SPB - Spectrum Brands Holdings: A Messy But Appealing Prospect Heading Into Q4 Earnings

2023-11-15 09:54:05 ET

Summary

- Spectrum Brands Holdings sold its Hardware and Home Improvement segment for $4.3 billion, improving its financial position.

- The company's revenue and profits have declined recently, but it has undergone significant changes and has a strong balance sheet.

- Shares of Spectrum Brands are cheap and analysts anticipate modest declines in revenue but strong earnings per share in the final quarter of this year.

Investing is tricky as is. But it can become much more complicated when the company that you are considering buying into or currently own is going through significant changes. One good example of this can be seen by looking at Spectrum Brands Holdings (SPB), a firm that focuses on the production and sale of branded consumer products and home essentials. In 2021, the company announced plans to sell its Hardware and Home Improvement segment for a massive $4.3 billion. In June of this year, the business finally achieved this goal, bringing in net proceeds of $3.8 billion. After paying down a significant amount of debt and buying back some stock, the company now seems to be working on improving its remaining operations. This does make understanding the business more complicated. But the good news is that shares currently look cheap and new data covering the final quarter of the 2023 fiscal year is about to come out. Leading up to that time, I have no doubt that investors are feeling a bit anxious. But given how the company is sitting right now, I would say that the odds are in their favor.

The picture could be better

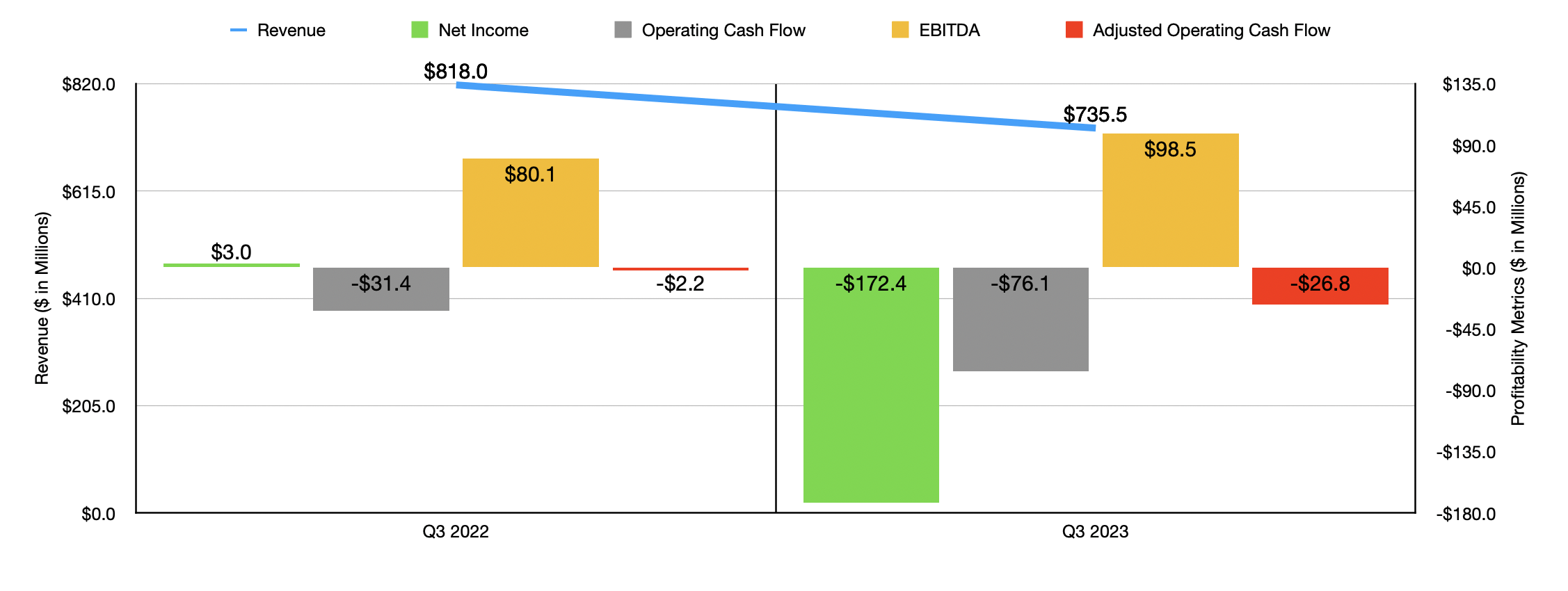

Back in May of this year, I wrote an article wherein I took a bullish stance on Spectrum Brands. In that article, I was optimistic because of the aforementioned asset sale that should pave the way toward a reinvention of the company. But just because this change should have a massive positive impact on the company does not mean that everything is great about it. For instance, in the most recent quarter for which data is available, which would be the third quarter of 2023, revenue took a beating. It came in at $735.5 million. That's down 10.1% from the $818 million generated one year earlier.

{kind=link}

To be very clear, this drop in sales is after the company accounted for the aforementioned divestiture. Actual organic revenue accounted for the vast majority of this decline, with the HPC (Home and Personal Care) set of operations leading the way. Revenue under this segment plunged 16% from $329.3 million to $276.6 million. All but $4.3 million of the drop in sales was driven by organic weakness that management attributed to a reduction in demand for things like kitchen appliances stemming from high retail inventory levels and consumers deciding not to spend more in light of uncertain economic conditions. Increased competition that was accompanied by higher promotional spending from competitors was also to blame for this. The remaining $4.3 million of the decline was attributable to foreign currency fluctuations. Keep in mind that this was only the worst-performing segment. The other two key segments for the company also reported drops in revenue year over year.

With the drop in revenue also came a decline in profits. The company went from generating a net profit of $3 million in the third quarter of 2022 to generating a loss of $172.4 million. Operating cash flow went from negative $31.4 million to negative $76.1 million, while the adjusted figure for this went from negative $2.2 million to negative $26.8 million. Meanwhile, EBITDA was the only profitability metric to improve, climbing from $80.1 million to $98.5 million. It's important to keep in mind the fact that, in addition to dealing with margin pain because of the aforementioned weaknesses, the company also had to contend with integration and separation costs. Restructuring initiatives have also been a hang-up for the company in recent quarters. But when you consider that management completed not only the aforementioned asset sale but also completed other transactions as well, it becomes understandable that there would be volatility on this front.

{kind=link}

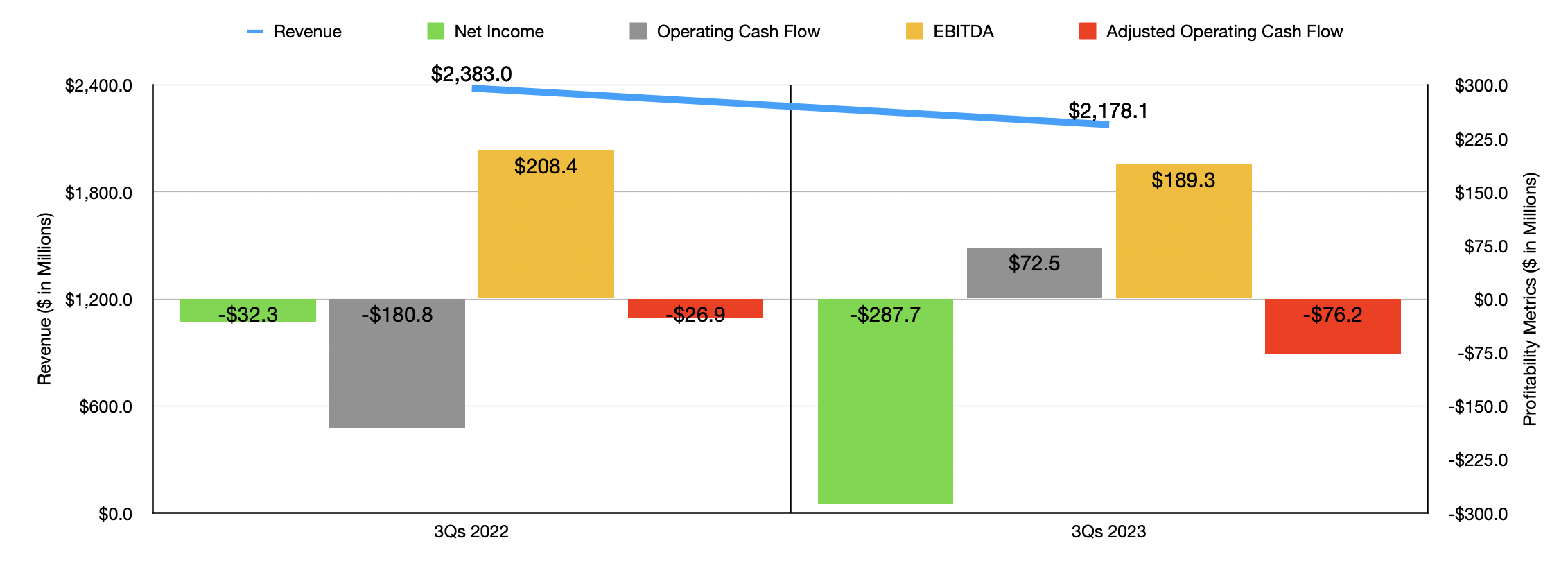

As you can see in the chart above, financial results for the first nine months of 2023 were, as a whole, worse than they were for the same time of 2022. For the 2023 fiscal year in its entirety, management has not provided much in the way of guidance. But we do know that if we annualize results for the year so far, we would expect an EBITDA of $257.2 million. This would represent a drop from the $283.1 million reported at the same time last year. If we make certain adjustments to account for all the changes the company has gone through, a good proxy for adjusted operating cash flow would be $158.4 million. A good approximation for last year would be $184.3 million.

{kind=link}

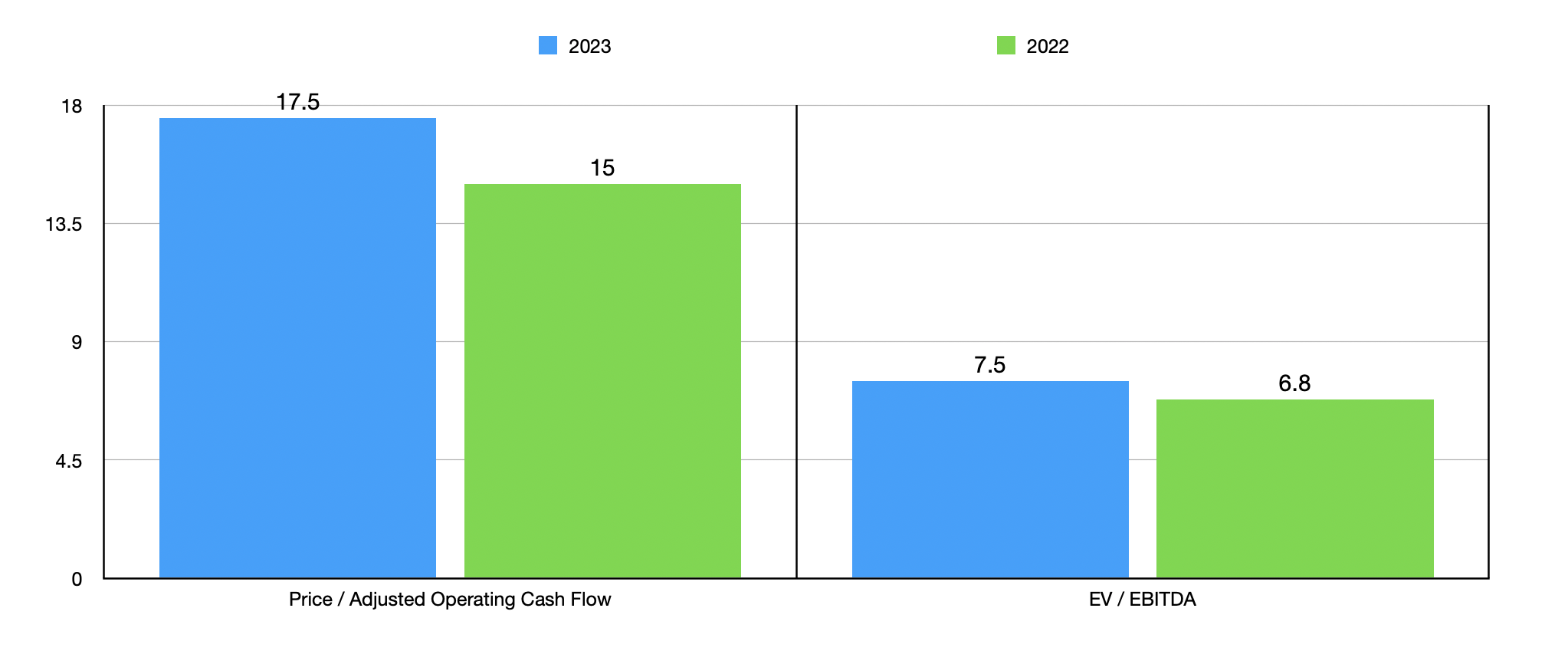

Taking these figures, we can then build the chart above. In it, you can see how shares are priced both on a forward pro forma basis and using data from 2022. You might notice a significant disparity between the price to operating cash flow multiple and the EV to EBITDA multiple of the company. This is because the firm currently has cash in excess of debt that totals $851.8 million. That brings the enterprise value down considerably. It's because of this balance sheet peculiarity that I would encourage the EV to EBITDA multiple of the company over the price-to-operating cash flow multiple. And when you do look at the picture through this lens, shares still look quite cheap. In the table below, you can see how the stock is priced relative to five similar firms. While on a price-to-operating cash flow basis, the stock looks more expensive than most of its peers, it's actually the cheapest on an EV to EBITDA basis.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Spectrum Brands Holdings |

| 17.5 |

| 7.5 |

| WD-40 Company ( WDFC ) |

| 31.0 |

| 30.6 |

| Energizer Holdings ( ENR ) |

| 6.4 |

| N/A |

| Central Garden & Pet Co ( CENT ) |

| 8.7 |

| 10.4 |

| Reynolds Consumer Products ( REYN ) |

| 10.8 |

| 12.5 |

| Clorox Co. ( CLX ) |

| 17.0 |

| 39.7 |

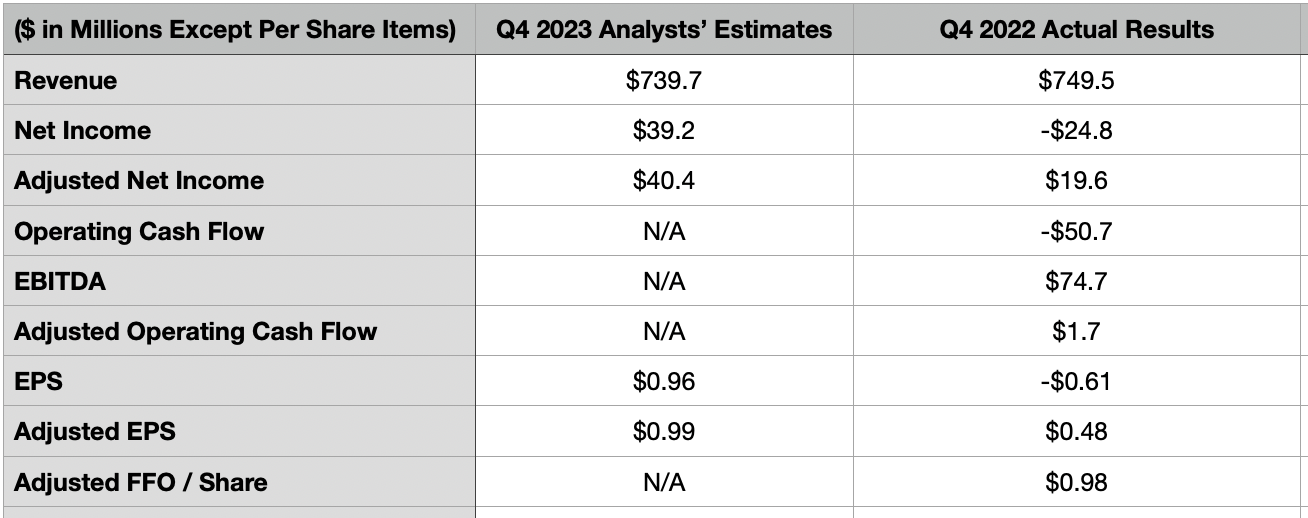

Of course, the picture can change from one quarter to the next. And that is why investors should be paying careful attention to data when it comes out before the market opens on November 17th. Currently, the expectation set by analysts is for revenue to come in at $739.7 million. That would represent only a modest decline from the $749.5 million generated one year earlier. Almost certainly, the same weaknesses that impacted sales so far this year would be instrumental in pushing sales down in the final quarter.

{kind=link}

On the bottom line, meanwhile, analysts believe that earnings per share will come in strong at $0.96 while adjusted earnings per share will be even higher at $0.99. To be perfectly honest, I would be surprised if this came to pass. After all, the company generated a net loss per share in the final quarter of 2022 of $0.61, while its adjusted profit was $0.48 per share. In the table above, I also provided some other profitability figures for the company. Investors should be paying attention to those data points when they come out as well. If earnings are higher like what analysts anticipate, it's almost certain that these profitability metrics will be higher as well.

Takeaway

Given all that I disclosed already, you might wonder why I am still bullish on Spectrum Brands. Yes, the picture is likely to be worse this year as a whole than it was last year even after accounting for the big asset sale. But the fact of the matter is that the company has undergone so many other changes that it is difficult to truly assess the bottom line. When you start looking at the adjusted figures reported by management, and you factor in not only the massive amount of cash the firm has on hand, but also the fact that it has already repurchased $400 million worth of stock this year, you start to see how the company is healthier now than it has been in a long while. Add on top of this how cheap shares are, both on an absolute basis and relative to similar firms, and I do believe that it makes for a decent 'buy' at this time.

For further details see:

Spectrum Brands Holdings: A Messy But Appealing Prospect Heading Into Q4 Earnings