REYN - Spectrum Brands Holdings: Latest Regulatory Green Light Is Bullish For Shareholders

2023-05-09 13:31:12 ET

Summary

- Spectrum Brands Holdings has done quite well for itself recently, with shares rising thanks to the regulatory picture facing the company clearing up.

- With only one more hurdle in the way, the company is on the path to sell one of its units for $4.3 billion.

- This will transform the company and, adjusting for it, shares look quite cheap at this point in time.

Outside of perhaps the banking sector, one of the most interesting and volatile companies so far this year has been Spectrum Brands Holdings (SPB). For those not familiar, the company operates as a global branded consumer products and home essentials company. Its operations are really split between three different segments the focus on sales of home appliances, personal care products, animal and pet products, cleaning goods, and a variety of other items. When I say that the company has been volatile, I do mean incredibly volatile. From the end of last year through today, inclusive of distributions, the company has achieved upside of 21.4%. Approximately half of this upside has been achieved this month alone. This move higher can be chalked up to some good news regarding a major asset divestiture. With the coast almost entirely clear at this point, this transaction will bring on a tremendous amount of cash for the company, enabling it to eliminate its debt and prepare itself for long-term growth. Add on top of this how cheap the company is after accounting for the divestiture, and I cannot help but to think that the business is easily worthy of a "buy" rating.

A green light

Back in September of 2021, Spectrum Brands announced that it had agreed to sell its Hardware and Home Improvement segment to ASSA ABLOY, a global leader in the production of doors and door systems, as well as other offerings, in an all-cash transaction valued at $4.3 billion. At first glance, such a sale may seem fairly simple. But it wasn't long before regulators intervened. The most significant challenge came from the US Department of Justice, which initially sued to block the Swedish acquirer from purchasing the business unit. This created a tremendous amount of uncertainty about whether the deal would ultimately be permitted or not.

My goal at this point is not to rehash every aspect of what has transpired. But we do know that the case ultimately made it to court, though it was delayed twice. Finally, on May 5 of this year, the management team at Spectrum Brands announced there it had agreed to a stipulation with the DOJ that would allow it to complete this transaction. This stipulation requires that ASSA ABLOY divest of certain assets prior to the deal between the two entities being finalized. The deal in question was originally announced in early December of last year, with ASSA ABLOY agreeing to sell off some of its assets to Fortune Brands Home & Security for $800 million. These particular assets include the company's Emtek and Smart Residential operations throughout the US and Canada.

This marks a major win for Spectrum Brands and its investors. After taxes, Spectrum Brands expects to bring in net proceeds of $3.5 billion. As of the end of the most recent quarter, the enterprise had $3.05 billion in net debt on its books. In theory, this should allow the company to pay off all of its debt and still have about $447.8 million in cash on its books. This is not to say that the deal is as good as done. Both parties are still waiting on approval from Mexican regulators. This does create some uncertainty for shareholders. Having said that, Spectrum Brands is still targeting a completion of this divestiture prior to the end of June.

{kind=link}

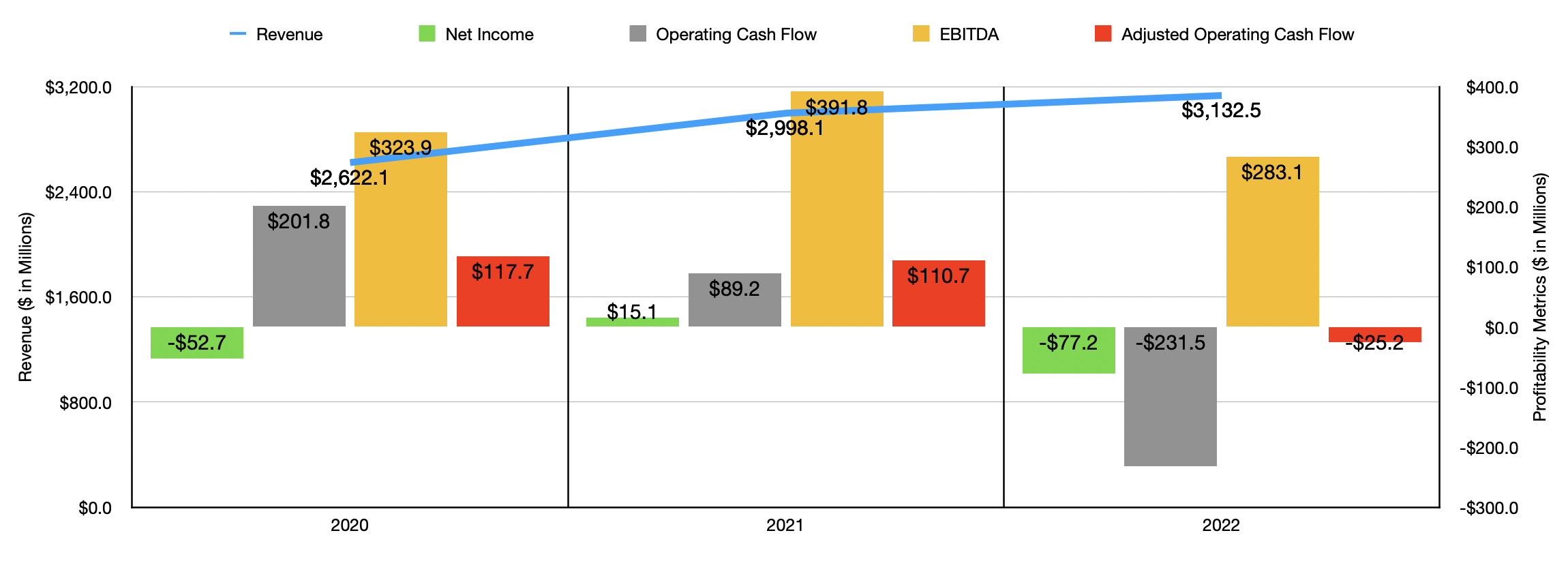

In the event that the transaction ultimately is completed, there could be some nice additional upside for shareholders of Spectrum Brands. On top of the company being completely de-risked from a leverage perspective should the deal go through, it's also true that the enterprise is trading on the cheap. Consider the most recent financial data available. Revenue in 2022 for the core operations that will remain totaled $3.13 billion. That was up 4.5% over the roughly $3 billion reported for 2021 and stacked up nicely against the $2.62 billion generated in 2020.

On the bottom line, however, we have seen some weakness. Two of the past three years saw the company generate net losses. Of the three years, the worst was 2020 when the company generated a net loss of $77.2 million. Cash flows also weakened to some degree because of changing market conditions. Operating cash flow, for instance, went from $89.2 million in 2021 to negative $231.5 million in 2022. Even if we adjust for changes in working capital, we would see that metric drop from $110 million to negative $25.2 million. And finally, EBITDA further business fell from $391.8 million to $283.1 million.

{kind=link}

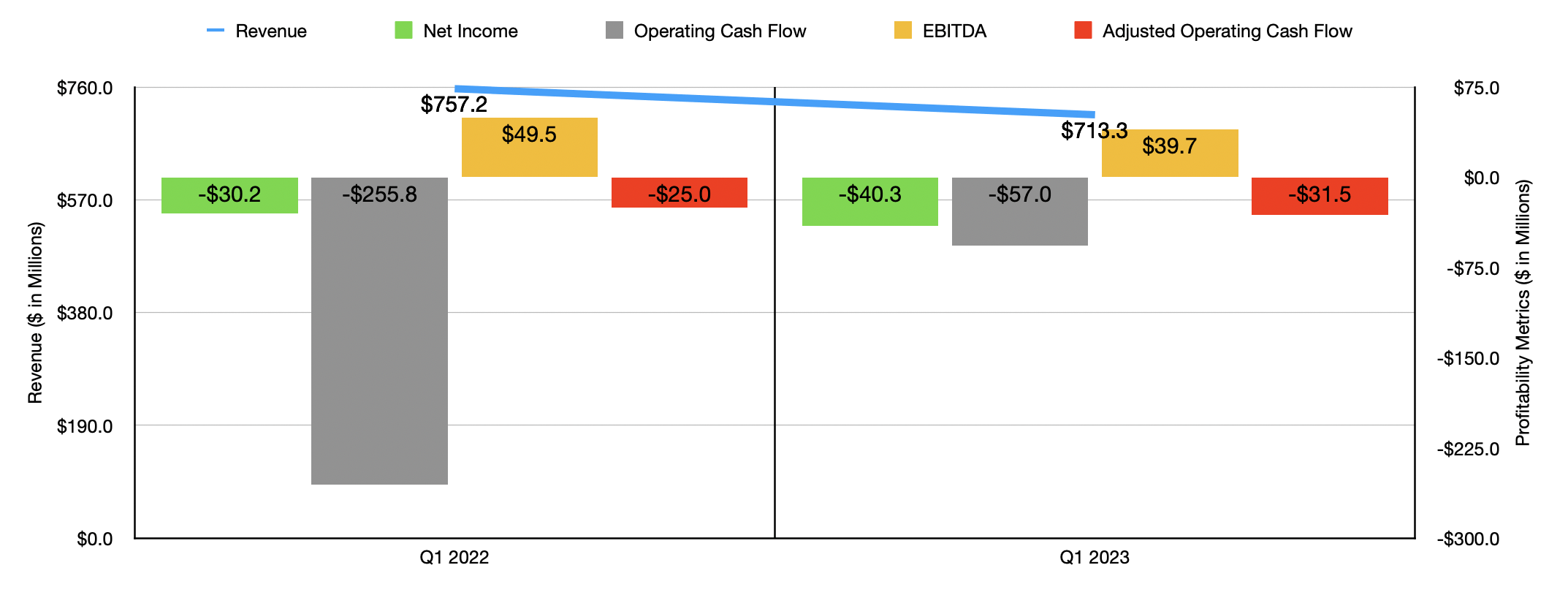

Given these results, you might find my optimism regarding the company to be a bit misplaced. This is especially true when you consider that the 2023 fiscal year is looking to be a bit rough for the company. Revenue in the first quarter of the year, for instance, came in at $713.3 million. That's down 5.8% compared to the $757.2 million generated one year earlier. However, it's important to note that much of this sales decline was driven by a $39.6 million hit associated with foreign currency fluctuations. But stripping that out, organic revenue for the company worsened year over year, dropping from $757.2 million to $685.1 million. Sales were only higher because of a $67.8 million contribution associated with acquisitions activities.

Bottom line results for the first quarter also suffered. The company went from generating a net loss of $30.2 million in the first quarter of 2022 to generating a net loss of $40.3 million during the first quarter of 2023. Operating cash flow actually improved, going from negative $255.8 million to negative $57 million. But if we adjust for changes in working capital, it would have worsened only modestly from negative $25 million to $31.5 million. Meanwhile, EBITDA for the company went from $49.5 million to $39.7 million.

In my opinion, both the top line and bottom line troubles that the company is facing are the result of top line factors. The space that the enterprise operates in is known for having low margins. And when you have sales in a low margin business contract, bottom line results suffer even more. And pretty much across the board, recent market conditions have been less than ideal. For instance, under the company's Home and Personal Care segment, revenue dropped 4% because of increased competition and high retail inventory levels. The Global Pet Care segment of the company reported an 8.2% plunge in revenue because of the exact same reasons. And finally, the Home and Garden segment reported a 5.2% drop in profits, largely due to these issues as well.

{kind=link}

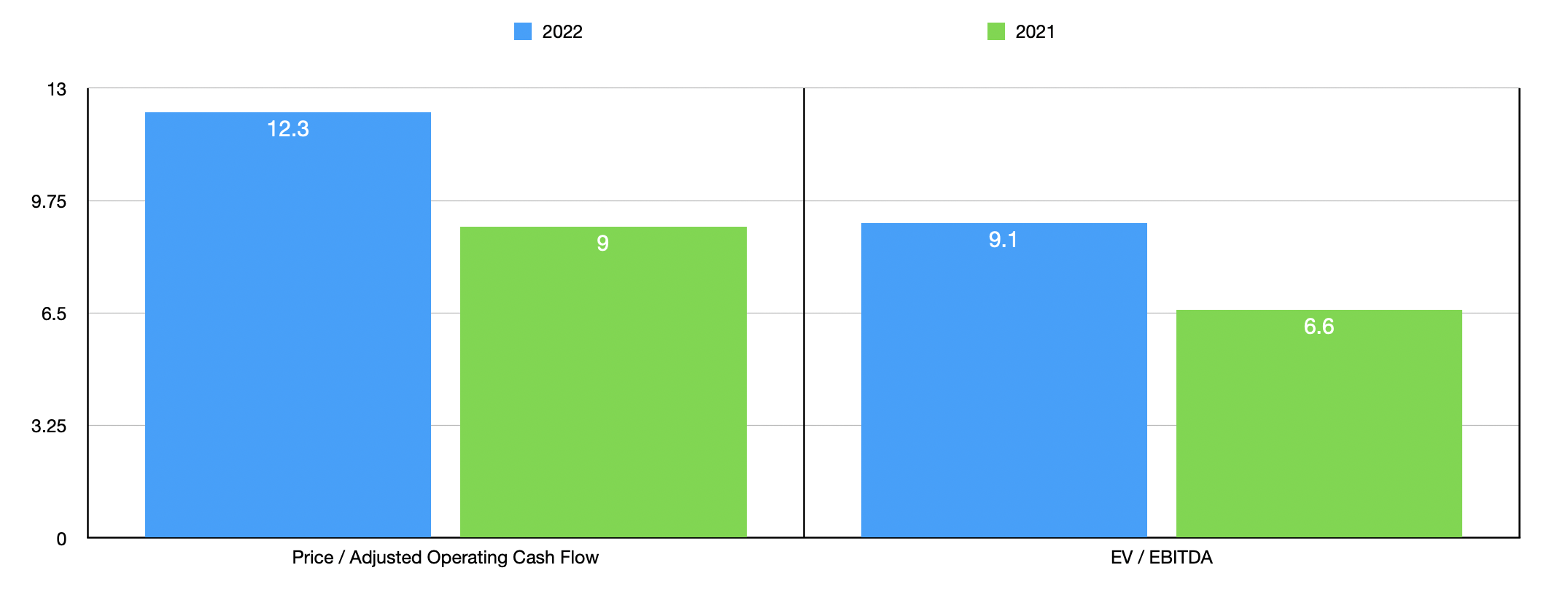

The fact of the matter is that this kind of space is not great for an inflationary environment that's causing consumers to be tight with their money. But in the long run, this space has always grown. So at some point, we should see some recovery. And with the company having cash in excess of debt should the deal ultimately go through, it will definitely be in a good position to weather this storm. To see what kind of upside potential, if any, the company does offer investors, I did create the chart above. In it, you can see how shares of the company are priced from both a price to adjusted operating cash flow perspective and from an EV to EBITDA perspective using results from both 2021 and 2022. In this case, the stock looks quite affordable. As part of my analysis, I also priced the company next to five similar firms. As you can see in the table below, only one of the five companies was cheaper than Spectrum Brands on a price to operating cash flow basis. Meanwhile, our prospect was the cheapest of the group when looking at matters through the lens of the EV to EBITDA multiple.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Spectrum Brands Holdings |

| 12.3 |

| 9.1 |

| WD-40 Company ( WDFC ) |

| 129.1 |

| 30.0 |

| Energizer ( ENR ) |

| 11.5 |

| 10.5 |

| Central Garden & Pet Company ( CENT ) |

| 14.3 |

| 11.1 |

| Reynolds Consumer Products ( REYN ) |

| 26.2 |

| 14.6 |

| Clorox ( CLX ) |

| 19.5 |

| 50.3 |

Takeaway

More than most any other company on the market today, Spectrum Brands is most certainly in an interesting position. It's still possible that the deal to sell off its assets could fall through. And if that does come to pass, I wouldn't be surprised to see the stock pull back. Having said that, shares do look affordable if we assume the asset sale is completed. This is especially the case when you consider the net cash position of the company under this scenario. Given how cheap shares are, both on an absolute basis and relative to similar enterprises, I would make the case that some upside from here is most certainly warranted. As such, I have elected to rate the company a "buy" for now, with that rating contingent on its major transaction ultimately being completed.

For further details see:

Spectrum Brands Holdings: Latest Regulatory Green Light Is Bullish For Shareholders