ACWI - SPDW: A Developed Market Value Proposition

2024-01-16 05:23:22 ET

Summary

- US stock market rises as investors hope for easing financial conditions in 2024, leading to stretched valuations.

- SPDR Portfolio Developed World ex-US ETF provides exposure to markets with more sensible valuations.

- US equities are overvalued, concentrated in tech stocks, and face potential risks from a more hawkish Federal Reserve.

As the curtains fell on Q4 2023, the US stock market witnessed a robust rise which was sparked by the market’s hope that tight financial conditions will ease in 2024. As a result, the surge in stock prices has led to stretched valuations, prompting investors to explore alternatives to US equities. One such alternative, the SPDR Portfolio Developed World ex-US ETF ( SPDW ), stands out as it provides exposure to markets with more sensible valuations. In this analysis, I will use The SPDR S&P 500 ETF Trust ( SPY ) and the iShares MSCI ACWI ETF ( ACWI ) as comparisons for an ETF representing the US stock market (the former) and an ETF representing a developed market fund with a strong US weight of 60% (the latter).

Overview

The SPDR Portfolio Developed World ex-US ETF is an ETF used to diversify a portfolio away from the US equity markets while maintaining investment in key global developed markets. The ETF is specifically designed to track the performance of S&P’s Developed Ex-US Broad Market Index which is a market capitalization-weighted index that covers investable publicly traded companies in developed markets outside of the US. As one of the core SPDR Portfolio ETFs that have lost costs, SPDW does this at a very low cost, boasting an expense ratio of just 0.03%. Compare this to Invesco FTSE RAFI Developed Markets ex-U.S. ETF’s ( PXF ) expense ratio of 0.45% and Xtrackers FTSE Developed ex US Multifactor ETF ( DEEF ) of 0.24%. It even beats out the Vanguard FTSE Developed Markets ETF’s ( VEA ) notably cheap expense ratio of just 0.05%.

Holdings

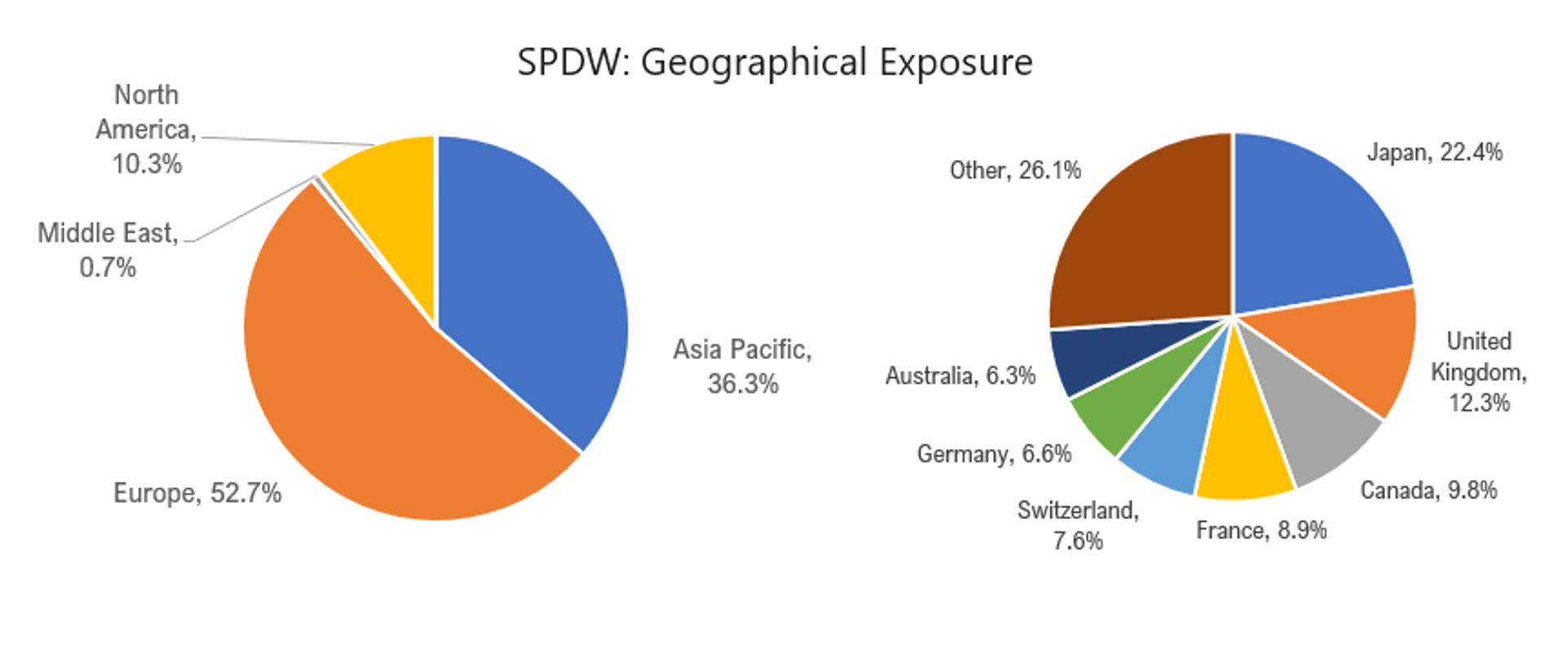

SPDW’s holdings are spread across 26 different geographical regions but over 70% of the portfolio is represented by the top seven regions. At the top spot, Japan has the highest weight of 22.36% which is just over 10 percentage points higher than the UK which is the second highest weight of 12.25%. Following these two regions, Canada, France, Switzerland, Germany, and Australia all have similar weightings between 6-9%. Despite Japan seeing the highest single country weight, the Asia Pacific region has the second largest weighting on the “continent” level. Europe has the highest concentration in this ETF at 53% when including the UK. Excluding the UK, the euro area still is the biggest slice of the pie with a weight of about 41%.

{kind=link}

US Equities Look Overvalued

Stock valuations have recently become stretched after a strong end to 2023 helped lead major indexes to post solid gains despite tough financial conditions. Specifically, we look at the return of SPY, the most popular ETF tracking the S&P 500, which saw a 26.2% return in 2023 which was driven by an 11.6% increase in Q4. This has certainly raised an eyebrow. Based on data from Multpl , the S&P 500 started 2024 with the highest price-to-earnings (P/E) ratio since 2021 and the 2nd highest since 2009 at 25.6x. The comparison funds demonstrate how the US overvaluation is appearing in ETFs. The holdings of SPY have a P/E ratio of 21.5x and a price-to-book (P/B) Ratio of 4.2x, and the holdings of the more diversified ACWI are at 18.8x and 2.9x. In contrast, SPDW offers a much better value proposition with a PE ratio of just 13.6x and a PB ratio of 1.60x. Even when compared to broader indices like ACWI, SPDW exhibits favorable metrics, emphasizing the attractiveness of markets outside the US. The dividend yield further supports this narrative, with SPDW offering a robust 2.79% compared to SPY’s 1.39% and ACWI’s 1.88%.

{kind=link}

Tech Concentration Could Be a Problem

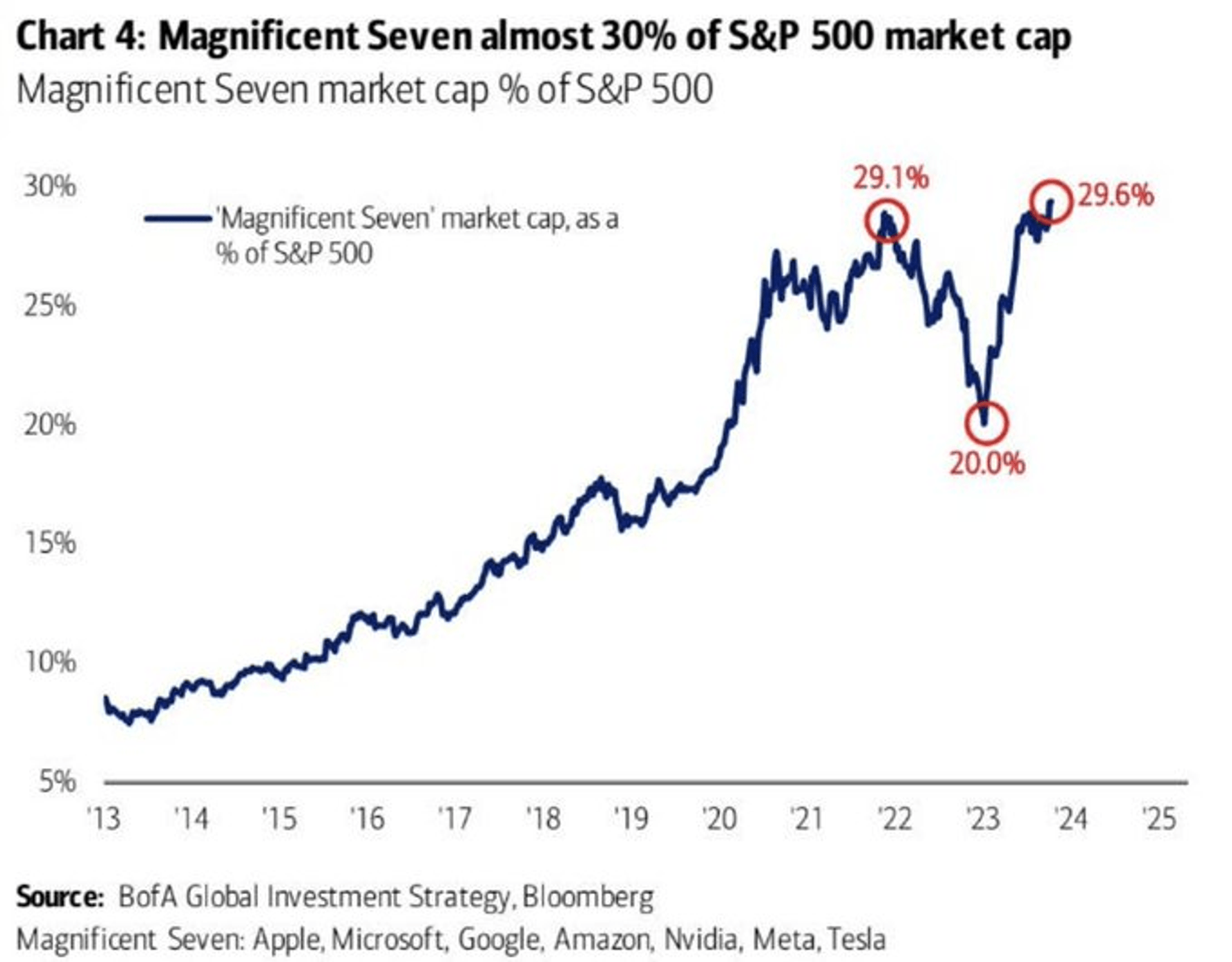

The recent rally in the US, particularly in tech stocks, has also fueled concerns about concentration risks in ETFs that are supposed to be more diversified. Specifically, we have seen the rise of the “Magnificent 7” stocks of the S&P 500 that have caused the technology tilt of the index to rise. Motley Fool notes that “The Magnificent Seven comprised 29.6% of the market cap of the S&P 500” as of data in October 2023 ( image source ). “That's higher than the previous concentration peak of 29.1%, which preceded the S&P 500 losing more than a quarter of its value during the 2022 bear market.” The most recent ETF data shows that SPY currently has a 28.0% information technology weight, and ACWI has a technology sector exposure of 22.9% (”Magnificent 7“ is 17.1% of that). In contrast, SPDW has a more prudent diversification, with tech accounting for just 10.11%. With recent stock returns causing ETFs to be over-exposed to this volatile sector, SPDW provides a more balanced exposure to mitigate downside risks.

{kind=link}

Major Non-US Markets Face Similar Risks but at Lower Valuations

Developed market central banks have all seen sharp monetary tightening over the past year and a half and have seen high returns in the last quarter due to an expectation that central banks will be easing in 2024. While these markets face similar risks, SPDW's exposure to developed markets offers better valuations. Japan’s Nikkei index has rallied above 35,000 for the first time in over 30 years but valuations were cheap before this. Improving macro conditions could support further gains as well. In a recent survey of Japanese firms, 70% were optimistic about economic growth in 2024. Macro conditions have been noticeably weaker in Europe, but negative economic trends look to be bottoming. If we look at valuations in iShares’ Japan and Europe ETFs, we’ll find that the price of earnings is well below US counterparts; specifically, the iShares MSCI Japan ETF ( EWJ ) has a PE ratio of 16.0x and the iShares Europe ETF ( IEV ) has a PE ratio of 14.2x. SPDW has significant exposure to these two markets with Japanese equities making up 22% of the portfolio and European (ex-UK) equities accounting for another 41% of the portfolio.

The US Market is Seeing Too Much Dovishness

Why else should we be wary of the US stock market? Perhaps because the market is setting a trap for itself. Contrary to market expectations, the Federal Reserve appears poised to adopt a more hawkish stance in 2024. Despite observing similar inflationary trends across developed economies, the resilience of US economic growth and employment has set it apart from its peers, especially Europe, the UK, Japan, and Australia. As of writing, the US unemployment rate is only 0.3 ppts off the post-pandemic lows, and the Atlanta Fed is projecting another strong quarter of growth of 2.2% in Q4. Meanwhile, the market sees a roughly 80% chance of a rate cut in March which is up from around 68% a week ago.

{kind=link}

The juxtaposition of strong macro data and a high March rate cut probability is concerning. Recent Fed member commentary also appears to contradict market rate cut pricing. FOMC Governor Bowman's comments on January 8th would be hard to be mistaken as dovish. She said clearly on the topic of lower rates that “we are not yet at that point” and that “upside inflation risks remain” including the risk that labor market tightness could make services inflation sticky. In her assurance that the Fed would remain data-dependent, she said that she would “remain willing to raise the Federal funds rate” if progress on inflation is reversed. These statements are not reflective of a Fed looking to pivot but instead a “higher for longer” narrative. The misalignment between the market and the Fed carries large downside risks for equities.

{kind=link}

This is less of a risk in other developed markets. While there are expectations of ECB cuts in 2024, growth and industrial activity are weak which should keep inflationary pressures contained and the ECB more willing to agree with the market’s dovishness. In Japan, the BoJ has yet to make any moves on rates and has shown itself to consistently tilt towards monetary easing. Normalization by the BoJ that is expected this year is not likely to be harsher than expected especially since GDP growth has been weak there as well. The UK is the only other country where hawkishness could maintain its foothold in 2024 because of how slow the disinflation trend has been. With that being said, UK equities are already cheap, and the region is only a small part of SPDW’s portfolio.

Conclusion

As the final quarter of 2023 drew to a close, the US stock market experienced a robust upswing fueled by market optimism surrounding the anticipated easing of tight financial conditions in 2024. This surge in stock prices, however, came hand in hand with stretched valuations, prompting astute investors to explore alternative avenues beyond the confines of US equities. The SPDR Portfolio Developed World ex-US ETF, emerges as a prudent choice, offering exposure to markets characterized by more reasonable valuations, an avenue to avoid potential overexposure to the technology sector, and diversification away from the US market’s naive bet on Fed dovishness.

For further details see:

SPDW: A Developed Market Value Proposition