SPEM - SPEM: Valuation Attractive But No Near-Term Catalyst Yet

2023-10-25 14:58:55 ET

Summary

- SPDR Portfolio Emerging Markets ETF has fallen considerably since 2021, losing over 30% of its value.

- Despite attractive valuation based on the Buffett Indicator, investors should exercise caution due to high exposure to China.

- The Federal Reserve's monetary policy has a large impact on SPEM's performance, and there is no near-term catalyst for outperformance.

Introduction

Emerging markets often are perceived as higher growth markets than developed markets. However, does better growth always translate to better returns for investors? In this article, we will analyze the SPDR Portfolio Emerging Markets ETF ( SPEM ) and provide our analysis and recommendations.

ETF Overview

SPEM invests in over 3,500 stocks in about 30 emerging markets. SPEM appears attractive based on our valuation analysis. While PMI data in emerging markets appears to be stabilized, China, SPEM’s largest exposure by country, is having some long-term structural issues. In addition, we do not see any near-term catalyst as the Federal Reserve is not ready to change its hawkish monetary policy to a dovish one. Hence, we think investors should wait on the sidelines.

YCharts

Fund Analysis

SPEM has fallen considerably since 2021

SPEM had a strong performance in 2020 following the sharp market selloff during the outbreak of the pandemic. As can be seen from the chart below, the fund has reached its price peak in early 2021. However, this strong performance quickly reversed. SPEM was on a decline for the rest of 2021. Unfortunately, this decline accelerated in 2022 as sky-rocketed inflation caused the Federal Reserve and many other central banks around the world to hike their rates aggressively. Since the peak in 2021, SPEM has lost over 30% of its value.

YCharts

Attractive valuation based on Buffett Indicator

To evaluate whether SPEM is an attractive investment opportunity or not, we will first take a look at the valuation. To help readers evaluate SPEM’s valuation, we will introduce readers to the revised Buffett Indicator.

According to Warren Buffett, we can evaluate whether the broader stock market is overvalued or not by checking the total market capitalization to GDP ratio. If this ratio is below 75%, the market valuation is cheap. If it is within the range of 75% to 90%, the market valuation is fair. If this ratio is above 90%, the market’s valuation is overvalued. This method to evaluate the valuation of the stock market as a whole is called the Buffett Indicator.

Since many central banks around the world have expanded their balance sheets significantly in the past 2 decades, this indicator needs to be revised to better reflect the effect of monetary policies on the stock markets. The denominator should also include the assets of central banks. Therefore, the revised Buffett Indicator should become "total market capitalization to (GDP + assets) ratio."

Below is a table that shows this revised Buffett Indicator in the top 4 countries in SPEM’s portfolio. Excluding Taiwan, which we do not have the data, the rest of the 3 countries represent about 57% of SPEM’s total portfolio. This should give us a good indication of the valuation of SPEM. As can be seen from the table, China’s total market capitalization to GDP and total asset ratio is 41.53%. This ratio tells us that China’s stock market is quite cheap. India, which represents about 20.93% of SPEM’s portfolio has a ratio of 85.19%. Therefore, India’s stock market appears to be fairly valued. Just like China, Brazil’s ratio of 34.39% is way below the fairly valued range. Based on the numbers for these three countries, it appears that SPEM is attractively valued.

| Buffett Indicator: TMC/(GDP + TA) Ratio |

| SPEM’s Exposure |

| China |

| 41.53% |

| 30.35% |

| India |

| 85.19% |

| 20.93% |

| Taiwan |

| N/A |

| 17.73% |

| Brazil |

| 34.39% |

| 5.63% |

Source: SPDR, GuruFocus.com

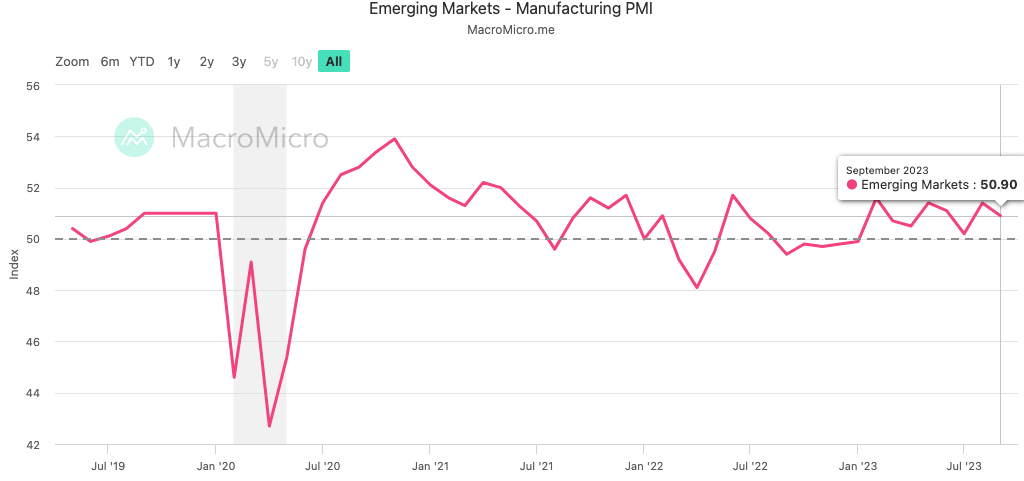

EM PMI showing signs of strength

Let us now look at an important forward indicator, the PMI data for emerging markets. As can be seen from the chart below, EM PMI have now stabilized after reaching its near-term low in 2022. Since the beginning of 2023, emerging markets PMI has stayed above 50. For reader’s information, a reading below 50 suggests that the economy may be heading for contraction. In contrast, a reading above 50 usually suggests that the economy is entering expansion. It appears that a global manufacturing inventory correction is now near the end and manufacturing activities are now showing some early signs of strength. While the worst may be over, this rebound is not a strong rebound as the PMI reading is still very close to 50.

{kind=link}

Reasons why we think investors should exercise caution

Despite SPEM’s attractive valuation, we do not think this is the right time to invest in SPEM. In fact, we think investors should remain cautious for the following reasons:

SPEM has underperformed against the S&P 500 in the long run

While emerging markets are often perceived as higher growth markets than developed markets, these markets often have higher risks than U.S. stocks. This has resulted in its underperformance in the long run. As can be seen from the chart below, SPEM’s total return in the past 10 years was only 23.4%. In contrast, the S&P 500 index delivered a total return of 188.3% in the past 10 years. For investors wanting some exposure outside of the U.S., perhaps S&P 500 stocks already provide enough exposure as many stocks in the index have sizable revenue and earnings internationally.

YCharts

SPEM has a high exposure to China

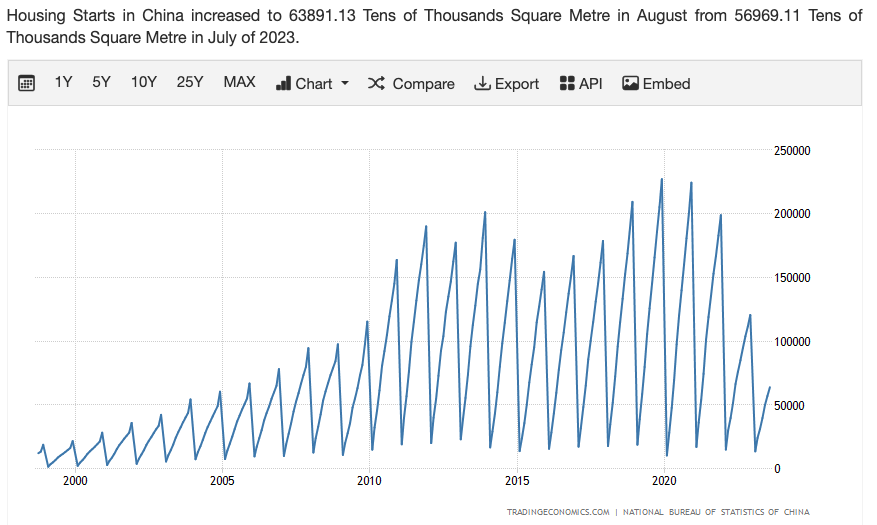

Stocks from China represents over 30% of SPEM’s total portfolio. Although China’s economy has enjoyed very strong growth in the past few decades, it is now facing serious problem. First, China’s population is aging and is actually declining. This will hurt its long-term GDP growth as consumer spending growth will inevitably slow down. Second, tensions between China and the U.S. has caused many companies to reorganize supply chains and move factories out of China. This will potentially cause higher unemployment rates in China and result in a weakening Chinese economy. Third, China’s housing market bubble appears to be bursting. As can be seen from the chart below, housing starts in China have clearly peaked in 2019/2020 and are in a declining trend. Since the housing sector represents a large chunk of China’s GDP, a burst in its housing market bubble will hurt its long-term GDP growth.

{kind=link}

The Federal Reserve’s monetary policy has a large impact on SPEM’s performance

Emerging markets’ performances often depends on the Federal Reserve’s monetary policy. As can be seen from the chart below, SPEM’s performance is often inversely correlated to the 10-year treasury rate and the Fed fund rate. This is because when the Federal Reserve eases its monetary policy, money will flow out of the U.S. to emerging markets and result in outperformance in these markets. In contrast, when the Federal Reserve tightens its monetary policy, capital will return to the U.S. and this often cause significant underperformance in equities.

YCharts

The question we need to ask is when will the Federal Reserve change its monetary policy from a hawkish stance to a dovish stance? To successfully combat the inflation, the Federal Reserve needs to keep this rate elevated for a lengthy period. Otherwise, inflation may rack up again. Therefore, we do not think the Federal Reserve will be ready to lower its interest rate until after 2024. In fact, the Federal Reserve may still need to raise the rate in the near-term to combat persistent inflation. Therefore, we do not see any catalyst to allow SPEM to outperform in the near-term.

Investor Takeaway

SPEM has an attractive valuation. However, we are concerned about China’s weakening fundamentals. Given that there is no near-term catalyst, we do not think investors should be buying SPEM right now.

Additional Disclosure : This is not financial advice and that all financial investments carry risks. Investors are expected to seek financial advice from professionals before making any investment.

For further details see:

SPEM: Valuation Attractive But No Near-Term Catalyst Yet