SPYV - SPGP: This S&P 500 GARP ETF Indicates Growth Stocks Are Overvalued

2023-06-27 05:36:34 ET

Summary

- SPGP tracks the S&P 500 GARP Index, selecting 75 stocks based on five factors relating to sales growth, earnings growth, financial leverage, ROE, and earnings-to-price ratios.

- The Index reconstitutes twice per year in June and December. This month's reconstitution substituted 1/3 of its holdings drove the portfolio's valuation down to 16x forward earnings.

- With a 1.27 beta and 37% exposure to risky Energy and Materials stocks, SPGP is borderline speculative and I don't recommend initiating a position today.

- However, by emphasizing the value factor, the June reconstitution did remind us that growth stocks are likely overvalued.

Investment Thesis

The Invesco S&P 500 GARP ETF ( SPGP ) is now a big gamble for the remainder of the year. That's my takeaway after evaluating its latest semi-annual reconstitution, which took effect last week. The changes included adding risky Energy and Material stocks while removing Health Care and Financial companies with consistent growth estimates. It's likely due to the S&P 500 GARP Index's approach of only including backward-looking metrics, which isn't my preference, especially with volatile commodity-price-linked stocks. While I acknowledge SPGP's selections have the potential to bounce back strongly, I have little comfort the opposite won't occur. Therefore, I recommend readers avoid SPGP for another six months, and I look forward to explaining why in more detail below.

SPGP Overview

Strategy Discussion

SPGP tracks the S&P 500 GARP Index, selecting 75 S&P 500 Index stocks each June and December based on five criteria:

- Three-year earnings per share growth

- Three-year sales per share growth

- Financial leverage

- Return on equity

- Earnings-To-Price

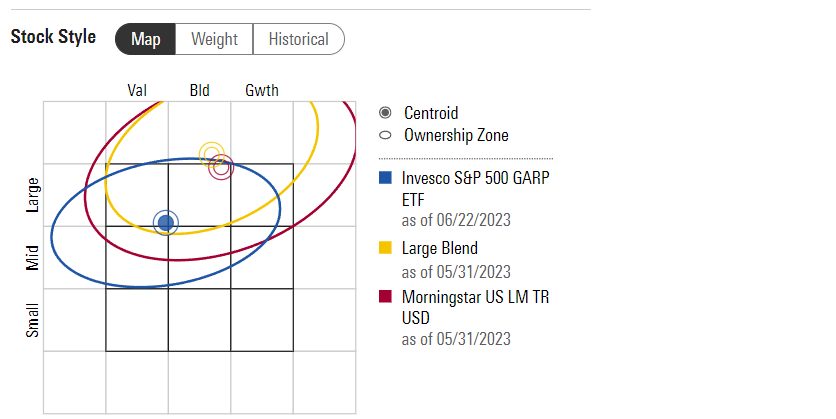

The selection process is growth-focused because it begins by calculating a growth score for S&P 500 companies, with the top 150 qualifying. The list is cut to 75 based on quality and value scores, with components weighted by their growth scores. This order of operations places SPGP primarily in the growth category, so it's notable whenever it crosses back into value territory. Morningstar's style graph suggests SPGP is now tilted closer to value than growth, which my fundamental analysis confirms.

{kind=link}

Morningstar

The GARP Approach

GARP investing typically involves calculating a company's PEG ratio, which stands for price-earnings-to-growth, by dividing the price-earnings ratio by the earnings growth rate. There are numerous ways to do this, as there are various price-earnings ratios (trailing, forward, GAAP, non-GAAP) and earnings growth rates (trailing, forward, short- and long-term). SPGP also incorporates sales growth and ensures constituents didn't "cheat" to achieve a high return on equity simply by boosting financial leverage.

However, the Index's criteria are backward-looking, which isn't my preference. I understand it because S&P 500 companies are more stable than small- and mid-cap stocks. Furthermore, some investors want an entirely objective selection process, which an estimated growth screen would ruin. Still, a mix of trailing and forward-looking metrics is more prudent.

To illustrate, SPGP's 16 Energy holdings have an average 27.32% three-year annualized sales growth rate, but analysts expect just 11.07% growth next year. Ignoring these latest estimates doesn't help investors because SPGP may not hold securities long enough for the market to realize their full value. Since SPGP began tracking its current Index in June 2019, annual portfolio turnover rates have ticked up, and as I will highlight next, this year is no different.

{kind=link}

Invesco

June Reconstitution Summary

SPGP Additions

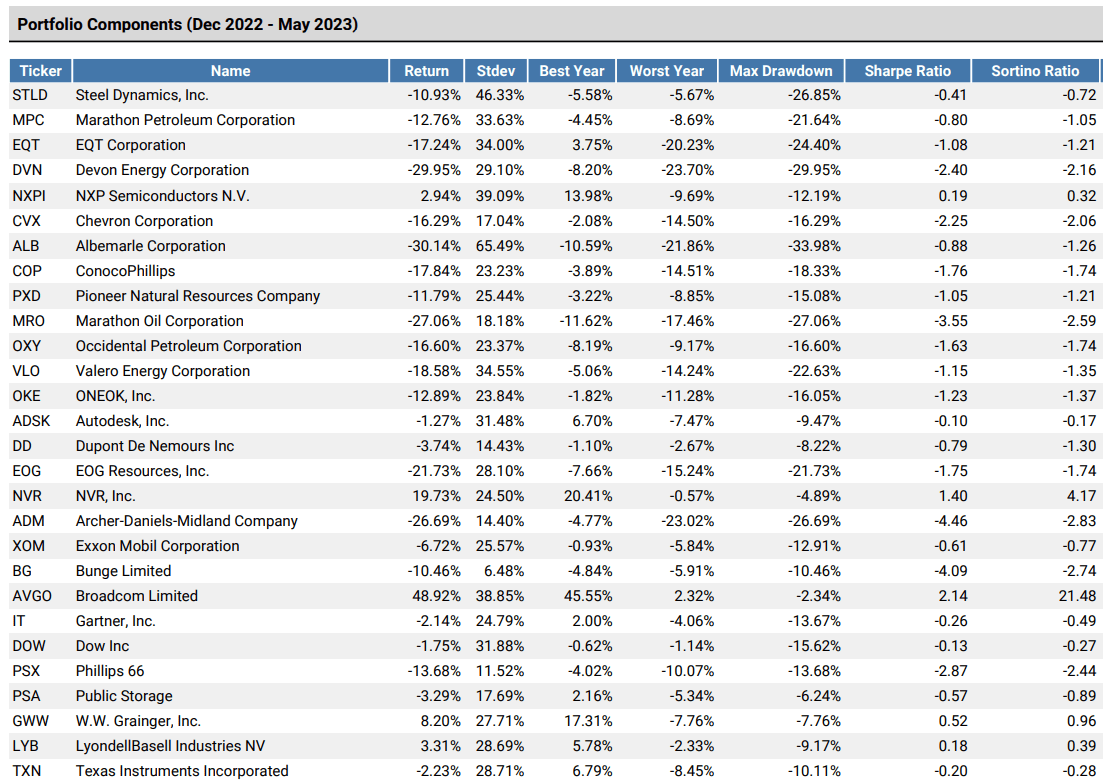

SPGP added 28 companies this month, significant for a fund of just 75 S&P 500 companies. These companies comprise 37% of SPGP and are listed below.

{kind=link}

Portfolio Visualizer

The sector breakdown is as follows:

- Consumer Discretionary: 1

- Consumer Staples: 2

- Energy: 13

- Industrials: 1

- Materials: 5

- Real Estate: 1

- Technology: 5

As shown, most suffered significant losses between December 2022 and May 2023, the latter roughly approximating the reference date used by the Index. It's a clue the Index is more value-driven than before. Also, these stocks have 16.78% less estimated one-year sales growth than on December 31, 2022. Growth estimates have dipped across the board, but it's still a remarkable statistic illustrating how growth stocks are likely overpriced today.

SPGP Deletions

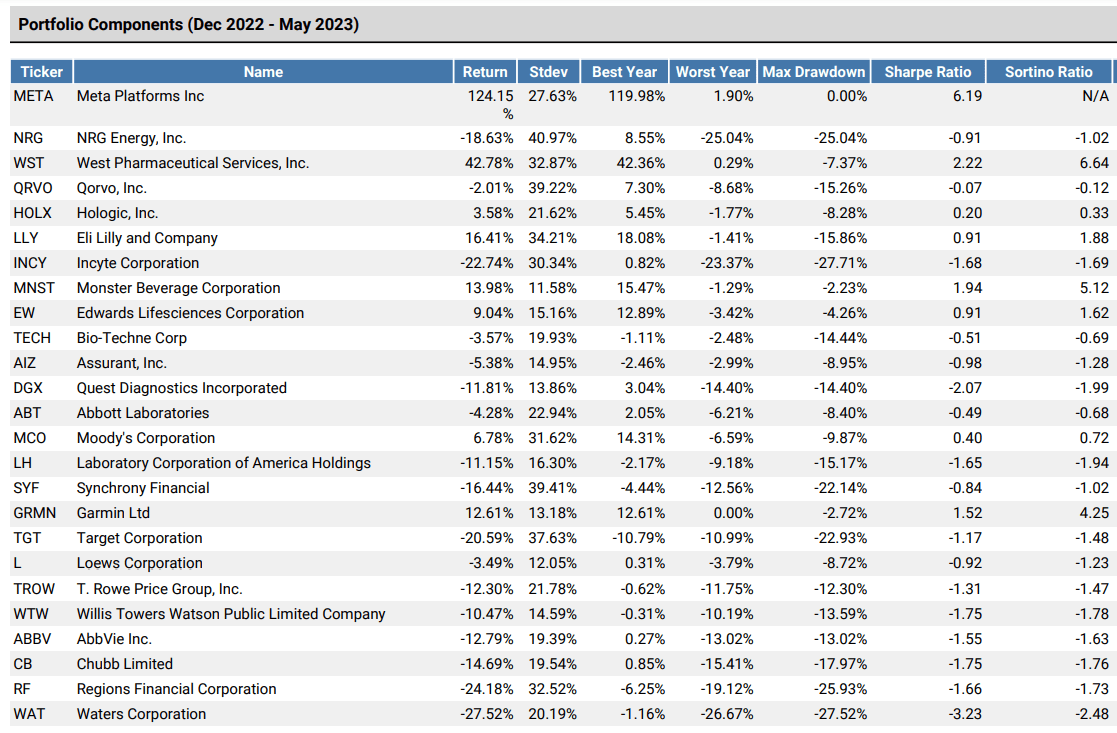

The 25 deleted stocks are below, sorted based on their Index weighting as of May 31, 2023. Except for Meta Platforms ( META ) and a handful of others, most deletions also experienced declines for the six months ending May 2023.

{kind=link}

Portfolio Visualizer

The sector breakdown is as follows:

- Communication Services: 1 (3.95%)

- Consumer Discretionary: 1 (1.10%)

- Consumer Staples: 2 (2.30%)

- Financials: 8 (8.07%)

- Health Care: 11 (14.06%)

- Technology: 1 (2.01%)

- Utilities: 1 (2.33%)

Unlike the additions, these 25 deletions' estimated one-year sales growth held up reasonably well, declining by just 4.32% on average since December 31, 2022. However, GARP investors should want to retain companies with consistently solid growth potential rather than remove them. Instead, this reconstitution accomplished two things:

1. It added stocks with drastically lower growth rates than in December, particularly in the volatile Energy sector.

2. It deleted stocks with consistent growth rates over the last six months, primarily in the more stable Health Care sector.

Next, let's look at how these changes impacted SPGP, starting with the fund's sector exposures.

SPGP Analysis

SPGP Sector Exposures and Top Ten Holdings

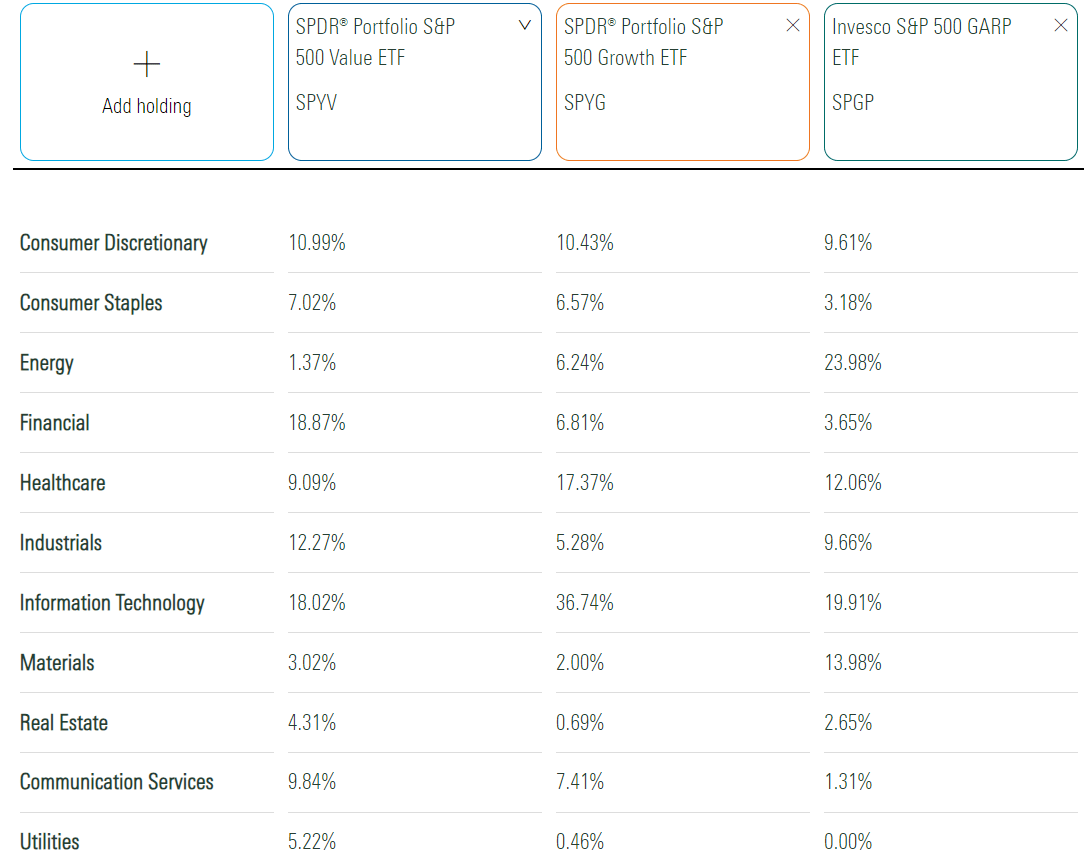

The following table highlights SPGP's sector exposures alongside the SPDR Portfolio S&P 500 Value ETF ( SPYV ) and the SPDR Portfolio S&P 500 Growth ETF ( SPYG ). Energy exposure is now at 24%, followed by Technology (20%), Materials (14%), and Health Care (12%).

{kind=link}

Morningstar

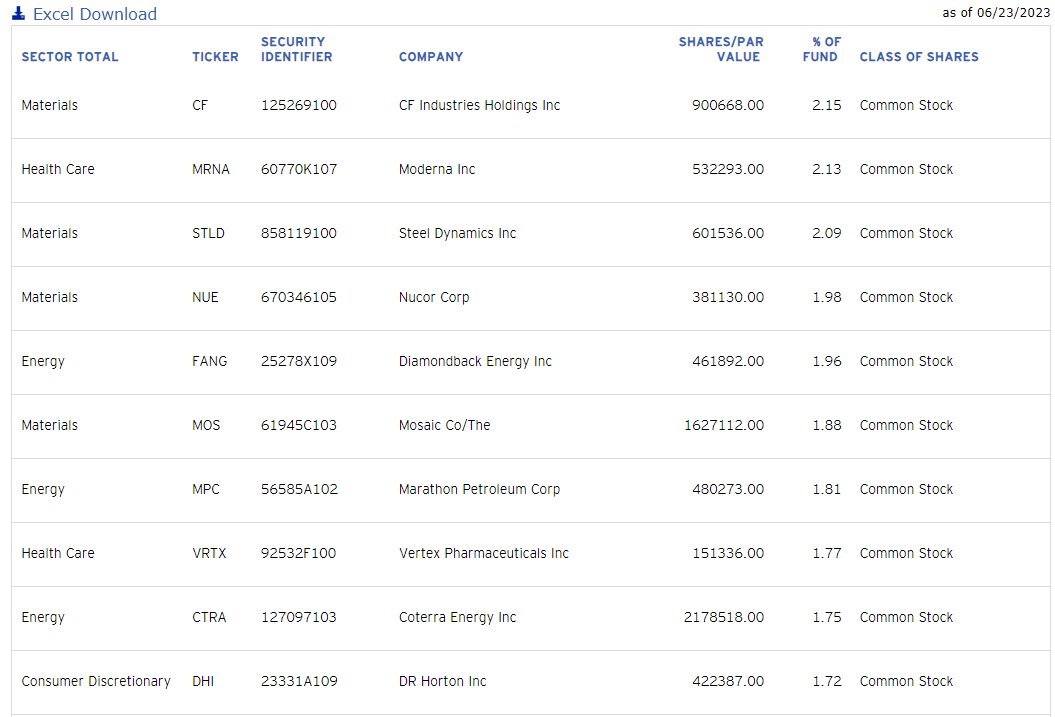

SPGP's top ten holdings are below, totaling 18% of the portfolio. Remember that SPGP's holdings are weighted by growth scores based on historical measures. For example, CF Industries ( CF ) is the top holding with 31% and 91% three-year trailing sales and EPS growth. However, worth noting is that analysts expect -0.14% and 4.50% sales and EPS growth over the next year. These changes might explain why the stock is down 14% in 2023.

{kind=link}

Invesco

Fundamentals By Industry

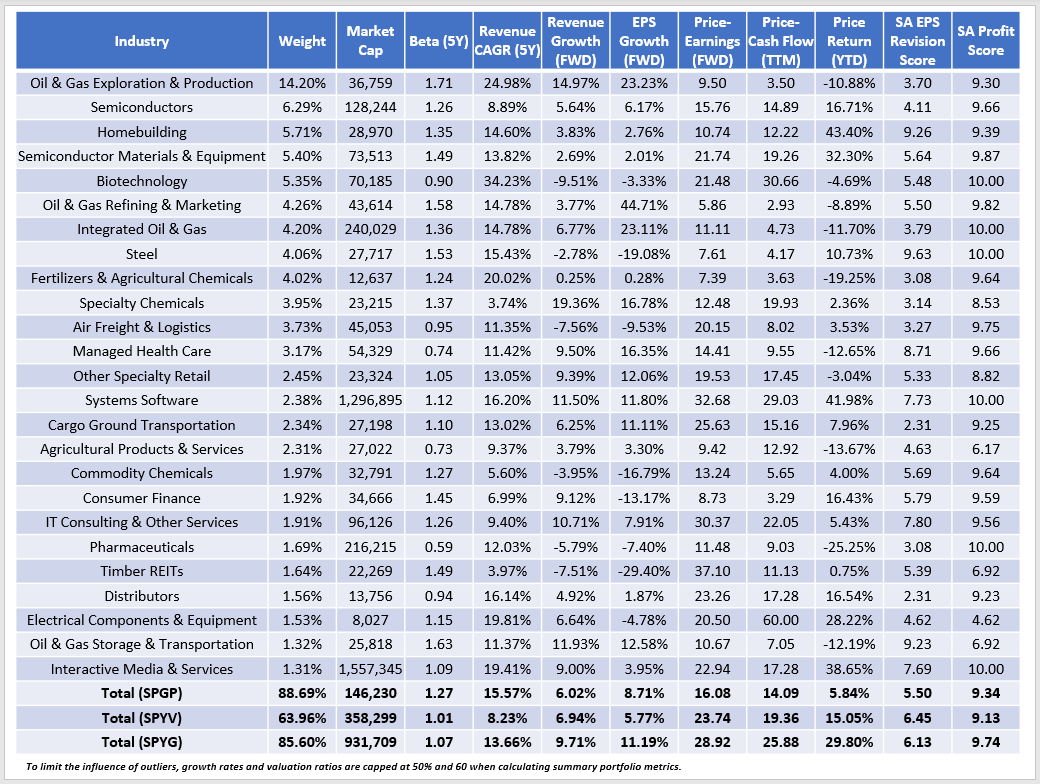

The following table highlights selected fundamental metrics for SPGP's top 25 industries, covering 89% of the fund. As shown, Oil & Gas E&P stocks account for 14.20%, followed by Semiconductors (6.29%), Homebuilding (5.71%), and Semiconductor Materials & Equipment (5.40%).

{kind=link}

The Sunday Investor

These industries are highly volatile betas and drive SPGP's 1.27 five-year beta, much higher than the 1.01 and 1.07 figures for SPYV and SPYG. Over the last five years, SPGP's constituents have grown sales by an annualized 15.57%, but that figure is just 6.02% today and even less than what SPYV features. SPGP's 8.71% estimated earnings growth rate looks solid, but estimated EBITDA growth is not. Not shown above, but analysts expect SPGP's constituents to grow EBITDA by 5.49% over the next year compared to 7.23% and 10.33% for SPYV and SPYG. Therefore, growth is not prominent in SPGP, implying growth stocks are overvalued.

Instead, the value factor is more emphasized. SPGP trades at 16.08x forward earnings, 7.66 and 12.84 points cheaper than SPYV and SPYG. It's a significant discount, but Energy and Material stocks drive this valuation. Without them, SPGP would trade at 20.33x forward earnings vs. 23.50x for SPYV. That discount is much less, considering all the additional risk you take by trying to time the bottom of commodity-linked stocks.

Performance Analysis

SPGP launched on June 16, 2011, but it's only tracked the S&P 500 GARP Index since June 21, 2019. I urge readers to refrain from basing their investment decisions on performance before this date. S&P Global notes that the Index's launch date was February 25, 2019.

{kind=link}

S&P Global

You may be tempted to look at Index performance since June 16, 1995, the Index's First Value Date. However, this performance is backtested, confirmed by the following disclaimer on the Index fact sheet :

All information for an index prior to its Launch Date is hypothetical back-tested, not actual performance, based on the index methodology in effect on the Launch Date.

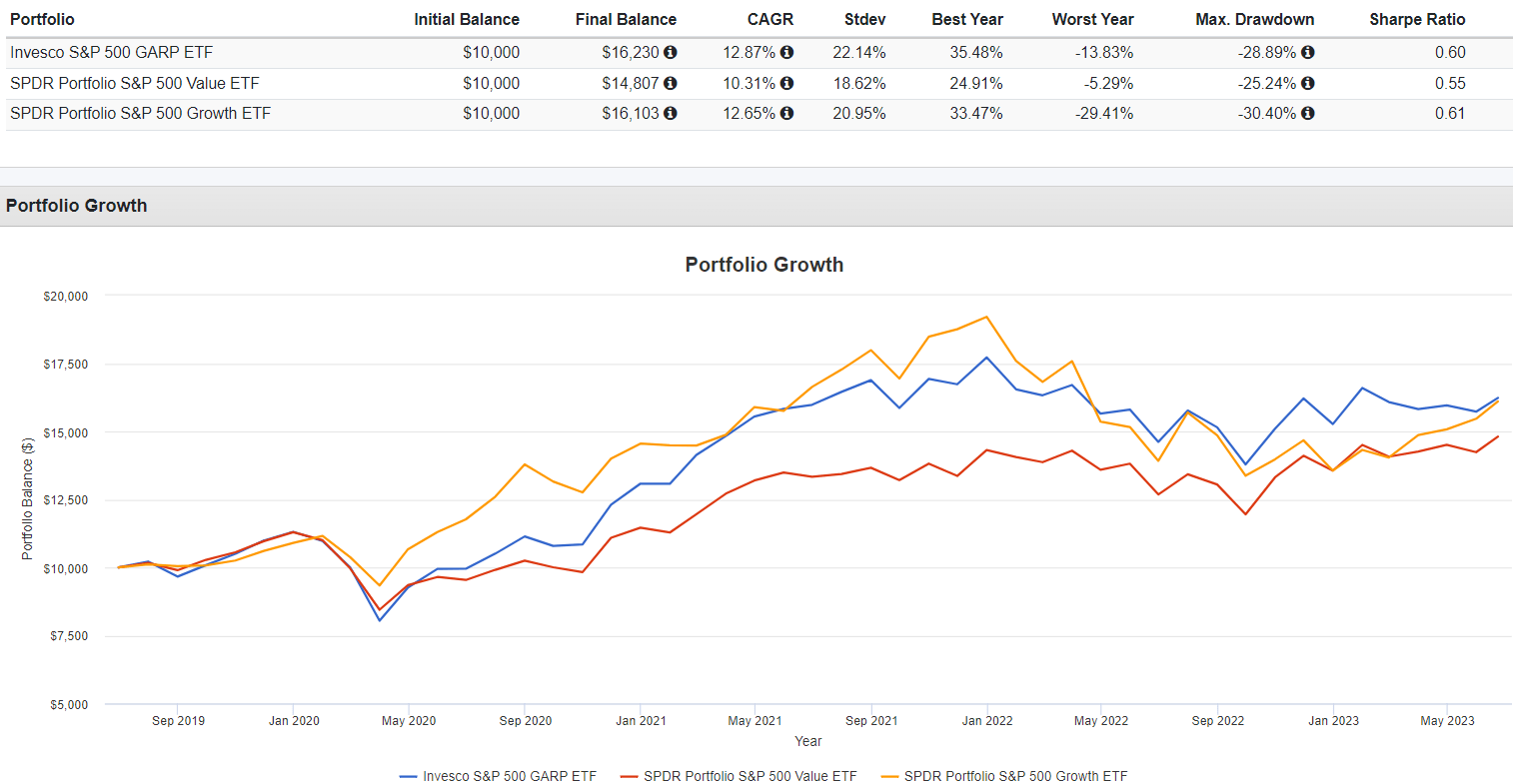

Backtested results almost always paint a positive picture but are crucial to the ETF launch process. However, it's all done with the benefit of hindsight. I consider it supplemental information and place much more importance on actual results. That said, here's how SPGP has done since July 2019 against SPYV and SPYG.

{kind=link}

Portfolio Visualizer

These results are solid. SPGP outperformed SPYV and SPYG by 2.66% and 0.22% per year, though it was more volatile. As a result, SPYG's risk-adjusted returns (Sharpe Ratio) were better. Based on the fundamental analysis presented earlier, SPGP will continue to be more volatile.

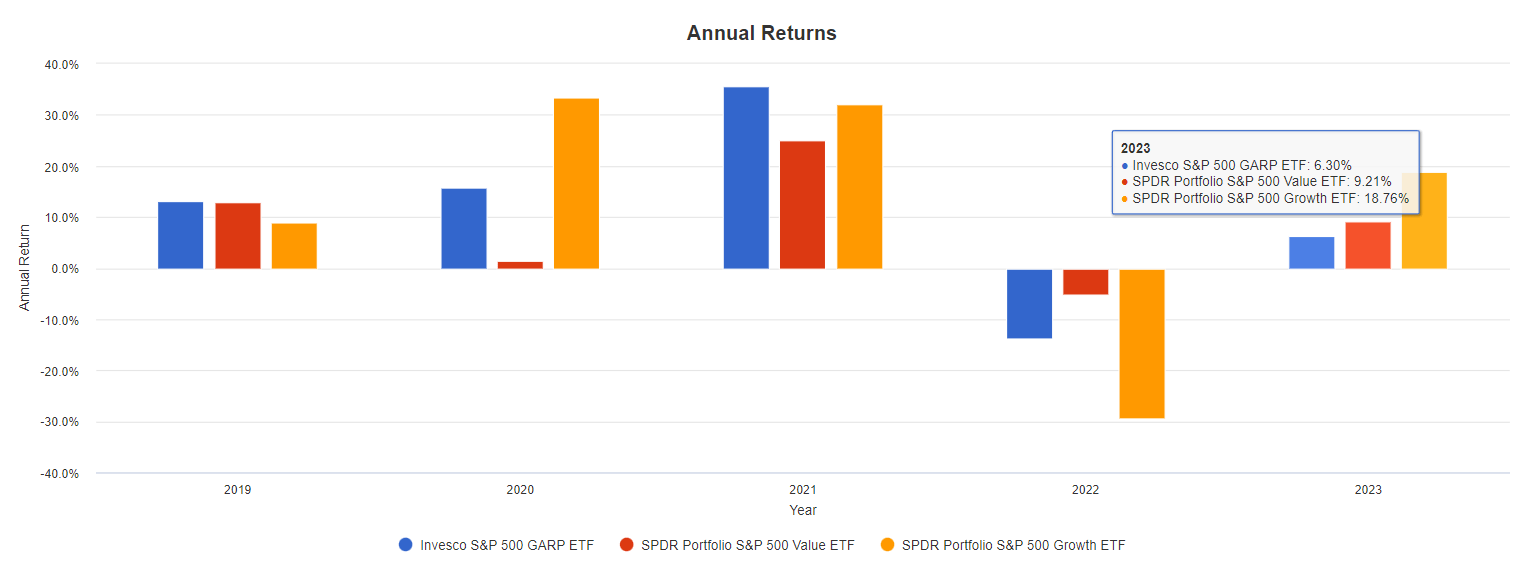

With high turnover, evaluating SPGP's annual returns is also helpful. In the chart below, SPGP outperformed both peers in 2021 but lagged by 3-12% in 2023. It underperformed SPYG by 18% in 2020 but made up that difference last year by outperforming by 16%.

{kind=link}

Portfolio Visualizer

I don't know what to make of these results other than that they are inconsistent. SPGP doesn't necessarily fall between SPYV and SPGP, so unless you consider four years as a sufficient track record, I think SPGP's fundamentals deserve the most consideration.

Investment Recommendation

SPGP substituted more than one-third of its holdings with this month's reconstitution and is now primarily a deep-value, concentrated, and highly volatile ETF. I was surprised by the degree to which estimated and historical growth rates differed among current selections, and I believe only focusing on historical metrics is a design flaw that could exacerbate high turnover in fast-changing markets. It could become an exercise in timing the markets, contrary to most investors' investment objectives. Therefore, I recommend readers avoid buying SPGP today, and I look forward to covering the ETF again at its subsequent reconstitution in December.

For further details see:

SPGP: This S&P 500 GARP ETF Indicates Growth Stocks Are Overvalued