MSGE - Sphere: Trading At A Substantial Discount To TBV

2023-06-15 16:04:26 ET

Summary

- $1.25B of Pro Forma debt - Only $300m associated with Sphere.

- Delays and cost overruns subside as the venue opens in September 2023.

- A state-of-the-art venue in Las Vegas, trading at a substantial discount to replacement cost.

Background

Sphere (SPHR) recently went through a spinoff with MSG Entertainment (MSGE). On April 20, 2023, Sphere Entertainment Co. (hereafter known as Sphere, SPHR, or "the company"), previously known as Madison Square Garden Entertainment Corp., spun off ~67% of MSGE shares to stockholders with Sphere Entertainment retaining approximately 33% of MSGE. SPHR shareholders own MSG Networks, Sphere Entertainment, and 33% of MSGE. We recommend buying SPHR based on the dramatic discount to replacement costs the stock is trading at.

Business Description

The Sphere is a unique, state-of-the-art entertainment venue in Las Vegas, Nevada, with 17,500 seats, 23 VIP suites, and the most advanced sound and highest resolution screen, spanning over three football fields. To go with the incredible picture is a state-of-the-art beam-forming speaker. Utilizing 157,000 ultra-directional speakers and an infrasound haptic flooring system that transmits bass sounds through the floor allows guests to experience music beneath their feet. Additionally, this technology enables the simultaneous delivery of multiple forms of content. Guests sitting in different sections could hear different languages and instruments. The exterior is just as impressive, with 60,000 SF of LED screens. U2 will open the venue, performing 25 shows from September 20 to December 16. The venue will be active up to 365 days per year, sometimes with multiple shows in a day. Smaller events will be able to be run simultaneously with a main event.

MSG Networks (also known as MSGN) is the company's traditional live entertainment business operating two regional sports and entertainment networks, MSG Network and MSG Sportsnet, along with the streaming service MSG GO. In FY 22 , MSGN generated $608m in revenue and $131.5m in Operating income. YTD , MSGN generated $442.8m in revenue and $66.8m in Operating Income (Fiscal Year ends in June).

In addition, the company also owned the TAO Group, a hospitality company delivering culinary and premium entertainment experiences through a portfolio of restaurants, nightclubs, lounges, and daylife venues. On April 17, 2023, SPHR announced an agreement to sell the Tao Group Hospitality for $550m, of which they owned 66.9%. On May 8, the transaction closed , and SPHR received $295m net of accrued management fees and debt repayments.

Thesis

The Sphere construction incurred nothing but problems. Announced in 2018 with a target open in 2021. Covid, project delays, and cost overruns pushed the open date from 2021 to late 2023 and the initial cost from $1.2B to almost $2.3B. With the project almost complete, and a concert scheduled, these delays and cost overruns appear to be in the past. Investors and the market can now focus on the economics of the venue.

The focal point of the thesis revolves around the Las Vegas Sphere. Ticket sales to concerts and events, food and beverage sales, and advertising (including naming rights) are the primary revenue drivers. Coming up with estimates for these segments with no operating history is challenging.

Most MLB, NFL, NHL, and NBA arenas have a title sponsor. For example, AT&T for the Cowboys, Allegiant Field for the LV Raiders, and Metlife for the Giants and Jets Stadium. Below is a list of public stadium naming rights with average annual value. In addition to naming rights, the venue's exterior is a giant LED screen. One can imagine title sponsors of Boxing or UFC fights could pay hefty amounts to display their logo. Given the minimal costs, advertising revenue will have high margins.

| Team/Stadium |

| AAV (In m) |

| LAFC |

| $ 6.7 |

| SOFI Stadium |

| $ 30.0 |

| Allegiant |

| $ 25.0 |

| Empower |

| $ 3.0 |

| AT&T |

| $ 20.0 |

| Metlife |

| $ 19.0 |

| Warriors |

| $ 22.0 |

| Barclays |

| $ 20.0 |

| Citi Field |

| $ 20.0 |

| Steelers |

| $ 10.0 |

| Bengals |

| $ 10.0 |

The market does not like uncertainty. How much more uncertain could one get than a $2.3B property, not opened, with several delays, and $1.1B in cost overruns? Once the model is proven and stabilized, the dramatic discount between the cost to build and the current market value should close.

I recommend watching a few videos to understand this work of art's sheer scale and breadth. U2 opens the Sphere in September, and they did a tour and interview of the venue. You can imagine going to an E-Sport tournament, concert, or other entertainment shows. The difference between your traditional event center space and Sphere is incomparable. Residents in Las Vegas are saying this is another wonder of the world.

Valuation

The stock trades around $27.50 and has ~37m shares outstanding or ~$1B market cap. SPHR has an additional $1.25B of debt and $340m of cash for ~$2B EV. The remaining construction costs are ~$220m. The current cash balance will go toward the final construction costs. Looking at the Q3 Balance Sheet (FY ends June 30), the company reported $326m of cash and $1.85B of debt because the TAO sale occurred after the quarter ended. The 10-Q filing disclosed that the unrestricted cash post-sale was $232m (they must hold ~$110m of restricted cash for construction collateral purposes) and total debt of $1.25B.

In addition to owning the Sphere and MSGN, SPHR holders retained a 33% interest in MSGE. The value of this ownership stake is ~$640m. MSGE is a liquid, publicly traded stock. SPHR also owns other equity/debt investments in Saco Tech, HoloPlot, DraftKings, and TSQ, which are currently on the books for another $93m for a combined value of $733m.

The final part is determining what MSGN is worth. A legacy business, likely in decline, however, has the rights to stream and show Knicks, Rangers, Sabres, and other sports games. In FY22, MSG networks generated $608m in revenues and $131m in Operating income. Through the first three-quarters of FY23, MSGN generated $442m of revenues and $66.9m of Operating income. Revenues are relatively flat. However, operating income was down substantially in Q3 due to higher SG&A costs. The company stated that selling, general and administrative expenses of $60m increased $27.8m compared to the prior year quarter, primarily due to an approximately $44.6m increase in litigation expenses associated with the acquisition of MSG Networks Inc. These one-time expenses should dissipate, returning MSGN to its previously more profitable levels.

Of the $1.25B debt, $950m is a term loan to MSG Networks maturing in 10/2024. This loan is at the MSGN level, not the company level. If MSGN defaults, lenders can only go after the MSGN assets. The sphere assets and equity holdings are remote at different LLCs or parent companies, leaving ~$300m of debt, primarily comprised of the $270m Sphere term loan.

From the latest SPHR 10-Q:

" Guarantors and Collateral. All obligations under the MSGN Credit Agreement are guaranteed by the MSGN Holdings Entities and MSGN LP's existing and future direct and indirect domestic subsidiaries that are not designated as excluded subsidiaries or unrestricted subsidiaries (the "MSGN Subsidiary Guarantors," and together with the MSGN Holdings Entities, the "MSGN Guarantors"). All obligations under the MSGN Credit Agreement, including the guarantees of those obligations, are secured by certain assets of MSGN LP and each MSGN Guarantor (collectively, "MSGN Collateral"), including, but not limited to, a pledge of the equity interests in MSGN LP held directly by the Holdings Entities and the equity interests in each MSGN Subsidiary Guarantor held directly or indirectly by MSGN LP."

If we assume either the company throws the keys or the value of MSGN is roughly the value of the debt, putting the Equity value at $0, we can calculate the implied value of the Las Vegas Sphere.

SPHR Market Value

Stock Price - $27.50

Shares Outstanding – 34,727,000

Market Capitalization - $955m

Sphere Debt - $300m

Payable associated with Sphere construction - $307m

Enterprise Value = ~$1.6B

Assets

Las Vegas Sphere - $2.2B

Equity Investments of $733m

London Land - $65m

Total = $3.1B

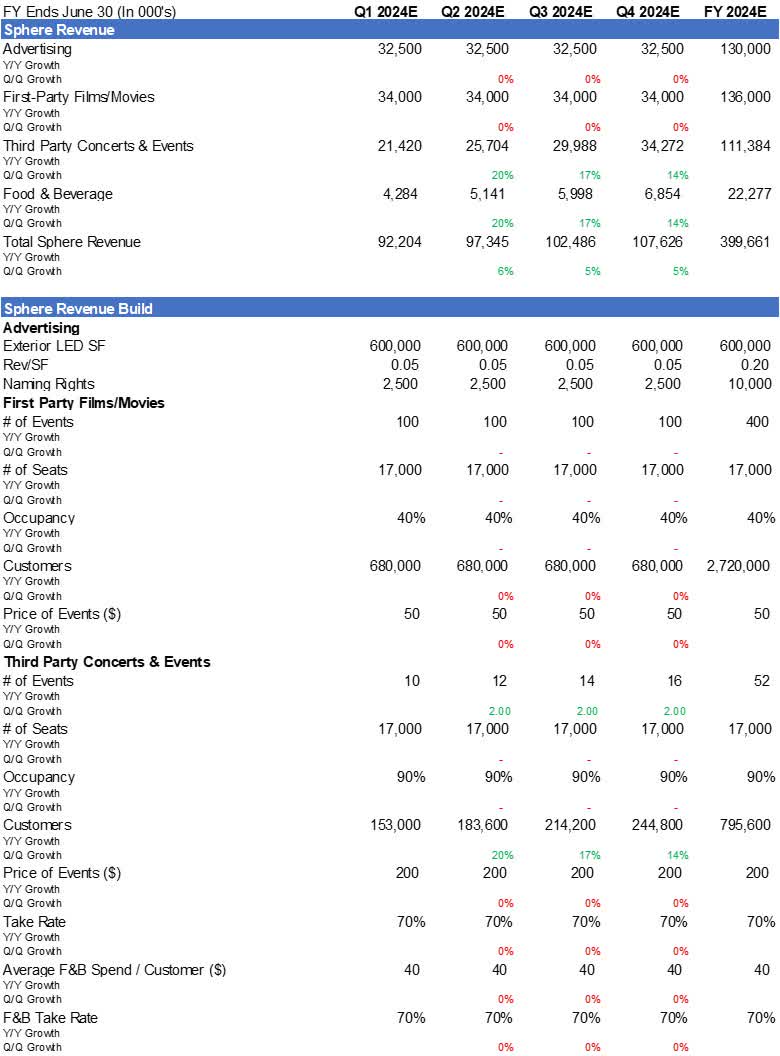

The revenue build below is my best estimate for its first full year of operations. The margin profiles for these segments will be much different, with advertising and naming rights having high margins while Third Party Concerts and Events have lower margins. It would not surprise me if they had 30% EBIT margins on the higher end of comparables Cedar Fair (FUN) and SeaWorld (SEAS). On ~$400m of revenues, they would generate ~$120m of EBIT or an 8.3x EV/EBIT multiple (assuming EV of $1B – Equity Investments & debt net to ~$0). As the property stabilizes, I expect future Revenue, EBIT, and EBIT margins to be higher than in year one.

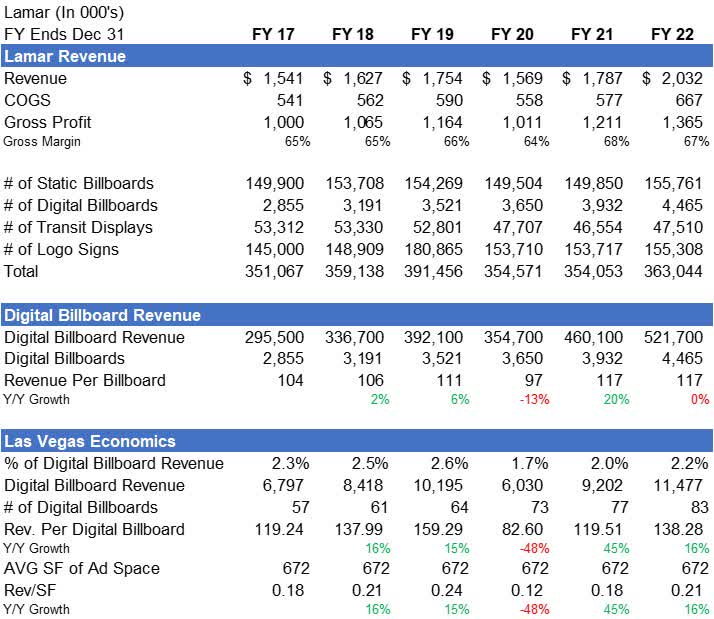

To get a sense of what Advertising revenue could be, Lamar's (LAMR) business model is billboard advertising. Within their filings , they disclose Las Vegas is the highest revenue-generating city for them in the digital billboard space. Using Lamar's Las Vegas digital billboard economics, one can develop a framework for the potential advertising revenue the Sphere LED exterior could generate. The average Lamar billboard is 672 SF. In 2022, Lamar's Las Vegas Billboards generated $11.5m in revenue, equating to $21,000/SF. Two aspects should be considered regarding Sphere's advertising revenue potential. First, Lamar's signs generate revenue every second, whereas the Sphere exterior will not always display an ad. On the other hand, the number of eyes on the Sphere should be multiple of the typical Lamar sign, which is worth more to ad partners. With this give and take, I used 600,000 SF as the potential ad space and slightly under Lamar's 2022 Rev/SF of $21,000 to estimate ~$120m in advertising revenue. Lamar generates ~65% gross margins on their billboards, showing the high margin profile of the business.

SPHR Revenue Build (SPHR & LAMR Filings & Dominick D'Angelo Estimates) Lamar Revenue (LAMR 10-K's)

{kind=link}

{kind=link}

Balance Sheet

The previous two sections briefly mentioned the balance sheet. At the end of Q3 and before the sale of Tao Holdings, SPHR had $1.78 billion of debt, held $327 million of cash, and had $700 million of accounts payable (A/P), with approximately $300 million of that amount being associated with the construction of the Sphere. After the Tao sale, they held $332.7 million in cash, with $232m unrestricted and $110m restricted, while debt amounted to $1.23B. Furthermore, they possessed approximately $733 million in equity investments, of which $650 million was liquid and could be sold at any time. I suspect management will sell the bulk of the MSGE stock over the next few quarters to fund the remaining Sphere construction costs.

The three outstanding loans are the 6.9% MSGN Term Loan maturing in 10/2024, the 7.4% revolver maturing in 06/2027, and finally, the $270m Sphere term loan maturing in 12/2027 baring a 9.27% interest rate. The total yearly interest expense is $92m.

The primary concern is the company's ability to refinance the MSGN debt. Given the rise in interest rates, the 6.9% interest rate will likely increase and may be closer to 9%, depending on the duration.

Risks

SPHR has a dual-class share structure. As of March 31, 2023, James Dolan owns 100% of the company's outstanding Class B shares and approximately 5.5% of Class A, representing approximately 72.4% of the aggregate voting power. Members of the Dolan family are also the controlling stockholders of MSG Sports and AMC Networks Inc., as well as MSG Entertainment. Class B shareholders are entitled to 10 votes per share. Minority shareholders have no say in any decision and are thus at the mercy of the decisions by the Dolans.

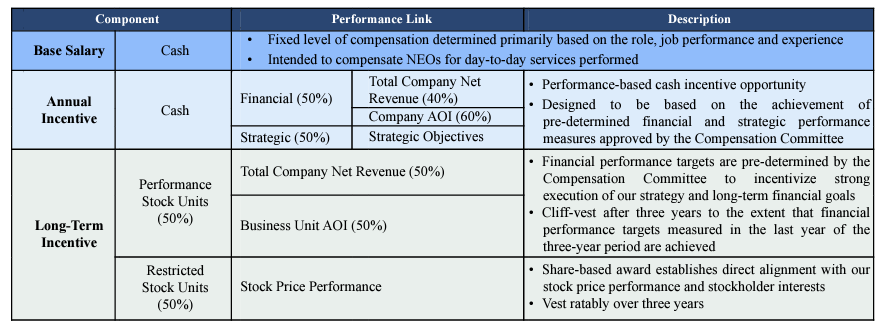

Management Bonus Compensation (MSGE Proxy)

{kind=link}

Management's bonus calculation considers Revenue and AOI (Adjusted Operating Income). Although revenue is a valuable metric, management has the discretion to make several adjustments to the AOI figure. The company excludes Share-Based Compensation (an actual expense), and given the number of financial transactions the company has gone through over the past several years, these "one-time" merger and acquisition expenses have not been one time. I believe one should worry about the liberty management may take when calculating adjusted figures.

Summary

We can purchase a one-of-a-kind asset at a fraction of the construction cost. With the venue slated to open at the end of September, the uncertainty surrounding the economics of the venue is virtually unknown. Management has been very quiet thus far about potential advertising revenues, naming rights, residencies, and event targets. Uncertainty subsides as the venue opens and stabilizes, and the profitability and unique venue experience become known. The stock undeservedly trades at a fraction of its $79 TBV. Depending on the economics of the property, the business is worth a minimum of $50 but likely north of its $79 TBV.

Go Forward KPIs

Not mentioned above, the company owns land in London and is in the process of building a second sphere; however, there is one main difference. Sphere Entertainment is not looking to fund its construction but to partner with a developer or other entertainment company and manage the property. Like the Las Vegas Sphere, the London project has suffered several delays. The London Sphere is still in the permitting stage with no concrete timetable for when a partner or construction will commence.

Advertising and Naming rights - The company should announce the naming rights sometime in 2024.

Number of Shows, Occupancy Rate, and Artist Residency - The profitability of Sphere is driven by the number and occupancy of shows. While movies and films will have lower occupancy rates, high-end shows will determine the ultimate success of the venue. More prominent names will likely perform there if it sells out consistently, leading to higher revenues.

For further details see:

Sphere: Trading At A Substantial Discount To TBV