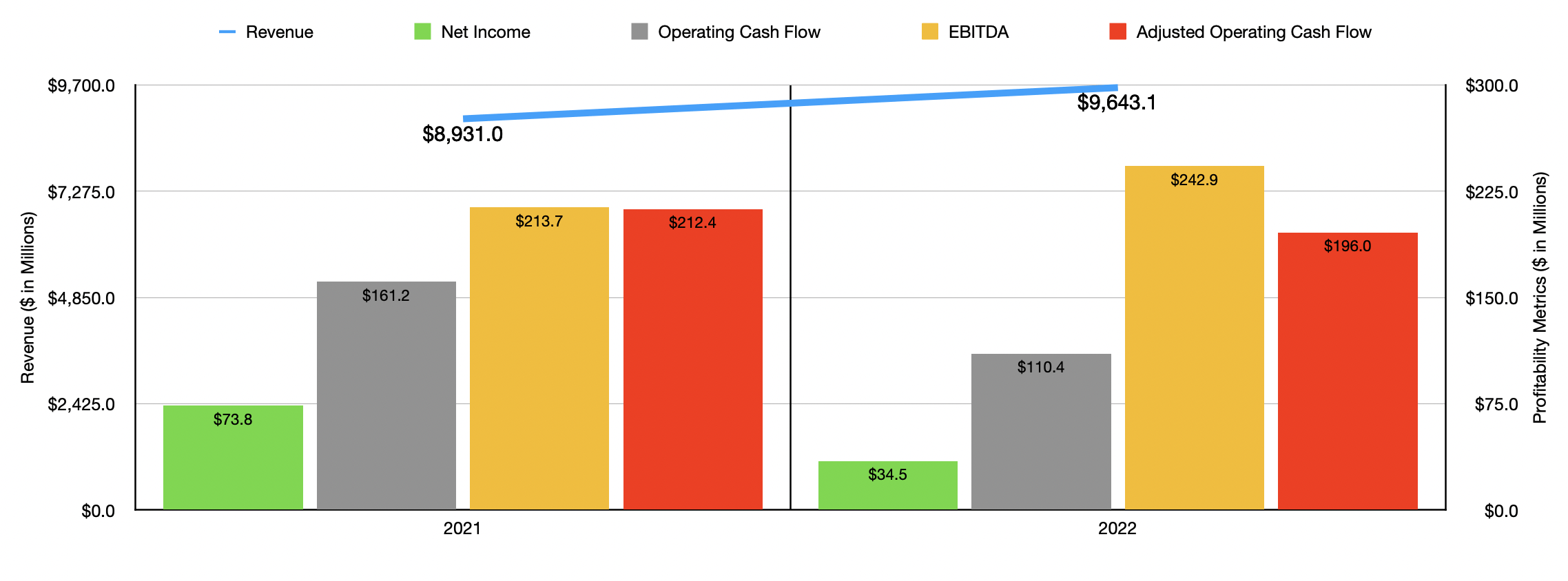

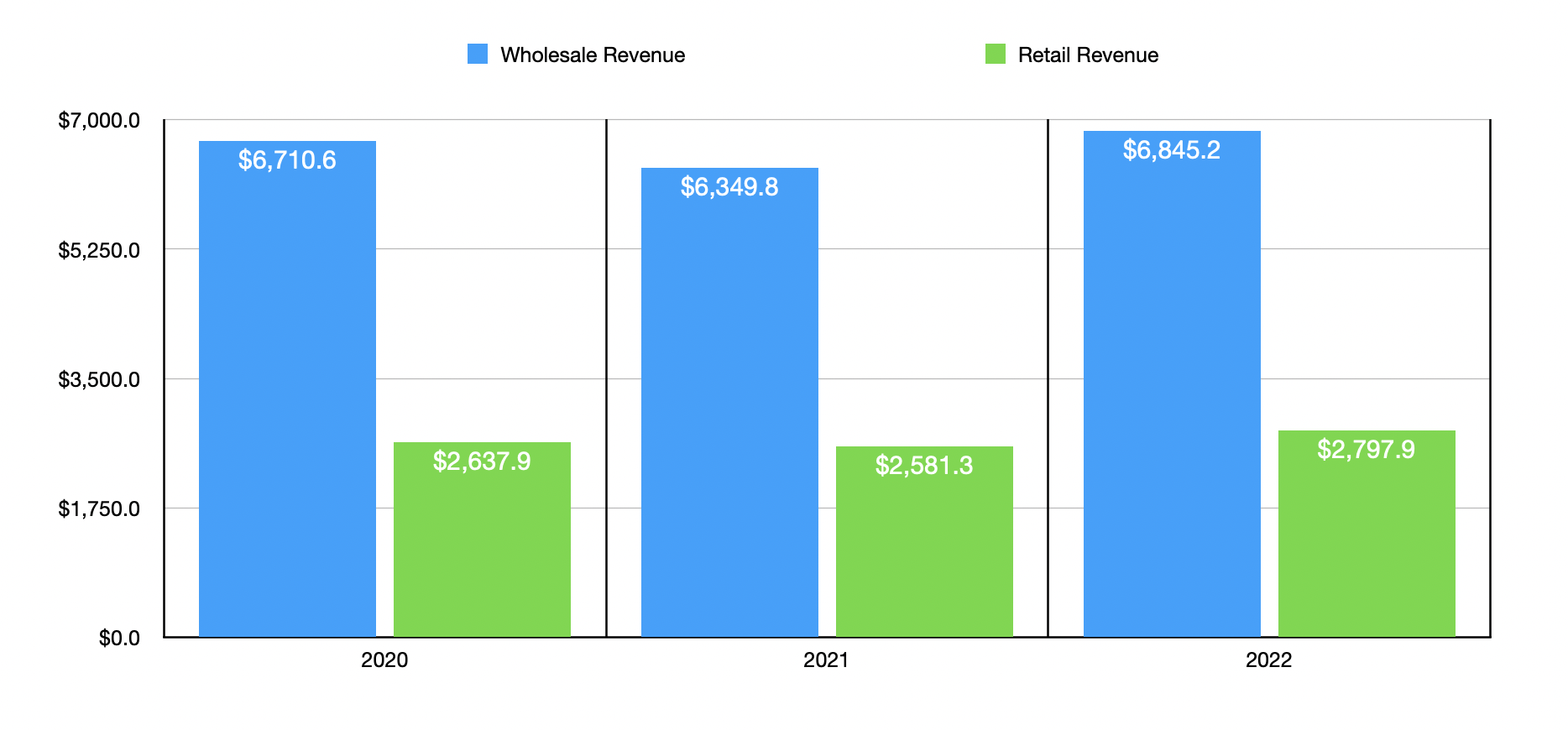

This decline in share price came at a time when overall revenue for the company has been looking up. Consider how the company fared during its 2022 fiscal year . Revenue during that time came in at $9.64 billion. That's 8% higher than the $8.93 billion the business reported for the 2021 fiscal year. Under the massive Wholesale segment, the company saw revenue expand by 7.8%, climbing from $6.35 billion to $6.85 billion. This increase, management said, was driven by a 10.4% rise in pricing because of inflationary pressures. This was offset to some degree by a 2.6% drop in volume. Meanwhile, the smaller Retail segment of the company reported sales growth of 8.4%, with revenue climbing from $2.58 billion to nearly $2.80 billion. This increase was driven mostly by a 7.7% rise in comparable store sales, with a 9.6% hike in pricing more than offsetting a 1.9% reduction in the number of items sold.

Although the top line for the company was great, bottom line results were somewhat mixed. Net income, for instance, tanked, dropping from $73.8 million down to $34.5 million. A reduction in margins under gross profits negatively impacted the Retail segment, while a $38.2 million increase in LIFO expense hit the Wholesale segment. The company also saw a slight increase in selling, general, and administrative costs on a percentage of revenue basis, largely because of higher corporate administrative expenses like incentive compensation that totaled $21.6 million. Other profitability metrics were somewhat mixed. For instance, EBITDA for the company actually rose from $213.7 million to $242.9 million. On the other hand, operating cash flow declined from $161.2 million to $110.4 million. If we adjust for changes in working capital, it still would have dropped, falling from $212.4 million to $196 million.

When it comes to the 2023 fiscal year, management believes that revenue will come in at between $9.9 billion and $10.2 billion. Management said that earnings per share should be between $2.20 and $2.35 on an adjusted basis. At the midpoint, that would translate to net income of $81.6 million. Meanwhile, EBITDA for the company should be between $248 million and $263 million. No estimate was given when it came to other profitability metrics. No estimate was given when it came to operating cash flow. But if we assume that it, on an adjusted basis, will rise at the same rate that EBITDA is expected to at the midpoint, we should anticipate a reading for 2023 of $206.2 million.

{kind=link}

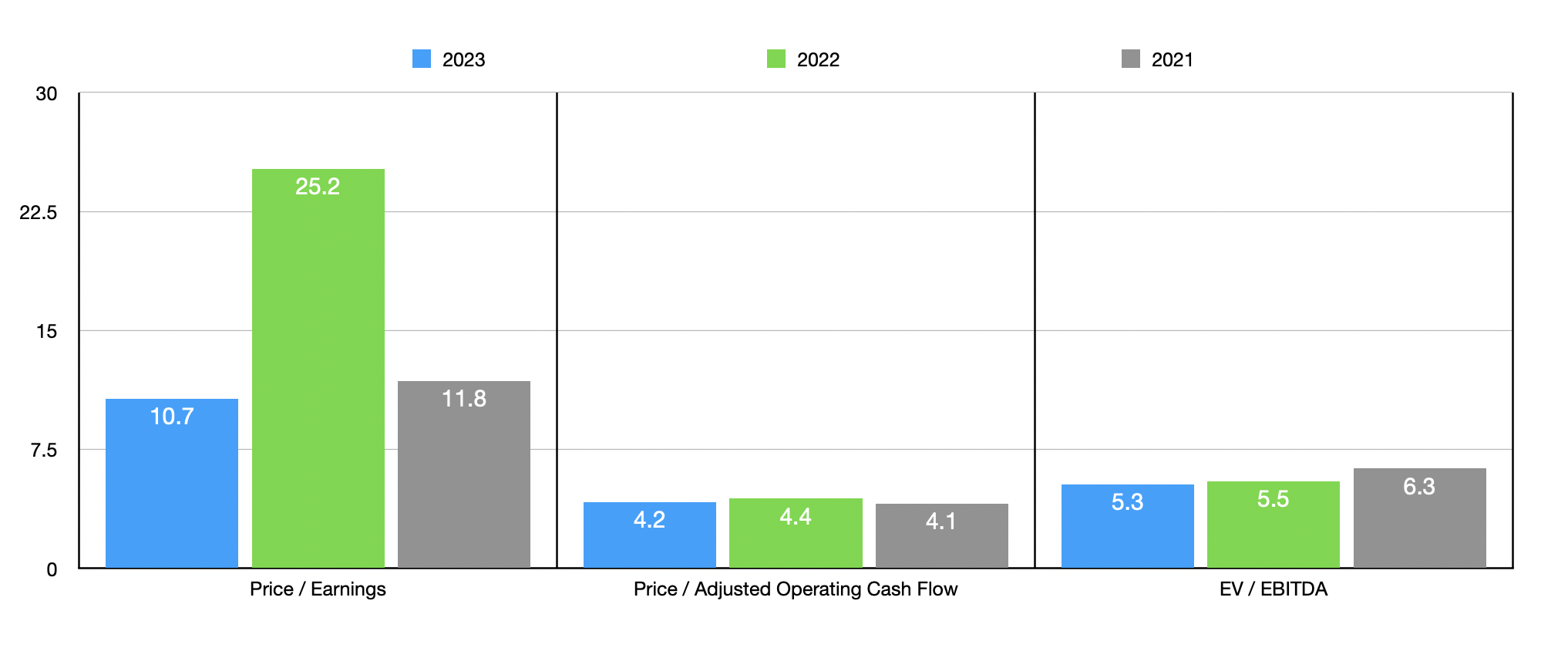

As you can see in the chart above, I priced the company using three different approaches and utilizing data from 2021 and 2022, as well as estimates for 2023. On an absolute basis, shares of the company look quite cheap. Meanwhile, in the table below, you can see how shares are priced next to five similar firms. On a price-to-earnings basis, only two of the five companies were cheaper than our prospect. Meanwhile, using both the price to operating cash flow approach and the EV to EBITDA approach, only one of the five firms was cheaper.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| SpartanNash Company |

| 25.2 |

| 4.4 |

| 5.5 |

| United Natural Foods ( UNFI ) |

| 8.6 |

| 2.9 |

| 5.4 |

| The Andersons ( ANDE ) |

| 10.7 |

| 4.9 |

| 6.2 |

| Performance Food Group Company ( PFGC ) |

| 34.9 |

| 17.0 |

| 12.3 |

| US Foods Holding Corp. ( USFD ) |

| 36.4 |

| 11.0 |

| 13.9 |

| Sysco ( SYY ) |

| 28.1 |

| 20.7 |

| 15.7 |

Where management's focus should be

From an operational and valuation perspective, I believe that SpartanNash is a decent company and is attractively priced. Part of the allure of the business is the fact that management also remains optimistic about the picture moving forward. By 2025, for instance, management hopes for revenue to exceed $10.5 billion annually. Bottom line results are also expected to continue improving, with EBITDA exceeding $300 million annually. Acquisitions, as well as the introduction of value-added offerings, are expected to help the company materially in this regard. In addition to this, from 2021 through 2025, the company is planning to realize benefits of between $125 million and $150 million because of supply chain and merchandising transformation initiatives, as well as how the company approaches its marketing activities.

{kind=link}

This is all great. But it's also somewhat vague. One thing that I do know, however, is that there is no significant amount of evidence that these efforts will focus the company's operations more toward the Retail side of things. As I made clear already, this is the smaller portion of the company, taking place through the 147 corporate supermarkets and 36 fuel centers that the company has split between 9 Midwestern states. These stores are generally between 14,000 and 90,000 square feet, with an average of around 44,000 square feet. The company has done some things on this front in recent years. For instance, at 142 of its locations, it offers online grocery shopping and curbside pickup or delivery. 91 of its stores also have pharmacy services, with 81 of those pharmacies being owned by the business.

{kind=link}

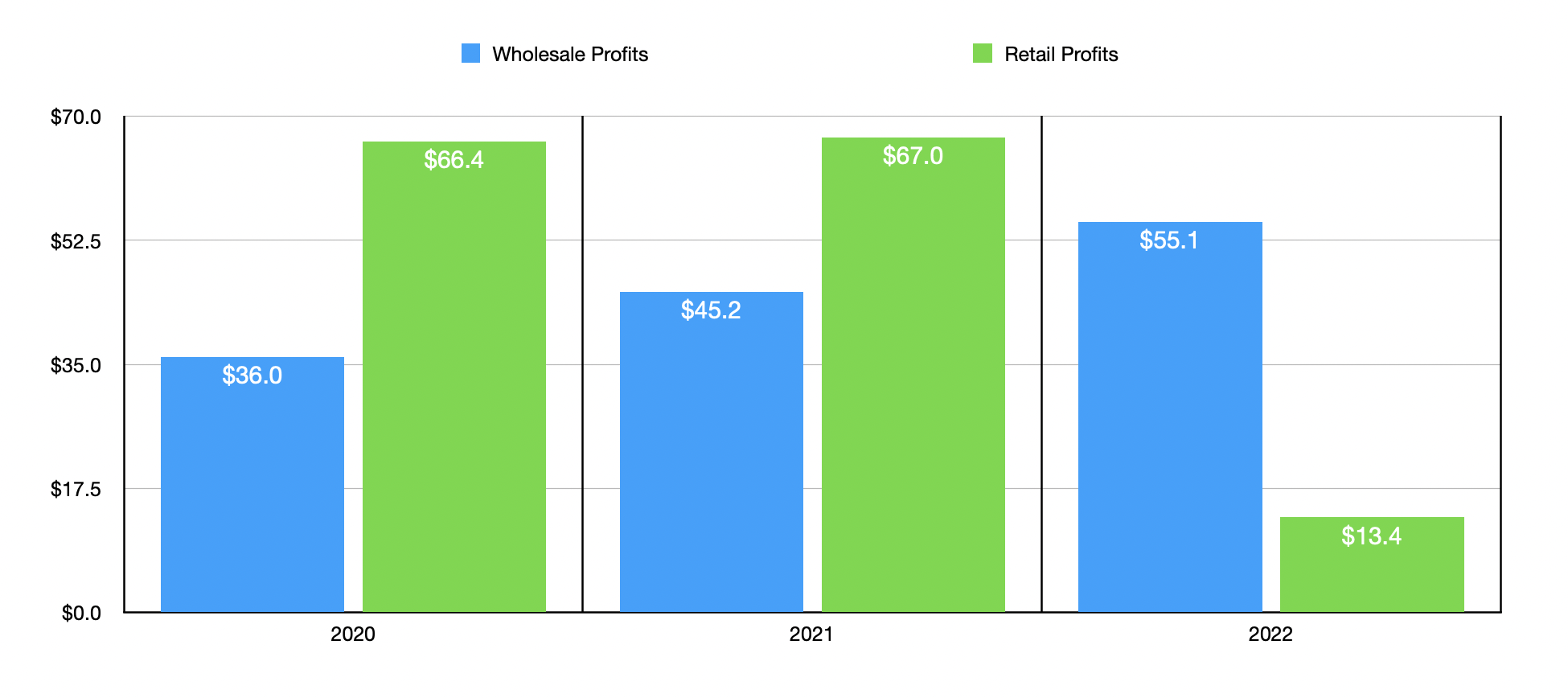

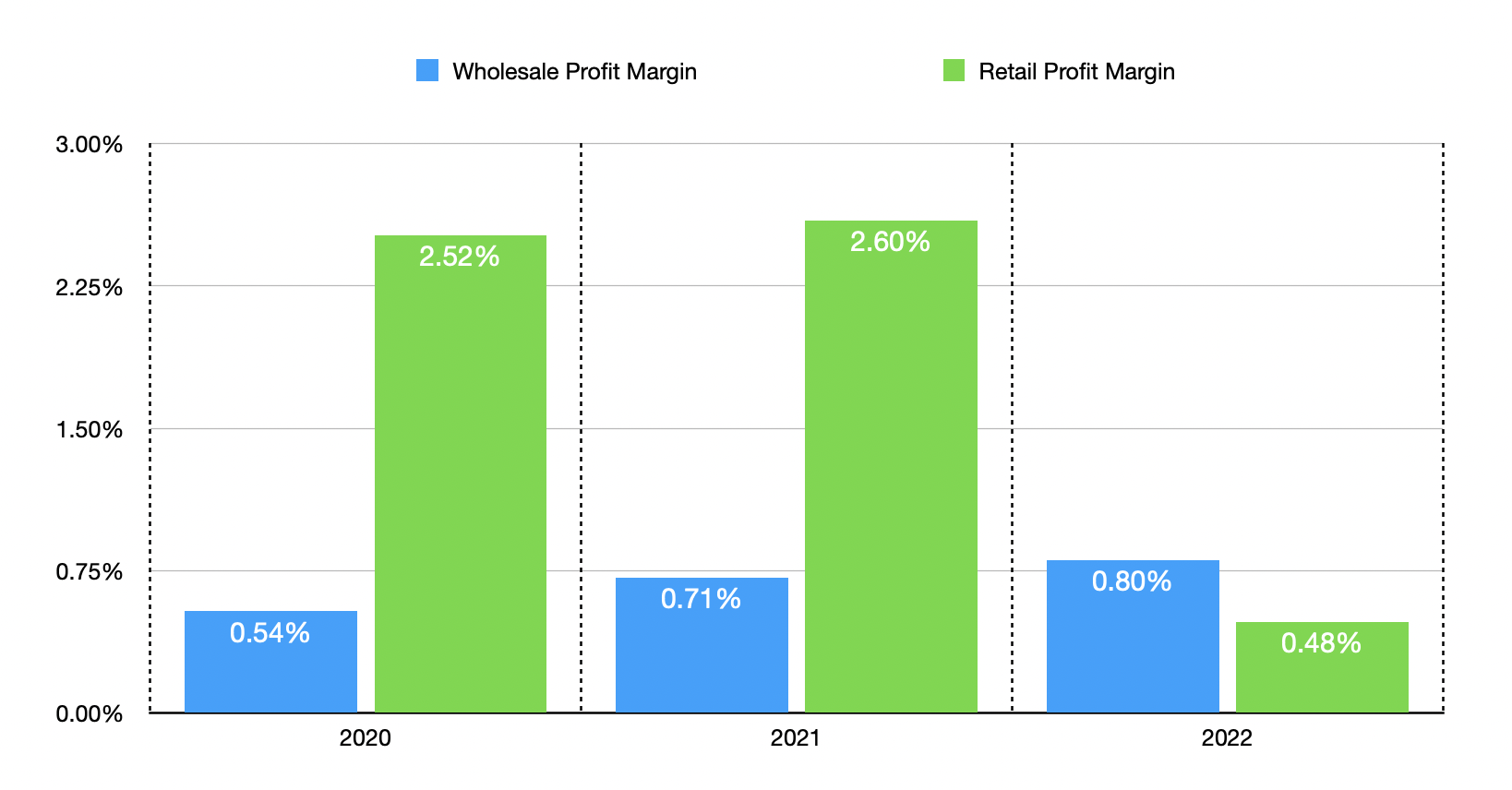

My problem with the company, however, is that it has not made a concerted effort to grow on this front. After seeing the number of locations in operation rise from 139 in 2018 to 156 and 2020, the company then moved to close some of its locations in 2021, dropping total store count to 145. That number has since crept up to 147. The reason why I say that these operations need additional attention is because their profit margins are far higher than the Wholesale operations of the company. This much can be seen in the table below. Yes, there was the difficult 2021 fiscal year. But with the exception of that, margins are significantly higher than the rest of the business. Seeing a greater emphasis on this side of the picture would be excellent for shareholders. But instead, the company seems to be more dedicated to growing its Wholesale business, with the latest transaction being the acquisition of Great Lakes Foods in January of this year. That entity serves 100 independent grocery customers from a 300,000-square-foot distribution center located in Michigan.

{kind=link}

Takeaway

At this point in time, I believe that SpartanNash is a decent company that investors would be wise to consider if they are interested in the grocery distribution market. In the long run, I fully suspect the company would do just fine. Add on top of this how cheap shares are, both on an absolute basis and relative to similar firms, and I definitely have to rate it a 'buy'. But I do think that investors would be better off if management made more of an effort to grow the Retail operations of the company. If this does come to pass, it could prove to be a rather bullish catalyst for investors.

For further details see:

SpartanNash Company: Still Attractive On Growth, Though An Emphasis On Retail Would Be Wise