SAVE - Spirit Airlines: Thank You JetBlue

2023-09-14 12:37:32 ET

Summary

- Spirit Airlines, Inc. faces margin pressure and earnings cuts due to high fuel costs and increased promotions.

- The airline is still set to merge with JetBlue Airways in an all-cash deal.

- Shareholders have nearly 100% upside potential in a $31 all-cash deal, but the stock faces material risk on any failure to close.

After another profit warning from Spirit Airlines, Inc. ( SAVE ), investors are far more happy with the cash deal with JetBlue Airways Corporation ( JBLU ). The ultra low-cost carrier is facing a tough operating environment due to rolling COVID impacts and higher fuel prices. My investment thesis remains ultra Bullish on the stock due to the pending deal, though risks are elevated with the earnings cuts.

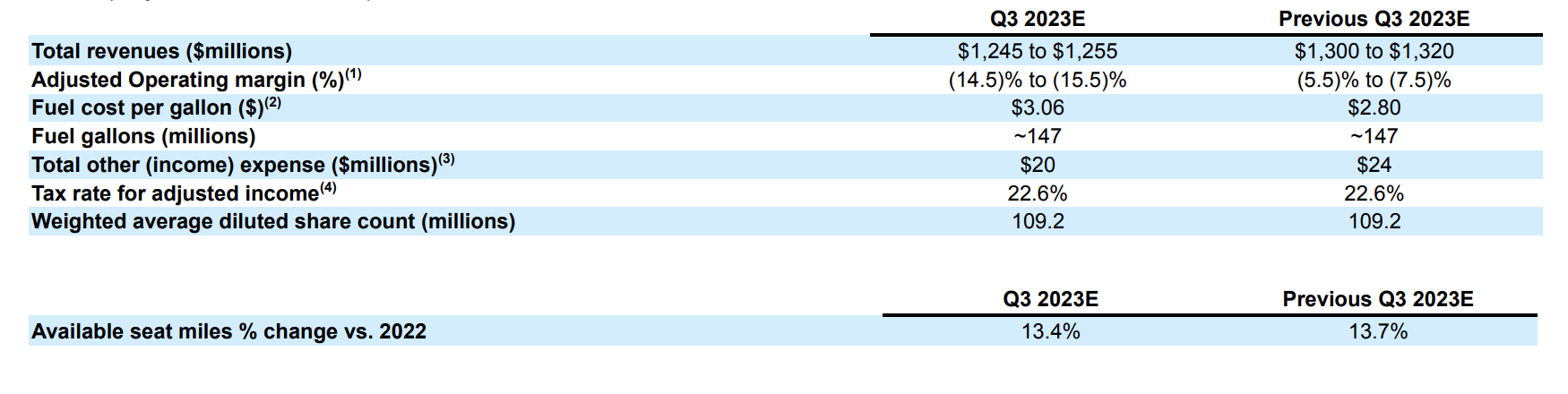

Source: Finviz

Big Margin Pressure

Spirit just slashed Q3 '23 EPS targets to a massive loss as high fuel costs hit hard for an ultra low-cost carrier, or ULCC. At the same time, the airline suggests the revenue side is under pressure due to suddenly heavier promotions.

The legacy airlines aren't facing the same issue with travelers shifting travel to international destinations where ULCCs don't operate. The biggest problem facing Spirit is the shift away from domestic travel as the removal of Covid restrictions have opened up international travel after being shut since early 2020.

The combination leaves Spirit Airlines squeezed in the short term until fares can be adjusted to account for higher jet fuel costs. As well, domestic demand is likely to normalize next year.

The airline is guiding to average jet fuel costs of $3.06 per gallon, up from nearly 10% from prior guidance of $2.80 per gallon. At 147 million gallons consumed, Spirit will spend an additional $38 million on jet fuel without the associated higher fares to subsidize the costs.

{kind=link}

Of course, Spirit has long run into issues where capacity growth causes its own problems. The airline is still forecasting over 14% ASM growth in Q3 and ULCC competitor Frontier Group Holdings ( ULCC ) forecasts at least 20% capacity growth in the quarter while also guiding to a steep lowering of pre-tax margins to losses.

Noticeably, though, Frontier is only guiding to pre-tax margin losses of 4% to 7% versus the guide down to a 15% loss for Spirit Airlines. Last Q3, the airline reported a small profit when fuel prices were equally high.

Merger On Track

Only last week, JetBlue announced an agreement with Allegiant Travel ( ALGT ) to purchase assets at Boston and Newark airports from Spirit. The deal includes 5 gates and ground facilities at Fort Lauderdale's airport.

The move should alleviate some of the Department of Justice's concerns surrounding the deal. The trial is expected to start on October 16.

Assuming JetBlue wins the case, Spirit shareholders will obtain a cash payment of $31.00 when the deal closes in the 1H'24. Investors still obtain the $0.10 monthly payment to wait for the deal to close.

What shouldn't be lost on investors is that the weak results of Spirit help the case that a merger is needed to compete. The DoJ case to block the merger has far more substance when the target company is highly profitable. An unprofitable business model isn't sustainable, and the irony shouldn't go unnoticed.

A few weeks back, documents were leaked where JetBlue plans to hike fares by 40% while removing 24 seats from each of the 200 planes operated by Spirit currently. One can now argue Spirit needs to increase fares in order to return to profits with a forecasted pre-tax margin loss of 15% during the prime Summer travel months.

Of course, the big risk to Spirit shareholders is the deal failing to close. JetBlue has a $70 million breakup fee plus up to $400 million already paid directly to shareholders, but the large losses being racked up by Spirit would likely lead to a materially lower stock price than the current $16.50 level. The upside potential is nearly 100% to shareholders holding onto the stock.

Takeaway

The key investor takeaway is that the deal doesn't appear at risk with JetBlue recently announcing an updated deal with Allegiant on airport assets. The airline executives clearly knew about the ongoing margin pressures at Spirit heading into that additional divestment deal. The merger could still get blocked by the DoJ, but the weak results by Spirit Airlines reduce the case of the regulators.

Spirit is a high risk/reward stock, but investors are still set for a very nice cash payout.

For further details see:

Spirit Airlines: Thank You JetBlue